The Yield Clears at 4.5%. South Australia's $25,000 Trust Threshold, Community Title Insurance Trap, and No-Cause Eviction Ban Will Correct That.

You found a northern suburbs house projecting 4.5% gross yield. Or an Elizabeth property where the entry price is half of what you'd pay in Sydney and the vacancy rate sits at 0.6% — the tightest of any capital city in Australia. Or a Salisbury asset near the Edinburgh Defence Precinct where the $30 billion AUKUS submarine program is creating a permanent, high-income tenant pool. The numbers clear. Adelaide is absorbing 22,000 new residents per year. Only 9,700 new dwellings commenced in 2024. The median house price reached $960,000. You're ready to move.

Then South Australia's regulatory reality arrives. Your accountant recommends a discretionary trust for asset protection — a reasonable strategy in most states. But South Australia's land tax trust threshold is $25,000, not $833,000. You're liable from essentially the first dollar of site value, and the designated beneficiary concession closed permanently for any property acquired after October 2019. You find a community-titled townhouse with low quarterly levies and assume the corporation insures the building — as it would in a NSW or Victoria strata scheme. It doesn't. Under the Community Titles Act 1996, the individual lot owner is solely responsible for insuring the physical structure. Your building is uninsured and you don't know it. Your tenant's fixed-term lease expires and you want to renovate. Under the 2024-2026 tenancy reforms, no-cause terminations are abolished — you need prescribed grounds and 60 days' notice, plus a six-month re-letting ban if you terminate to sell. Your conveyancer sends the Form 1 vendor disclosure without verifying the tenancy agreement details. A defective Form 1 gives the buyer the legal right to void the contract entirely, even outside the cooling-off window — catastrophic if you're relying on a synchronised settlement to fund your next acquisition.

Here's what no single free resource explains: South Australia layers a land tax system where the trust threshold sits at $25,000 (triggering liability from the first dollar on post-2019 trust acquisitions) and the aggregation formula for joint owners operates in two stages that most interstate accountants have never modelled, against a title structure where community-titled properties shift building insurance responsibility entirely to the individual owner unlike every other state's strata model, against tenancy reforms that abolished no-cause evictions and imposed a six-month re-letting ban alongside automatic pet approval within 14 days and instant lease termination for domestic abuse victims, against a Form 1 vendor disclosure regime where a single missing tenancy detail can void a completed contract. Each of these has cost real investors five to six figures because the information existed — scattered across RevenueSA calculators, Consumer and Business Services guides, REISA Panorama reports, and PropertyChat threads — but nobody had assembled it into a single underwriting system calibrated to South Australia.

The South Australia Investment Property Guide is a Defence Corridor Investment System — not a motivational overview of Adelaide real estate, but a structured due diligence framework that maps every SA-specific financial trap, regulatory restriction, and tax structuring mechanic into a process you work through before you commit capital. It replaces months of cross-referencing RevenueSA rate tables, CBS tenancy regulations, Land Services SA title records, and forum posts with a single reference that tells you exactly what to verify, exactly what the numbers should look like, and exactly where deals go wrong in this state.

What's Inside the Defence Corridor Investment System

A comprehensive 12-chapter guide and a quick-start checklist — covering every stage from market selection through post-settlement compliance and portfolio scaling, built specifically for the regulatory mechanics and tax structures that make South Australia different from every other Australian state:

Land Tax Calculation, Trust Surcharges, and Entity Structuring

South Australia's land tax regime catches interstate investors who rely on trust structures without understanding the SA-specific rules. The general tax-free threshold for individuals is $833,000 — generous by national standards and enough to hold one or two median-priced houses without triggering any liability. But land held in a discretionary trust faces a threshold of just $25,000, with the designated beneficiary concession permanently closed for post-October 2019 acquisitions. The guide walks through every rate tier, the two-stage aggregation formula for joint owners, worked examples for individual and trust portfolios, the corporate grouping rules for related entities, and the interstate comparison showing exactly how SA's land tax compares to Victoria ($50,000 threshold), Queensland ($600,000), and NSW ($1,075,000) at equivalent portfolio values. You model the impact of your next acquisition before you sign — not when the RevenueSA assessment arrives.

