You Found a Character Home in River Heights for $360,000. Nobody Mentioned the $30,000 Sewer Line, the Knob-and-Tube Insurance Deadline, or the Land Transfer Tax Bill Due in Cash on Closing Day.

You have browsed MLS listings in St. Vital and East Kildonan. You have run the CMHC mortgage calculator and received a pre-approval that limits you to $250,000 to $350,000 — a range that pushes you straight into Winnipeg's older housing stock. You have scrolled through r/Winnipeg threads where first-time buyers describe losing their third consecutive offer to unconditional bids that close $80,000 over asking. And you have probably assumed that because Manitoba is "affordable" compared to Toronto or Vancouver, the transaction itself must be simple.

It is not. Manitoba layers a progressive land transfer tax with no first-time buyer rebate, a mandatory separate-lawyer closing requirement, a 7% Retail Sales Tax on CMHC insurance premiums payable in cash at closing, reactive glacial clay soils that crack foundations across Winnipeg, pre-1970 clay sewer lines that collapse under mature tree roots, knob-and-tube wiring that triggers 30-day insurance ultimatums, lead water service pipes in one out of nine older homes, and radon levels that exceed Health Canada guidelines in nearly a quarter of Manitoba houses. The free CMHC workbook does not mention any of this. Your agent's blog post covers none of it. The r/Winnipeg threads mention pieces of it, but they are scattered across hundreds of posts with no way to tell which advice is current and which is dangerously outdated.

The core problem: Manitoba's "affordable" housing market hides the most punishing combination of closing-day cash requirements and older-home structural liabilities in Western Canada — and every free resource covers one piece without connecting it to the rest. There is no single resource that maps how reactive clay soil affects your foundation and your sewer line simultaneously, how the absence of a provincial LTT rebate changes your cash-to-close calculation, how to stack the FHSA and HBP to cover the gap, or how to spot the five hidden five-figure traps in a pre-1970 Winnipeg home before your offer becomes unconditional. Until now.

The Manitoba First-Time Home Buyer Guide is a Manitoba Property Intelligence System — a structured decision framework that connects every Manitoba-specific financial trap, structural risk, and federal program strategy into a single step-by-step roadmap from pre-approval through possession day.

What's Inside the Manitoba Property Intelligence System

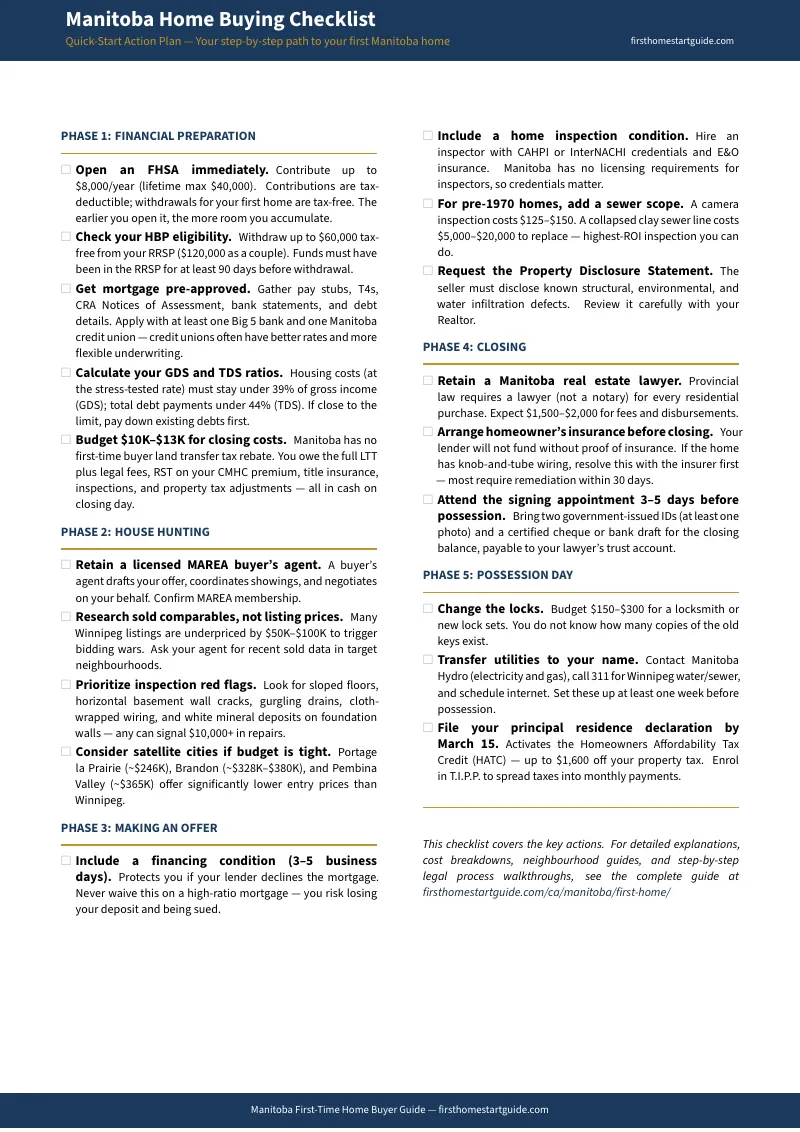

The complete 61-page guide plus three standalone printable tools — covering every stage from calculating your true Manitoba borrowing power through collecting the keys, plus a fillable closing cost worksheet, a pre-1970 home inspection checklist, and a closing timeline reference card you can bring to lawyer meetings, mortgage broker appointments, open houses, and home inspections:

Manitoba Closing Cost Breakdown

The cash requirements nobody warns you about. Manitoba charges a progressive land transfer tax that hits $5,650 on a $400,000 home — and unlike Ontario or British Columbia, offers zero rebate for first-time buyers. On top of that, Manitoba collects 7% RST on your CMHC insurance premium in cash at closing. Add mandatory legal fees ($1,500 to $2,500 with disbursements), title insurance ($300 to $750), property tax adjustments, and the home inspection — and a buyer targeting a $400,000 Winnipeg detached home needs roughly $31,000 in total cash at closing. The guide breaks down every line item with a fillable worksheet so you know the exact number before you make an offer.

FHSA and HBP Stacking Strategy

How to build a down payment that actually covers Manitoba's cash requirements. Manitoba's missing LTT rebate means you need more cash at closing than buyers in most other provinces. The guide walks through the First Home Savings Account ($8,000 annual limit, $40,000 lifetime, fully tax-deductible contributions, completely tax-free withdrawals with no repayment requirement) and the Home Buyers' Plan ($60,000 RRSP withdrawal with 15-year repayment over a 5-year grace period). It shows exactly how a buying couple can combine both programs to maximize down payment power — and how to sequence contributions to avoid the repayment trap that adds missed HBP amounts directly to your taxable income.

Pre-1970 Older Home Hazard System

The five hidden five-figure traps in Winnipeg's character homes. Winnipeg sits on a deep bed of glaciolacustrine clay left by ancient Lake Agassiz. This soil swells when saturated with spring meltwater and shrinks during summer — cracking foundations, heaving floors, and misaligning door frames across the city. The same soil movement destroys the jointed clay sewer pipes in pre-1970 homes, creating entry points for tree roots that cause basement backups. The guide covers reactive clay foundations ($5,000 to $30,000+ repair), clay and cast iron sewer lines ($5,000 to $20,000 replacement), knob-and-tube wiring ($8,000 to $15,000 removal with a 30-day insurance deadline), lead water service pipes ($3,000 to $7,000 replacement), and asbestos materials — with a visual identification checklist you can use during open houses to spot each hazard before your offer goes in.

Radon Risk Assessment

Manitoba is the second most radon-prone province in Canada. Approximately 24% of Manitoba homes exceed Health Canada's guideline of 200 Becquerels per cubic metre. Radon enters through foundation cracks and sumps, concentrating in basements where buyers build bedrooms and recreation rooms. The guide covers testing protocols (minimum three-month winter placement), mitigation costs (active sub-slab depressurization starting at $1,500), and how to negotiate radon testing as a condition of your offer.

Mortgage Stress Test and Debt Ratio Strategy

Why your $60,000 household income only qualifies you for $240,000. The stress test requires qualification at your contract rate plus 2.0% or 5.25%, whichever is higher. The guide walks through the Gross Debt Service Ratio and Total Debt Service Ratio formulas with Manitoba-specific examples, showing exactly how existing debts reduce your borrowing power and how to restructure before applying to maximize your pre-approval amount.

Bidding War Defence and Underpricing Strategy

Why the $299,000 listing will sell for $380,000 — and how to stop losing to unconditional offers. Winnipeg agents routinely list properties $50,000 to $100,000 below market value to trigger emotional bidding wars. The guide teaches you how to read recent comparable sales to calculate true market value before attending a showing, how to set a strict walk-away limit based on your own numbers, how to identify overpriced properties that have sat on the market where sellers are ready to negotiate, and how to make your conditional offer competitive without waiving protections that could cost you tens of thousands.

Manitoba Closing Process and Legal Requirements

What happens in the 30 to 45 days between an accepted offer and possession. Manitoba requires separate legal representation for buyer and seller — your lawyer handles title searches, mortgage registration, land transfer tax collection, and trust account management. The guide maps the complete timeline from accepted offer through key collection, explains the choice between title insurance ($300 to $750) and a physical surveyor's certificate ($1,200), and lists every disbursement your lawyer will charge so the final invoice holds no surprises.

