The Home Was $275,000. The Closing Cost Surprise Was $4,200 More Than You Budgeted. The Oil Tank Was Uninsurable. The Septic Field Failed Three Months Later.

You found a three-bedroom bungalow in Moncton listed at $275,000. Or a century-old character home in Saint John's uptown for $310,000. Or a sprawling rural property near Sussex on five acres for $240,000 with a detached garage, mature trees, and a price that would barely cover a parking spot in Toronto. Your mortgage broker says you qualify. Your real estate agent says it's a great deal. You're ready to sign.

Then the layers start peeling back. Your lawyer calls about the Real Property Transfer Tax. You budgeted for 1% of $275,000 — $2,750. But Service New Brunswick assessed the property at $310,000 based on recent neighbourhood sales, and the tax is calculated on the greater of the purchase price or the assessed value. Your tax bill is $3,100. Then the lawyer mentions the Land Titles conversion. The home has been in the same family since the 1960s and has never been registered in the modern Land Titles system — your purchase triggers the first registration, which adds $450 to $500 in legal fees and weeks of administrative delay on top of the standard $800 to $1,500 in closing legal costs. Then your insurance broker calls. The oil tank in the basement was manufactured in 2005. It's now 21 years old. No insurer in the province will write a policy on a tank that age, and without home insurance your lender will not fund the mortgage. Replacing the tank costs $1,000. If it has already leaked and nobody noticed — which nearly 40% of all domestic oil spills in New Brunswick involve — soil remediation runs $8,000 to $100,000. That five-acre rural property? The septic system was last inspected never. Three months after closing, the drainage field collapses. A full replacement with imported sand costs $35,000. Your insurance doesn't cover it. Your agent never mentioned it.

Here's the problem: New Brunswick layers a Real Property Transfer Tax calculated on the greater of the purchase price or the provincially assessed value with zero first-time buyer exemptions, a dual land registration system actively transitioning from a two-century-old Registry of Deeds to a government-guaranteed Land Titles system where your purchase may trigger a mandatory first registration with hundreds of dollars in additional legal fees and processing delays, widespread oil heating systems with tanks that become uninsurable after 15 to 20 years and carry cleanup liabilities up to $100,000 under the Environmental Protection Act, thousands of rural properties operating on private septic systems where a failed drainage field replacement can reach $40,000, elevated radon gas concentrations requiring 91-day testing and $3,000 to $5,000 mitigation systems, annual spring freshet flooding along the Saint John River basin that caused $75 million in damages during the 2018 event alone, and a severe absence of provincial grants or tax rebates for first-time buyers — into a market where every property that looks affordable carries infrastructure liabilities that no listing photograph and no mortgage calculator will show you. Every one of these has cost real first-time buyers thousands or tens of thousands of dollars because the information existed across different government websites, different provincial statutes, different Reddit threads, and different insurance broker phone calls, and nobody had assembled it into a single decision framework.

The New Brunswick First-Time Home Buyer Guide is a Total Cost of Ownership System — not a motivational overview of Atlantic Canadian homeownership, but a structured process that maps every NB-specific tax calculation, every infrastructure risk signal, every legal fee, and every environmental hazard into a framework you work through before you sign anything. It replaces months of cross-referencing Service New Brunswick assessment databases, Land Titles Act procedures, CMHC default insurance tables, Department of Environment regulations, and contradictory advice on r/newbrunswickcanada with a single reference that tells you exactly what you owe, exactly what can go wrong, and exactly how to protect yourself in a market where the purchase price is only the beginning of the cost.