Stamp Duty and the Foreign Ownership Surcharge

South Australia charges a progressive stamp duty up to 5.5% on every investment purchase — no concessions, no relief for investors. A $600,000 property costs $26,830 in duty. Foreign buyers face an additional 7% surcharge ($42,000 on a $600,000 property), bringing total duties to $68,830 — an 11.4% capital deficit at acquisition. The guide covers the full progressive rate schedule with worked examples, the foreign ownership surcharge mechanics, the temporary resident refund pathway (achieve permanent residency within 12 months for a full surcharge refund), and the three-year clawback rule for domestic entities that become foreign persons after acquisition.

Community Title vs. Strata Title: The Insurance Trap

South Australia abolished the creation of new Strata Titles in 1996, replacing them with Community Titles. The critical difference: in a Community Title, the individual lot owner is solely responsible for insuring the physical structure on their lot — the Community Corporation's insurance covers common property only. Interstate investors from NSW or Victoria, where the Owners Corporation insures the entire building, routinely buy community-titled properties and leave the building entirely uninsured. The guide provides a title identification system, insurance obligation comparison across Torrens, Community, and Strata titles, and the specific due diligence steps to verify insurance coverage before settlement.

The Form 1 Vendor Disclosure Process

South Australia's Form 1 is the most consequential document in the purchase process. It triggers the buyer's two-business-day cooling-off period, and a defective Form 1 — one that fails to accurately disclose tenancy agreements, encumbrances, or zoning details — gives the buyer the right to void the contract entirely, even outside the cooling-off window. The guide covers the Form 1 from both sides: what buyers must scrutinise (tenancy disclosures, bond lodgement verification, encumbrance review) and what investor-sellers must audit with their conveyancer to prevent voided contracts that destroy synchronised settlements. It also covers auction exceptions — where the Form 1 must be available for inspection three business days before the auction.

Tenancy Law Reforms (2024-2026) and Compliance Framework

South Australia's tenancy overhaul is the most significant since the Residential Tenancies Act 1995 was enacted. No-cause terminations are abolished — landlords must provide prescribed grounds and 60 days' notice. A six-month re-letting ban applies if you terminate to sell. Tenants can request pets with automatic approval if you fail to respond within 14 days. Domestic abuse victims can break leases with seven days' notice. Rent increases are limited to once every 12 months with 60 days' written notice, and rent bidding is explicitly outlawed. The guide consolidates every obligation into a single reference: prescribed termination grounds, notice periods, bond limits ($800/week threshold), minimum housing standards that must be met before and during tenancy, and the SACAT dispute resolution pathway.

Geographic Investment Strategy: Defence Corridors, Regions, and Risk Zones

The guide analyses South Australia's distinct investment corridors with current medians, vacancy rates, rental yields, and infrastructure catalysts. The northern suburbs — Elizabeth, Salisbury, Davoren Park, Munno Para, Paralowie — offer 4.0% to 4.8% gross yields driven by the Osborne Naval Shipyard and Edinburgh Defence Precinct. The southern suburbs provide lifestyle-driven capital preservation. Regional markets like the Riverland (4.7% to 5.5% yields, 0.17% vacancy) and the Iron Triangle (up to 7.9% yields) offer high cash flow with higher risk. The Adelaide Hills section covers bushfire BAL ratings, CFS referral requirements, fire-rated construction mandates, and the insurance cost multipliers ($2,500 to $4,000+ annually) that transform neutrally geared assets into cash-flow liabilities. Defence Housing Australia lease-back opportunities — 9-to-12-year government-backed leases with guaranteed rental income — are covered as a separate strategy for risk-averse investors.

Portfolio Structuring and Aggregation Modelling

The guide covers five ownership structures — individual, joint, discretionary trust, company, and SMSF — with the land tax implications of each modelled at different portfolio values. It includes the two-stage aggregation formula for joint owners, worked examples showing how a third property can push the entire portfolio above the $833,000 threshold, the interstate diversification strategy (holding SA properties in personal names to maximise the threshold, then expanding into NSW's $1,075,000 threshold), and the specific dangers of corporate grouping where related entities are aggregated regardless of separate legal identities.

