The Gross Yield Clears at 5.5%. The ACT's Zero-Threshold Land Tax, Crown Lease Restrictions, and Rent Increase Cap Will Correct That.

You found a Belconnen unit projecting 5.8% gross yield. Or a Ngunnawal house where Defence Housing tenants pay $730 a week and the vacancy rate sits at 1.2%. Or a Greenway townhouse where the entry price is half of what you'd pay for equivalent yield in Sydney and the tenant pool is 75% public servants on permanent contracts. The numbers clear. Canberra's median household income leads the nation. Vacancy is at 1.5%. Federal government employment underwrites the entire demand side. You're ready to move.

Then the ACT's regulatory reality arrives. Your property has an Average Unimproved Value (AUV) of $450,000. In New South Wales, that's safely under the $1,075,000 land tax threshold — you'd owe nothing. In Queensland, you're under the $600,000 threshold — nothing again. In the ACT, there is no threshold. Land tax is payable from the first dollar. Your annual bill: $3,780 — before you've collected a single week's rent. Buy a detached house in an established suburb and the AUV jumps to $900,000+, pushing your land tax above $9,360 annually. Your Greenway apartment looked like a 5.6% yield until the strata levies ($4,500), municipal rates ($3,200), and that land tax bill reduce your actual net yield to 2.1%. Your tenant's fixed-term lease expires and you want to increase the rent by $40 a week to cover rising rates. Under the ACT's prescribed amount formula, you're capped at the rental CPI growth multiplied by 1.10 — which last year meant a maximum increase of 3.3%, or roughly $18 on a $550 rent. The remaining $22 comes out of your pocket, every week, for the next twelve months. You want to remove a non-paying tenant? The ACT has completely abolished no-grounds evictions. You need a specific statutory reason, 8 to 12 weeks' notice, and the realistic prospect of an ACAT hearing that takes months to resolve.

Here's what no single free resource explains: The ACT is the only Australian jurisdiction that charges land tax from the first dollar of every investment property with no threshold whatsoever, while simultaneously imposing a mathematical rent increase cap tied to a CPI formula that prevents you from passing rising costs to tenants, while enforcing a 99-year Crown Lease system where changing a property's use triggers a Lease Variation Charge of $43,000 per additional dwelling, while mandating minimum R5 ceiling insulation upgrades on all rental properties by November 2026, while introducing a 5% Short-Term Rental Accommodation levy from July 2025 that closes the Airbnb escape route. Each of these has cost real investors five to six figures because the information existed — scattered across the ACT Revenue Office, the Environment and Planning Directorate, ACAT rulings, and PropertyChat threads — but nobody had assembled it into a single underwriting system calibrated to the ACT's unique leasehold market.

The Australian Capital Territory Investment Property Guide is an ACT Regulatory Arbitrage Playbook — not a motivational overview of Australian real estate, but a structured due diligence and cash-flow optimization system that maps every ACT-specific financial trap, regulatory restriction, and tax structuring mechanic into a process you work through before you commit capital. It replaces months of cross-referencing Revenue Office AUV notices, Planning Directorate lease purpose clauses, ACAT tenancy precedents, and forum posts with a single reference that tells you exactly what to verify, exactly what the numbers should look like, and exactly where deals go wrong in the territory.

