You Found the Perfect House. Then You Googled the Flood Zone.

The listing looked great. The price was right. You drove by twice. You started imagining your furniture in the living room. Then you noticed the tiny line in the disclosure: "Property located in Special Flood Hazard Area, Zone AE." Or your lender flagged the wildfire severity zone. Or you pulled up the FEMA map and the entire lot was colored blue.

So you did what everyone does. You googled it. And you got a Reddit thread where half the people said walk away and half said their house has been in a flood zone for 20 years with no problems. Your agent said "people buy in flood zones all the time." Your insurance broker quoted you $6,200 a year but could not tell you what it would be in year three. The seller's disclosure said "no prior flooding" but the FEMA map says the house sits three feet below the Base Flood Elevation.

You are now making a 30-year financial decision with information that contradicts itself at every turn. Your agent earns a commission when the deal closes. Your insurance broker earns a commission when a policy binds. The seller wants the highest possible price. None of these people will sit down with you and run the actual math on what this hazard zone costs you over the life of the mortgage --- and every free resource online gives you either outdated government maps, anecdotal forum advice, or insurance quotes with no context on how fast they will escalate.

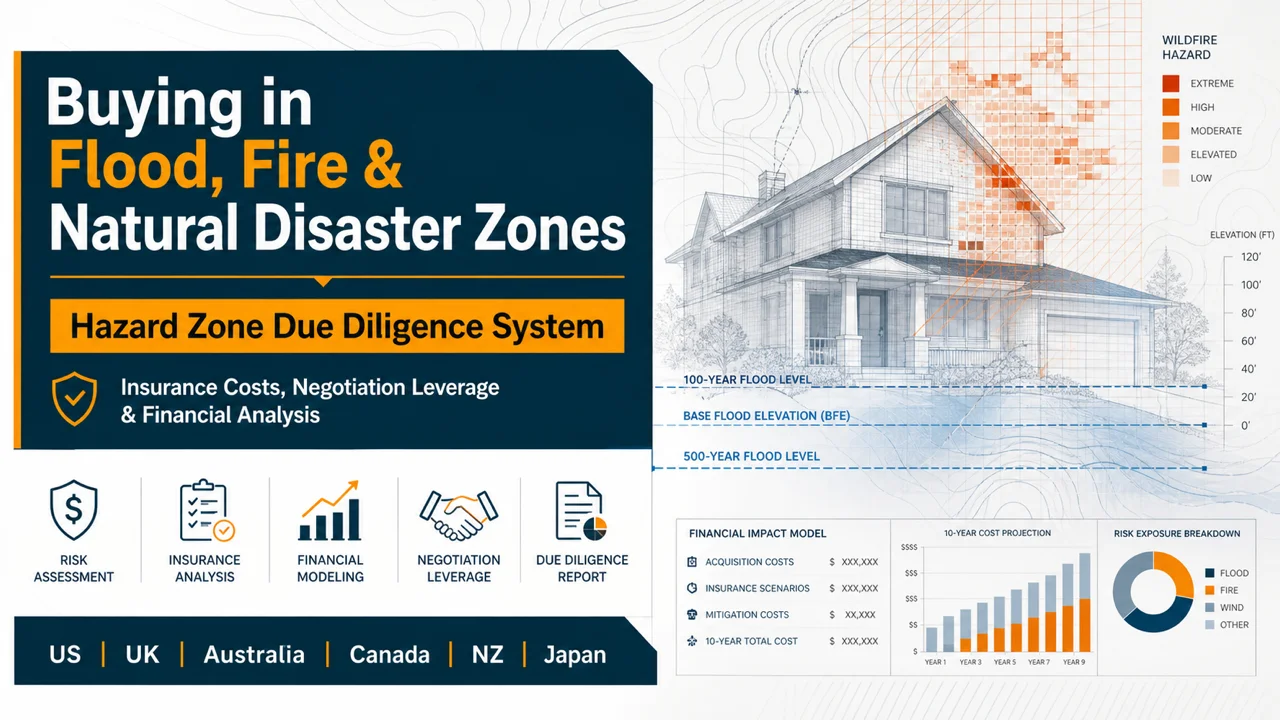

The Buying in Flood, Fire & Natural Disaster Zones guide is a Hazard Zone Due Diligence System --- a structured framework that replaces guesswork with the actual financial math, insurance mechanics, disclosure requirements, mitigation costs, and negotiation leverage for buying any property in a flood zone, wildfire zone, earthquake zone, hurricane corridor, or cyclone-prone area. It covers the United States, the United Kingdom, Australia, Canada, New Zealand, and Japan in detail. The principles apply everywhere.

