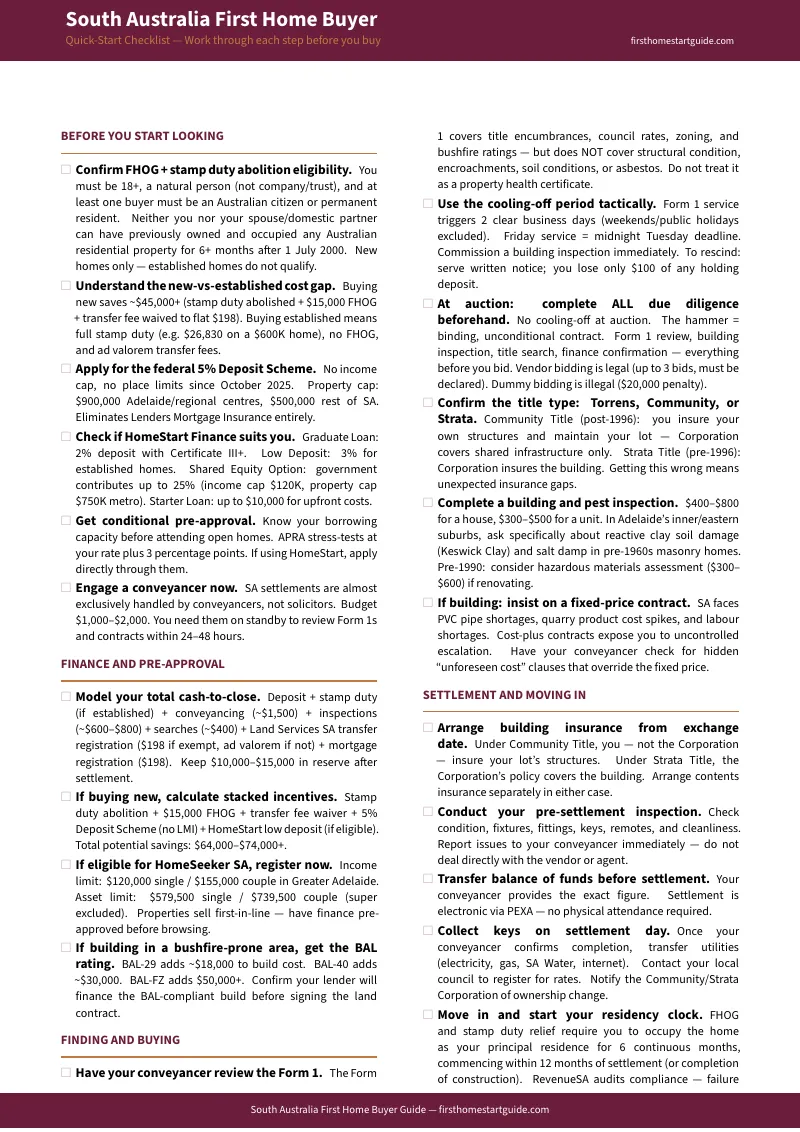

You Have Run the RevenueSA Stamp Duty Calculator, Read the FHOG Eligibility Page, and Browsed Fifty House-and-Land Packages in Playford. You Still Cannot Work Out Whether That $550,000 New Build Saves You $42,000 or $47,000 Compared to the Established Home Down the Street — Because No Single Resource Explains How to Stack Stamp Duty Abolition, the $15,000 Grant, a 2% HomeStart Deposit, and the Federal 5% Scheme Together, and the Form 1 Your Conveyancer Mentioned Is Not the Property Health Certificate You Think It Is.

You have looked at house-and-land packages in Munno Para West and townhouses in Morphettville. You have compared land allotments in Playford Alive and off-the-plan apartments in the CBD. You have tried to figure out whether a $259,000 HomeSeeker SA block plus a $350,000 build contract gets you a better outcome than a $600,000 established home in Prospect — knowing one path saves you tens of thousands in government incentives and the other charges you $26,830 in stamp duty alone. You may have seen the r/Adelaide thread about a couple who bought a Community Title townhouse assuming the Corporation covered building insurance — and discovered after a roof leak that they were individually liable for every structure on their lot. Or the post about a first home buyer who signed a cost-plus building contract in 2024 and watched the final price climb $68,000 above the estimate because PVC pipe shortages and quarry product costs blew out the budget with no contractual ceiling.