What's Inside the Total Cost of Ownership System

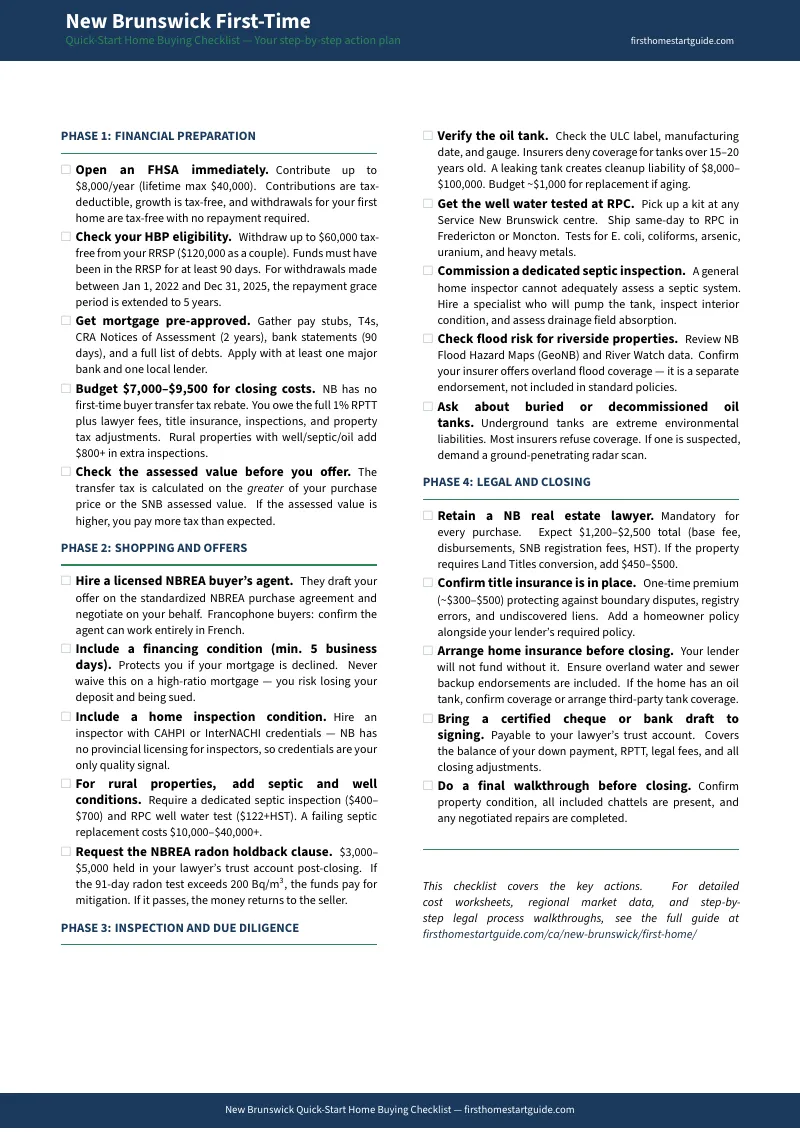

A 12-chapter guide, a quick-start checklist, and 3 standalone printable tools — covering every stage from financial preparation through your first year of ownership, built specifically for the infrastructure complexities and legal peculiarities that make New Brunswick different from every other province:

The Real Property Transfer Tax — Why Your Budget Is Wrong Before You Start

The RPTT is calculated at 1% of the greater of the purchase price or the Service New Brunswick assessed value. If you negotiate a below-market price on a fixer-upper but the assessed value reflects recent neighbourhood sales, you pay tax on the higher number. The guide walks through the exact calculation with worked examples at every common price point, explains why there is no first-time buyer exemption or rebate in New Brunswick, shows you how to look up any property's assessed value before you make an offer so you can budget accurately, and identifies the narrow statutory exemptions that do exist (spouse transfers, estate transfers) so you stop searching for relief that isn't there.

The Land Titles Conversion — The Hidden Fee on Older Properties

New Brunswick is partway through converting from an antiquated Registry of Deeds to a modern, government-guaranteed Land Titles system. If the property you buy has never been sold or mortgaged since the Land Titles Act was introduced, your purchase triggers a mandatory first registration. Your lawyer must conduct a final exhaustive historical title search, submit an Application for First Registration with an Owner's Affidavit to Service New Brunswick, and pay $85 per document plus $35 for the Certificate of Registered Ownership. The conversion adds $450 to $500 in legal fees and can delay your closing by weeks. The guide explains which properties require conversion, what the process involves, what it costs, and how to factor this into your offer timeline — so it's a budget line, not a surprise.

Oil Tank Inspection — The Environmental Liability That Can Bankrupt You

Nearly 40% of all oil spills reported annually in New Brunswick originate from domestic tanks. Standard homeowner insurance strictly excludes pollution liability from fuel oil leaks. Under the Environmental Protection Act, the homeowner bears sole legal responsibility for cleanup — $8,000 to $100,000 depending on severity. The guide covers how to verify tank age and ULC certification, when tanks become uninsurable (15 to 20 years), how to negotiate tank replacement before closing, when to demand ground-penetrating radar for suspected buried tanks, and which third-party coverage programs (ProGuard, MyTankPlan) provide up to $100,000 in cleanup liability protection. This chapter alone can save you from a six-figure environmental remediation bill.

