You Saved $12,000 by Not Paying Land Transfer Tax. Then You Lost $30,000 on a Condo Special Assessment Nobody Told You How to Spot.

You found a two-bedroom condo in Calgary's Beltline listed at $420,000. Or a townhouse in Edmonton's Rutherford neighborhood where the mortgage payment is less than your current rent. Or a starter home in Airdrie where the commute is 20 minutes and the price is $200,000 less than anything in Vancouver. Your mortgage broker ran the stress test and you qualify. Your agent says the market is moving. You're ready to write an offer.

Then the details start surfacing. The Calgary condo board just passed a $25,000 special assessment because the reserve fund sat at 18% for five years while the parkade membrane deteriorated. Nobody mentioned the Poly-B piping in the 1992 building — the kind that fails without warning and costs $8,000 to $15,000 per unit to replace. The Edmonton townhouse seemed simple until your lawyer explained that the seller can't produce a current Real Property Report, the existing one shows an encroachment, and now you're choosing between a $3,500 survey or title insurance that won't cover the encroachment if the city ever enforces the bylaw. The Airdrie home closes at noon on completion day under the Western Conveyancing Protocol, and your lender's wire transfer didn't arrive by 12:00 — so now you owe the seller penalty interest at prime plus 3% for every day of delay.

Here's the thing about Alberta that everyone gets half right: Alberta has no land transfer tax, and that saves you $3,295 to $12,460 compared to the same purchase in Ontario or BC. But Alberta also has a collateral mortgage registration trap that inflates your closing fees if your lender uses a readvanceable mortgage (January 2025 change). Alberta requires a lawyer — not a notary — to close every transaction, at $1,200 to $1,500. Alberta's condo market carries Poly-B piping and aluminum wiring risks in buildings from the 1980s and 1990s that don't show up in a standard inspection. Alberta's resource towns — Fort McMurray, Grande Prairie — have a boom-bust cycle that can put you in negative equity within 18 months of purchase. And Alberta is the only province where the FHSA, HBP, and HBTC federal programs represent nearly the entire first-time buyer support system, because the province offers no land transfer tax rebate, no first-time buyer grant, and no down payment assistance outside of Attainable Homes Calgary and a handful of municipal programs with waiting lists. Getting the savings right means getting all of it right — the advantage and the risk — in a single framework.

The Alberta First-Time Home Buyer Guide is an Alberta Buyer Advantage System — not a motivational overview of Canadian homeownership, but a structured decision framework that maps Alberta's fee advantage, federal program stacking strategy, condo risk signals, resource town economics, and closing process into a system you work through before you sign anything. It replaces months of cross-referencing the Alberta Land Titles office fee schedule, the CRA FHSA rules, the CMHC stress test calculator, the Condominium Property Act, and conflicting advice on r/PersonalFinanceCanada with a single reference that tells you exactly what you save, exactly what you owe, and exactly where first-time buyers lose money in Alberta.

What's Inside the Alberta Buyer Advantage System

A 10-chapter guide, a printable step-by-step checklist, and 6 standalone worksheets — covering every stage from building your down payment through your first 30 days as a homeowner, built specifically for the provincial rules and market dynamics that make Alberta different from every other province:

Alberta's Fee Advantage — The Math That Proves What You Actually Save

Everyone says Alberta has no land transfer tax. The guide shows you what that means in dollars: $1,180 total government fees on a $600,000 home versus $4,475 in Ontario (after the first-time rebate) and $10,000 in BC. At $800,000, you save $6,935 versus Ontario and $12,460 versus BC. But the guide also covers the Bill 20 fee restructure (October 2024) and the January 2025 collateral mortgage change — if your lender registers a readvanceable mortgage at 125% of property value, you pay registration fees on the full registered amount, not the property price. You'll know exactly what your closing fees will be before you sign a mortgage commitment.

