You Have Researched the $50,000 HomeGrown Grant, the HLPE Stamp Duty Exemption, and the Federal Deposit Schemes. You Still Cannot Calculate What You Will Actually Pay to Buy in the Northern Territory.

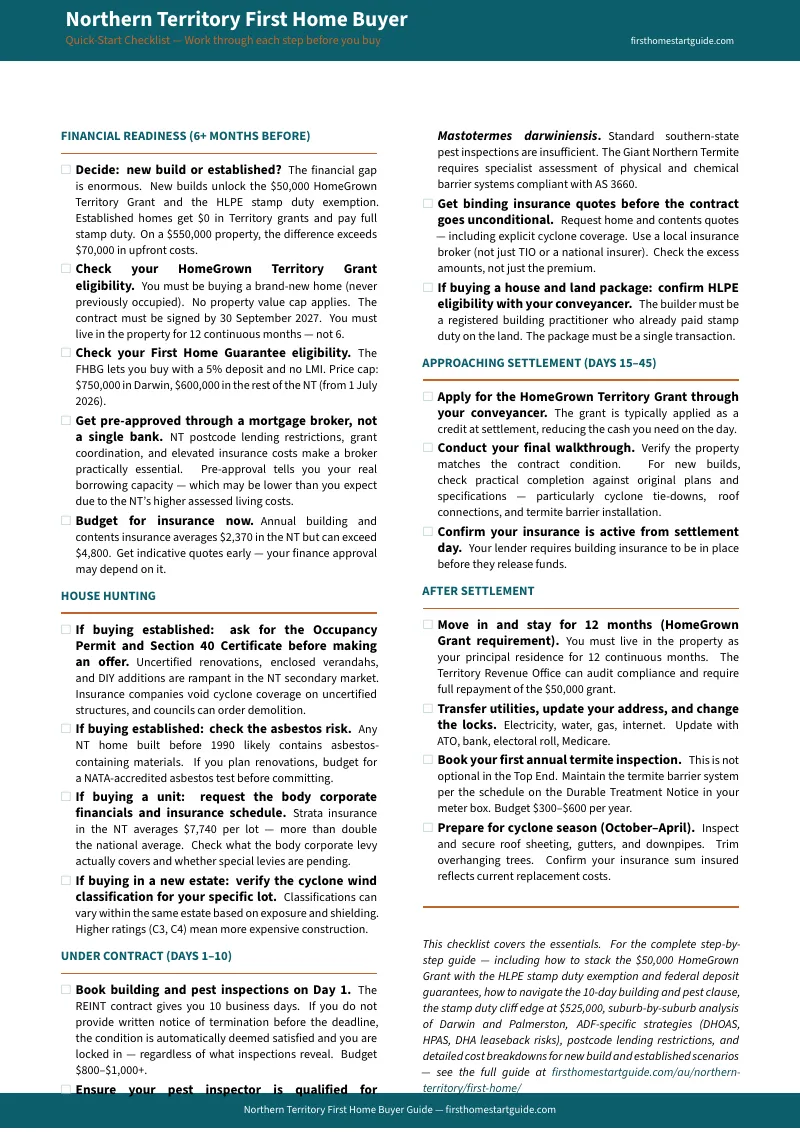

You have read the Territory Revenue Office pages on the HomeGrown Territory Grant. You have looked at house-and-land packages in Zuccoli and established homes in Nightcliff. You may have seen the Reddit thread about a buyer who purchased a Palmerston house with an enclosed veranda that turned out to be uncertified — no Section 40 certificate, no Occupancy Permit — and discovered their insurer voided all cyclone coverage the week before the wet season. Or the r/darwin post about someone who missed the 10-business-day building and pest deadline by a single day, got automatically locked into a contract, and then found $38,000 in termite damage behind the gyprock.

The problem is not a lack of information. The Territory Revenue Office covers the HomeGrown grant. The NT Building Advisory Service publishes cyclone construction guides. The REINT has standard contract templates. But no single resource explains how the $50,000 HomeGrown grant interacts with the HomeBuild Access $550,000 price cap and the First Home Guarantee's new $750,000 Darwin ceiling, how the HLPE stamp duty exemption saves you more than $23,000 on a $550,000 new build while established buyers pay full stamp duty with zero concessions, how a missing Section 40 certificate on an enclosed veranda can void your entire cyclone insurance policy, or why the 10-business-day REINT clause automatically locks you into a contract if you do not send written notice in time — regardless of what inspections later reveal.

