You Found Your Dream Property in France. The System Between You and the Keys Was Designed for Someone Who Grew Up Inside It.

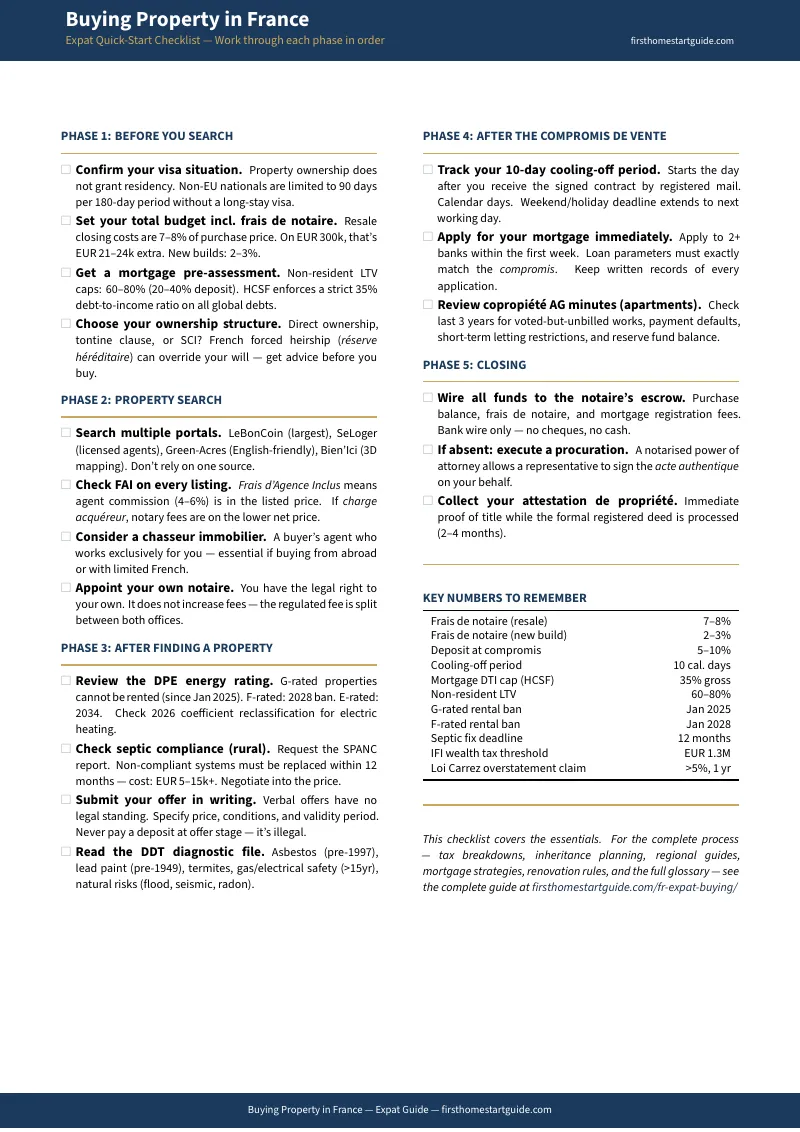

You've found a stone farmhouse in the Dordogne, a sun-drenched apartment in Provence, or a pied-a-terre in the Marais. You've run the numbers, checked the exchange rate, and confirmed you can afford the asking price. So you start the process. Within a week you've learned that closing costs on a resale property aren't 1-2% like back home — they're 7-8%. On a €300,000 house, that's €21,000-24,000 in fees you didn't budget for, payable in full before you receive the keys. The notaire handling the transaction isn't your lawyer — they're a state official whose legal duty is to the French Republic, not to you. And the inheritance law that applies to your new property doesn't care what your will says: French forced heirship gives your children a legally protected share of the house, even if you wanted to leave everything to your spouse.