The $200,000 FHSA + HBP Couple Stacking Strategy

The First Home Savings Account lets you contribute $8,000/year with a $40,000 lifetime cap — tax-deductible going in and tax-free coming out, with no repayment ever. The Home Buyers' Plan lets you withdraw $60,000 from your RRSP tax-free, repaid over 15 years. A couple using both programs can assemble up to $200,000 in tax-advantaged down payment capital. But the priority sequence matters: employer RRSP match first (free money), then FHSA (no repayment), then HBP (repayment required). At a ~38% marginal rate, an $8,000 FHSA contribution generates ~$3,000 in tax refunds you can reinvest. The guide maps the optimal contribution order, the 90-day RRSP seasoning requirement, and the exact timeline so you capture every dollar of available tax relief.

Federal and Provincial Programs — Every Dollar You're Entitled To

Alberta doesn't have a provincial first-time buyer grant. That means the federal programs carry the entire weight — and most buyers leave money on the table because they don't know all of them. The guide covers the FHSA in full detail, the enhanced $60,000 HBP, the $10,000 Home Buyers' Tax Credit, CMHC eco-incentive programs, plus the three municipal programs most guides skip entirely: Attainable Homes Calgary (purchase a home with as little as $2,000 down), Edmonton First Place (deferred land cost), and PEAK Housing (second mortgage to cover the down payment gap). Each program includes eligibility criteria, application steps, and the specific deadlines that disqualify you if you miss them.

The Alberta Purchase Process — What's Different Here

Alberta's buying process has rules that don't exist in Ontario or BC. Your agent must be RECA-licensed. Your closing must be handled by a lawyer — not a notary. The Western Conveyancing Protocol requires full payment by noon on completion day, and late funds trigger penalty interest at prime plus 3%. The seller is expected to provide a current Real Property Report, but if they don't, you're choosing between ordering a new survey ($3,500+) or accepting title insurance (~$250) that covers different risks. The guide walks through every step from pre-approval through possession day, including subject clauses, the RPR decision, and how to coordinate with your lawyer and lender to avoid the noon deadline trap.

Buying a Condo — The Red Flags That Cost $25,000+

Alberta condos are governed by the Condominium Property Act, and the risks are specific. A reserve fund study below 50-60% funding signals that a special assessment is coming — and assessments of $15,000 to $30,000 per unit are common in buildings that deferred maintenance for a decade. Insurance deductibles above $25,000 mean a single water leak in your unit could cost you the full deductible out of pocket. Buildings from the late 1980s and early 1990s carry Poly-B piping (prone to sudden failure) and aluminum wiring (insurance complications). Ground-floor units in older buildings face sewage backup risk that standard home insurance doesn't cover. The guide provides a condo document review framework — what to look for in the reserve fund study, the insurance certificate, the meeting minutes, and the estoppel certificate — with a proceed/negotiate/walk-away decision at the end. A professional condo document review costs $250 to $499; knowing how to read the results yourself is worth far more.

New Construction — The GST Rebate Nobody Calculates Correctly

New homes in Alberta are subject to 5% federal GST with no provincial component. The federal rebate returns up to $6,300 on homes priced under $350,000 and is available on homes up to $1 million under the expanded Bill C-4 provisions, phasing out between $1 million and $1.5 million. Combined with Alberta's 1-2-5-10 warranty coverage (1 year materials/labour, 2 years delivery systems, 5 years building envelope, 10 years structural), new construction offers protections that resale doesn't. The guide covers the rebate calculation at multiple price points, the warranty claims process, and the builder red flags that tell you whether the warranty is worth the paper it's printed on.

Calgary vs. Edmonton — The Market Analysis That Changes Your Strategy

Calgary and Edmonton are two different markets with different math. Calgary: median detached home around $640,000, condos starting in the low $400,000s, driven by energy sector headquarters and interprovincial migration. Edmonton: average detached home around $511,000, townhomes from the high $200,000s, anchored by government, education, and a more stable employment base. The practical implication: a $400,000 budget buys you a condo in Calgary or a detached home in Edmonton. The guide maps each city's price ranges by property type, the neighborhoods where first-time buyers are actually purchasing, and the supply dynamics that determine whether you'll face bidding wars or have negotiating room.