The Northern Territory First Home Buyer Guide is a Territory Risk Shield — a single, structured reference that maps every grant, concession, environmental hazard, lending restriction, and contract trap into a step-by-step process you work through before you sign anything. It replaces weeks of cross-referencing government portals, forum threads, and broker marketing with a reference that tells you exactly what to check, exactly what the numbers should look like, and exactly where Territory-specific deals fall apart.

What's Inside the Territory Risk Shield

A comprehensive 14-chapter guide, a quick-start checklist, and standalone worksheets and reference cards — covering every stage from calculating your true borrowing power through to collecting your keys, built specifically for the grants, hazards, and legal frameworks that make buying in the Northern Territory different from every other Australian jurisdiction:

The $50,000 HomeGrown Territory Grant and Eligibility Strategy

The HomeGrown Territory Grant is the largest first home buyer grant in Australia — $50,000 in tax-free cash for new homes that have never been previously occupied, with no property value cap. Contracts must be signed by 30 September 2027. But the residency requirement has been tightened to 12 continuous months — up from the previous 6 months — and failing to comply means repaying the entire $50,000. The guide walks through every eligibility rule, the interaction with the FreshStart grant for non-first-home-buyers competing for the same land allotments, and the exact timeline you need to protect your grant compliance.

The HLPE Stamp Duty Exemption — Why THOD Is Dead and What Replaced It

The Territory Home Owner Discount is gone. There are no general stamp duty concessions for first home buyers purchasing established homes in the NT. Instead, the House and Land Package Exemption provides a full stamp duty exemption for buyers purchasing a house and land package from a registered building practitioner before 30 June 2027. On a $550,000 property, this saves more than $23,000 compared to buying established. The guide includes the NT's unique quadratic stamp duty formula with worked calculations at every major price point, so you see the exact dollar difference between new build and established at your target price — not a generic claim that "new builds are cheaper."

Federal and Territory Scheme Stacking

The First Home Guarantee lets you purchase with a 5% deposit and no Lenders Mortgage Insurance. The 2026 price cap split is critical: $750,000 for Darwin, $600,000 for the rest of the NT — up from the previous blanket $600,000. HomeBuild Access lets you build with just a 2.5% deposit by providing a government-subsidized 17.5% deposit loan through People First Bank. The guide maps out how to stack these federal and Territory programs with the $50,000 HomeGrown grant and the HLPE exemption — showing the exact combination that compresses your upfront cash requirement to its minimum for your specific purchase price and location.

Cyclone Construction Ratings, Region C, and the Section 40 Certificate

The NT sits in Wind Region C — one of the most severe cyclone classifications in the Australian building code. Every residential property must withstand 250 km/h wind gusts with certified structural tie-downs, engineered roof trusses, and impact-resistant cladding. The real danger for buyers is the secondary market. Uncertified renovations — enclosed verandas, DIY carports, unapproved shed additions — are rampant across Darwin and Palmerston. If the structure lacks a Section 40 certificate and Occupancy Permit, insurers void cyclone coverage entirely and councils can order demolition. The guide provides the exact legal verification process: what certificates to demand before making an offer, how to check the NT Building Practitioner Register, and what to do when the seller cannot produce documentation.

The Mastotermes Threat — Why Standard Pest Inspections Are Not Enough

Mastotermes darwiniensis — the Giant Northern Termite — is the most destructive subterranean termite species on the continent. Colonies of over 100,000 insects can gut structural timber framing within months. Standard southern-state pest inspections miss what matters in the Top End. The guide covers the AS 3660 physical barrier systems (Termimesh marine-grade stainless steel mesh), why chemical reticulation barriers degrade rapidly in monsoonal soil conditions, how to verify that an established home's termite management system has been continuously maintained, and what happens when a buyer inadvertently breaches the barrier through minor landscaping — rendering the property uninsurable against pest damage.