Who This Guide Is For

This guide is for first-time buyers in Manitoba who:

- Are buying in Winnipeg and targeting older homes in neighbourhoods like St. Vital, East Kildonan, or River Heights — where attractive prices hide reactive clay foundation risks, pre-1970 sewer liabilities, knob-and-tube wiring, lead pipes, and asbestos that can add $15,000 to $50,000 in remediation costs within the first year of possession

- Are recent immigrants who arrived through economic immigration streams and are navigating the Canadian home buying process for the first time — often purchasing at higher price-to-income ratios and needing a clear map of how the FHSA, HBP, stress test, and CMHC insurance interact for buyers without established Canadian credit histories

- Are renting in Winnipeg at $1,300+ per month and want to transition to ownership but need to understand exactly how much cash they need beyond the down payment — because Manitoba's missing LTT rebate and RST on CMHC premiums add over $6,700 in unexpected closing costs on a $400,000 home

- Are considering secondary markets like Steinbach, Brandon, Winkler, or Portage la Prairie to avoid Winnipeg's bidding wars — and need region-specific pricing data, financing strategies, and risk assessments for properties outside the capital

- Are buying as a couple and want to maximise their combined FHSA and HBP withdrawals to build the largest possible down payment — while understanding the repayment obligations, tax implications, and timing requirements that determine whether these programs save you thousands or create a tax bill you did not expect

Why Not Free Resources?

Free information on buying your first home in Manitoba is everywhere. Here is what each source actually delivers:

- CMHC "Homebuying Step by Step" workbook provides detailed financial planning tools — debt ratio calculators, credit score explanations, mortgage insurance tables. What it does not do: mention that Manitoba offers no provincial land transfer tax rebate, explain Winnipeg's reactive clay soil and its effect on foundations and sewer lines, address the 7% RST on CMHC premiums that must be paid in cash at closing, or provide any guidance on pre-1970 home hazards. The national framework is solid. The Manitoba-specific traps are completely absent.

- Local real estate agent blogs offer neighbourhood guides and step-by-step buying overviews with genuine Winnipeg knowledge — from the perspective of professionals who earn a commission when you buy. They mention foundation cracks and knob-and-tube wiring as items for your inspector to check. They do not explain the underlying geology, the typical remediation cost, the 30-day insurance ultimatum, or why a $15,000 electrical rewiring is not optional. They will tell you to "be ready to move fast." They will not explain that the $299,000 list price is a marketing tactic designed to generate a bidding war at $380,000.

- Reddit (r/Winnipeg, r/PersonalFinanceCanada) is where real Manitoba buyers share unfiltered experiences — and where advice about the FHSA from 2023 sits alongside current figures, where one poster's $250,000 success story ignores the $20,000 sewer replacement six months later, and where "Manitoba is affordable, just buy" is accepted wisdom by people who have never calculated the full cash-to-close requirement. The signal is real. So is the noise.

- Winnipeg real estate law firms (Tacium Vincent, Lange Law) publish excellent breakdowns of legal fees, disbursements, and the closing process in precise legal language. They do not provide guidance on property search strategy, neighbourhood selection, structural risk identification, or how to stack federal programs to cover your down payment. They will tell you what closing costs exist. They will not tell you how to prepare for them nine months in advance.

- Mortgage broker blogs and YouTube channels explain pre-approval, stress testing, and down payment minimums with local market context. They do not cover the physical condition of the housing stock you will actually be buying with that mortgage — the clay sewers, the knob-and-tube wiring, the lead pipes, the radon exposure. They will qualify you to buy. They will not prepare you for what you are buying.

This guide fills the navigation gap — the space between knowing Manitoba has a land transfer tax, older home risks, and federal savings programs, and understanding how they all interact across a single home purchase. It is the analysis an independent advisor with no properties to sell would give you, structured as a permanent reference you own.

— Less Than the RST on Your CMHC Premium

Manitoba charges over $1,000 in Retail Sales Tax on the CMHC premium alone for a typical first-time buyer purchase. A professional home inspection costs $500. A single sewer camera inspection runs $350 to $600. Replacing a compromised clay sewer line after possession costs $10,000 to $20,000. A knob-and-tube removal runs $8,000 to $15,000 — and your insurer will give you 30 days to complete it or lose your coverage.

This guide does not replace your real estate lawyer, your mortgage broker, or your home inspector. But it gives you the closing cost breakdown, the older home hazard identification system, the FHSA and HBP stacking strategy, and the bidding war defence framework that ensure you walk into every appointment knowing exactly what to ask, exactly what to budget, and exactly what to never skip — instead of discovering expensive traps in real time.

If it prevents a single sewer surprise, catches a knob-and-tube deadline you would have missed, or helps you stack the FHSA and HBP to cover your full down payment and closing costs, it pays for itself before you have finished reading it.

30-day money-back guarantee. If the guide does not make your Manitoba home buying process clearer and your financial position stronger, you pay nothing.

Download the free Manitoba Quick-Start Home Buying Checklist to see the step-by-step action plan covering closing cost estimates, older home hazard identification, FHSA and HBP eligibility, and the mandatory legal closing process. When you are ready for the full intelligence system — the 61-page guide plus the fillable closing cost worksheet, the pre-1970 home inspection checklist, and the closing timeline reference card — the complete toolkit is here.

You have been saving for this. Now make sure the house you buy does not cost you twice.