Septic and Well Water Due Diligence — The Rural Property Survival Guide

A huge share of affordable New Brunswick homes operate on private septic systems and private wells with zero municipal oversight after installation. A general home inspection does not assess septic systems — you need a specialist. The guide covers the full septic inspection process ($400 to $700), what the inspector should check, what a failing system looks like, the cost spectrum from a $290 pump-out to a $40,000 imported-sand drainage field replacement, where to get RPC well water testing ($122 plus HST), the same-day shipping requirement that invalidates results if you miss it, and why waiving a septic inspection to win a bidding war is the single most expensive mistake a rural buyer can make.

Flood Risk and Radon — The Invisible Threats

The Saint John River basin floods catastrophically during spring freshet. The 2018 event hit 8.36 metres in the Fredericton area, affected 12,000 properties, and caused $75 million in damages. Standard home insurance does not cover overland flooding — it requires a separate endorsement that may be unavailable in high-risk zones. The guide shows you how to check the New Brunswick Flood Hazard Maps and River Watch data before making an offer, what your insurance policy must include, and when to walk away from a riverside property. For radon, New Brunswick has elevated concentrations across much of its bedrock. The guide covers the NBREA radon holdback clause (a $3,000 to $5,000 escrow mechanism built into your purchase agreement), the 91-day testing requirement, and the $3,000 to $5,000 sub-slab depressurization system that reduces levels by over 80%.

Government Programs — What Actually Exists and What Doesn't

The guide dismantles the most dangerous assumption New Brunswick buyers make: that there is provincial "free money" waiting for them. The provincial Home Ownership Program provides repayable loans — but only to households earning under $40,000, which excludes the vast majority of buyers. There is no land transfer tax rebate. No first-time buyer tax credit. Instead, the guide teaches you how to maximize the federal programs that actually apply: the FHSA ($40,000 lifetime, tax-deductible in, tax-free out), the HBP ($60,000 RRSP withdrawal, $120,000 as a couple), the HBTC ($1,500 tax credit), and the advanced RRSP-to-HBP-to-FHSA stacking strategy that lets you claim two tax deductions on the same dollar. It also covers the Fredericton HAF First-Time Homebuyers Grant (up to $20,000 for new construction on specific lots) and explains what Moncton and Saint John's HAF programs do and don't offer individual buyers.

Mortgage Qualification, Bilingual Banking, and the Caisse Populaire System

Every buyer must pass the OSFI stress test at contract rate plus 2.0% or the 5.25% floor. New Brunswick median incomes are below the national average, which means the stress test bites harder here. The guide covers GDS and TDS calculations with worked examples, CMHC default insurance premiums at every down payment tier, and the choice between Big Six banks, mortgage brokers, and the caisse populaire system. For Francophone and Acadian buyers, the guide details UNI Financial Cooperation — $5.2 billion in assets, 51 locations, cooperative structure, fully bilingual mortgage service — and explains how UNI's localized underwriting understands seasonal employment patterns in fishing, forestry, and tourism that national banks may not.

Complete Closing Cost Worksheet and 30-to-45 Day Timeline

A line-by-line closing cost breakdown with pre-filled examples for both urban properties (no well or septic) and rural properties (well, septic, and oil heat), showing the full cash requirement beyond your down payment. The closing timeline maps every milestone from condition waiver through key delivery, with specific attention to Land Titles conversion delays and the coordination between your lawyer, your lender, and Service New Brunswick.

Who This Guide Is For

This guide is for first-time home buyers in New Brunswick who:

- Are a local renter in Moncton, Fredericton, or Saint John who watched the market reprice since 2020, works on a 5% to 10% down payment, and needs to squeeze every federal program to close the gap — while understanding exactly what closing costs, transfer taxes, and inspection fees will take from that narrow capital reserve

- Are moving to New Brunswick from Ontario, BC, or Alberta and see a $350,000 detached home on acreage as a bargain — but have zero experience with private wells, septic fields, oil heating systems, unregulated home inspectors, or a land registration system that requires your purchase to trigger a title conversion

- Are a Francophone or Acadian buyer who wants to conduct the entire transaction in French, work with a caisse populaire rather than a Big Six bank, and need guidance that acknowledges the specific financial institutions and community-based financing options available in Dieppe, Caraquet, Edmundston, and northern New Brunswick

- Are a newcomer to Canada through the Atlantic Immigration Program or a Provincial Nominee Program, building a credit profile from scratch, and need to understand Canadian mortgage mechanics, the stress test, closing cost budgeting, and bilingual legal services before entering a market with unfamiliar infrastructure

- Are buying a rural or semi-rural property and need to understand the full infrastructure stack — oil tank age verification, septic system assessment, well water testing protocols, radon holdback clauses, and flood zone mapping — before you commit to a property where the purchase price is only the first line item

Why Not Free Tools and Government Websites?