The 10-Business-Day REINT Clause Trap

The NT operates with a standardised REINT contract that gives you exactly 10 business days for building and pest inspections. This clause operates as "deemed satisfied" — if you do not provide formal, written notice of rescission to the vendor's conveyancer before the deadline, the condition is automatically waived. You are permanently locked into the contract regardless of what subsequent inspections reveal. Finding a building inspector, licensed plumber, certified electrician, and specialist Mastotermes pest inspector within 10 business days is extremely difficult due to severe labour shortages. Inspections cost $800 to $1,000+. The guide provides a day-by-day scheduling strategy and the exact written notice format required to preserve your termination rights.

Postcode Lending Restrictions and the Serviceability Illusion

NT wages are statistically higher than the national average. But lenders assess living costs — insurance premiums, continuous air conditioning, structural maintenance — at a significant premium. A seemingly robust income produces a lower borrowing capacity than buyers expect. Outside Greater Darwin, the restrictions escalate: Alice Springs, Katherine, and single-industry mining towns face maximum LVR caps of 60% to 80%, requiring deposits of 20% to 40% that completely negate low-deposit federal schemes. The guide includes a postcode-by-postcode lending restriction reference so you know your borrowing reality before you start house hunting — not when your finance application is rejected.

The Darwin-Palmerston Location Strategy

Palmerston is the engine of NT first home buyer activity, but buyer sentiment is sharply divided along suburb lines. Moulden, Gray, Woodroffe, and Driver offer the lowest entry prices but carry entrenched reputational issues — property crime, anti-social behaviour, and historically poor capital growth. Zuccoli, Bellamack, Johnston, and Rosebery command premiums for master-planned estates and access to the $50,000 HomeGrown grant on house-and-land packages. The guide provides the unfiltered suburb analysis — crime data, capital growth history, rental yield comparison, and the specific trade-offs between affordability and long-term capital position — so you make your location decision with data, not forum opinions.

Defence Housing — Buying as an ADF Member

Darwin is a critical strategic military hub. ADF personnel can stack DHOAS monthly interest subsidies (based on years of service) with HPAS ($16,949 one-off payment) and HPSEA transactional cost coverage on top of the $50,000 HomeGrown grant. The guide explains how to maximise these benefits within a typical three-to-four-year posting cycle, how to structure the purchase for rental conversion when you rotate out, and how to avoid the negative equity trap that catches buyers who purchase at the peak of a posting-driven price surge.

The Insurance Premium Crisis

Northern Australians pay approximately $2,370 annually for residential building and contents insurance — 76% more than the rest of Australia. Strata insurance for units averages $7,740 per lot, more than double the national figure. The Cyclone Reinsurance Pool has reduced some premiums, but quotes from local legacy insurers like TIO still exceed $4,800 for standard Palmerston properties. The guide covers how to use local insurance brokers to bypass the TIO monopoly, navigate the Cyclone Reinsurance Pool, secure viable mainland coverage, and factor insurance costs into your serviceability calculations before — not after — your finance approval.

New Build vs Established: The Full Financial Comparison

Side-by-side worked examples at $450,000, $550,000, and $650,000 showing HomeGrown grant eligibility, HLPE stamp duty exemption, deposit requirements, and total upfront costs for new builds versus established homes. On a $550,000 property, a first home buyer purchasing a new build saves over $73,000 in combined grants and stamp duty compared to buying established — the largest new-build advantage of any Australian state or territory. These are not generalised estimates; they are NT-specific calculations with the current stamp duty formula applied.

Conveyancing, Settlement, and Post-Purchase Compliance

The full settlement timeline from contract exchange to key handover, handled by a conveyancer or solicitor. The 4-business-day statutory cooling-off period. Contract conditions you should always include, conditions you should never waive. Building and pest inspection scheduling within the 10-day window. And the post-settlement obligations that catch new owners: HomeGrown grant 12-month residency compliance, annual termite inspection requirements, insurance activation, and the real first-year cost of owning a home in the Top End — where air conditioning alone can add $300+ per month to your power bill.