Resource Town Risk — What Every Other Guide Ignores

Fort McMurray and Grande Prairie offer some of the lowest price-per-square-foot housing in Canada. They also carry boom-bust risk that can erase 30-40% of your home's value when oil prices drop. The guide covers the economics of resource towns — why prices are elastic to extraction project decisions, how the 1980s NEP crash and 2014 oil collapse played out in real housing data, and the specific risk factors (employer concentration, population volatility, resale market liquidity) you need to evaluate before buying. This chapter exists because no institutional guide — not CMHC, not any bank, not any realtor website — addresses resource town risk for first-time buyers.

Who This Guide Is For

This guide is for first-time home buyers in Alberta who:

- Are buying their first home in Calgary or Edmonton and need to understand how to stack the FHSA, HBP, and HBTC to maximize their down payment — and how the collateral mortgage registration change affects their closing costs

- Are looking at condos and need a framework for reading reserve fund studies, spotting special assessment risk, evaluating insurance deductibles, and identifying Poly-B piping and aluminum wiring buildings before they make an offer

- Are relocating from British Columbia or Ontario and assume Alberta is straightforward because there's no land transfer tax — without realizing that the lawyer-only closing requirement, the noon payment deadline, the RPR obligation, and the resource town risk create a different set of traps

- Are a couple coordinating FHSA and HBP contributions and need the optimal sequencing, contribution limits, and tax refund reinvestment math mapped out in one place

- Are weighing new construction against resale and need to compare the GST rebate, the 1-2-5-10 warranty, and the total cost at multiple price points to determine which actually saves more

Why Not Free Tools and Government Websites?

Free information on Alberta home buying exists across dozens of sources. Here's what it actually delivers:

- The Alberta Land Titles Office website publishes the fee schedule. It does not explain the January 2025 collateral mortgage change, does not compare Alberta's total closing costs against other provinces, and does not show you how the Bill 20 restructure affects your specific purchase price. You get a formula without the context that tells you whether your lender's mortgage type is costing you extra.

- CMHC and bank websites explain the FHSA and HBP as separate programs. They don't explain how to sequence contributions between the two, how the employer RRSP match fits into the priority order, how the 90-day RRSP seasoning rule affects your closing timeline, or how a couple can reach $200,000 in combined tax-advantaged capital. You get program descriptions without the strategy that maximizes them.

- Reddit threads on r/PersonalFinanceCanada and r/Calgary are where buyers share real experiences with condo special assessments, resource town losses, and closing day surprises — mixed with advice that predates the 2024 HBP increase to $60,000, the January 2025 collateral mortgage change, and the current Calgary-Edmonton price gap. Sorting current from outdated requires cross-referencing every claim against legislation and market data.

- Realtor-produced buyer guides cover the general purchase process and emphasize how affordable Alberta is compared to BC and Ontario. They rarely explain condo reserve fund red flags, resource town risk factors, the noon deadline penalty, or the RPR vs. title insurance tradeoff — because their business model depends on you buying, not on you deciding that a particular building or town isn't worth the risk.

This guide fills the Alberta-specific gap — the space between knowing Alberta is affordable and knowing how to buy here without walking into a condo liability, a resource town gamble, a closing cost surprise, or a program you should have enrolled in six months earlier. It's the analysis that would take a real estate lawyer, a mortgage broker, a condo specialist, and a tax accountant to assemble — structured as a reference you own permanently.

— Less Than One Hour of Your Real Estate Lawyer's Time

A single condo special assessment in an underfunded building runs $15,000 to $30,000. A missed FHSA contribution year is $8,000 in tax-deductible room you can never reclaim. A collateral mortgage registration on a $500,000 home at 125% registered value adds $75 in unnecessary fees — and that's the small one. A resource town purchase at the top of a boom cycle can cost you 30% of your home's value. An unused HBTC is $1,500 in federal tax credits you never claimed.

