You Have Researched the $30,000 Grant, the Stamp Duty Exemption, and the Federal Deposit Schemes. You Still Cannot Calculate What You Will Actually Pay to Buy in Queensland.

You have read the Queensland Revenue Office eligibility page for the First Home Owner Grant. You have looked at house-and-land packages in Ripley and townhouses in Toowong. You may have seen the Reddit thread about a buyer whose builder quoted $720,000, then added fencing, landscaping, and a driveway upgrade that pushed the contract to $753,000 — wiping out the entire $30,000 grant. Or the Whirlpool post about someone who bought a unit in a body corporate scheme and received a $14,000 special levy notice eight months after settlement because the sinking fund was depleted and nobody told them how to read the Form 33 certificate.

The problem is not a lack of information. The Queensland Revenue Office covers the FHOG. Brisbane City Council publishes flood maps. The QBCC has termite management guides. But no single resource explains how the $750,000 FHOG price cap interacts with building contract variations, how the 1 May 2025 stamp duty reforms create a financial gap of over $26,000 between new builds and established homes at $900,000, how overland flow paths — the flood risk that does not appear on the main combined flood maps — can make a property uninsurable, or why a missing Form 36 gives you the legal right to walk away from a pool property contract at any point before settlement.

The Queensland First Home Buyer Guide is a Queensland Due Diligence System — a single, structured reference that maps every grant, concession, environmental hazard, legal disclosure, and settlement trap into a step-by-step process you work through before you sign a contract. It replaces weeks of cross-referencing government portals, forum posts, and broker marketing with a reference that tells you exactly what to check, exactly what the numbers should look like, and exactly where Queensland-specific deals fall apart.

What's Inside the Queensland Due Diligence System

A comprehensive guide, a quick-start checklist, and 8 standalone worksheets and reference cards (10 PDFs) — covering every stage from calculating your true borrowing power through to collecting your keys, built specifically for the grants, hazards, and legal frameworks that make buying in Queensland different from every other Australian state:

The $30,000 FHOG and the Building Contract Variation Trap

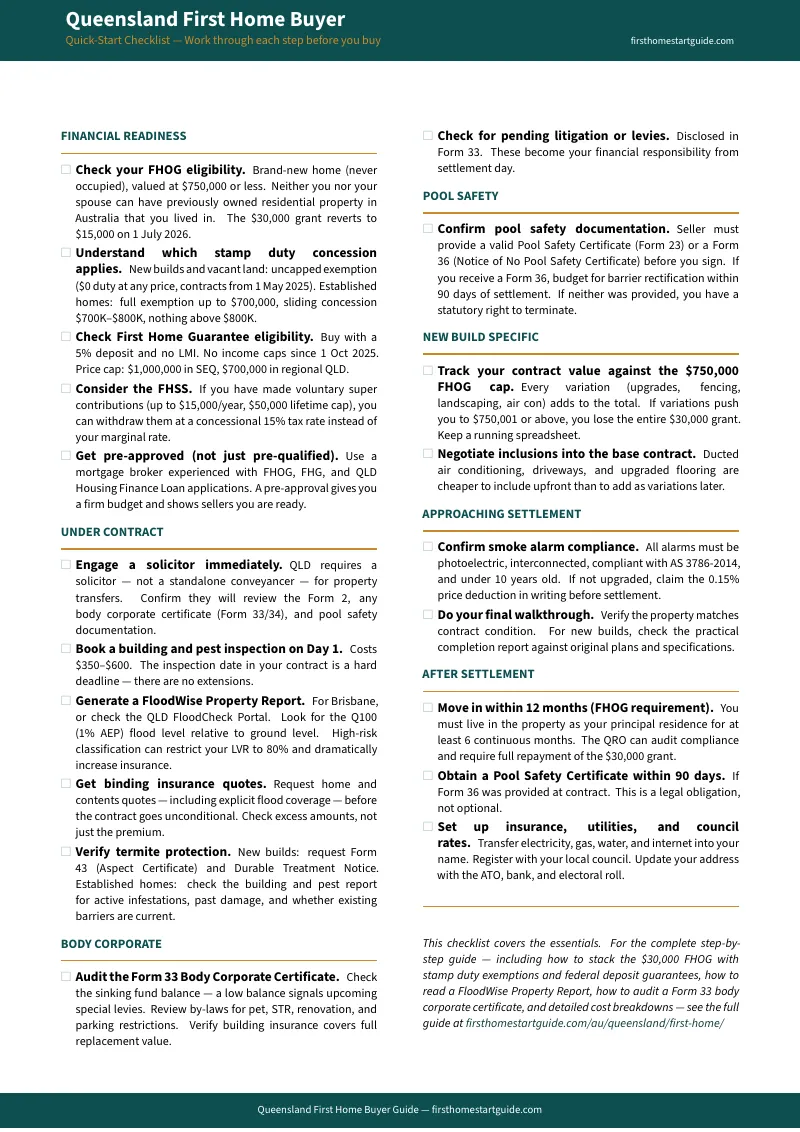

The Queensland First Home Owner Grant is the largest state grant in Australia — $30,000 in tax-free cash for new homes under $750,000 with contracts signed before 30 June 2026. But the price cap is absolute. Builders quote a base price, then add site costs, premium fixtures, fencing, and landscaping as extras. A $720,000 base price plus $31,000 in variations means $0 in grant money. The guide walks through every eligibility rule — the new-home-only restriction, the contract date window, the 12-month move-in and 6-month residency requirements — and shows you how to audit your building contract line by line so a $2,000 upgrade does not cost you $30,000.

