The Listing Says "Low HOA Fees." The Reserve Study Says the Roof Fund Is 12% Funded and the Board Just Commissioned an Emergency Engineering Assessment.

You found a condo in a well-maintained building. The pool is clean. The hallways are freshly painted. Monthly fees are $280 — low for the area. Your agent says the association is "financially healthy." You make an offer.

Then escrow opens and the management company sends you 200 pages of governing documents. The CC&Rs mention a rental cap at 20% with a two-year waiting list. The pet restrictions prohibit dogs over 30 pounds — yours is 45. The reserve study is dated 2022 and shows a percent funded level of 28%. The last twelve months of board meeting minutes include a discussion about "exploring funding options" for concrete spalling in the parking garage. The master insurance certificate shows a per-unit deductible of $75,000 — which now violates the 2026 Fannie Mae cap of $50,000.

You search "how to read a reserve study" and get a two-paragraph blog post from a property management company that says "higher is better." You search "Fannie Mae condo rules 2026" and discover the lending standards changed dramatically this year — but every article explains a different fragment of the update. You find a Reddit thread where someone was hit with a $65,000 special assessment eight months after closing because the board had suppressed dues for a decade. Another buyer's mortgage was denied at the last minute because the building became non-warrantable under the new rules.

Your agent says "every HOA has rules." Your lender needs the condo questionnaire by Thursday. You have five days left in your contingency period, and nobody is going to translate those 200 pages into a financial risk assessment for you.

The core problem: free resources cover fragments. CMHC explains reserve studies in theory but won't tell you what a 28% funded level means for your specific purchase. Your agent mentions the governing documents but doesn't explain the rental cap that kills your exit strategy. Reddit threads mix outdated advice with genuine warnings. Nolo articles outline state law without connecting it to the Fannie Mae lending changes that just made half the condo inventory harder to finance. Nobody integrates the reserve fund analysis, the governing document red flags, the lending eligibility rules, the insurance requirements, and the dispute resolution process into a single decision framework. Until now.

The HOA Survival Guide is an Association Due Diligence System — a structured decision framework that connects every financial health indicator, governing document red flag, lending eligibility requirement, insurance gap, and dispute resolution pathway into a step-by-step evaluation you can complete during your contingency period.

What's Inside the Association Due Diligence System

The complete guide plus a quick-start checklist — covering every stage from identifying the type of community association you're buying into through ongoing financial monitoring after you close:

Community Association Classification

The ownership structures that determine your financial exposure. The three types of managed communities — Planned Unit Development (PUD), condominium (COA), and co-op — create fundamentally different risk profiles. In a PUD, a mismanaged HOA means overgrown common areas. In a condo, a mismanaged COA means a collapsing roof over your head and a unit you can't sell. In a co-op, the board can reject your buyer for any non-discriminatory reason, making your exit entirely dependent on corporate approval. The guide maps each structure's insurance requirements (HO-3 vs. HO-6 vs. co-op policy), lender scrutiny levels, and worst-case failure scenarios so you understand exactly what you're buying into before you negotiate.

Reserve Fund Analysis Framework

The single most important number in your due diligence — and how to find it. A reserve study is the engineering and financial document that reveals whether the association can fund upcoming roof replacements, elevator overhauls, and structural repairs without levying special assessments. The guide walks you through reading the study: checking the date (anything older than 36 months is stale), finding the percent funded metric, evaluating whether the board adopted the recommended funding level or cherry-picked a lower tier to keep dues artificially low, and interpreting the component-by-component remaining useful life schedule. Above 70% funded is strong. Below 30% means special assessments are virtually guaranteed. The guide shows you exactly where those numbers hide in the document and what they mean for your purchase decision.