Who This Guide Is For

- Darwin renters paying $683 to $711 per week who are ready to buy but cannot work out whether the HomeGrown grant, HLPE exemption, and federal deposit schemes add up to enough to bridge the gap between their savings and what the market demands

- Buyers choosing between a house-and-land package in Zuccoli or Bellamack and an established home in Nightcliff or Rapid Creek who need the actual dollar comparison — grant eligibility, stamp duty, deposit requirement, insurance costs — at their specific price point

- ADF personnel posted to Darwin who need to stack DHOAS, HPAS, HPSEA, and the HomeGrown grant within a posting cycle and understand the rental conversion strategy for when they rotate out

- Public servants and healthcare workers drawn to the Territory by remote area salary premiums who need a buying strategy that accounts for the transient nature of the NT population and the risk of negative equity during market downturns

- Anyone buying an established home in Darwin or Palmerston who needs to verify Section 40 certificates, Occupancy Permits, cyclone compliance, and Mastotermes termite barrier integrity before signing a contract

- Regional buyers in Alice Springs, Katherine, or mining towns who need to understand postcode lending restrictions before discovering their 5% deposit scheme is worthless in their area

Why Not Free Resources?

Free information on buying your first home in the Northern Territory exists across a dozen government websites. Here is what it actually delivers:

- The Territory Revenue Office publishes HomeGrown grant eligibility rules, stamp duty calculators, and application forms. It does not warn you that the 12-month residency requirement means ADF members on short rotations risk repaying the entire $50,000 if they are posted out early. It does not explain the $73,000+ financial gap between new builds and established homes. You get the rules without the strategy that makes them useful.

- The NT Building Advisory Service publishes cyclone construction guides and termite management standards. It does not connect these to buying decisions — it does not tell you that a missing Section 40 certificate on an enclosed veranda voids your cyclone insurance, or that a lapsed chemical reticulation warranty leaves you exposed to Mastotermes damage that standard policies exclude. You get the building regulations without the buyer risk assessment.

- Housing Australia publishes the First Home Guarantee rules. It does not explain that the 2026 Darwin price cap increase to $750,000 finally makes the scheme viable for median-priced houses, or how to stack it with the HomeBuild Access 2.5% deposit scheme. You get the eligibility criteria without the Territory-specific stacking strategy.

- Reddit, Facebook groups, and Whirlpool contain real buyer experiences mixed with advice that predates the THOD cessation, the FHBG price cap split, or the HomeGrown grant extension to 2027. A thread from 2024 explaining stamp duty concessions references a scheme that no longer exists. Sorting current from outdated takes longer than reading a guide that has already done it.

This guide fills the Territory-specific gap — the space between knowing you want to buy a first home and knowing how to navigate a jurisdiction where a $50,000 grant has a 12-month residency compliance trap, stamp duty exemptions only apply to house-and-land packages from registered builders, termite damage can gut a house in months, cyclone compliance failures void your insurance, and a 10-day contract clause can lock you in permanently if you miss a deadline.

— Less Than a Single Building and Pest Inspection

A building and pest inspection in Darwin costs $800 to $1,000+. Stamp duty on a $550,000 established home in the NT exceeds $23,000. Losing the $50,000 HomeGrown grant because you rented the property out 11 months in costs $50,000. An insurance claim denied because of an uncertified veranda extension can cost the entire replacement value of the structure. A Mastotermes infestation in an unprotected home can cause structural damage requiring tens of thousands in remediation.

This guide does not replace your conveyancer. But it gives you the grant stacking calculations, stamp duty comparison tables, cyclone certification checklists, termite due diligence protocols, and REINT contract strategies that ensure you identify every Territory-specific risk before you sign a contract — not when the insurance company denies your claim, the council orders a demolition, or the 10-day deadline passes without you realising it.

If it saves you from a single uncertified renovation that voids your insurance, a single missed inspection deadline that locks you into a contract, or a single miscalculation that costs you the $50,000 grant, it pays for itself before you finish reading it.

30-day money-back guarantee. If the guide does not sharpen your due diligence and protect your deposit in the Territory's property market, you pay nothing.

Download the free Northern Territory Quick-Start Home Buying Checklist to see the step-by-step framework covering pre-approval, house hunting, inspections, and settlement. When you are ready for the full grant stacking calculations, cyclone certification checklists, termite due diligence protocols, and REINT contract strategies, the complete guide is here.

The grants are the most generous in Australia. The hazards are unlike anywhere else. This guide makes sure you claim the first without being caught by the second.