Stamp Duty After the 1 May 2025 Reforms

Queensland rewrote the transfer duty rules for first home buyers in May 2025. New builds now attract zero stamp duty with no upper price cap — a first home buyer purchasing a $900,000 new home pays $0 in transfer duty while the same buyer purchasing a $900,000 established home pays $26,350. For established homes, the full exemption applies up to $700,000, with a sliding concession between $700,001 and $800,000 that disappears entirely at $800,000. The guide includes a comparison table at every major price point so you can see the exact dollar difference between new build and established in your price range — not a generic claim that "new builds are cheaper."

Federal and State Deposit Scheme Stacking

The First Home Guarantee lets you purchase with a 5% deposit and no Lenders Mortgage Insurance, with price caps of $1,000,000 in Brisbane, the Gold Coast, and the Sunshine Coast. The Boost to Buy shared equity scheme has the government contributing up to 30% of the purchase price for new homes, reducing your deposit to 2%. The Family Home Guarantee gives single parents access with a 2% deposit and 5,000 places. The guide maps out how to stack these federal and state programs with the $30,000 FHOG and the stamp duty exemption — showing you the exact combination that compresses your upfront cash requirement to its minimum for your specific purchase price and location.

The BCC FloodWise Report — How to Read the Document That Determines Your Insurance Bill

Brisbane sits on a floodplain with creek, river, storm tide, and overland flow flooding — four distinct hazard types, each with different insurance and lending implications. The guide walks you through every element of the Technical FloodWise Property Report: Australian Height Datum (AHD) elevations, Annual Exceedance Probability (AEP) bars colour-coded by flood type, the minimum habitable floor level calculation, and the overland flow path flag that does not appear on the main combined flood extent maps. A property with an overland flow flag can face insurance premiums that add thousands per year to your holding costs or outright exclusions for flood damage. You will know how to read this report before you attend a single open home.

Termite Protection, QBCC Compliance, and Inspection Costs

In Queensland's subtropical climate, termites are a structural threat, not a cosmetic nuisance. A standard pest inspection costs $200 to $400, but skipping it can mean inheriting damage where chemical soil barrier remediation alone runs $500 to $2,000+. For new builds, the guide covers the three documents your builder must provide under AS 3660.1 — the Form 43 Aspect Certificate, the Durable Treatment Notice on the meter box, and the 75mm visual inspection zone — so you can verify compliance before final payment. For established homes, it covers what to look for in inspection reports and how to negotiate repairs or price reductions based on findings.

Cyclonic Wind Ratings for North Queensland Buyers

If you are buying in Townsville, Cairns, or anywhere in North or Far North Queensland, the property's cyclonic wind rating determines its construction standard, insurance premium, and resale value. Wind Regions C and D require ratings from C1 to C4, involving heavy-duty framing, specialised roof battens, and reinforced foundations. Homes built before the mid-1980s may not meet current cyclonic standards and can be difficult to insure at any price. The guide explains how to verify a property's wind classification and what a C2 or C3 rating means for your annual costs.

The Seller Disclosure Scheme and Your Termination Rights

From 1 August 2025, sellers must provide a completed Form 2 (Seller Disclosure Statement) with all prescribed certificates before the buyer signs a contract. If the form is missing, incomplete, or inaccurate on a material matter, you have a statutory right to terminate at any time before settlement. The guide explains what the Form 2 covers, what counts as a material matter, and how this disclosure requirement gives you a legal exit route that most first home buyers do not know exists.

Body Corporate Certificates — Auditing Sinking Funds Before You Buy

If you are buying a townhouse, unit, or duplex in a Community Titles Scheme, the body corporate's financial health becomes your financial problem on settlement day. Outstanding levies, depleted sinking funds, and unapproved common property improvements all transfer to the new owner. The guide explains how to read a Form 33 certificate (or Form 34 for two-lot schemes), how to audit the administration and sinking fund balances, how to check consolidated by-laws for restrictions, and how to identify the warning signs of a body corporate heading for a special levy.

The Pool Safety Termination Trap

When a Queensland property with a pool is sold without a valid Pool Safety Certificate (Form 23), the seller must issue a Form 36 (Notice of No Pool Safety Certificate) before contract signing. If the seller fails to provide Form 36 and does not supply a valid Form 23 by settlement, you have a statutory right to terminate the contract at any point before settlement. If you buy with a Form 36, you inherit a 90-day obligation to bring the pool into compliance — fencing rectification and inspection costs can run into thousands. The guide shows you how to check the QBCC pool register, how to use the absence of a certificate in negotiations, and what to budget for post-settlement compliance.