The 2026 Fannie Mae Lending Revolution

Four changes reshaping condominium finance right now. Fannie Mae eliminated Limited Review (every condo now faces Full Review scrutiny). Boards must adopt the highest recommended reserve allocation from their study — no more hiding behind the minimum tier. Buildings without a current reserve study must contribute at least 15% of annual budgeted income to reserves (up from 10%). The master insurance per-unit deductible is capped at $50,000. These rules determine whether your target building qualifies for conventional financing at standard rates — or becomes non-warrantable, restricting you to portfolio loans with higher rates and 10%–20% minimum down payments. The guide explains each change, its effective date, and the specific documents to request to verify compliance before you commit.

Governing Document Red Flag System

The CC&R provisions that cause the most post-purchase devastation — and the exact search terms to find them. Rental caps, short-term rental bans, pet weight limits, breed restrictions, architectural review timelines, lien and foreclosure powers, and amendment procedures. The guide explains the document hierarchy (CC&Rs override bylaws, bylaws override rules), identifies which provisions are nearly permanent because they require supermajority votes to change, and flags the three restrictions that generate the most buyer regret: the rental cap that blocks your exit strategy, the pet rule that forces a decision about your dog, and the short-term rental ban that kills your investment income.

Warrantable vs. Non-Warrantable Financing

Why this distinction controls your interest rate, your buyer pool, and your resale value. A non-warrantable condo means portfolio loans only: higher rates, larger down payments, and a severely restricted buyer pool when you eventually sell. The guide covers the specific metrics lenders evaluate — reserve funding levels, investor concentration, delinquency rates, commercial space limits, litigation status, single-entity ownership thresholds — and includes the FHA and VA condo approval requirements, HUD's searchable approval database, and the Single-Unit Approval process for buildings not on the list.

State-Specific Homeowner Rights

What your state says you can do when the board won't cooperate. California's Davis-Stirling Act assessment caps and record access rights. Florida's SIRS mandate forcing decades of suppressed dues to correct overnight. Texas's mandatory payment plan protections that prevent predatory collection. New York's four-month Article 78 statute of limitations that kills claims if you wait too long. The guide covers the major high-HOA-density states plus a directory of ombudsman offices in Florida, Virginia, Colorado, Nevada, Utah, and Illinois — so you know where to file a formal complaint when internal remedies fail.

HOA Liens, Super Liens, and Foreclosure Risk

The weapon the association holds over your property — and where it can override your mortgage. Approximately 20 states grant HOA assessment liens priority over your first mortgage for a limited amount. In Nevada, that's up to nine months of assessments. In Maryland, up to four months or $1,200, whichever is less. If the HOA forecloses on that super lien portion and your bank doesn't intervene, you can lose your home over a few thousand dollars in unpaid dues. The guide lists every super lien state, explains how liens compound with late fees and attorney's costs, and covers the protective steps (including paying under protest) that keep small disputes from escalating into foreclosure.

Insurance Gap Analysis

The two-layer system that leaves most condo owners underinsured. The master policy covers the building. Your HO-6 covers your unit's interior. But if the master policy has a $25,000 per-unit deductible and a pipe bursts, that deductible falls on you — and your HO-6 only covers it if you bought enough loss assessment coverage. The guide explains "bare walls" vs. "all-in" master policies, the new Fannie Mae Actual Cash Value allowance for roofs (and why that creates a hidden depreciation gap), and exactly how much HO-6 coverage you need to avoid being caught between the two layers.

Dispute Resolution Escalation Ladder

From fines to foreclosure — every level, when to use it, and what evidence to maintain. Internal complaints and selective enforcement defenses. Board recall procedures and quorum requirements. State ombudsman complaints. Mediation ($500–$2,000) and binding arbitration. Civil litigation ($10,000–$100,000+). The guide covers each level with the documentation requirements, the procedural traps that invalidate your case if missed, and the Business Judgment Rule standard that governs how courts evaluate board decisions.