The problem is not a shortage of information. RevenueSA publishes the stamp duty rates and FHOG rules. Consumer and Business Services SA describes the Form 1. HomeStart Finance lists its loan products. But no single resource models how the complete stamp duty abolition for new builds, the uncapped $15,000 FHOG, HomeStart's 2% Graduate Loan, the Shared Equity Option, and the federal First Home Guarantee interact — where they stack, where they conflict, and what the total cash-to-close looks like when you combine all of them versus buying established. Nobody explains that the Form 1 does not cover structural condition, soil quality, encroachments, or asbestos — so the two clear business days it triggers are your only window to commission the inspections that actually tell you whether the property is sound. Nobody warns you that building on a scenic Adelaide Hills block rated BAL-40 adds $30,000 in mandatory construction costs that your lender may not have factored into your borrowing capacity.

The South Australia First Home Buyer Guide is an SA Incentive Stacking System — a single reference that maps every grant, every stamp duty formula, every Form 1 tactical window, every title insurance trap, every construction cost risk, and the full SA buying process into a step-by-step system you work through before you sign any contract, bid at any auction, or commit to any building agreement. It replaces weeks of cross-referencing government portals, Reddit warnings, conveyancer blogs, and mortgage broker marketing with a document that tells you exactly what to stack, exactly what the numbers should look like, and exactly where South Australia-specific transactions fall apart.

What's Inside the SA Incentive Stacking System

A comprehensive guide, a quick-start checklist, and 8 standalone printable worksheets and reference cards — covering every stage from calculating your real borrowing power through to collecting your keys, built specifically for the grants, stamp duty abolition, Form 1 mechanics, title insurance traps, and construction risks that make buying in South Australia fundamentally different from every other Australian state:

The Full Incentive Stack — Every Dollar You Save (and Every Dollar You Lose) on New vs. Established

Stamp duty on a $600,000 established home is $26,830. On a new build at the same price, it is zero. Add the $15,000 FHOG, the waived Land Services SA transfer fee (reduced from thousands to a flat $198), and you are looking at a financial swing of more than $42,000 — before you even consider HomeStart or the federal scheme. But the incentive stack gets more powerful when you layer programs. The guide includes worked cash-to-close calculations showing what happens when you combine stamp duty abolition, the FHOG, a HomeStart Graduate Loan at 2% deposit, and the federal First Home Guarantee at three realistic price points. It also models the Shared Equity Option — where HomeStart contributes up to 25% of the purchase price interest-free and repayment-free — and shows at what income and property price it makes mathematical sense versus a standard low-deposit loan. No government website models any of this for you.

The Form 1 Tactical Guide — What It Actually Covers, What It Hides, and How to Use the 48-Hour Window

Most first home buyers in SA assume the Form 1 vendor disclosure statement is a property health certificate. It is not. It covers encumbrances, zoning, council rates, easements, and bushfire ratings — but it says nothing about structural condition, soil quality, encroachments onto neighbouring properties, or asbestos. The real value of the Form 1 is the cooling-off period it triggers: two clear business days where you can walk away and lose only $100 of your holding deposit. The guide teaches you to use this window tactically — including the Friday service strategy where a Form 1 served on Friday gives you until midnight Tuesday because weekends do not count as business days. It covers what to look for in the Form 1 itself, what inspections to commission immediately upon receiving it, how to serve written notice if you need to rescind, and why signing a waiver certificate or buying at auction eliminates your cooling-off rights entirely.

The Community Title Insurance Trap — Why Your Corporation Does Not Cover What You Think

Since 1996, South Australia has not created new Strata Plans. Almost every townhouse, duplex, and new multi-dwelling development is Community Title — and the insurance rules are the opposite of what most buyers expect. Under a Community Title, the Corporation insures shared infrastructure like driveways and communal lighting. You insure every structure on your lot — the roof, walls, plumbing, and everything in between. Under the older Strata Title, the Corporation insures the entire building. The guide explains exactly how to identify which title type you are buying, what your maintenance and insurance obligations are under each, what questions to ask the Corporation before you sign, and how to avoid the devastating out-of-pocket surprise that hits buyers who assume their Community Title corporation covers building repairs.