New Build vs Established: The Full Financial Comparison

Side-by-side worked examples at $500,000, $700,000, and $900,000 showing FHOG eligibility, stamp duty liability, deposit requirements, and total upfront costs for new builds versus established homes. At $900,000, a first home buyer purchasing a new build saves over $26,000 in stamp duty alone compared to an established home — a financial gap that did not exist before the May 2025 reforms. These are not generalised estimates; they are Queensland-specific calculations with the current rate tables applied.

Conveyancing, Settlement, and Post-Purchase Setup

The full settlement timeline from contract exchange to key handover: 30 to 42 days in Queensland, handled by a conveyancer or solicitor. Contract conditions you should always include, conditions you should never waive, building and pest inspection scheduling, and the immediate post-settlement obligations — FHOG residency compliance (move in within 12 months, live there for 6 months continuously), insurance activation, body corporate levy payments, annual termite inspections, and first-year budget planning for the real cost of owning a home in Queensland.

Who This Guide Is For

- Brisbane renters paying $500 to $700 per week who are ready to buy but cannot work out whether the FHOG, stamp duty exemption, and federal guarantee schemes add up to enough to bridge the gap between their deposit and what the market demands

- Buyers choosing between a house-and-land package in Ripley, Logan, or Caboolture and an established townhouse in a middle-ring suburb who need the actual dollar comparison — FHOG eligibility, stamp duty, deposit requirement — at their specific price point

- First home buyers targeting properties near the $750,000 FHOG cap who need to understand how building contract variations silently push you past the threshold and cost you $30,000

- Anyone buying a unit or townhouse in a body corporate scheme who needs to audit the sinking fund, check for unapproved common property improvements, and know whether the body corporate is financially healthy or heading for a special levy

- Buyers looking at properties in Brisbane flood zones who need to read a FloodWise report, interpret AEP probability bars, and check for overland flow flags before making an offer

- North Queensland buyers in Townsville or Cairns who need to verify cyclonic wind ratings and assess whether a property meets current construction standards

Why Not Free Resources?

Free information on buying your first home in Queensland exists across a dozen government websites. Here is what it actually delivers:

- The Queensland Revenue Office publishes FHOG eligibility rules, transfer duty calculators, and application forms. It does not warn you about the building contract variation trap — the mechanism that causes real buyers to lose $30,000 because their builder added $31,000 in site costs and upgrades to a $720,000 base price. You get the rules without the practical scenarios that explain how people fail them.

- Brisbane City Council's Flood Awareness Hub lets you generate a FloodWise report. It does not explain how to interpret AEP probability bars, what the difference between creek and river flooding means for insurance pricing, or why overland flow paths — which do not appear on the main combined flood maps — are the risk most likely to make a property unaffordable. You get the raw data without the interpretation that makes it useable.

- The QBCC publishes termite management guides and pool safety rules. It does not connect these to buying decisions — it does not explain how a missing Form 36 gives you a termination right, how to use a pest inspection finding to negotiate a price reduction, or what the three post-construction documents from your builder should contain. You get the regulation without the buyer strategy.

- Reddit, Whirlpool, and Facebook groups contain real buyer experiences mixed with advice that predates the May 2025 stamp duty reforms, the August 2025 Seller Disclosure Scheme, or the latest FHOG policy. A thread from 2024 explaining stamp duty thresholds does not reflect the uncapped new-build exemption. Sorting current from outdated takes longer than reading a guide that has already done it.

This guide fills the Queensland-specific gap — the space between knowing you want to buy a first home and knowing how to navigate a state where a $30,000 grant has a hard price cap with a looming deadline, stamp duty rules changed fundamentally in May 2025, flood risk varies at the individual-property level, and legal disclosure requirements can give you termination rights that most buyers do not exercise because they do not know they exist.

— Less Than a Single Building and Pest Inspection

A building and pest inspection in Queensland costs $200 to $400. Stamp duty on a $750,000 established home is approximately $10,925. Losing the $30,000 FHOG because your building contract crossed the $750,000 cap costs $30,000. A special levy from a body corporate with a depleted sinking fund can run $5,000 to $20,000. A property in an overland flow zone can add thousands per year in insurance premiums — or make flood coverage unavailable entirely.

This guide does not replace your conveyancer. But it gives you the grant stacking calculations, stamp duty comparison tables, flood risk interpretation framework, legal disclosure checklists, and body corporate audit process that ensure you identify every Queensland-specific risk before you sign a contract — not when the QRO assessment arrives, the insurance quote comes back, or the body corporate issues a special levy notice.

If it saves you from a single contract variation that crosses the $750,000 cap, a single flood zone purchase you would not have checked, or a single body corporate with a depleted sinking fund, it pays for itself before you finish reading it.

30-day money-back guarantee. If the guide does not sharpen your due diligence and protect your deposit in Queensland's property market, you pay nothing.

Download the free Queensland Quick-Start Home Buying Checklist to see the step-by-step framework covering pre-approval, house hunting, inspections, and settlement. When you are ready for the full grant stacking calculations, flood risk interpretation guide, legal disclosure checklists, and body corporate audit process, the complete guide is here.

The grants are generous. The hazards are real. This guide makes sure you claim the first without being caught by the second.