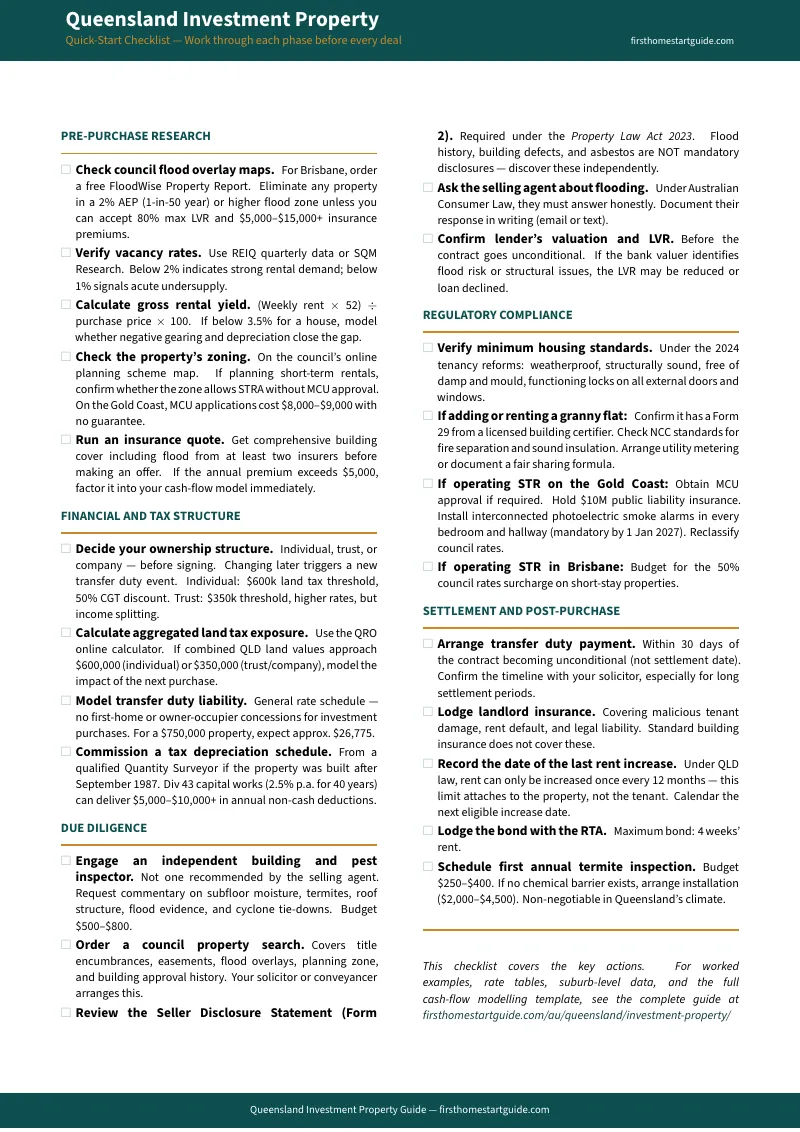

The Yield Looks Strong on Paper. Queensland's Land Tax Aggregation, Flood Zone LVR Caps, and $15,000 MCU Fines Will Correct That.

You found a townhouse in Springfield projecting 5.8% gross yield. Or a detached house in North Lakes where the price-to-rent ratio is half of what you'd pay in Sydney. Or a coastal apartment on the Gold Coast where Airbnb occupancy runs at 84% and there's no state-level short-stay booking levy. The numbers clear. The population growth is structural — 662,000 new residents arriving in South-East Queensland by 2031. The 2032 Olympics are a capital growth catalyst you can actually model. You're ready to move.

Then Queensland's layered regulatory reality arrives. Your two investment properties — one valued at $420,000 and the other at $220,000 — don't individually trigger land tax. But the Queensland Revenue Office aggregates their site values to $640,000, and now you're paying a progressive tax bill you didn't budget for. Your trust structure? Even worse — the tax-free threshold drops from $600,000 to $350,000, and trust rates start at 1.7% above that limit. Your Gold Coast holiday let generates strong weekly cash flow until the council discovers you're operating an unhosted short-term rental in a residential zone without Material Change of Use approval — fines run from $1,000 to $15,000 for individuals, $75,000 for corporations. Your Brisbane investment looks solid until you check the 5-metre resolution flood map and discover the property sits in a 2% AEP zone — insurance premiums jump to $5,000-$15,000 annually, banks cap your LVR at 80%, and in the 5% AEP zone next door, lenders decline finance entirely.

