You Qualified for the Home Buyer Concession Scheme. Three Years Later, the ACT Revenue Office Data-Matched Your ATO Returns, Found Your Partner's Income Pushed You $4,200 Over the Threshold, and Sent You a Bill for $35,238 Plus 12.42% Compounding Interest From the Date of Settlement.

You found a two-bedroom unit in Gungahlin for $580,000. You checked the HBCS thresholds. Your income was well under $250,000. You self-assessed, your conveyancer filed the concession, and you paid zero stamp duty at settlement. You moved in, decorated, started repaying the mortgage.

Then, two and a half years later, a Notice of Reassessment arrives from the ACT Revenue Office. They have matched your self-assessment against ATO tax returns and discovered that your de facto partner's salary — the one you assumed was not relevant because you were not married and not on the same title — pushed total household income to $254,200. Four thousand two hundred dollars above the threshold. The reassessment demands the full conveyance duty of $19,400, plus compounding simple interest at 12.42% per annum backdated to the date of settlement, plus a penalty of up to 25%. The total exceeds $28,000 — for a $4,200 oversight you did not know you were making.

Or you qualified cleanly on income, but your employer deployed you interstate for a four-month secondment eight months after settlement. When the data-matching audit runs, the Revenue Office determines you failed to maintain twelve months of continuous occupancy as your principal place of residence. The strict liability framework has no administrative discretion for APS deployments, health crises, or relationship breakdowns. You owe the full duty, the interest, and the penalty.

Here's what no single free resource in Canberra explains: the ACT layers a means-tested concession scheme with retrospective data-matching audits that spiked 191% in 2023–24 against a 99-year Crown lease system where you never own the land against a 20-year tax reform replacing stamp duty with escalating annual rates against the legacy of Mr Fluffy loose-fill asbestos in over 1,000 established homes against a Land Rent Scheme with annual income reviews and a conversion trap that erases years of rent payments. Each of these has cost real Canberra buyers tens of thousands because the information existed — scattered across Revenue Office circulars, Auditor-General reports, Crown lease registers, ACAT rulings, and panicked Reddit threads on r/canberra — but nobody had assembled it into a single defensive framework calibrated to how the ACT actually works in 2026.

The Australian Capital Territory First Home Buyer Guide is a Concession Audit Defence System — not a generic overview of buying your first home, but a structured reference that maps every ACT-specific regulation, concession trap, lease mechanic, and environmental hazard into a process you work through before your offer is signed. It replaces months of cross-referencing Revenue Office factsheets, Auditor-General findings, EPSDD lease registers, Access Canberra databases, and Whirlpool threads with a single guide that tells you exactly what to verify, exactly how the audit works, and exactly where buyers in this territory lose money.

What's Inside the Concession Audit Defence System

A comprehensive guide, a quick-start checklist, and 8 standalone worksheets and reference cards (10 PDFs) — covering every stage from pre-approval through post-settlement compliance, built specifically for the regulations, concession schemes, lease mechanics, and environmental hazards that make the ACT unlike any other Australian jurisdiction:

HBCS Eligibility and Audit Defence Playbook

The Home Buyer Concession Scheme saves you up to $35,238 in stamp duty — and the ACT Revenue Office uses retrospective ATO data-matching to claw it back if you get the rules wrong. The guide covers the full 2025–26 income thresholds by dependant count ($250,000 base scaling to $273,000 for five or more children), the zero-duty band up to $1,020,000, the concessional taper zone to $1,455,000, and the three most common audit triggers: de facto partner income inclusion, First Home Super Saver withdrawals reclassified as taxable income, and occupancy breaches from interstate deployments. It details how ACTRO's data-matching process works — cross-referencing ATO tax returns, superannuation withdrawal records, and rental bond databases — the 12.42% compounding interest and 25% penalty structure, and a step-by-step evidentiary framework for documenting continuous occupancy so your file survives the audit that may come two to four years after settlement.

Crown Lease System Decoded

Every parcel of residential land in the ACT is owned by the Commonwealth. When you buy a property in Canberra, you acquire a 99-year Crown lease — not freehold title. The guide explains what this means in practice: how purpose clauses restrict subdivision and secondary dwellings, how to have your conveyancer evaluate the lease before you make an offer, how the Lease Variation Charge works if you want to change the permitted use, how banks assess Crown leases for lending (and the minimum remaining term they require), and what happens when unregistered leases in new developments create a timing gap between contract exchange and finance drawdown. It covers lease renewal on expiry — straightforward and nominal — and the ACAT appeals process when a variation is refused.