What's Inside the Hazard Zone Due Diligence System

A 45-page guide, a quick-start checklist, and 7 standalone reference cards and worksheets --- organized by the exact question you are trying to answer right now. Print the reference cards and bring them to property viewings, insurance broker meetings, and negotiations:

Hazard Zone Classifications Decoded

Your lender said "Zone AE" and your agent said "it's not a big deal." The guide explains every US flood zone (AE, VE, A, AO, X shaded, X unshaded), California wildfire severity zones (Moderate, High, VHFHSZ), Australia's Bushfire Attack Level ratings (BAL-LOW through BAL-FZ), and seismic classifications for New Zealand and Japan. Each classification comes with what it means for your insurance obligations, your mortgage terms, your building restrictions, and your future resale value. Not a glossary --- a financial impact assessment for each designation.

Insurance Realities Nobody Tells You

A flood insurance quote means nothing without understanding what happens to it in year two. The guide walks you through FEMA's Risk Rating 2.0 pricing model (why two houses on the same street can have wildly different premiums), the California FAIR Plan coverage gap (it does not cover theft, liability, water damage, or additional living expenses --- your lender will not accept it alone), how to structure a Difference in Conditions wrap policy, the wind-versus-water coverage gap in hurricane zones, and the Anti-Concurrent Causation clause that lets insurers deny your entire claim after a storm. It explains force-placed insurance --- the lender's power to bind a policy at double or triple the market rate if your coverage lapses --- and why the seller's current premium tells you almost nothing about what yours will be.

Structural Mitigation and Home Hardening

Insurance premiums are a symptom. The underlying condition is the structure's vulnerability. The guide covers what structural upgrades exist for each hazard type, what they actually cost, and which ones permanently reduce your premiums versus which ones the insurance industry does not yet reward. Foundation flood vents, house elevation, defensible space clearing, ember-resistant construction, seismic bracing, wind-mitigation retrofits, the Florida My Safe Florida Home grant program, California AB 38 defensible space requirements, and Australia's BAL compliance cost ranges from $13,000 to over $69,000 depending on the rating.

Financial Due Diligence Framework

The property is discounted because of the hazard zone. But is the discount large enough to offset the carry costs? The guide gives you the True Cost of Ownership calculation --- purchase price plus all insurance premiums, annual mitigation maintenance, amortized upfront mitigation costs, and deductible exposure over your holding period. It includes a stress test at 15% annual premium escalation over 10 years. It explains the FEMA 50% Rule (if renovation costs exceed 50% of the structure's pre-disaster value, you must bring the entire structure into current code compliance). And it shows you how to build a 30-year carry cost model that reveals whether the deal actually makes financial sense.

Negotiation Strategies

Hazard zone status is not just a risk --- it is leverage. The guide shows you how to capitalize the insurance premium differential into a lower purchase price (if the property costs $4,000 more per year to insure than a non-hazard alternative, that is $40,000+ over a 10-year holding period). It covers the Elevation Certificate as your primary negotiation tool, the assumable NFIP policy loophole that lets you inherit the seller's lower historical rate, why you should never ask for pre-paid insurance premiums as a concession (premiums are only guaranteed for 12 months --- the seller's concession evaporates when rates jump), and how to demand structural mitigation as a permanent concession instead.

Disclosure Requirements by Jurisdiction

What sellers are legally required to tell you --- and what they can legally hide --- varies dramatically by state and country. The guide covers California's Natural Hazard Disclosure Statement, Florida's hurricane and flood zone seller disclosures, New Zealand's statutory vendor disclosure requirements including the Deed of Assignment for seismic claims, Japan's building standards disclosure system, and the UK and Australian equivalents. It flags the specific items that sellers routinely omit or downplay because the law does not explicitly require them.