The Hidden Costs of Building in SA — BAL Ratings, Reactive Clay, and Fixed-Price Contract Defence

Government incentives push first home buyers hard toward new builds. But building in South Australia carries site-specific costs that no promotional brochure mentions. In the Adelaide Hills, a BAL-12.5 rating adds approximately $5,000 to construction costs. BAL-29 adds $18,000. BAL-40 adds $30,000. BAL-FZ (Flame Zone) adds $50,000 or more — for fire-retardant timbers, specialised glazing, and engineered foundations you cannot avoid. In Adelaide's inner and eastern suburbs, Keswick Clay — reactive soil that swells and shrinks by up to 50% — cracks foundations of older homes and demands reinforced concrete raft slabs for new construction. Pre-1960s masonry homes are vulnerable to salt damp, where saline groundwater wicks up through permeable mortar and destroys walls from the inside — remediation costs $5,000 to $30,000. The guide covers how to check the BAL rating before committing to land, how to request a soil test report, and why you must insist on a fixed-price building contract in a market where PVC pipe shortages and quarry product cost spikes have turned cost-plus contracts into open-ended financial liabilities.

HomeStart Finance Deep Dive — Graduate Loan, Shared Equity, Starter Loan, and the Repayment Safeguard

HomeStart is Australia's only state-backed lender offering 2% deposit home loans. The Graduate Loan lets you buy with just 2% down if you hold a Certificate III or higher — no LMI, no private mortgage insurance. The Low Deposit Loan drops the requirement to 3% for established homes. The Shared Equity Option lets the government put up 25% of the purchase price as an interest-free, repayment-free loan — repaid only when you sell, refinance, or choose to buy out the share. The Starter Loan covers up to $10,000 in upfront costs. And the Repayment Safeguard calculates your initial repayments on affordability rather than a fixed loan term, insulating you from rate hikes for 12-month periods. The guide maps every product's eligibility criteria, income caps, property price caps, and how each one interacts with the FHOG and federal schemes — so you choose based on mathematics, not marketing.

Auction Survival — Vendor Bids, No Cooling-Off, and the Due Diligence Deadline

At auction in South Australia, there is no cooling-off period. The hammer falls, you are contractually bound — no finance clause, no building inspection condition, no escape. Vendor bidding is legal: the auctioneer can place up to three bids on behalf of the seller, and each must be declared aloud. Dummy bidding — undisclosed associates inflating the price — is illegal and carries a $20,000 penalty. But if you cannot distinguish a declared vendor bid from the crowd's genuine competition, you will overbid. The guide covers the complete pre-auction due diligence checklist (Form 1 review, building inspection, title search, finance confirmation — everything before you raise your hand), how to set a maximum bid based on comparable sales rather than the agent's price guide, and the psychological traps that cause first home buyers to exceed their limit.

Full Cost Worksheet with Three Worked Scenarios

A fillable worksheet covering deposit, stamp duty (zero for new builds, full rate schedule for established), LMI, conveyancing fees, building and pest inspections, searches, Land Services SA transfer registration, mortgage registration, and post-settlement costs. Three pre-worked scenarios: a $550,000 new house-and-land package with full incentive stacking (stamp duty abolished + FHOG + HomeStart Graduate Loan), a $600,000 established home showing the full government cost burden, and a $480,000 off-the-plan apartment showing how construction cost deductions apply. Plus a blank worksheet for your own target property. Your budget is not what the bank will lend you — it is the total cash you need on settlement day plus a $10,000 to $15,000 safety buffer.

Who This Guide Is For

- Adelaide renters and savers earning $60,000 to $200,000 who cannot work out whether a $550,000 house-and-land package in Playford, a $480,000 off-the-plan apartment in the city, or a $600,000 established home in a middle-ring suburb leaves them with more cash after stacking every available scheme

- Anyone deciding between a new build and an established home who needs to see the exact dollar gap — $42,000 to $47,000 or more in government costs — before committing to a path that determines their entire purchasing power

- First home buyers looking at house-and-land packages in Playford, Aldinga, Mount Barker, or Angle Vale who need to understand BAL ratings, soil classifications, fixed-price contract protections, and construction delay risks before signing a building agreement

- Buyers considering a townhouse or unit who need to understand whether they are buying Community Title or Strata Title — and what that means for their insurance, maintenance obligations, and corporate levies

- Anyone confused by the overlap between the FHOG, stamp duty abolition, HomeStart Finance products, the federal First Home Guarantee, and Help to Buy who needs to see which combinations they qualify for, which produce the lowest cash requirement, and where programs conflict