Free information on buying a home in New Brunswick exists across dozens of sources. Here's what it actually delivers:

- CMHC and CRA resources explain the FHSA, HBP, and stress test mechanics at a national level. They do not explain that New Brunswick offers no provincial transfer tax rebate, that the RPTT is calculated on assessed value rather than purchase price, that the provincial Home Ownership Program has a $40,000 income cap that excludes most buyers, or that Land Titles conversion adds hundreds of dollars in unexpected legal fees. You get federal program descriptions without the provincial context that determines what you actually owe.

- Service New Brunswick publishes technical documentation on property assessments, the Land Titles Act, and the Registry of Deeds. These documents are written in bureaucratic legalese for legal professionals and surveyors — not as a chronological roadmap for a 28-year-old buyer trying to close on their first home under transaction-day pressure.

- Reddit threads on r/newbrunswickcanada, r/Moncton, and r/fredericton are where buyers share real experiences with transfer tax surprises, oil tank nightmares, and septic failures — mixed with anecdotal advice, outdated information, and warnings from people who got burned. The advice is contradictory, legally dubious, and impossible to verify under time pressure. Sorting signal from noise while your condition deadline is ticking is a recipe for disaster.

- Realtor blogs and brokerage guides cover the basic purchase process and market conditions. They rarely dedicate thousands of words to explaining the catastrophic liabilities of soil remediation from a leaking oil tank, the cost range of a failed drainage field, or the $450 to $500 Land Titles conversion fee on an older property — because realtors earn commissions when you buy, not when you discover a five-figure infrastructure liability and walk away.

This guide fills the New Brunswick-specific gap — the space between knowing you want to buy a home in the province and knowing how to buy one without a transfer tax surprise, an uninsurable oil tank, a failed septic system, or a legal fee you didn't budget for. It's the analysis that would take a real estate lawyer, an environmental consultant, a mortgage broker, and a septic engineer to assemble — structured as a reference you own permanently.

— Less Than One Septic Pump-Out

A single transfer tax miscalculation based on purchase price instead of assessed value costs hundreds of dollars. An uninsured oil tank that leaks costs $8,000 to $100,000 in mandatory remediation. A failed septic drainage field costs $15,000 to $40,000 to replace. A Land Titles conversion fee you didn't know about adds $500 on closing day. A missed FHSA contribution is $8,000 per year in tax deductions you never claimed.

This guide doesn't replace your lawyer or your mortgage broker. But it gives you the transfer tax calculation framework, the oil tank verification checklist, the septic inspection protocol, the federal program stacking strategy, and the complete closing cost worksheet that ensure you budget accurately, inspect thoroughly, claim every dollar of available tax relief, and spot every infrastructure risk before you sign — instead of discovering them on closing day, in your first heating season, or during spring thaw.

If it catches a single transfer tax miscalculation, prevents a single uninsured oil tank purchase, or captures a single tax-sheltered contribution you would have missed, it pays for itself before you finish reading it.

30-day money-back guarantee. If the guide doesn't sharpen your buying strategy and protect your closing costs in New Brunswick's unique market, you pay nothing.

Your download includes the full 12-chapter guide, the quick-start checklist, and 3 standalone printable tools — a Closing Cost Worksheet (fillable, with pre-filled examples for urban and rural properties), a Due Diligence Checklist (print and bring to every property viewing), and a Transfer Tax Reference Card (the RPTT assessed value calculation on one page). Plus the complete guide covering total cost of ownership budgeting, government program optimization, mortgage qualification, regional market profiles, oil tank and septic due diligence, the Land Titles conversion process, flood and radon risk assessment, and the full legal closing process.

Download the free New Brunswick Quick-Start Home Buying Checklist to see the step-by-step action plan covering financial preparation, offer strategy, inspection due diligence, and legal closing. When you're ready for the full Total Cost of Ownership System — the 12-chapter guide plus the Closing Cost Worksheet, Due Diligence Checklist, and Transfer Tax Reference Card — the complete toolkit is here.

The mortgage calculator says you can afford the home. This guide tells you what the home will actually cost.