Mr Fluffy Asbestos Due Diligence Framework

Between 1968 and 1979, a Canberra contractor installed loose-fill amosite asbestos insulation into over 1,000 homes. Unlike bonded asbestos in fibro sheeting, loose-fill asbestos is friable and migrates into living spaces. A standard building and pest inspection will not reliably detect it. The guide walks you through checking the Affected Residential Premises Register under the Dangerous Substances Act 2004, interpreting the difference between eradicated blocks (demolished, soil remediated, resold) and properties with active Asbestos Management Plans, how banks view remediated blocks for lending, and the Purchaser of Last Resort and Request for Acquisition pathways. It also addresses the persistent anxiety about soil contamination on remediated blocks in suburbs like Lawson — giving you a framework to assess risk rather than avoid entire postcodes.

The 20-Year Tax Transition Modelled

Since 2012, the ACT has been replacing stamp duty with annual land tax through progressively higher general rates. The HBCS eliminates your upfront duty — but your annual rates will be significantly higher than equivalent properties in other states, and they compound over time. The guide models this trade-off over 5, 10, and 20-year holding periods so you can budget accurately for the total cost of ownership. It explains the NATSEM microsimulation finding that lower-income households can spend up to 5.91% of income on rates under the new system — a critical nuance for buyers near the HBCS income threshold who are budgeting to the limit.

Land Rent Scheme Deep Dive

For buyers under $160,000 household income who cannot raise a full deposit, the Land Rent Scheme separates land cost from construction cost. The guide covers the 2% discounted annual rent rate, the mandatory CIT information session, the annual income review and two-year loss-of-eligibility trigger, and the conversion trap that catches buyers who assume past rent accrues as equity. When you convert to a standard Crown lease later, you pay the current market value — not the historical value from when you entered the scheme. If land values have risen 30% over five years, your conversion costs 30% more than you originally planned.

Federal Scheme Stacking Strategy

The First Home Guarantee (5% deposit, no LMI), First Home Super Saver Scheme, and HBCS can all be combined — but the interaction between FHSS withdrawals and the HBCS income threshold is the single most common audit trigger. The guide details the exact tax treatment of FHSS voluntary contributions on withdrawal, how this amount flows into your ATO gross income figure, and how to time withdrawals and structure contributions so you do not accidentally push household income above the threshold and lose a $35,000 stamp duty exemption to save $2,000 in deposit accumulation.

Three Worked Cash-to-Close Scenarios

Complete acquisition cost breakdowns for a $650K unit in Gungahlin (full HBCS exemption plus First Home Guarantee), an $850K house in Belconnen (within the HBCS concessional band), and a $1.1M house-and-land package in a new estate (above HBCS threshold, using Land Rent). Every dollar mapped: deposit, conveyance duty or concession, conveyancing fees, building inspections, pest inspections, asbestos assessments, title search fees, rates clearance certificates, PEXA settlement fees, and Crown lease registration.

Suburb Entry Point Analysis

Current median prices across Canberra's districts — Gungahlin units from $405K, Belconnen from $471K, Charnwood houses from $615K, Banks from $750K — mapped against HBCS property value thresholds and transport connectivity to the Parliamentary Triangle, Russell, and major APS hubs. The guide covers the bifurcation in buying behaviour: affordable units in town centres versus detached housing in outer suburbs, and which entry points keep you within the zero-duty HBCS band.