- Single-income earners who need HomeStart's Shared Equity Option to boost purchasing power without increasing monthly repayments — and need to understand the income caps, property price limits, and repayment triggers before relying on it

- Interstate or international migrants who assume other states' property rules apply in SA — and do not realise that Form 1 cooling-off mechanics, the absence of Strata Plans for new developments, and the total stamp duty abolition for new builds create a fundamentally different buying environment

- Couples relying on parental financial help who need to structure the arrangement correctly — cash gift, guarantor, or living at home rent-free — so their lender accepts the deposit and the arrangement does not create hidden financial stress for either generation

Why Not Free Resources?

Free information on buying your first home in South Australia exists across half a dozen government websites. Here is what it actually delivers:

- RevenueSA publishes the stamp duty rates, the FHOG eligibility criteria, and the June 2024 policy changes. But the information is layered across transitional dates — contracts signed before June 2023, between June 2023 and June 2024, and post-June 2024 — using dense legal definitions of "dutiable value" and "relevant interests." It does not model how the stamp duty abolition, the FHOG, and HomeStart products interact. It does not calculate your total cash-to-close. You get the rules without the financial planning that makes the rules actionable.

- Consumer and Business Services SA describes the Form 1 and the cooling-off framework. It does not explain that the Form 1 covers zero information about structural condition, soil quality, encroachments, or asbestos. It does not teach you the Friday service tactic or how to use the two-day window for rapid inspections. You get the statutory definition without the tactical survival guide.

- HomeStart Finance lists its loan products — Graduate Loan, Low Deposit, Shared Equity, Starter Loan. But each product page describes itself in isolation. There is no comparison across products, no modelling of how each interacts with government grants, no worked scenario showing what your total cash requirement looks like when you combine a 2% Graduate Loan with the FHOG and stamp duty abolition. You get the product descriptions without the decision framework.

- Reddit, Whirlpool, and Facebook groups contain real buyer experiences — but advice from 2023 does not reflect the June 2024 stamp duty abolition, posts about the FHOG still reference the old $650,000 value cap, and eastern-state users describe Section 32 certificates, auction deposit rules, and cooling-off frameworks that do not apply in South Australia. Sorting current from outdated, SA-specific from interstate, takes longer than reading a guide that has already done it.

This guide fills the South Australia-specific gap — the space between knowing you want to buy a first home and knowing how to navigate a state where the government has effectively created a $45,000+ financial incentive for new builds, but surrounded it with Form 1 traps, Community Title insurance gaps, construction cost blowouts, and an auction system where a single mistake is unconditional and irreversible.

— Less Than One Hour of a Conveyancer's Time

A conveyancer in South Australia costs $1,000 to $2,000 for settlement. A building and pest inspection costs $400 to $800. Stamp duty on a $600,000 established home costs $26,830 — money you pay zero on a new build, if you understand how to qualify. A Community Title insurance gap discovered after settlement can cost thousands in uninsured repairs. A cost-plus building contract in a market with material shortages can blow out by tens of thousands with no contractual ceiling. A BAL-40 rating you did not check before buying land in the Adelaide Hills adds $30,000 to your build.

This guide does not replace your conveyancer. But it gives you the incentive stacking calculations, the Form 1 tactical guide, the Community Title insurance checklist, the construction cost defence framework, and the complete cost worksheets that ensure you identify every SA-specific risk before you sign — not when the RevenueSA assessment arrives, the building contract escalates, or the insurance claim is denied.

If it saves you from a single missed incentive you would not have stacked, a single Form 1 gap you would not have caught, or a single insurance trap you would not have spotted, it pays for itself before you finish reading it.

30-day money-back guarantee. If the guide does not sharpen your due diligence and protect your deposit in South Australia's incentive-heavy property market, you pay nothing.

Download the free South Australia Quick-Start Home Buying Checklist to see the step-by-step framework covering pre-approval, incentive eligibility, Form 1 review, and settlement. When you are ready for the full incentive stacking calculations, Form 1 tactical guide, Community Title insurance checklist, construction cost breakdowns, and complete acquisition cost worksheets, the complete guide is here.

The incentives are the most generous in the country. The traps are buried in the details. This guide makes sure you claim the first without falling into the second.