You search online for help. FrenchEntree publishes beautiful regional guides written by estate agents who earn commission when you buy. Ibanista offers relocation checklists that gloss over the condition suspensive clause — the financing contingency that can cost you your entire 5-10% deposit if you can't produce formal written mortgage rejection letters from multiple French banks within the contractual deadline. The UK government's guide to buying in France hasn't been updated to reflect the DPE rental bans that make G-rated properties illegal to rent since January 2025. And every English-speaking "buyer's agent" in the south of France charges thousands in upfront consultation fees before they've shown you a single property.

Here's the problem no free resource solves: France's property transaction runs on a Napoleonic legal framework where the notaire is neutral, the cooling-off period gives you exactly 10 calendar days to change your mind, the mortgage contingency protects you only if you follow its procedural requirements to the letter, and the inheritance regime can override your estate plan the moment you sign the deed. The process has genuine buyer protections built in — more than most countries — but only if you know they exist, understand their deadlines, and activate them correctly. Miss one procedural step and the protection vanishes.

The Buying Property in France — Expat Guide is The Transaction Blueprint. Not a lifestyle magazine article about finding your dream mas in Provence. It's a structured decision system that decodes every stage of the French property purchase — from the offre d'achat through the compromis de vente, the condition suspensive, the diagnostic dossier, and the acte authentique — so you make each decision understanding the legal mechanism behind it, the deadline attached to it, and the financial consequence of getting it wrong.

What's Inside The Transaction Blueprint

The complete guide plus standalone printable worksheets — covering every stage from property search through key collection, plus fillable tools you print, bring to notaire appointments, and use when reviewing contracts:

The Frais de Notaire Decoder

Closing costs on a resale property in France run 7-8% of the purchase price — but only a fraction of that goes to the notaire. The bulk is droits de mutation (transfer taxes), which vary by department: the standard rate is 5.807%, but since April 2025, departments including Paris, Rhone, and Gironde have raised their share to 6.32%. The guide breaks down every component — departmental tax, municipal tax, state levy, notaire emoluments on the regulated sliding scale, and disbursements — so you know exactly where each euro goes. Including why designating agency fees as charge acquereur (buyer-paid) can reduce your tax base and save hundreds on a single transaction.

The Notaire Playbook

The notaire is not your lawyer. They're a public official appointed by the Ministry of Justice whose duty is to guarantee the legal validity of the transaction and collect state taxes — not to advocate for your interests. Most foreigners don't know that they have the absolute legal right to appoint their own independent notaire, and that doing so costs nothing extra: the regulated fee is simply split between the two offices. The guide explains when you need your own notaire, how to find an English-speaking one, what the dual-notaire structure actually looks like in practice, and the specific contract clauses where having independent representation prevents expensive oversights.

Condition Suspensive Strategy

The compromis de vente requires a 5-10% deposit held in the notaire's escrow account. If your mortgage is declined, the condition suspensive d'obtention de pret protects you — but only if you produce formal, written refusal letters from the required number of lenders within the contractual deadline. French banks are notoriously slow to issue written denials. Fail to collect them in time and you face forfeiture of your entire deposit — potentially €15,000-30,000 on a mid-range property. The guide maps the exact procedural requirements: how many banks must refuse, what the refusal letter must contain, the deadline calculation, and how to build your mortgage application timeline so the contingency actually protects you instead of becoming a trap.

DPE and Diagnostic Dossier Analysis

The seller must provide a Dossier de Diagnostic Technique covering energy performance, asbestos, lead, termites, electrical safety, gas compliance, sanitation, and natural risk exposure. The DPE energy rating now determines whether a property can legally be rented: G-rated properties have been banned from new leases since January 2025, with F-rated banned from 2028. But here's what most guides miss: a government decree effective January 2026 adjusts the electricity conversion coefficient from 2.3 to 1.9, automatically upgrading the ratings of approximately 850,000 electrically heated homes. The guide explains how to check whether a property qualifies for this retroactive upgrade via the ADEME portal, what the small-space bonus means for apartments under 40 square metres, and how to read each diagnostic report for the red flags that indicate renovation costs the asking price doesn't reflect.

