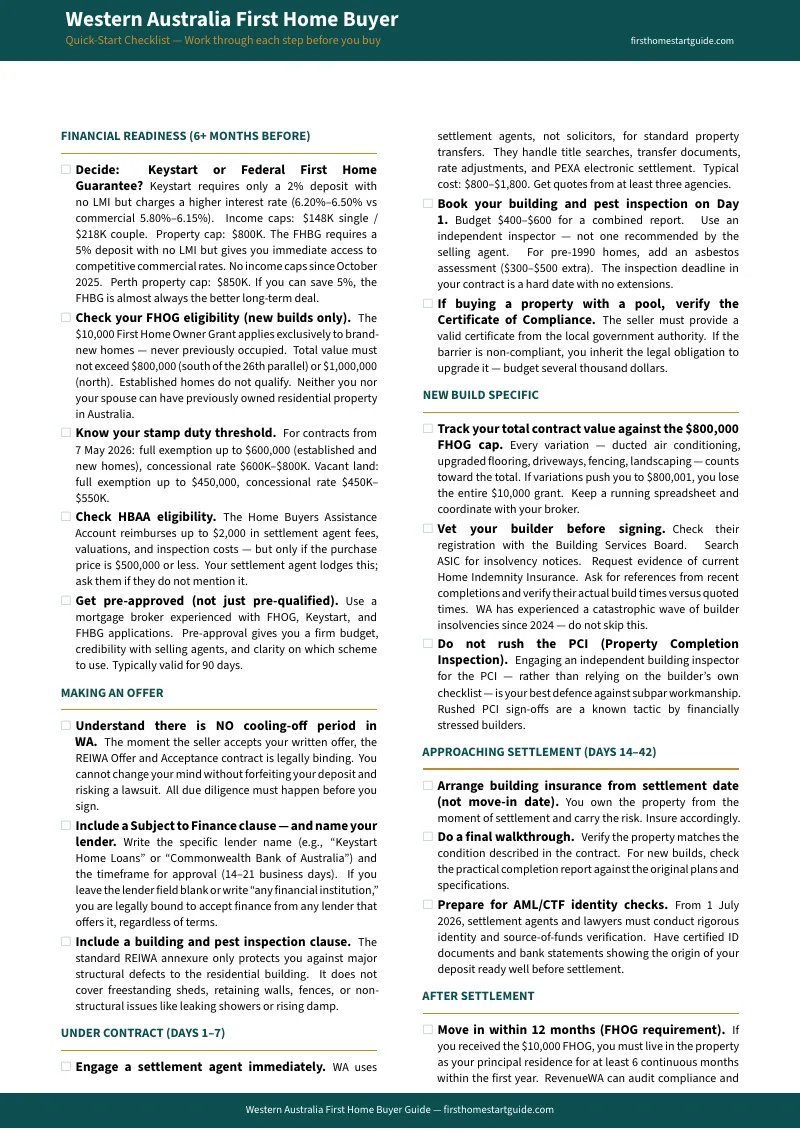

You Have Checked the FHOG Eligibility Page, the Keystart Calculator, and the Federal Guarantee Scheme. You Still Cannot Work Out Whether Keystart's 2% Deposit Actually Saves You Money or Traps You in a Higher Interest Rate for Five Years.

You have read the RevenueWA fact sheet on the First Home Owner Rate. You have looked at house-and-land packages in Baldivis and villas in Midland. You may have seen the Reddit thread about a buyer who took a Keystart loan at 6.20%–6.50% because they only had $16,000 saved, then watched a colleague use the Federal First Home Guarantee at 5.89% with no income cap and no LMI — and realised nobody had told them the federal scheme existed. Or the r/Perth post about a couple who signed a fixed-price contract with a volume builder in Ellenbrook, only for the builder to enter administration eight months later — leaving them paying rent and servicing a land mortgage simultaneously while 80 other families fought over the same insurance bond.

The problem is not a lack of information. RevenueWA covers the stamp duty thresholds. Keystart publishes its income limits. The WA Government lists the FHOG eligibility rules. But no single resource explains how the $600,000 stamp duty exemption, the $800,000 FHOG cap, the $800,000 Keystart limit, and the $850,000 Federal First Home Guarantee cap interact — where they overlap, where they conflict, and at which exact price points you lose thousands because you crossed the wrong threshold by a single dollar. Nobody compares Keystart's 2% deposit with zero LMI against the federal scheme's 5% deposit with zero LMI and lower interest rates in a side-by-side cost model. Nobody explains why WA uses settlement agents instead of solicitors, what a settlement agent legally cannot do for you, and when you need a property lawyer because your settlement agent is prohibited by law from advising you on a contract dispute.