Here's what no single free resource explains: Queensland layers a progressive land tax system that aggregates across all your holdings (punishing multi-property investors who structure incorrectly), against flood zone mapping that directly determines your insurance costs and bank lending limits (5-metre resolution means the house across the street can have a completely different risk profile), against short-term rental frameworks that differ fundamentally between Brisbane and the Gold Coast (Brisbane's scrapped permit scheme still left a 50% rates surcharge in place; the Gold Coast requires MCU planning approval in residential zones but has no night caps), against a tenancy reform program that has introduced new penalty structures in three legislative phases since June 2024 — including $3,338 fines for failing to disclose rent payment commissions. Each of these has cost real investors five to six figures because the information existed — scattered across QRO calculators, council flood maps, RTA compliance guides, and PropertyChat threads — but nobody had assembled it into a single underwriting system calibrated to Queensland.

The Queensland Investment Property Guide is a Queensland Investor Underwriting System — not a motivational overview of Australian real estate, but a structured due diligence framework that maps every Queensland-specific financial trap, regulatory restriction, and tax structuring mechanic into a process you work through before you commit capital. It replaces months of cross-referencing QRO rate tables, council planning portals, RTA reform bulletins, and forum posts with a single reference that tells you exactly what to verify, exactly what the numbers should look like, and exactly where deals go wrong in this state.

What's Inside the Queensland Investor Underwriting System

A comprehensive guide, four standalone worksheets, and a quick-start checklist (six PDFs total) — covering every stage from market selection through post-purchase landlord compliance, built specifically for the regulatory mechanics and tax structures that make Queensland different from every other Australian state:

Land Tax Aggregation Mechanics and Entity Structuring

Queensland's progressive land tax system aggregates the unimproved value of every piece of freehold land you hold on 30 June — not per property, but per entity. Two properties worth $420,000 and $220,000 individually look safe under the $600,000 individual threshold, but the QRO combines them to $640,000 and sends you a bill. Hold those same properties in a family trust and the threshold drops to $350,000, with standard trust rates starting at 1.7% — meaning a combined value of $640,000 triggers a significantly higher annual liability than individual ownership. Foreign companies and trusts face a 3% surcharge on top of corporate rates above $350,000. The guide walks through every rate tier for individuals, companies, trusts, and foreign entities, maps the crossover points where different holding structures become cheaper or more expensive, and shows you how to model the land tax impact before you sign a contract — not when the QRO assessment arrives twelve months later.

Transfer Duty Calculations and Closing Cost Model

Queensland charges transfer duty on a sliding scale up to 5.75% for investment properties — no first-home concession applies when you're buying as an investor. On a $750,000 investment property, duty runs approximately $26,775. The guide breaks down every tier of the progressive duty schedule, shows the additional foreign acquirer surcharge (8% for non-residents), and models the full closing cost stack including solicitor or conveyancer fees, title search, council and water rate adjustments, building and pest inspection costs, and lender fees. Your pro-forma closing cost model should match reality to within a few hundred dollars — not discover a five-figure duty bill at settlement.

Flood Risk Due Diligence and LVR Impact Framework

After 2011 and 2022, Queensland insurers moved to high-resolution 5-metre flood mapping that prices risk on an individual property basis. Two houses on the same street can have fundamentally different insurance premiums. A property in a 2% AEP (1-in-50-year) flood zone faces premiums of $5,000 to $15,000 annually and bank LVR caps at 80% — requiring a larger deposit. A property in a 5% AEP (1-in-20-year) zone is generally declined by standard commercial lenders entirely. The guide details how to read Brisbane City Council flood awareness maps, how Annual Exceedance Probability categories map to specific bank lending criteria, the four mandatory conditions lenders enforce on flood-affected properties (existing habitable structure, floor height above modelled flood, Certificate of Currency with explicit flood cover, independent valuer approval), and how to run a pre-purchase flood risk assessment that catches the properties that will destroy your cash flow before you're under contract.

Short-Term Rental Compliance: Brisbane vs Gold Coast

Brisbane and the Gold Coast operate under fundamentally different short-term rental frameworks — and investors who assume one set of rules applies everywhere get caught. Brisbane scrapped its proposed permit scheme in May 2026 but continues to enforce a 50% rates surcharge on short-stay properties. The Gold Coast doesn't charge a rates surcharge but requires properties used for unhosted short-term rentals in residential zones to obtain Material Change of Use (MCU) planning approval — a formal, impact-assessable application in low-density zones. Properties in designated tourism zones (Surfers Paradise, Broadbeach) are typically code-assessable or pre-approved. The guide maps which zones require MCU, which are code-assessable, the correct council rates category registration process (which functions as an annual rental license on the Gold Coast), noise and quiet hour rules (10 PM to 7 AM), "party house" zone enforcement, body corporate protections under Section 180 of the BCCMA, and the smoke alarm interconnection deadline of 1 January 2027. Operate without this framework and fines start at $1,000 — corporations face up to $75,000.

