You Have Read the Revenue NSW Fact Sheet, Run the FHBAS Calculator, and Checked the Federal 5% Deposit Scheme. You Still Cannot Work Out Whether Signing a Section 66W Certificate Will Save Your Purchase or Cost You Your Entire $150,000 Deposit.

You have looked at apartments in Granville and townhouses in Merrylands. You have checked house-and-land packages around Marsden Park and compared median prices in Newcastle and Wollongong. You may have seen the Reddit thread about a buyer who exchanged on a $780,000 unit after their agent pressured them into a 66W, only for the bank valuation to come in $60,000 short — leaving them contractually locked into a purchase they could not fund, facing the loss of their entire deposit. Or the r/AusPropertyChat post about a couple who settled on a strata apartment in Mascot, only to receive a $28,000 special levy notice four months later for waterproofing remediation that was buried in 200 pages of committee minutes they never read.

The problem is not a lack of information. Revenue NSW covers the FHBAS thresholds. Service NSW explains the FHOG eligibility rules. Housing Australia publishes the 5% deposit scheme caps. But no single resource explains how the $800,000 stamp duty exemption, the $600,000 FHOG cap, the $1,500,000 federal guarantee limit, and the abolished First Home Buyer Choice property tax interact — where they stack, where they conflict, and at which exact price points you lose tens of thousands because you crossed the wrong threshold. Nobody explains when signing a Section 66W is a calculated risk and when it is financial recklessness. Nobody gives you a go/no-go matrix for reading strata reports in plain English. Nobody warns you that the "Company Title" apartment in Potts Point your bank pre-approved you for at 95% LVR will be rejected the moment the lender discovers you are buying shares in a company, not real property.

The New South Wales First Home Buyer Guide is an NSW Transaction Protocol — a single, structured reference that maps every grant threshold, stamp duty formula, ownership structure trap, strata defect signal, and the full exchange-to-settlement timeline into a step-by-step process you work through before you sign anything unconditional. It replaces weeks of cross-referencing government portals, Reddit warnings, conveyancer blog posts, and mortgage broker pitches with a reference that tells you exactly what to check, exactly what the numbers should look like, and exactly where NSW-specific transactions fall apart.

What's Inside the NSW Transaction Protocol

A complete guide, a quick-start checklist, and standalone worksheets and reference cards — covering every stage from calculating your true borrowing power through to collecting your keys, built specifically for the grants, ownership structures, legal mechanisms, and strata risks that make buying in New South Wales different from every other Australian state:

The Scheme-Stacking Strategy — FHBAS + FHOG + FHBG in One Purchase

The FHBAS eliminates stamp duty on properties up to $800,000, saving you up to $31,207 in upfront cash. The FHOG gives you $10,000 for new homes under $600,000 (or $750,000 for house-and-land). The federal First Home Guarantee lets you buy with a 5% deposit and zero LMI, with a $1,500,000 cap in Sydney, Newcastle, Illawarra, and Lake Macquarie. These three programs stack. A buyer choosing a $750,000 property can secure it with $37,500 in deposit, zero stamp duty, and zero LMI — reducing cash-to-close by over $150,000 compared to buying without any scheme. The guide provides worked cash-to-close calculations at three price points — $750,000, $850,000, and $700,000 house-and-land — showing exactly what you need in the bank on settlement day, not just a generic claim that "concessions are available."

The Section 66W Survival Guide — When to Sign, When to Refuse, and What Happens If You Get It Wrong

A 66W certificate waives your five-day cooling-off period and makes the contract instantly unconditional — exactly like buying at auction. If your finance falls through, the bank valuation comes in low, or a post-exchange inspection reveals catastrophic defects, you forfeit your entire 10% deposit and can be sued for any shortfall on resale. Agents will pressure you to sign one on a Friday afternoon before a Saturday auction. The guide covers the five conditions that must be true before signing a 66W, the three scenarios where you should refuse no matter what the agent says, and the rapid 48-hour due diligence sequence for when unconditional exchange is genuinely the only way to secure the property.

The Strata Defect Decoder — A Go/No-Go Matrix for Reading Committee Minutes

76% of assessed NSW strata buildings show active water ingress or waterproofing failure. 65% of surveyed schemes have issued special levies — ranging from $1,200 to $38,000 per unit. The stamp duty exemption funnels first home buyers into apartments, directly into the path of the state's strata defect crisis. The guide provides a plain-English red flag matrix for evaluating strata reports: Capital Works Fund adequacy ratios (below 50% means a special levy is coming), AFSS compliance failures (87% of reports show fire safety issues), repeated water damage motions in minutes, and defeated maintenance motions that signal a dysfunctional owners corporation. You do not need a law degree to read strata minutes — you need a checklist that tells you what to look for and when to walk away.