Who This Guide Is For

- First-time home buyers entering an HOA community who have never reviewed governing documents, evaluated a reserve study, or calculated how HOA dues reduce their mortgage qualification — and need a framework that turns 200 pages of legal language into clear financial and lifestyle risk assessments within the five-day contingency window

- Condo buyers navigating the 2026 Fannie Mae changes who need to know whether their target building is warrantable under the new rules, what the elimination of Limited Review means for closing timelines, and whether the board's reserve contribution meets the new mandatory highest-recommended allocation

- Buyers relocating to Sun Belt and Western states (Florida, Arizona, Texas, Nevada, California, Colorado) where 65%–82% of new construction is inside an HOA and state-specific laws like Florida's SIRS mandate create additional financial exposure that national-level guides don't cover

- Real estate investors evaluating rental income potential who need to verify rental caps, short-term rental bans, tenant screening requirements, and investor concentration limits before purchasing a unit they plan to lease — because a single CC&R provision can eliminate the entire financial model

- Current HOA homeowners dealing with disputes or rising assessments who want to understand the selective enforcement defense, the records request process, the board recall procedure, and the escalation path from internal remedies through state ombudsman complaints to litigation

Why Not Free Resources?

- Nolo.com HOA articles and guidebooks explain state statutes and general HOA law clearly. They do not connect reserve fund analysis to the 2026 Fannie Mae warrantability rules, explain how to read a percent funded metric in context, or provide a decision framework for whether to buy, negotiate, or walk away based on the specific financial data in front of you.

- Community Associations Institute (CAI) publications provide macro-level industry data and advocacy materials from the trade association that represents HOA management companies and boards. The educational content is accurate. The perspective is institutional. It does not tell you how to evaluate whether your specific building's board has been suppressing dues, how to spot a special assessment hiding in the meeting minutes, or how to contest a fine using selective enforcement.

- AI-powered document analysis tools (Eli Report, governingdocs.dev, DecodeHOA) charge $39–$40 per property to parse your CC&Rs and generate a health score. They solve one problem well — reading the documents faster. They do not teach you the underlying framework for evaluating financial health across multiple properties, understanding why certain red flags matter more than others, navigating the lending eligibility landscape, or knowing your dispute resolution rights when something goes wrong after you buy.

- Reddit (r/HOA, r/fuckHOA, r/FirstTimeHomeBuyer) is where real homeowners share unfiltered experiences — including buyers blindsided by $50,000 special assessments, pet owners forced to rehome animals they didn't know were restricted, and investors who discovered rental caps after closing. The warnings are genuine. The advice is unstructured, contradictory, and impossible to apply systematically across a time-pressured purchase decision.

- Real estate agent blogs and management company websites offer general overviews of what governing documents contain, from the perspective of professionals who earn fees when you buy or when the board retains their company. They mention reserve studies as something to review. They do not explain why a 28% funded level at a building with a 2022 study means you should probably walk away, or why flat dues for five consecutive years is a more reliable predictor of financial crisis than any single number in the budget.

This guide fills the analysis gap — the space between knowing that reserve studies and CC&Rs exist and understanding how to evaluate them, connect them to current lending rules, and make a buy-or-walk decision under time pressure. It is the evaluation an independent advisor with no units to sell and no boards to represent would give you, structured as a permanent reference you own.

— Less Than a Single HOA Fine

The average HOA fine for a first violation runs $50 to $200. A special assessment triggered by a depleted reserve fund runs $10,000 to $200,000 per unit. A non-warrantable building depresses your unit value by 5%–30%. Moving into a community that bans your dog breed forces a decision no price tag can measure. Hiring an attorney to fight a lien that started as a $500 unpaid assessment costs $5,000 to $20,000.

This guide does not replace your real estate attorney, your lender, or your home inspector. But it gives you the reserve fund analysis framework, the governing document red flag checklist, the lending eligibility verification process, and the dispute resolution playbook that ensure you walk into every appointment knowing exactly what to ask, exactly what to verify, and exactly when to walk away — instead of discovering six-figure liabilities after you've signed.

If it prevents a single special assessment surprise, catches a warrantability issue before your mortgage is denied, or identifies a CC&R restriction that conflicts with your lifestyle before you close, it pays for itself before you've finished the first chapter.

30-day money-back guarantee. If the guide does not make your HOA evaluation process clearer and your purchase decision better informed, you pay nothing.