What's Inside the ACT Regulatory Arbitrage Playbook

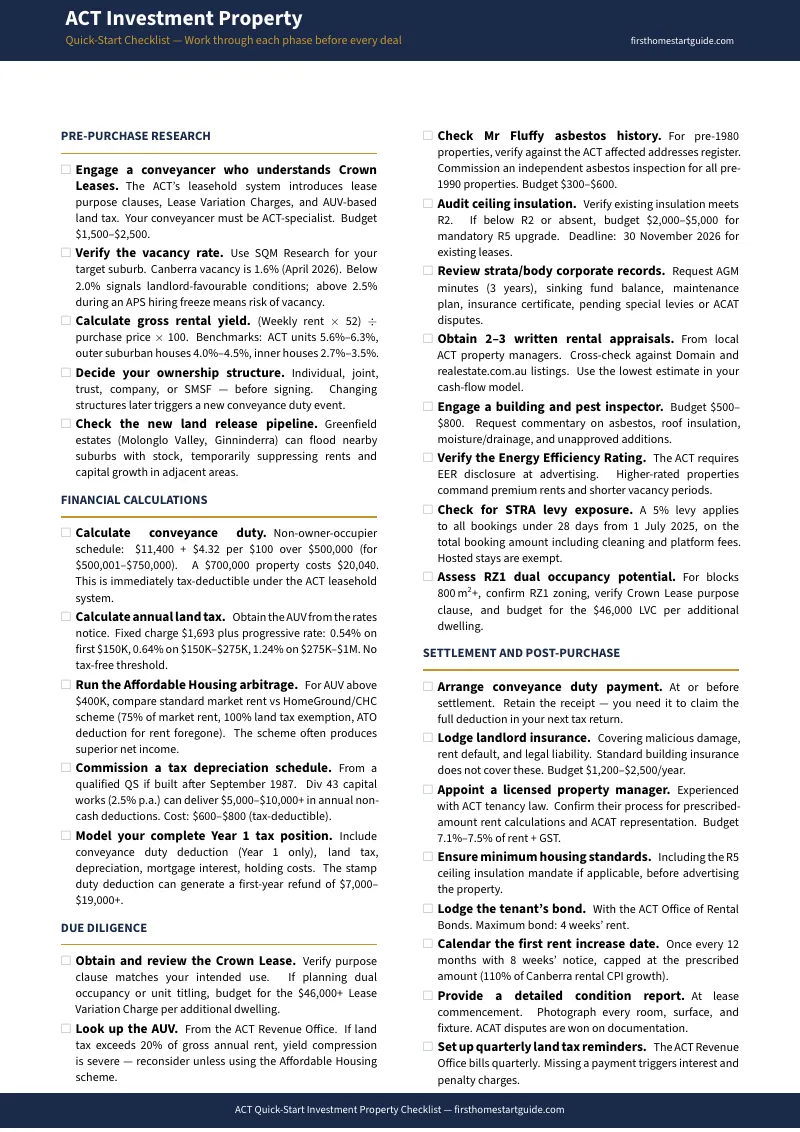

A comprehensive guide, a quick-start checklist, and standalone printable tools — covering every stage from market selection through post-purchase compliance and portfolio optimization, built specifically for the regulatory mechanics and tax structures that make the ACT different from every other Australian jurisdiction:

Land Tax Calculation From the First Dollar

The ACT is the only Australian state or territory with absolutely no tax-free threshold for investment property land tax. In NSW, you hold up to $1,075,000 in land value before triggering any liability. In Queensland, $600,000. In the ACT, a property with an AUV of just $150,000 already owes $810. Move into the $275,001 to $1,000,000 bracket — where most established Canberra houses sit — and the formula becomes $1,610 plus 1.24% of the value above $275,000. An AUV of $700,000 means $6,880 in annual land tax. The guide walks through every progressive rate tier, the fixed charge plus marginal rate calculation, worked examples at different AUV levels, the distinction between AUV (what the Revenue Office assesses) and market value (what you paid), the interaction between land tax and municipal rates (both calculated on AUV), and the interstate comparison showing exactly how much more you pay in the ACT versus an equivalent portfolio in NSW, Victoria, or Queensland. You model the true holding cost before you sign — not when the Revenue Office assessment arrives in July.

The Affordable Housing Land Tax Exemption — The Arbitrage

Buried in the ACT's legislation is a strategy that turns the territory's most punitive cost into a competitive advantage. Lease your property through a registered Community Housing Provider — HomeGround Real Estate Canberra or CHC Australia — at 75% or less of market rent to an income-tested tenant, and the ACT Government grants a 100% full exemption on land tax. On a property with an AUV of $981,000, that's roughly $12,000 per year in land tax eliminated. The rent discount costs approximately $8,060 annually ($600 market rent reduced to $445 per week). But the exemption saves $12,000, and a specific ATO class ruling allows you to claim a tax-deductible donation for the rent foregone — adding approximately $2,980 in additional tax savings at a 37% marginal rate. Net result: $26,120 in operational cash flow under the exemption scheme versus $19,200 under standard market rent. The guide walks through the full eligibility criteria, tenant income thresholds (Tier 4: $64,992 for a first adult), the CHP registration process, how the ATO donation receipt works, worked financial models at different AUV levels and marginal tax rates, the vacancy risk reduction (affordable housing tenants rarely vacate secure housing), and the properties and suburbs where the arbitrage delivers the strongest outcome.

The 99-Year Crown Lease and Lease Variation Charges

Every parcel of land in the ACT is held under a Crown Lease, not the Torrens title freehold system that operates in NSW, Victoria, and Queensland. Practically, a Crown Lease behaves identically to freehold — you can sell, mortgage, or bequeath the property. But the lease dictates explicit permitted uses and development conditions. If you want to subdivide, convert a single dwelling to dual occupancy, or unit-title a property to sell individually, you must apply for a formal lease variation — and pay the Lease Variation Charge. The LVC is a betterment tax on the value uplift from new planning permissions, and it can destroy a small-scale development. The current codified charge for adding a dwelling is $43,000 per new dwelling. The guide covers the Crown Lease structure, how to read the lease purpose clause, the LVC calculation methodology, which development strategies trigger the charge and which don't, the interaction between LVC and RZ1/RZ2 dual occupancy rules, and a feasibility framework for assessing whether a development play actually works after the charge is applied — not just on the yield spreadsheet before it.