The Western Australia First Home Buyer Guide is a WA Budget Cliff Navigator — a single, structured reference that maps every grant threshold, stamp duty cliff, lending scheme, legal limitation, and construction risk into a step-by-step process you work through before you sign the Offer and Acceptance. It replaces weeks of cross-referencing government portals, Keystart marketing, Reddit warnings, and mortgage broker pitches with a reference that tells you exactly what to check, exactly what the numbers should look like, and exactly where WA-specific deals fall apart.

What's Inside the WA Budget Cliff Navigator

A 75-page guide, a quick-start checklist, and 10 standalone worksheets and reference cards — covering every stage from calculating your true borrowing power through to collecting your keys, built specifically for the grants, lending schemes, legal frameworks, and construction risks that make buying in Western Australia different from every other Australian state:

The Keystart vs. Commercial Mortgage Decision — The Comparison Nobody Publishes

Keystart requires only a 2% deposit and waives LMI entirely — saving you upwards of $30,000 in insurance premiums on a high-LVR loan. But Keystart's variable rate sits at 6.20%–6.50%, while commercial lenders under the Federal First Home Guarantee offer rates in the high 5% to low 6% range. On an $800,000 property, that gap costs you tens of thousands in additional interest over five years. The guide provides a side-by-side financial model: Keystart (2% deposit, $800,000 cap, $148,000/$218,000 income limits) versus the Federal FHBG (5% deposit, $850,000 cap, no income caps since October 2025). It shows you exactly when Keystart is your best entry point and exactly when the federal scheme saves you more — including the 24-month refinancing escape plan that Keystart's own website encourages but never quantifies.

The $600,000 Stamp Duty Cliff and the HBAA Rebate

Following the May 2026 Budget reforms, first home buyers pay zero transfer duty on properties up to $600,000, with a sliding concession from $600,001 to $800,000. One dollar above $600,000 triggers an immediate duty liability. Below $500,000, you also qualify for the Home Buyers Assistance Account — a WA-exclusive $2,000 rebate that covers your settlement agent fees, building inspection, and valuation costs. The guide includes a stamp duty comparison table at every major price point so you can see the exact cost difference between $499,000, $550,000, $650,000, and $800,000 — not a generic claim that "concessions are available."

The $10,000 FHOG — Price Caps, Building Contract Traps, and the 26th Parallel Split

The First Home Owner Grant is $10,000 for new homes only — not established properties. South of the 26th parallel (including Perth), the total value must not exceed $800,000. North of the 26th parallel (Pilbara, Kimberley), the cap is $1,000,000. But the "total value" calculation includes land, base contract, and all post-contractual variations — site works, upgraded fixtures, fencing, landscaping. A builder quoting $760,000 who adds $45,000 in variations costs you the entire $10,000 grant. The guide walks through every eligibility rule, the 12-month move-in requirement, the 6-month residency obligation, and how to audit your building contract line by line so an upgrade does not push you past the cap.

Federal Deposit Scheme Stacking — FHBG, Family Home Guarantee, and Shared Equity

The Federal First Home Guarantee lets you buy with a 5% deposit and no LMI, with a Perth price cap of $850,000 and no income caps since October 2025. The Family Home Guarantee gives single parents access with a 2% deposit. WA's own Shared Home Ownership scheme has the Housing Authority funding up to 30% of the property value, reducing your mortgage to 70% while you still only need a 2% deposit. The guide maps how to stack these federal and state programs with the $10,000 FHOG and the stamp duty exemption — showing you the exact combination that compresses your upfront cash requirement to its minimum for your specific purchase price and location.

Settlement Agents — What They Do, What They Cannot Do, and When You Need a Lawyer

Western Australia is the only state where property transfers are handled by licensed settlement agents rather than solicitors. Settlement agents are highly efficient administrators — they prepare transfer documents, liaise with your lender, and coordinate settlement for $800 to $1,500. But they are legally prohibited from providing legal advice under the Settlement Agents Act 1981. If a boundary dispute arises, if the seller breaches the contract, if you discover unapproved structures — your settlement agent cannot advise you, and you must independently engage a property lawyer at additional cost. The guide explains exactly what a settlement agent does, exactly what they cannot do, and exactly when to escalate to a conveyancing lawyer before you are exposed to a legal risk nobody warned you about.