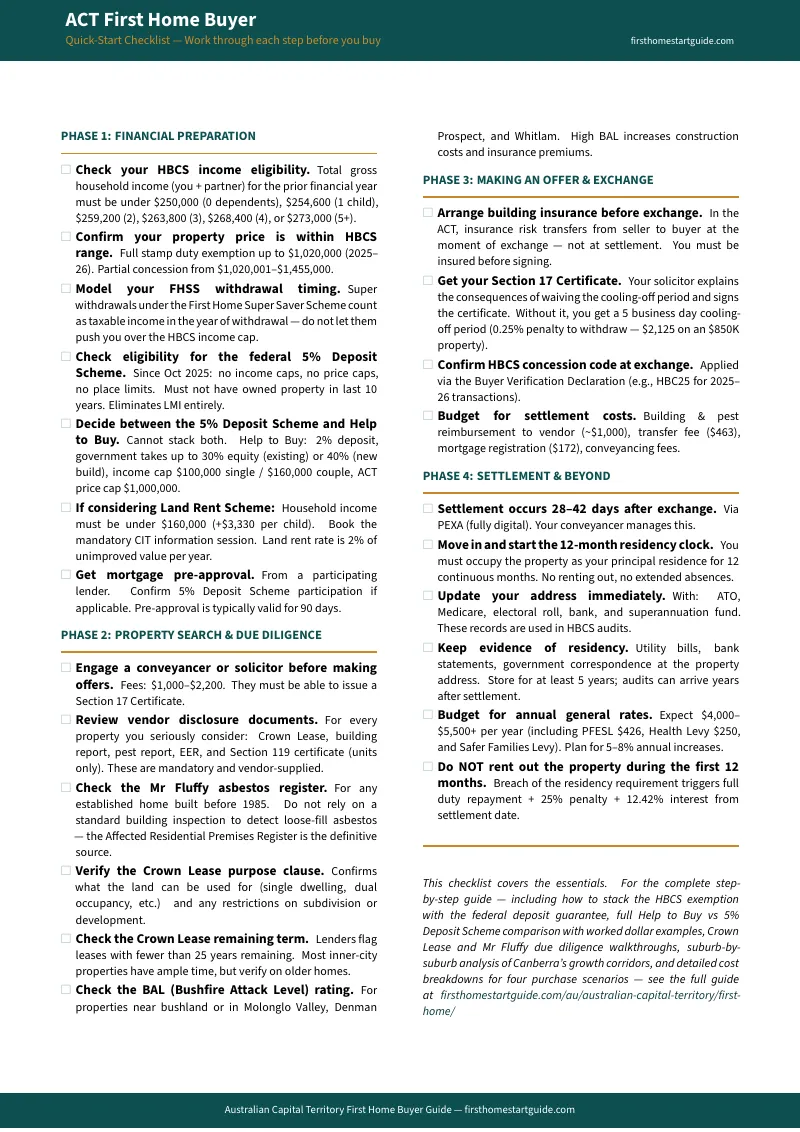

20-Item Quick-Start Checklist

A structured checklist covering four phases — pre-approval, due diligence, settlement, and post-purchase compliance — with every ACT-specific verification step. Items include HBCS income threshold calculation, Crown lease purpose clause review, Mr Fluffy register search, asbestos assessment booking, conveyancer engagement timing, barrier-free duty payment, PEXA settlement, and the 12-month occupancy evidence trail that protects your concession.

8 Standalone Worksheets and Reference Cards

Print-ready tools you can bring to your conveyancer, mortgage broker, or CIT session:

- HBCS Eligibility Calculator — income threshold tables by dependant count, property value bands, duty savings at each tier, and common income items that catch buyers (FHSS withdrawals, overtime, de facto partner income)

- Crown Lease Purpose Clause Checklist — what to ask your conveyancer to verify before making an offer, permitted use categories, and Lease Variation Charge implications

- Mr Fluffy Due Diligence Checklist — register search process, eradicated versus managed property classification, questions for your building inspector, and lending implications

- ACTRO Audit Evidence Tracker — month-by-month log for documenting continuous occupancy during the 12-month requirement, with evidence types the Revenue Office accepts

- Cash-to-Close Worksheet — three worked scenarios plus a blank fillable version for modelling your own purchase with every ACT-specific line item

- Land Rent Scheme Comparison Calculator — side-by-side modelling of traditional purchase versus Land Rent over 5, 10, and 15 years, including conversion cost at projected land value growth rates

- Settlement Timeline Planner — day-by-day planner from contract exchange through cooling-off, building inspections, finance approval, PEXA settlement, and Crown lease registration

- Property Inspection Checklist — ACT-specific items including Crown lease verification, asbestos assessment, Energy Efficiency Rating, and Unit Title records for apartments

Who This Guide Is For

This guide is for first home buyers in the Australian Capital Territory who:

- Qualify or may qualify for the Home Buyer Concession Scheme and need to protect that eligibility through settlement and the 12-month occupancy period — including understanding exactly what counts as household income, how de facto partner earnings are assessed, and what happens if life circumstances change before the occupancy requirement is met

- Are buying in Canberra for the first time and need to understand the Crown lease system — especially buyers from interstate who assume ACT property works like freehold, and buyers looking at large blocks who want to know whether subdivision or a secondary dwelling is possible under the existing purpose clause

- Are searching established suburbs and need a practical framework for Mr Fluffy asbestos due diligence — not just "check the register" but how to evaluate remediated blocks, active Asbestos Management Plans, and the lending implications for each