Tenancy Law Reform Compliance Matrix

Queensland has rolled out three phases of tenancy reform since June 2024 under the Residential Tenancies and Rooming Accommodation and Other Legislation Amendment Act 2024, and each phase introduced new compliance obligations with real penalty exposure. From June 2024: rent increases capped to once every 12 months per property (not per tenancy), and rent bidding banned. From September 2024: mandatory Minimum Housing Standards (weatherproof, structurally sound, free of damp and mould), and maximum bonds capped at four weeks' rent regardless of weekly amount. From May 2025: minimum notice for routine entries increased from 24 to 48 hours, entries limited to two per week after a notice to end tenancy, standardised application forms (Form 22/R22) mandatory with at least one fee-free submission method, and landlords must disclose in writing any financial benefit from requiring a specific rent payment method — penalty for non-disclosure: 20 penalty units ($3,338). The guide consolidates every obligation, deadline, and penalty into a single compliance reference so you're not discovering them via an RTA notice.

Secondary Dwelling and Granny Flat Rules

Adding a secondary dwelling is one of the most effective yield-boosting strategies in Queensland — but the rules vary significantly by council. The guide covers the Queensland Development Code provisions for secondary dwellings, council-specific lot size and floor area requirements, fire separation and building code standards, how secondary dwellings interact with land tax calculations (the improvement adds value, but the unimproved land value drives the tax), and when a secondary dwelling triggers an MCU application versus falling under accepted development. It also addresses the rental income implications — a legal secondary dwelling generates assessable income that must be structured correctly across your ownership entity.

Growth Corridor and Suburb-Level Investment Analysis

South-East Queensland's $137 billion infrastructure pipeline creates identifiable growth corridors — but not every suburb along a rail line or highway extension will appreciate equally. The guide analyses the Cross River Rail station catchments (Woolloongabba, Boggo Road, Roma Street), Springfield corridor, North Lakes, Sunshine Coast rail extension, and regional high-yield centres (Townsville at 7.8%-12.6% gross yields, Hervey Bay, Mackay, Gladstone). For each corridor, it maps current median prices, vacancy rates, rental yields, population growth projections, and the 2032 Olympics infrastructure that will directly impact property values — separated from the speculative hype that follows every host city announcement. Historical data from previous Olympic host cities gives you the growth pattern to expect: acceleration leading into the Games, consolidation afterward, and which property segments capture the most durable gains.

Settlement Process and Post-Purchase Setup

Queensland settlements run 30-42 days and are handled by a conveyancer or solicitor. The guide covers the full timeline from contract exchange to settlement, including the mandatory building and pest inspection (critical in Queensland — termite risk is materially higher than in southern states), cooling-off period mechanics and waiver implications, body corporate records review for strata properties, insurance activation timing, rental management setup, and the immediate post-settlement compliance steps: smoke alarm certification, pool safety compliance (if applicable), and landlord registration with the RTA. It also covers the FHOG ($30,000 for new builds — the highest nationally) and how owner-occupier concessions interact with investment property structuring.

Who This Guide Is For

This guide is for property investors targeting Queensland markets who:

- Are investing from Victoria or New South Wales and executing a regulatory arbitrage strategy — escaping Victoria's frozen $1,075,000 land tax threshold, COVID-19 debt levy, and 7.5% short-stay booking levy for Queensland's $600,000 individual threshold and uncapped Gold Coast rental nights — but need to understand the aggregation mechanics, transfer duty schedules, and flood risk frameworks that apply before they deploy capital 1,000 kilometres from home

- Are local South-East Queensland wealth builders using infrastructure-led growth — Cross River Rail, Sunshine Coast rail, the 2032 Olympics pipeline — to expand a rental portfolio and need to model how land tax aggregation, tenancy reform penalties, and council-specific secondary dwelling rules affect their actual net yield as holdings grow

- Want to operate short-term rentals on the Gold Coast or in Brisbane and need to verify which council framework applies, whether they need MCU planning approval, what the correct rates category registration process looks like, whether body corporate bylaws can override their rental strategy under Section 180 of the BCCMA, and what happens when the smoke alarm interconnection deadline arrives on 1 January 2027