No Cooling-Off Period — The WA Rule Most Buyers Discover Too Late

Western Australia has no statutory cooling-off period. The moment the seller accepts your written Offer and Acceptance, the contract is legally binding. Walking away exposes you to forfeiting your deposit and being sued for damages or specific performance — a court order forcing you to complete the purchase. Buyers migrating from New South Wales or Victoria assume the 3-to-5-day cooling-off window exists nationwide. It does not exist in WA. The guide covers how to structure your O&A conditions — subject to finance, building inspection, pest inspection — so your due diligence is complete before you sign, not after.

The Builder Insolvency Crisis — Due Diligence Before You Sign a Fixed-Price Contract

Start Right Homes. Inspired Homes. Zorzi Builders. WA construction insolvencies surged 24% in 2024, with over 1,200 companies going under. Buyers who signed fixed-price contracts found themselves paying rent and servicing a land mortgage while their builder entered administration and their unfinished home sat exposed to weather damage. The guide provides a builder due diligence framework: how to check a builder's registration status, how to verify their financial position, the warning signs of a distressed builder (demanding premature PCI sign-offs, requesting upfront payments outside the statutory progress payment schedule), and what protections exist through the Home Building Contracts Act 1991.

The Pilbara Mining Town Warning — Why 10% Rental Yields Can Destroy Your Equity

Karratha's median house price peaked at over $820,000 during the 2012-2014 iron ore boom. By 2017, it had collapsed to $340,000 — a capital destruction of more than 60%. Entire cohorts of buyers were trapped in extreme negative equity, unable to sell, unable to rent profitably, facing bank repossessions. Current yields in Pilbara towns are again hitting 9-11%, and marketing materials promote the "Mining Boom 2.0." The guide analyses the structural dynamics that drive these cycles — construction-phase labour demand versus automated-operations workforce reduction — and explains why high rental yields in resource towns are the market pricing in the risk of catastrophic capital loss, not a signal of safe investment.

Physical Due Diligence — Asbestos, Bushfire, Termites, and Pool Barriers

Perth's pre-1990 housing stock is saturated with asbestos-containing materials — fibro cladding, eaves, Super Six roofing, wet-area cement sheeting. Properties in the Perth Hills face Bushfire Attack Level ratings that inflate construction costs and insurance premiums. Termites target the timber roof trusses and framing even in Perth's masonry-dominant "double brick" housing. Swimming pool barrier non-compliance transfers to the buyer at settlement. The guide covers what to look for in building and pest inspection reports, how to assess asbestos risk before buying an older home with renovation plans, how to check BAL ratings for fringe properties, and what pool compliance certificates you need to verify before signing.

The Complete WA Acquisition Cost Breakdown

Side-by-side worked examples at $400,000, $550,000, and $800,000 showing FHOG eligibility, stamp duty liability, Keystart versus FHBG deposit requirements, settlement agent fees, Landgate registration costs, building and pest inspection costs, and the HBAA rebate. These are not generalised estimates — they are WA-specific calculations using the May 2026 rate tables, current Keystart limits, and updated FHOR thresholds.

Settlement, AML/CTF Changes, and Post-Purchase Obligations

The full settlement timeline from Offer and Acceptance to key handover: 28 to 42 days in WA, processed electronically via PEXA and registered at Landgate. From 1 July 2026, new Anti-Money Laundering laws require settlement agents and lawyers to conduct rigorous identity and source-of-funds checks on all buyers — increasing the documentation burden and baseline cost of settlements. The guide covers the REIWA standard contract conditions, the subject-to-finance trap (leaving the nominated lender field blank means you must accept finance from any institution), post-settlement FHOG residency compliance, insurance activation, and first-year budget planning for the real cost of owning a home in Western Australia.