- Are dual-income APS, defence, or university households near the HBCS income threshold who need to model exactly how overtime, superannuation withdrawals, and salary sacrifice interact with the eligibility calculation

- Are weighing the Land Rent Scheme against a traditional purchase and need to understand the long-term financial implications — including the annual income review, the two-year eligibility loss rule, and the conversion cost trap

- Want to combine the First Home Guarantee, First Home Super Saver Scheme, and HBCS without accidentally breaching income thresholds that trigger a retrospective reassessment

- Want every ACT-specific regulation, concession rule, lease mechanic, and environmental hazard in one reference — instead of assembling it from Revenue Office factsheets, Auditor-General reports, EPSDD databases, and Reddit threads from buyers who already paid the penalty

Why Not Free Resources?

Free information on buying a first home in the ACT exists. Here's what it actually delivers:

- ACT Government websites publish the HBCS eligibility criteria and application forms. The 2026 Auditor-General explicitly found they fail to effectively communicate the complex requirements, the interaction between income sources, and the audit consequences of non-compliance. The information is siloed across the Revenue Office, the Environment and Planning Directorate, and Access Canberra. You get the rules without understanding how they interact — and the interaction is where buyers lose $35,000.

- Mortgage broker blogs (Loan Market Canberra, Beyond Bank) provide 6-step overviews of the buying process. They outline deposit organisation and pre-approval basics. They deliberately stop before compliance advice because they are lead-generation content for mortgage applications, not defensive guides for surviving a government audit three years after settlement.

- National first home buyer guides (Canstar, realestate.com.au, Domain) assume freehold title, standard stamp duty, and a First Home Owner Grant. The ACT has none of these. Applying their advice in Canberra means budgeting for a grant that does not exist, ignoring the Crown lease mechanics that restrict your property rights, and missing the tax transition that will increase your annual holding costs every year for the next decade.

- Reddit (r/canberra) and Whirlpool threads contain genuine buyer panic — people posting about $50,000 reassessment demands, confusion over whether their partner's income counts, terror about Mr Fluffy properties three streets from the house they are about to sign on. The experiences are real, but the advice is fragmented, often out of date, and spread across hundreds of threads. Sorting 2026 law from 2019 advice takes longer than reading a guide that has already done it.

This guide fills the ACT-specific gap — the space between knowing how to buy a first home generally and knowing how to buy in a territory where you never own the land, where the First Home Owner Grant was abolished seven years ago, where concession scheme audits spiked 191% in a single year, where over 1,000 homes contained loose-fill asbestos, and where stamp duty is being systematically replaced with escalating annual rates. It is the analysis that would take an ACT conveyancer, a tax accountant, an asbestos assessor, and an ACTRO compliance specialist to assemble — structured as a reference you own permanently.

— Less Than One Session With a Canberra Conveyancer

A Canberra conveyancer charges $1,200 to $2,500 for a standard residential transaction. A specialist asbestos assessment on a suspect property runs $400 to $800. Failing an HBCS audit triggers the full conveyance duty — up to $35,238 — plus compounding interest at 12.42% per annum from the date of settlement, plus penalties of up to 25%. A single reassessment demand can exceed $50,000. Discovering a Crown lease purpose clause restriction after settlement means applying for a Lease Variation — a process with no guaranteed outcome and a Lease Variation Charge that can run into tens of thousands.

This guide does not replace your conveyancer or your mortgage broker. But it gives you the HBCS audit defence framework, the Crown lease evaluation protocol, the Mr Fluffy due diligence checklist, the tax transition model, the federal scheme stacking strategy, and the worked cash-to-close scenarios that ensure you identify every ACT-specific risk before your cooling-off period expires — instead of discovering them on a Notice of Reassessment two years after you moved in.

If it catches a single income threshold miscalculation, prevents a single occupancy compliance breach, or flags a single Crown lease restriction before you sign, it pays for itself before you have finished reading it.

30-day money-back guarantee. If the guide does not protect your purchase and clarify the ACT's unique regulatory environment, you pay nothing.

Download the free Australian Capital Territory Quick-Start Home Buying Checklist to see the 20-item action plan covering pre-approval, due diligence, settlement, and post-purchase compliance. When you are ready for the full HBCS audit defence playbook, Crown lease evaluation framework, and Mr Fluffy due diligence system, the complete guide is here.

The numbers work on the borrowing calculator. This guide tells you whether the ACT agrees.