Company Title vs. Strata — The Ownership Trap That Kills 95% LVR Pre-Approvals

Company Title apartments survive in Sydney's Eastern Suburbs, Lower North Shore, and Inner West — premium locations that attract first home buyers hunting for character and lifestyle. But Company Title means you do not own real estate. You own shares in a company. Banks cap LVR at 70%–80%, meaning your 5% deposit strategy and your federal guarantee eligibility are both destroyed the moment the lender discovers the title structure. The guide explains how to identify Company Title before making an offer, why the board can reject your purchase for any reason, and when the price discount on a Company Title apartment is worth the financing restrictions.

The Exchange-to-Settlement Timeline — 42 Days, Step by Step

Exchange triggers the contract. Settlement completes the transfer 42 days later. Between those dates, you need to finalise loan documents, arrange building insurance (from exchange, not settlement — you carry the risk from the moment you exchange), confirm PEXA workspace setup, conduct your pre-settlement inspection within 3 business days of completion, and transfer the balance of funds. The guide maps every obligation to its deadline, explains who insures the property between exchange and settlement (you do, even though you do not have the keys), and covers the pro-rated adjustments your conveyancer calculates for council rates, water, and strata levies.

The Abolished Property Tax Clarification

In January 2023, NSW introduced the First Home Buyer Choice scheme — opt out of stamp duty and pay an annual property tax instead. It was abolished on 1 July 2023 when the government changed. It no longer exists. The internet remains saturated with outdated articles and calculators from early 2023 telling buyers to "choose between stamp duty and the annual property tax." Buyers are building financial models around a tax option that does not exist. The guide clears this up in one page so you do not waste weeks modelling an option that was scrapped three years ago.

Section 10.7 Planning Certificates — Why the Basic Version Is Not Enough

Every contract includes a Section 10.7(2) certificate. It tells you the zoning. It does not tell you that the property sits in a future road corridor, on contaminated land, in an acid sulfate soil zone, or in a flood-prone area that will void your insurance. The full Section 10.7(2)(5) certificate does. It costs $70–$120 from the council and takes a few days. The guide explains the difference, lists the specific risks the full certificate reveals, and makes the case for why ordering it is non-negotiable on every purchase.

10 Standalone Printable PDFs

Stamp duty rate tables with the FHBAS concession formula. Scheme eligibility checklist for FHBAS, FHOG, FHBG, and Help to Buy. Cash-to-close worksheets with three worked scenarios ($750K, $850K, $700K house-and-land) plus a blank fillable worksheet. Strata report evaluation matrix. Section 66W decision framework. Auction preparation checklist. Settlement timeline planner. Property inspection checklist covering building and pest, strata, pool compliance, asbestos, and planning certificates. Print the ones you need and bring them to your conveyancer, broker, or open home.

Who This Guide Is For

- Sydney renters earning $100,000 to $300,000 who have the income to service a mortgage but cannot work out whether a $780,000 apartment in Merrylands or a $700,000 house-and-land package in Marsden Park saves them more money after stacking the FHBAS, FHOG, and FHBG

- Buyers who have been told to sign a Section 66W by an agent and need to understand exactly what they are giving up — and whether their due diligence is complete enough to justify the risk

- Anyone buying a strata-titled apartment who needs to decode committee minutes, evaluate the Capital Works Fund, and identify special levy risk before exchanging on a property that could become a financial sinkhole

- First home buyers comparing Sydney versus regional NSW — Newcastle, Wollongong, Central Coast — who need the actual numbers at each location: median prices, FHBAS status, FHBG caps, and the trade-offs in capital growth and commute times

- Buyers considering house-and-land packages in Western Sydney who need to understand split contracts, the FHOG price cap on new builds, Section 88B covenants, and construction-phase risks

- Anyone who has seen articles about the "property tax option" and needs a definitive answer on whether it still exists (it does not) before building a savings plan around outdated information

Why Not Free Resources?

Free information on buying your first home in New South Wales exists across a dozen government websites. Here is what it actually delivers:

- Revenue NSW publishes the FHBAS thresholds and stamp duty rates. It does not provide worked cash-to-close calculations at your target price point, explain how the concession formula produces vastly different outcomes at $850,000 versus $950,000, or model how the FHBAS interacts with the federal 5% deposit scheme. You get the rules without the financial planning that makes the rules actionable.

- Service NSW explains the FHOG eligibility criteria. It does not warn you that a house-and-land package where builder variations push the total value past $750,000 costs you the entire $10,000 grant. You get the criteria without the mechanism that causes real buyers to fail them.

- Government websites define a Section 66W certificate as a waiver of the cooling-off period. They do not describe the psychological pressure tactics an agent will use on a Friday afternoon to force its signature, the five conditions that must be met before it is safe to sign, or the financial exposure if your finance falls through after signing. You get the legal definition without the tactical survival guide.

- Reddit, Whirlpool, and Facebook groups contain real buyer experiences — but strata advice from 2024 does not reflect 2026 SBBIS bond changes, posts about the "property tax option" reference a scheme abolished in July 2023, and 66W discussions from Melbourne-based users describe Victorian cooling-off rules that do not apply in NSW. Sorting current from outdated, NSW-specific from interstate, takes longer than reading a guide that has already done it.