Who This Guide Is For

- Perth renters earning $80,000 to $180,000 who have the income to service a mortgage but cannot work out whether Keystart's 2% deposit or the federal guarantee's 5% deposit actually saves them more money over the first five years of ownership

- Buyers targeting properties near the $600,000 stamp duty threshold who need to understand exactly how much one dollar above the exemption costs them — and whether restructuring their offer or negotiating chattels separately keeps them below the cliff

- First home buyers choosing between a house-and-land package in Baldivis, Alkimos, or Ellenbrook and an established home in an inner suburb who need the actual dollar comparison — FHOG eligibility, stamp duty, deposit requirement, construction risk — at their specific price point

- FIFO and mining sector workers considering buying in Karratha, Port Hedland, or Kalgoorlie who need the historical Pilbara crash data before committing to a purchase at current elevated prices

- Interstate migrants from NSW, Victoria, or Queensland who assume cooling-off periods, conveyancing solicitors, and eastern-state disclosure requirements exist in WA — and need to understand the legal framework before they sign an Offer and Acceptance they cannot undo

- Anyone buying a new build in the current WA construction market who needs a framework for vetting their builder's financial health before signing a fixed-price contract in a state where over 1,200 construction companies collapsed in a single year

Why Not Free Resources?

Free information on buying your first home in Western Australia exists across a dozen government websites. Here is what it actually delivers:

- RevenueWA publishes transfer duty rates and the First Home Owner Rate thresholds. It does not compare the financial impact of buying at $595,000 versus $605,000 — the boundary where you cross the exemption cliff and trigger an immediate duty liability. You get the rate table without the worked examples that explain what the threshold actually costs you.

- Keystart's website explains its 2% deposit, zero LMI, and income limits. It does not compare its 6.20%–6.50% variable rate against the Federal First Home Guarantee's access to commercial rates in the high 5% range. It does not model the excess interest you pay over five years while waiting to build enough equity to refinance. You get the marketing pitch without the objective cost comparison.

- The WA Government's FHOG page lists eligibility rules and price caps. It does not explain how building contract variations push your total value past the $800,000 cap, how the 26th parallel split creates different caps for Perth and the Pilbara, or how the "total value" calculation aggregates land, base contract, and every post-contractual change order. You get the rules without the mechanism that causes real buyers to fail them.

- Reddit, Whirlpool, and Perth Facebook groups contain real buyer experiences — but advice about stamp duty thresholds posted before the May 2026 Budget reforms references the old $500,000 exemption, not the current $600,000 threshold. Keystart rate discussions from early 2025 cite different figures. Sorting current from outdated takes longer than reading a guide that has already done it.

This guide fills the Western Australia-specific gap — the space between knowing you want to buy a first home and knowing how to navigate a state where Keystart and the federal guarantee compete for the same buyers, stamp duty thresholds shifted fundamentally in May 2026, settlement agents cannot give you legal advice, there is no cooling-off period, and builders are collapsing at a rate that makes every fixed-price contract a calculated risk.

— Less Than a Single Building and Pest Inspection

A building and pest inspection in Perth costs $300 to $600. Settlement agent fees run $800 to $1,500. Crossing the $600,000 stamp duty exemption threshold by $5,000 costs you thousands in transfer duty. Taking Keystart at 6.20%–6.50% instead of a commercial rate at 5.89% on an $800,000 loan costs tens of thousands over five years. Losing the $10,000 FHOG because your builder added $45,000 in variations costs exactly $10,000. Buying in a Pilbara mining town at the peak of a cycle cost real buyers over $480,000 in capital destruction between 2014 and 2017.

This guide does not replace your settlement agent. But it gives you the Keystart-versus-FHBG comparison, the stamp duty cliff tables, the builder due diligence framework, the settlement agent limitation guide, and the complete WA acquisition cost breakdowns that ensure you identify every Western Australia-specific risk before you sign an Offer and Acceptance — not when the RevenueWA assessment arrives, the Keystart rate review hits, or the builder's administrator sends you a letter.

If it saves you from a single stamp duty cliff you would not have calculated, a single Keystart trap you would not have modelled, or a single builder you would not have vetted, it pays for itself before you finish reading it.

30-day money-back guarantee. If the guide does not sharpen your due diligence and protect your deposit in Western Australia's property market, you pay nothing.

Download the free Western Australia Quick-Start Home Buying Checklist to see the step-by-step framework covering pre-approval, house hunting, inspections, and settlement. When you are ready for the full Keystart-versus-FHBG comparison, stamp duty cliff tables, builder due diligence framework, and complete acquisition cost breakdowns, the complete guide is here.

The grants are generous. The thresholds are unforgiving. This guide makes sure you claim the first without falling off the second.