The Inheritance Shield — Forced Heirship, SCI, and Brussels IV

French succession law applies a regime of reserve hereditaire: your children are entitled to a legally protected share of any French property you own, regardless of what your will says or where you're domiciled. For one child, the reserved portion is 50%. For two children, two-thirds. For three or more, three-quarters. This means your surviving spouse could be forced to share ownership of the family home with your children — or sell it to satisfy their claims. The guide covers three structural solutions: the tontine clause that makes the surviving partner retroactively the sole owner from the date of purchase, the SCI (Societe Civile Immobiliere) that converts real property into company shares governed by the SCI's own statutes, and the Brussels IV regulation that allows EU property owners to elect the succession law of their nationality instead of French law. Each option has different tax consequences, formation costs, and limitations — the guide compares them side by side so you choose the right structure before you sign the deed, not after a death forces the issue.

Non-Resident Mortgage Navigator

Non-resident buyers face a deposit requirement of 20-30%, rising to 40% for self-employed or non-EU applicants. The HCSF enforces a hard 35% debt-to-income cap on all French mortgages, calculated on gross taxable income including all existing global debt obligations. Interest rates for non-residents in 2026 run 3.50-4.25% for a 20-year fixed term — a premium of 0.4-0.65% over resident rates. The guide covers which French banks actively lend to non-residents (BNP Paribas, Credit Agricole, Societe Generale, BRED), the difference between a hypotheque and the cheaper IPPD lien, the mandatory 10-day reflection period on mortgage offers under the Loi Scrivener, and how to structure your application timeline so your financing approval arrives before the condition suspensive deadline expires.

Coproprietaire Survival Guide

Buying an apartment means entering a copropriete — a commonhold where you own your private lot plus a percentage of the building's common elements. The syndic manages the building, the annual assemblee generale votes on works and budgets, and any exterior modification requires co-owner approval that can delay renovations by a year. In Paris, the 2024 Bioclimatic PLU adds environmental restrictions on facade work and extensions. The guide covers how to read the copropriete accounts before purchase, what the carnet d'entretien reveals about deferred maintenance, how to interpret the three-year works plan, and the financial red flags in the charges de copropriete that signal a building heading toward a special assessment.

Rural Purchase Playbook — PLU, SAFER, and Renovation Rules

Buying a barn, a farmhouse, or rural land introduces three complications that urban purchases avoid. The Plan Local d'Urbanisme dictates whether your property sits in an agricultural zone where residential conversion may be prohibited. SAFER — the agricultural development body — holds a statutory right of pre-emption that can delay your transaction by two months while they decide whether to exercise it. And if your renovation increases habitable floor area beyond 150 square metres, French law requires you to hire a registered architect. The guide covers how to check PLU zoning at the mairie before making an offer, what triggers a SAFER notification, the two-month neighbour contestation window after you display your planning board, and the breathable insulation requirements for stone properties that prevent the moisture damage caused by modern materials.

Who This Guide Is For

This guide is for foreign buyers and expats purchasing property in France who:

- Are buying their first French property and need the entire transaction mapped — from the written offer through the compromis de vente, the 10-day cooling-off period, the diagnostic dossier, mortgage approval, and the acte authentique signing at the notaire's office — so they understand what happens at each stage, what it costs, and what can go wrong

- Have found a property they want to make an offer on and need to know, before they sign anything, whether to appoint their own notaire, how much the frais de notaire will actually cost, and what the condition suspensive requires them to do if their mortgage application is declined

- Are American, British, Australian, or Canadian and assume their home-country will covers their French property — and need to understand forced heirship before their children inherit a legally protected share of the house they intended to leave entirely to their spouse

- Are buying for rental income and need to verify the property's DPE rating before signing a compromis on a property that is or will become illegal to rent — including how to check the January 2026 electric reclassification that could upgrade the rating without any physical renovation

- Are considering a rural renovation and need to know whether the PLU allows residential use, whether SAFER will pre-empt the sale, and what the architect requirement and planning contestation window mean for their timeline and budget

- Want every transaction cost, every legal deadline, and every procedural requirement in one document — so they walk into notaire appointments, mortgage meetings, and property viewings with the same structural understanding as a French buyer, not the surface-level confidence of someone who read a lifestyle blog

Why Not Free Resources?