The Decision Framework

After you have done the research, run the math, and gathered the quotes, you need a clear decision framework. The guide provides the specific conditions under which you should walk away --- an uninsurable property in the private market where the insurer of last resort quotes premiums that make the deal unworkable, required structural modifications that are physically or legally impossible, or a True Cost of Ownership that exceeds a comparable non-hazard property by more than the purchase discount. It also covers the conditions under which hazard zone properties can be excellent purchases --- when the premium differential is manageable, the mitigation path is clear, and the purchase discount exceeds the capitalized carry cost.

Who This Guide Is For

- Buyers who just discovered their dream house is in a flood zone and need to understand what that actually costs before their contingency window closes --- not anecdotes from Reddit, not a vague reassurance from their agent, but the financial math with real numbers

- Buyers in wildfire-prone California whose insurance carrier just pulled out of their area and need to understand the FAIR Plan, DIC wrap policies, and the dual-premium structure before they commit to a purchase that could cost $15,000+ per year to insure

- Buyers in hurricane and cyclone corridors who need to understand the wind-versus-water coverage gap, wind mitigation credits, and how to structure insurance before a storm turns a coverage dispute into a total loss

- Buyers considering properties in earthquake zones (California, New Zealand, Japan) who need to understand seismic insurance deductibles, building standard classifications, and the claims transfer process before signing

- Anyone comparing a hazard-zone property to a non-hazard alternative and who wants a structured financial framework to determine whether the discount is large enough to justify the long-term carry costs

Why Not Free Resources?

- FEMA flood maps and government hazard portals tell you which zone you are in. They do not tell you what that zone costs over 30 years. FEMA maps are static (some rely on 2011 data), they do not model pluvial drainage failures, and roughly 40% of all flood insurance claims come from properties outside designated high-risk zones. A zone classification is not a financial analysis.

- Reddit and homebuyer forums are where panicking buyers go at 10 PM after getting their flood zone quote. The advice is genuine but contradictory, anecdotal, geographically inconsistent, and often based on transactions under different market conditions. "We've been in Zone AE for 15 years and never flooded" tells you nothing about your insurance costs under Risk Rating 2.0.

- Insurance broker consultations give you a quote for today. They do not model what happens when the FAIR Plan raises rates 35% to 55% in a single year (proposed for 2026), when your property gets remapped into a higher-risk zone, or when a minor flood claim lands you on the Repetitive Loss list. The broker's job is to bind a policy, not to advise you on whether the property makes financial sense over the life of your mortgage.

- Real estate listing portals (Zillow, Redfin) now show flood and fire risk scores. These are useful starting points but they do not explain mortgage implications, policy workarounds, structural mitigation options, or how to negotiate using the hazard as leverage. A risk score without a cost model is a warning without a solution.

This guide fills the gap between knowing you are in a hazard zone and understanding what that actually means for your money, your mortgage, and your decision.

--- Less Than One Insurance Quote Call

A single hour with a real estate attorney to review hazard zone implications runs $200 to $500. A professional Elevation Certificate costs $350 to $600. The average buyer who skips the insurance stress test and discovers their premiums have tripled in year three faces a cost shock of $3,000 to $8,000 per year that they cannot escape without selling --- often at a loss, because the next buyer will run the same math.

This guide gives you the complete financial framework for evaluating any property in a hazard zone --- the classifications, the insurance mechanics, the mitigation costs, the negotiation leverage, the stress tests, and the walk-away criteria. It covers six countries and every major hazard type. If it prevents even one miscalculated purchase or helps you negotiate even one insurance-based price reduction, it pays for itself before you finish the first chapter.

30-day money-back guarantee. If the guide does not give you a clear, financially grounded framework for evaluating your hazard zone purchase, you pay nothing.

Download the free Quick-Start Checklist to see the 20 concrete steps you should take before making an offer on any property in a flood zone, wildfire zone, earthquake zone, or hurricane corridor. When you are ready for the full financial analysis framework, insurance mechanics, negotiation strategies, and jurisdiction-specific guidance, the full guide is here.

Every house in a hazard zone is a financial equation. This guide makes sure you can solve it before you sign.