This guide fills the New South Wales-specific gap — the space between knowing you want to buy a first home and knowing how to navigate a state where 66W certificates can cost you $150,000, strata defects are systemic, Company Title kills your financing, stamp duty concessions taper to zero at $1,000,000, and the most-discussed tax option of 2023 no longer exists.

— Less Than a Single Strata Inspection Report

A strata inspection report costs $250 to $400. Conveyancing fees run $1,000 to $3,000. Crossing the $800,000 stamp duty exemption threshold by $50,000 costs you $8,166 in transfer duty. Defaulting on a purchase after signing a 66W on an $800,000 property forfeits $80,000 in deposit. Settling on a Company Title apartment after assuming your 95% LVR pre-approval would hold means scrambling for a 20% to 30% deposit you do not have. Missing a $28,000 special levy buried in strata minutes costs exactly $28,000.

This guide does not replace your conveyancer. But it gives you the scheme-stacking strategy, the 66W survival framework, the strata defect decoder, the Company Title warning checklist, and the complete cash-to-close worksheets that ensure you identify every New South Wales-specific risk before you exchange contracts — not when the Revenue NSW assessment arrives, the bank valuation comes in short, or the special levy notice hits your letterbox.

If it saves you from a single stamp duty cliff you would not have calculated, a single 66W you would not have questioned, or a single strata red flag you would not have spotted, it pays for itself before you finish reading it.

30-day money-back guarantee. If the guide does not sharpen your due diligence and protect your deposit in New South Wales's property market, you pay nothing.

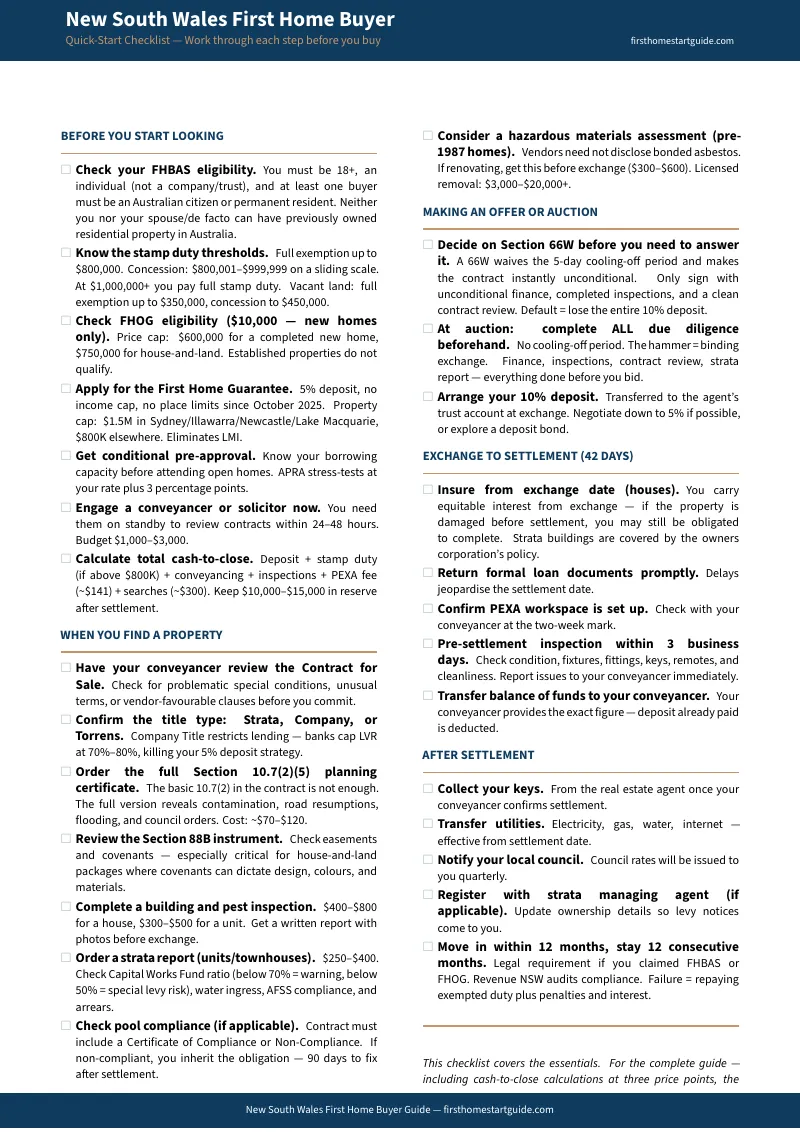

Download the free New South Wales Quick-Start Home Buying Checklist to see the step-by-step framework covering pre-approval, house hunting, inspections, and settlement. When you are ready for the full scheme-stacking strategy, 66W survival guide, strata defect decoder, and complete acquisition cost breakdowns, the complete guide is here.

The schemes are generous. The traps are hidden. This guide makes sure you claim the first without falling into the second.