Tenant Protection Laws, Rent Caps, and ACAT Navigation

The ACT's Residential Tenancies Act 1997 has been amended to create one of Australia's most tenant-protective regulatory environments. No-grounds evictions have been completely abolished — termination requires a specific statutory reason (sale, family occupation, or major renovation), 8 to 12 weeks' notice, and provable documentation at the time of serving notice. Rent increases are capped at the prescribed amount: the rental CPI growth multiplied by 1.10, applied no more than once every 12 months. Exceeding the cap without tenant consent or an ACAT order is prohibited. The guide consolidates every landlord obligation into a single reference: permitted grounds for termination with notice periods and evidence requirements, the rent increase formula with worked examples at different CPI levels, the ACAT dispute resolution pathway and realistic timelines, property manager selection criteria specific to the ACT regulatory environment, and the practical strategies for managing tenant relationships within the tightest legislative framework in Australia.

Minimum Energy Efficiency Standards and the Insulation Mandate

The ACT is mandating minimum R5 ceiling insulation for all rental properties. Properties with no insulation or insulation below R2 must be upgraded — landlords with existing leases must comply by November 30, 2026, and new leases trigger an immediate 9-month compliance window. For investors purchasing older housing stock in suburbs like Chisholm, Weston Creek, or Woden Valley, this represents an unavoidable capital expenditure that affects initial return calculations. The guide covers the specific R-value requirements, compliance timelines, estimated upgrade costs by property type, how to factor insulation CapEx into your offer price, and the broader energy efficiency trajectory the ACT Government is pursuing — so you know what additional mandates are likely in the next 3 to 5 years.

Short-Term Rental Accommodation Levy and the Airbnb Calculus

From July 1, 2025, a 5% STRA levy applies to all short-term bookings under 28 days facilitated by a booking platform. The levy is calculated on the total booking amount — nightly rate plus cleaning fees, pet fees, and the platform's booking fee. For investors considering Airbnb as an alternative to the long-term rental market's rent caps and eviction restrictions, the guide models the true financial comparison: short-term yields after the 5% levy, platform fees (typically 3% host fee), higher vacancy, higher maintenance, and furniture costs versus long-term yields after land tax, municipal rates, and the CPI rent cap. The numbers don't always favour the strategy you'd expect.

The High-Density Oversupply Trap

New investors are consistently drawn to Canberra apartments by entry prices under $550,000 and advertised gross yields above 5.5%. The reality: investment forums document case after case of apartment investors trapped in assets with zero or negative capital growth over multi-year holding periods. The cause is a sustained development pipeline that floods Greenway, Gungahlin, and Molonglo Valley with new stock that directly competes with secondary resales. When pristine new apartments come online in adjacent blocks every year, your older unit doesn't appreciate. The guide provides a suburb-by-suburb oversupply risk assessment, the indicators that distinguish genuinely supply-constrained corridors from saturated ones, how to calculate true net yield after strata levies, municipal rates, and zero-threshold land tax are applied, and the asset types and locations where capital growth actually occurs in the ACT market.

Standalone Printable Tools

In addition to the guide and checklist, your download includes standalone PDFs you can print and take to inspections, conveyancer meetings, and accountant appointments:

- Land Tax Calculator Worksheet — every progressive rate tier with worked examples at different AUV levels, the fixed charge plus marginal rate formula, AUV-to-market-value translation, and an interstate comparison so you can see exactly how much more the ACT charges versus NSW, Queensland, and Victoria

- Affordable Housing Arbitrage Modeller — side-by-side financial comparison of standard market rent versus the CHP exemption scheme at different AUV levels and marginal tax rates, with the ATO donation receipt calculation and net cash-flow outcome

- Crown Lease and LVC Feasibility Checklist — how to read your lease purpose clause, determine if your development triggers the LVC, calculate the $43,000-per-dwelling charge, and assess whether the project is feasible after the charge is applied

- Tenant Law Compliance Reference Card — no-grounds eviction ban quick reference, permitted termination grounds with notice periods, the rent increase prescribed amount formula, ACAT dispute pathway, and insulation compliance deadlines

- Due Diligence Checklist — per-property evaluation covering contract review, Crown Lease purpose clause verification, building inspection, AUV assessment, strata records, and rental appraisal

Who This Guide Is For

This guide is for property investors targeting the ACT market who:

- Are interstate investors from Sydney, Melbourne, or Brisbane attracted by Canberra's low vacancy rates, high median incomes, and 5%+ gross yields — but need to model how the ACT's zero-threshold land tax, progressive rate tiers, and municipal rates will reduce that theoretical yield to actual net cash flow before they deploy capital 300 kilometres from home based on numbers that don't account for the territory's unique holding costs