This guide doesn't replace your lawyer or your mortgage broker. But it gives you the fee advantage math, the program stacking strategy, the condo risk framework, and the market analysis that ensure you capture every program, avoid every red flag, and understand every closing cost before you sign — instead of discovering them at the lawyer's office, on your first condo board meeting, or when you try to sell in a down market.

If it catches a single condo red flag, captures a single tax credit you would have missed, or prevents a single uninformed purchase in a volatile market, it pays for itself before you finish reading it.

30-day money-back guarantee. If the guide doesn't sharpen your buying strategy and protect your closing costs in Alberta's market, you pay nothing.

Your download includes 8 PDFs: the full 10-chapter guide, the quick-start checklist, plus 6 standalone worksheets you can print and use independently — the Registration Fee Calculator, Program Stacking Worksheet (FHSA + HBP + HBTC), Condo Document Audit Checklist, Closing Cost Worksheet, New Build vs. Resale Comparison, and Resource Town Risk Assessment.

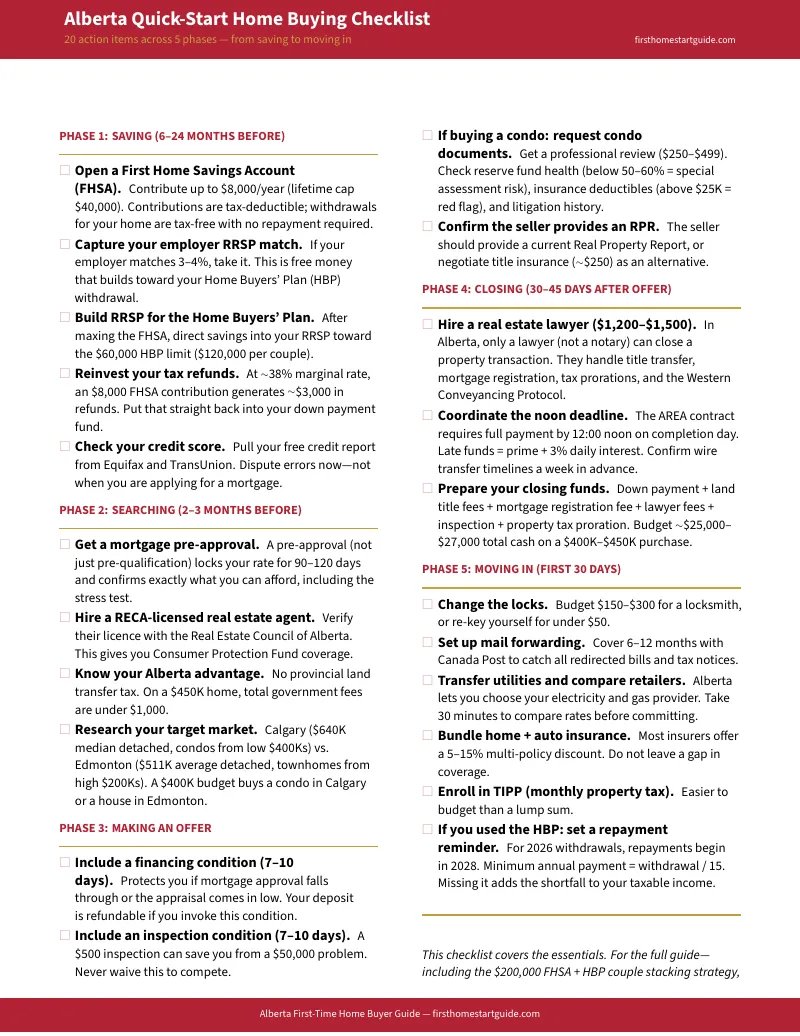

Download the free Alberta Quick-Start Home Buying Checklist to see the step-by-step action plan covering saving, searching, making an offer, closing, and moving in. When you're ready for the full program stacking strategy, condo risk framework, and market analysis, the complete guide is here.

Alberta gives you the lowest closing costs in Canada. This guide makes sure you keep that advantage — and don't lose it somewhere else.