Plus 8 standalone printable worksheets and reference cards you can print individually and bring to showings, escrow appointments, and insurance meetings: the pre-purchase due diligence checklist (document request table + five management company questions + buy/negotiate/walk-away framework), reserve fund comparison worksheet (evaluate up to 3 properties side by side), 2026 Fannie Mae reference card (all four changes with effective dates), governing document search guide (10 CC&R search terms + restriction matrix), super lien states reference card (which states, priority amounts, protection steps), insurance coverage worksheet (master policy vs. HO-6 gap analysis), dispute resolution escalation ladder (five levels with costs and deadlines), and annual monitoring checklist (yearly financial review sheet).

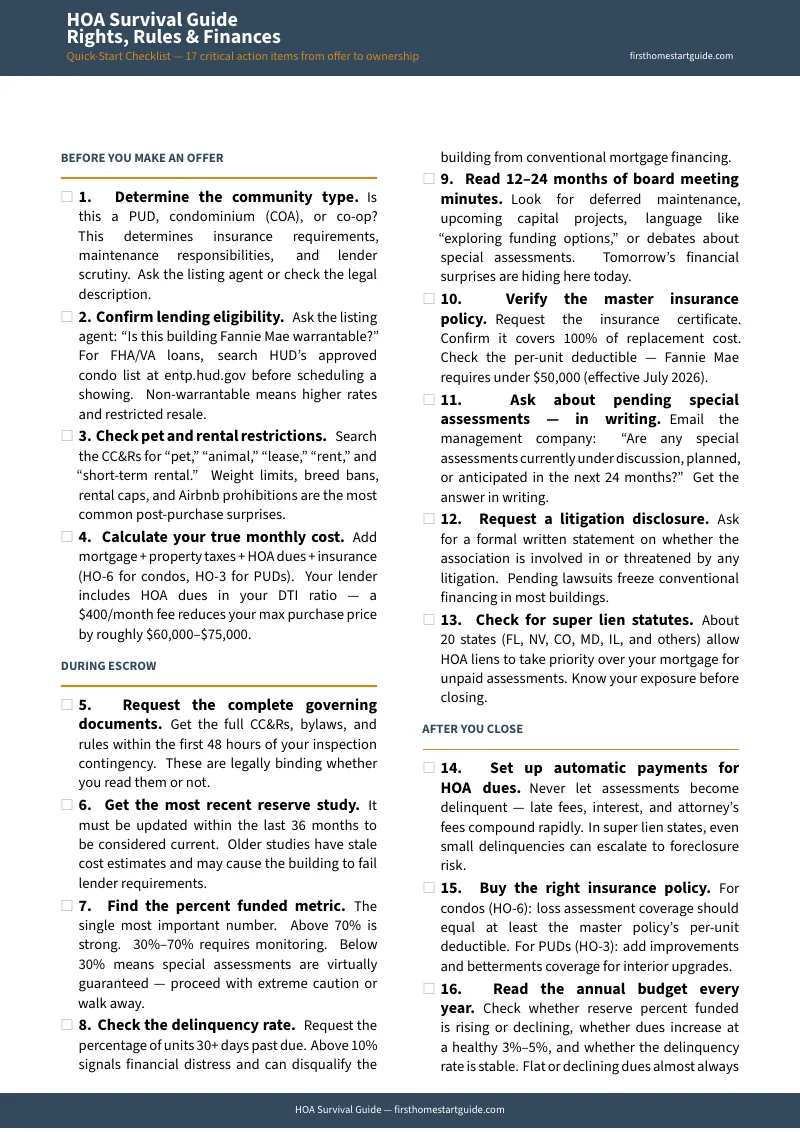

Download the free HOA Quick-Start Checklist to see the 17-item due diligence action plan covering reserve fund benchmarks, lending eligibility checks, and the five questions to ask the management company in writing. When you're ready for the full due diligence system — the complete 12-chapter guide with 8 standalone printable tools — the complete toolkit is here.

You found a home in an HOA community. Now find out what the community is hiding in its financials.