- Are existing Canberra homeowners leveraging equity to purchase a second or third investment property within the territory — and need to avoid the high-density oversupply trap where apartments in Greenway, Gungahlin, and Molonglo Valley deliver theoretical yields that mask years of stagnant capital growth, rising strata levies, and compounding negative cash flow that turns the property into nothing more than a depreciation schedule

- Are rentvestors living in Braddon, Kingston, or the inner south while investing in outer suburbs like Ngunnawal or Chisholm — operating on tight budgets and needing the land tax calculation, the affordable housing arbitrage model, and the insulation compliance costs quantified before a single unexpected bill derails their cash flow and forces a distressed sale

- Want every ACT-specific regulation, tax calculation, and due diligence requirement in one reference — instead of assembling it from Revenue Office rate tables, Planning Directorate lease variation schedules, ACAT tenancy rulings, HomeGround eligibility criteria, and PropertyChat threads that may predate the 2025 STRA levy, the 2026 insulation mandate, or the latest AUV assessments

Why Not Free Tools and Forums?

Free information on ACT property investing exists. Here's what it actually delivers:

- The ACT Revenue Office publishes land tax rate tables and AUV schedules. It doesn't explain how the gap between AUV and market value makes the actual bill unpredictable until you receive the assessment, doesn't compare the dollar impact against equivalent portfolios in NSW or Queensland, doesn't model the affordable housing exemption side by side with standard market rent, and doesn't tell you which AUV brackets make the CHP arbitrage mathematically superior. You get the rate schedule without the strategic analysis that makes it useable.

- The Environment and Planning Directorate publishes Crown Lease fact sheets and Lease Variation Charge schedules. They don't explain how to read the lease purpose clause on a specific property title, don't model whether a dual occupancy development is still feasible after the $43,000-per-dwelling LVC is applied, and don't map which RZ1 and RZ2 blocks actually offer development potential versus those where the charge eliminates the margin. The directorate administers the system — it doesn't help you financially model it.

- Mortgage brokers and buyer's agents produce suburb profiles highlighting vacancy rates, median rents, and Canberra's economic stability. They minimise the zero-threshold land tax, the rent increase cap, the insulation mandate, and the apartment oversupply — because their content is designed to generate transactions, not to help you identify reasons not to buy. The guide covers both sides.

- PropertyChat and Reddit threads (r/AusPropertyChat, r/AusFinance, r/canberra) contain genuine investor experience reports — including detailed accounts of being trapped in negatively geared Greenway apartments and the real costs of ACAT disputes. But the advice is often contradictory, mixes pre- and post-reform information, and a 2023 thread on land tax may not reflect the current rate tiers or the affordable housing exemption mechanics. Sorting current from outdated takes longer than reading a guide that has already done it.

This guide fills the ACT-specific gap — the space between knowing how to analyse a rental property in general and knowing how to underwrite one in the only Australian jurisdiction where land tax has no threshold, where rent increases are mathematically capped by a CPI formula, where all land is leasehold rather than freehold, where an affordable housing exemption can legally eliminate your largest holding cost, and where a $43,000-per-dwelling charge can kill a development project overnight. It's the analysis that would take an ACT property solicitor, a specialist tax adviser, and a community housing provider to assemble — structured as a reference you own permanently.

— Less Than One Quarter's Municipal Rates

A single quarterly municipal rates notice on a Canberra house runs $800 to $1,200. Annual land tax on a property with an AUV of $700,000 is $6,880. The Lease Variation Charge for adding one dwelling is $43,000. Minimum R5 ceiling insulation on an older property can cost $3,000 to $6,000. A 6-month ACAT dispute over a contested eviction costs thousands in legal fees and lost rent.

This guide doesn't replace your conveyancer or your tax adviser. But it gives you the land tax calculation model, the affordable housing arbitrage framework, the Crown Lease feasibility checklist, the tenant law compliance reference, and the oversupply risk assessment that ensure you identify every ACT-specific risk before you're contractually committed — instead of discovering them on your first Revenue Office assessment, your first ACAT hearing, or your first year of negative cash flow on an apartment that was supposed to yield 5.5%.

If it catches a single land tax miscalculation, prevents one oversupplied apartment purchase, or reveals that the affordable housing exemption would net you $7,000 more annually than standard market rent, it pays for itself before you've finished reading it.

30-day money-back guarantee. If the guide doesn't sharpen your underwriting and protect your capital in the ACT's unique regulatory environment, you pay nothing.

Download the free ACT Quick-Start Investment Property Checklist to see the due diligence framework covering pre-purchase research, land tax calculation, Crown Lease review, compliance requirements, and post-purchase setup. When you're ready for the full land tax arbitrage model, LVC feasibility checklist, tenant law compliance system, and portfolio optimization strategy, the complete guide is here.

The yield clears at 5.5%. This guide tells you whether the ACT agrees.