- Are self-managing landlords navigating Queensland's three-phase tenancy reform and need every obligation — notice periods, entry limits, standardised forms, rent payment disclosure, housing standards — consolidated in one reference with the specific penalty amounts attached, not scattered across RTA media releases and parliamentary schedules

- Are evaluating a property in Brisbane and need to read a 5-metre resolution flood map before making an offer — verifying the AEP rating, its impact on insurance premiums, and whether their target LVR is even possible given the lender restrictions that apply to that specific parcel

- Want every Queensland-specific regulation, tax calculation, and due diligence requirement in one reference — instead of assembling it from QRO calculators, council flood portals, RTA reform bulletins, REIQ reports, and PropertyChat threads that may predate the May 2025 tenancy reforms or Brisbane's May 2026 permit scheme reversal

Why Not Free Tools and Forums?

Free information on Queensland property investing exists. Here's what it actually delivers:

- QRO calculators and guides give you the tax-free thresholds and rate tables. They don't explain how aggregation catches multi-property investors who thought each property was assessed separately, don't compare the dollar impact of individual versus trust versus company ownership at different portfolio values, and don't walk you through the structuring decisions that determine whether your land tax bill is manageable or corrosive. You get the rate schedule without the strategy that makes it useable.

- REIQ quarterly reports provide median prices, historical growth percentages, and vacancy rates by region. They don't tell you which suburbs along the Cross River Rail corridor are already priced in, don't model how flood risk in specific catchments changes the effective yield, and don't connect macro data to individual purchase decisions. You get the market summary without the underwriting framework that turns it into action.

- Corporate educational content (builders, mortgage brokers, property managers) highlights the 2032 Olympics, SEQ population growth, and strong rental demand. It minimises flood zone LVR caps, progressive land tax aggregation, MCU planning requirements, and tenancy reform penalties — because that content is designed to generate leads, not to help you identify reasons not to buy. The guide covers both sides.

- PropertyChat and Reddit threads (r/AusPropertyChat, r/AusFinance) contain genuinely useful investor experience reports mixed with advice that predates the May 2025 tenancy reforms, Brisbane's May 2026 permit scheme reversal, and the latest QRO rate schedules. A 2023 thread explaining Gold Coast STRA rules may not reflect the current MCU requirements. Sorting current from outdated takes longer than reading a guide that has already done it.

This guide fills the Queensland-specific gap — the space between knowing how to analyse a rental property in general and knowing how to underwrite one in a state where land tax aggregation catches multi-property portfolios, flood zone mapping directly determines your bank lending terms, short-term rental frameworks differ between Brisbane and the Gold Coast in ways that can generate $75,000 in corporate fines, and a three-phase tenancy reform program has rewritten landlord obligations faster than most forums can track. It's the analysis that would take a Queensland property solicitor, a specialist tax adviser, and a local planning consultant to assemble — structured as a reference you own permanently.

— Less Than One Building and Pest Inspection

A single building and pest inspection in Queensland runs $400 to $700. Transfer duty on a $750,000 investment property is approximately $26,775. A flood insurance premium on a property in a 2% AEP zone costs $5,000 to $15,000 per year. A trust structure that triggers the $350,000 land tax threshold instead of the $600,000 individual threshold can cost $8,250 or more annually in additional tax. An unapproved short-term rental operation on the Gold Coast faces fines starting at $1,000 per offence.

This guide doesn't replace your conveyancer or your tax adviser. But it gives you the land tax aggregation model, flood risk due diligence framework, short-term rental compliance matrix, tenancy reform reference, and growth corridor analysis that ensure you identify every Queensland-specific risk before you're contractually committed — instead of discovering them on your first QRO assessment, your first insurance renewal, or your first council enforcement notice.

If it catches a single land tax structuring mistake, prevents a single flood zone miscalculation, or saves you from operating a short-term rental without the correct council approval, it pays for itself before you've finished reading it.

30-day money-back guarantee. If the guide doesn't sharpen your underwriting and protect your capital in Queensland's regulatory environment, you pay nothing.

Download the free Queensland Quick-Start Investment Property Checklist to see the due diligence framework covering pre-purchase research, financial analysis, flood risk assessment, closing, and post-purchase setup. When you're ready for the full land tax structuring model, flood zone LVR framework, short-term rental compliance matrix, and growth corridor analysis, the complete guide is here.

The yield looks strong on the spreadsheet. This guide tells you whether Queensland agrees.