The Complete Purchase Process

From engaging a conveyancer ($1,200 to $2,500) through settlement (28 to 42 days), the guide covers every step: title search through Land Services SA, building and pest inspection ($500 to $800), PlanSA planning overlay checks, rental appraisals, the auction rules (no vendor bids — unique to SA), and the settlement mechanics including stamp duty lodgement, rate adjustments, and RevenueSA notification. Post-settlement compliance covers landlord insurance requirements, property management fee benchmarks (6% to 9% of gross rent plus GST), depreciation schedules (Division 43 and Division 40), deductible expenses, capital gains tax on sale, and short-term rental considerations including Adelaide City Council's proposed commercial rate surcharge.

Who This Guide Is For

This guide is for property investors targeting South Australian markets who:

- Are building an Adelaide rental portfolio and need to model how the $833,000 individual threshold, the $25,000 trust threshold, and RevenueSA's two-stage aggregation formula for joint owners will affect their actual net yield — not the yield that appeared on the agent's advertisement

- Are interstate investors from Victoria or NSW viewing South Australia as a yield play and tax haven — attracted by the defence spending, 0.6% vacancy rate, and relatively affordable entry prices — but need to understand the community title insurance trap, Form 1 disclosure regime, and tenancy reform obligations before deploying capital from 800 kilometres away

- Are evaluating community-titled townhouses or units and need to verify exactly who is responsible for building insurance before they inherit an uninsured structure that the quarterly levies appeared to cover

- Are existing SA landlords navigating the no-cause eviction ban, six-month re-letting ban, automatic pet approval rules, and minimum housing standards — and need every obligation, notice period, and penalty consolidated in one reference rather than scattered across CBS fact sheets and SACAT rulings

- Are considering defence corridor properties near the Osborne Naval Shipyard or Edinburgh Precinct and need suburb-level yield data, commuting radius analysis, and DHA lease-back economics mapped against actual holding costs

- Want every SA-specific regulation, tax calculation, and due diligence requirement in one reference — instead of assembling it from RevenueSA calculators, REISA Panorama reports, CBS tenancy guides, PlanSA planning maps, and PropertyChat threads that may predate the 2024-2026 tenancy reforms or the latest land tax thresholds

Why Not Free Tools and Forums?

Free information on South Australian property investing exists. Here's what it actually delivers:

- RevenueSA calculators and documentation give you the land tax rate tables, the general and trust thresholds, and the foreign ownership surcharge rates. They don't explain how the two-stage aggregation formula catches joint owners who assumed each property was assessed separately, don't compare the dollar impact of individual versus trust versus company ownership at different portfolio values, and don't model how acquiring a third property pushes the entire portfolio above the $833,000 threshold. You get the rate schedule without the structuring strategy that makes it useable.

- REISA Panorama market reports provide excellent quarterly median price movements and macroeconomic summaries. They don't tell you which suburbs within the defence corridor offer the best yield-to-entry-price ratio, don't model insurance costs for BAL-rated properties in the Adelaide Hills, and don't cover the regulatory risks that determine whether a 4.5% gross yield actually delivers positive cash flow after land tax, insurance, and compliance costs. Market data without operational due diligence is a partial picture.

- PropertyChat and Reddit threads (r/AusPropertyChat, r/Adelaide) contain genuinely useful investor experience reports mixed with advice that predates the 2024-2026 tenancy reforms, the no-cause eviction ban, and the latest RevenueSA thresholds. Interstate investors routinely exchange anecdotal and often incorrect advice about SA's aggregation laws, Form 1 timelines, and community title insurance obligations. A 2023 thread explaining trust structuring may not reflect the designated beneficiary concession closure. Sorting current from outdated takes longer than reading a guide that has already done it.

This guide fills the South Australia-specific gap — the space between knowing how to analyse a rental property in general and knowing how to underwrite one in a state where the trust land tax threshold sits at $25,000, where community-titled properties shift building insurance entirely to the lot owner unlike every other state's strata model, where no-cause evictions are abolished with a six-month re-letting ban, and where a defective Form 1 can void a completed contract. It's the analysis that would take a South Australian conveyancer, a specialist tax adviser, and a property-focused accountant to assemble — structured as a reference you own permanently.

— Less Than One Building and Pest Inspection

A single building and pest inspection in South Australia runs $500 to $800. Stamp duty on a $600,000 investment property is $26,830. A trust structure that triggers the $25,000 land tax threshold instead of the $833,000 individual threshold can cost thousands more annually from the first dollar. An uninsured community-titled property leaves you exposed to total structural loss. Upgrading a non-compliant older property to meet minimum housing standards adds immediate capital expenditure before you can legally tenant it.