Free information on buying property in France as a foreigner is abundant. Here's what each source actually delivers:

- FrenchEntree publishes detailed regional guides with genuine local knowledge — written and sponsored by estate agents, mortgage brokers, and relocation companies who earn commission when you buy. Their advice to "trust your notaire" is technically sound, but it never explains that the notaire represents the state, not you, and that appointing your own costs nothing extra. The information is real. The financial incentive behind every recommendation is too.

- Ibanista offers a structured buying-in-France guide aimed at Americans. It covers the basics clearly and links to useful French government resources. What it doesn't cover: the condition suspensive procedural trap, the DPE rental bans and the January 2026 electric reclassification, copropriete financial analysis for apartment purchases, or the comparative tax treatment of SCI versus tontine versus Brussels IV election. It gets you oriented. It doesn't get you through the transaction.

- UK Government's guide to buying property abroad covers France in a few paragraphs of general advice — "take independent legal advice," "understand the local tax system" — without mentioning a single specific French mechanism. It was written before the DPE rental bans took effect and doesn't reference the post-April 2025 transfer tax increases. It's a liability disclaimer formatted as guidance.

- Expat forums (Survive France, France Forum, Reddit r/expats) contain real stories from real buyers — alongside advice that was accurate in 2023 but pre-dates the DPE reform timeline, the departmental tax increases, and the electric reclassification decree. You'll find someone who completed with one notaire and was fine, and someone who lost their deposit because they didn't understand the condition suspensive deadline. Both stories are true. Neither tells you which outcome applies to your situation.

- English-speaking buyer's agents offer professional representation — for fees of €3,000 to €10,000 or 2-3% of the purchase price. The good ones are worth it. But their pitch starts with "the process is too complicated to do alone" — which is true only if you don't understand the process. Understanding the process is what this guide provides.

This guide fills the structural gap — the space between knowing that France has a notaire system and understanding exactly how that system works at each stage, what protections it offers, what deadlines it imposes, and what happens to your money when you miss one. It's the analysis an independent advisor with no products to sell or commissions to earn would give you, structured as a permanent reference you own.

— Less Than One Hour of a Buyer's Agent's Time

A buyer's agent charges €3,000 to €10,000. A notaire's frais on a €300,000 property run €21,000-24,000. The condition suspensive deposit you're protecting is €15,000-30,000. A single DPE-related rental ban you didn't know about can make an investment property worthless overnight.

This guide doesn't replace your notaire or your mortgage broker. But it gives you the frais de notaire breakdown, the condition suspensive strategy, the inheritance structure comparison, the DPE analysis, and the transaction timeline that ensure you walk into every appointment, every viewing, and every contract signing understanding the mechanism behind each step — instead of discovering how French property law works by losing money to it.

If it prevents a single condition suspensive deposit forfeiture, catches a single DPE rental ban before you sign the compromis, or identifies the inheritance structure that protects your spouse, it pays for itself before you've finished reading it.

30-day money-back guarantee. If the guide doesn't make the French property transaction clearer and your financial position stronger, you pay nothing.

Download the free Quick Checklist to see the step-by-step action plan covering frais de notaire calculation, notaire selection, DPE verification, and the compromis de vente timeline. When you're ready for the full Transaction Blueprint — complete with condition suspensive strategy, inheritance structure comparison, mortgage navigator, and copropriete analysis — the complete guide is here.

You've found the property. Now decode the system that stands between you and the keys.