This guide doesn't replace your conveyancer or your tax adviser. But it gives you the land tax aggregation model, the community title insurance verification system, the Form 1 audit framework, and the tenancy reform compliance reference that ensure you identify every SA-specific risk before you're contractually committed — instead of discovering them on your first RevenueSA assessment, your first insurance claim denial, or your first SACAT hearing.

If it catches a single land tax structuring mistake, prevents a single uninsured community title purchase, or saves you from a voided contract due to a defective Form 1, it pays for itself before you've finished reading it.

30-day money-back guarantee. If the guide doesn't sharpen your underwriting and protect your capital in South Australia's regulatory environment, you pay nothing.

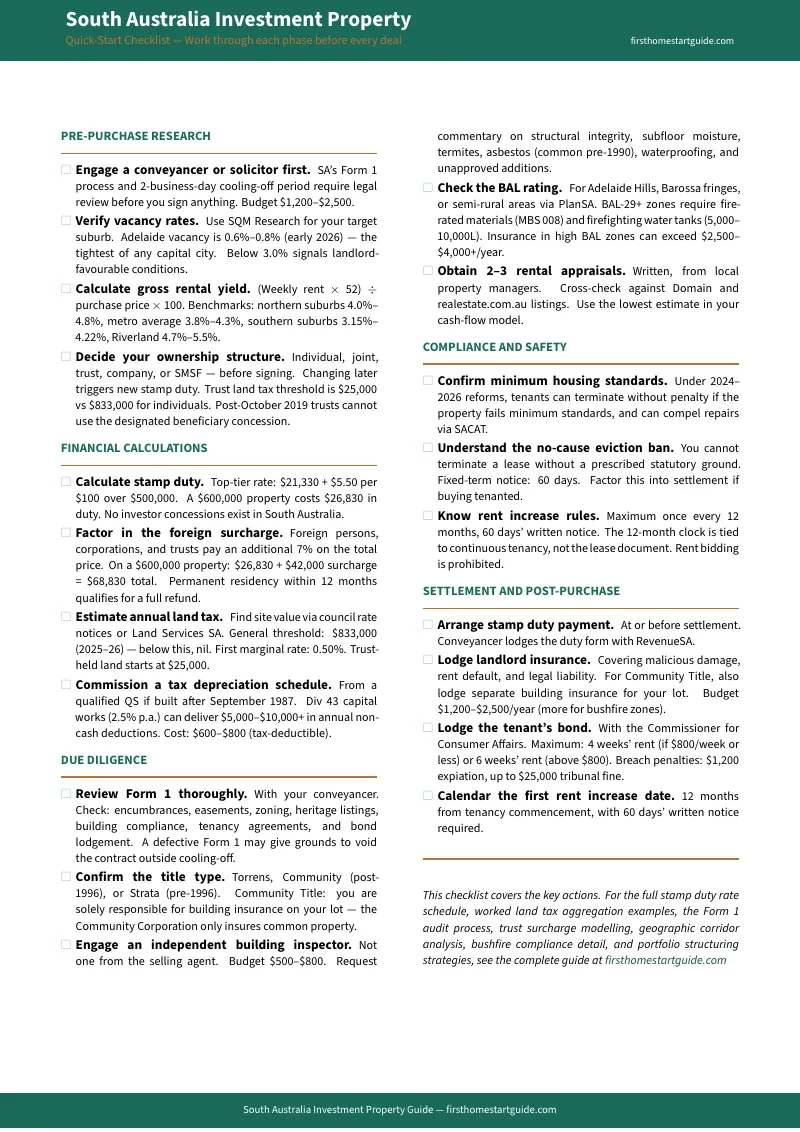

Download the free South Australia Quick-Start Investment Property Checklist to see the due diligence framework covering pre-purchase research, financial calculations, Form 1 review, compliance requirements, and post-purchase setup. When you're ready for the full land tax structuring model, community title insurance system, defence corridor analysis, and portfolio construction strategy, the complete guide is here.

The yield clears at 4.5%. This guide tells you whether South Australia agrees.