You Found a Cash-Flowing Duplex in Moncton for $250,000. Nobody Told You That the Transfer Tax Is Calculated on the Assessed Value (Not Your Purchase Price), That the Property Is Still in a Registry System That Will Cost You $1,500 to Convert Before Closing, or That 40% of NB Oil Spills Come From Residential Tanks Like the One Buried in the Backyard.

You have been watching New Brunswick from Ontario or BC. You have seen the numbers: duplexes at a quarter of Toronto prices, vacancy rates under 4%, no provincial speculation tax, no foreign buyer penalty, and rents that actually cover the mortgage. You have run the cap rate calculations on a tenanted triplex in Saint John listed at $195,000 and concluded that Atlantic Canada is the last market in the country where leveraged real estate still cash-flows from Day 1. You are about to make an offer.

Then your lawyer mentions that the property is still held under New Brunswick's legacy Registry of Deeds system — not the modern Land Titles system you assumed was standard everywhere — and that mandatory conversion before closing will cost you $500 to $1,500 in legal disbursements on top of your regular closing fees. You discover that the Real Property Transfer Tax is calculated on the higher of your purchase price or the provincial assessed value, which means the distressed duplex you negotiated down to $200,000 triggers a $3,000 tax bill based on its $300,000 assessment. You learn that non-owner-occupied properties are excluded from the 2026 assessment freeze, so you pay taxes on current market value while your neighbour pays on a frozen 2022 assessment for the identical building next door. And you find out that the charming oil-heated fourplex has an undocumented underground storage tank — the kind responsible for nearly 40% of all oil spills reported annually to the NB Department of Environment — and that a buried tank you did not find before closing costs $15,000 or more in soil remediation, with zero insurance coverage.

The core problem: New Brunswick is genuinely the best yield-per-dollar real estate market in Canada — and it hides the most localized combination of archaic title systems, assessment-based tax traps, discriminatory property tax policies, and environmental liabilities in the country. Every free resource covers one regulation without connecting it to your actual investment return. CMHC reports give you vacancy rates but not strategy. Service New Brunswick publishes oil tank compliance rules but not acquisition due diligence. Generic Canadian investing blogs treat all of Atlantic Canada as one market. There is no single resource that calculates how the RPTT assessment trap changes your closing costs, how the Registry-to-Titles conversion affects your timeline, how the "double tax" on non-owner-occupied properties erodes your cash flow, or how to identify buried oil tanks before your offer goes firm. Until now.

The New Brunswick Investment Property Guide is the NB Investor's Operating Manual — a province-specific acquisition and compliance system that connects every transfer tax calculation, title conversion requirement, property tax asymmetry, tenant regulation, and environmental liability into a single end-to-end framework built for out-of-province and local investors entering the Moncton, Saint John, and Fredericton markets.

What's Inside the NB Investor's Operating Manual

The complete guide plus standalone printable tools — covering every stage from market selection and financing strategy through tenant management and tax planning, plus a closing cost worksheet and an investment property checklist you can bring to lawyer meetings, property viewings, and lender appointments:

Three-City Market Analysis: Moncton, Saint John, and Fredericton

Because New Brunswick is not one market — it is three markets with completely different risk profiles. Moncton offers balanced growth with a 3.8% vacancy rate and average two-bedroom rents of $1,452, driven by logistics hubs, bilingual workforce demand, and the Atlantic Immigration Program. Fredericton anchors around provincial government and university employment with a 2.5% vacancy rate and the lowest turnover in the province. Saint John delivers the highest gross yields and the lowest acquisition costs — multi-unit buildings under $200,000 — but carries severe deferred maintenance risk on its aging housing stock and a vacancy rate that actually tightened to 2.1% in 2025. The guide maps sub-market vacancy rates, average rents, demand drivers, and risk profiles for each city so you choose your market based on data, not listing price excitement.

The RPTT Assessment Trap

The tax penalty for buying below market value. New Brunswick's Real Property Transfer Tax is 1% — but it is calculated on the greater of your purchase price or the provincially assessed value. When you negotiate a below-market acquisition on a distressed property (exactly the kind of deal value-add investors seek), the province taxes you on the higher assessed value that does not reflect the property's actual condition. The guide explains the calculation methodology, shows how to check assessments on Service New Brunswick's database before making an offer, walks through the formal Request for Review appeal process, and models the real RPTT cost at multiple price points so your closing cost projections are accurate from the first offer.

The Dual Land Registration System

The $1,500 closing cost that does not appear on any standard checklist. Many New Brunswick properties still reside under the legacy Registry of Deeds system — a framework where a deed is merely a historical snapshot of ownership, not a government-backed guarantee of title. If you purchase one of these properties, mandatory conversion to the Land Titles system is triggered at closing, entirely at your expense. Your lawyer must trace the chain of title back decades, potentially uncovering historical logging rights, forgotten utility easements, or restrictive covenants that limit your ability to renovate or add density. The guide explains both systems, details the conversion process, budgets the additional legal disbursements, and tells you how to identify whether a property is Registry or Land Titles before you make an offer.

The "Double Tax" and Assessment Freeze Exclusion

Why your property taxes are structurally higher than your neighbour's — even on an identical building. Non-owner-occupied properties in New Brunswick pay both municipal and provincial property tax rates. Despite a 50% reduction in the provincial rate between 2022 and 2024, rental properties still carry a materially higher tax burden than primary residences. Worse, the 2026 assessment freeze that protects existing homeowners from post-pandemic valuation spikes explicitly excludes new buyers and out-of-province investors. You pay taxes on current market value while the legacy owner next door pays on a frozen assessment from years ago. The guide quantifies the exact tax differential, models the cash flow impact at various assessment levels, and explains the assessment spike protection mechanisms that are phasing in for existing owners but do not apply to your first acquisition.

Oil Tank Environmental Due Diligence

The $15,000 liability hiding underground. Nearly 40% of all oil spills reported annually to the NB Department of Environment originate from domestic residential oil tanks. Older properties — especially in Saint John and historic Moncton neighbourhoods — frequently have undocumented underground storage tanks abandoned in place when heating systems were upgraded decades ago. A buried tank you did not discover before closing becomes your environmental liability: $2,000 to $5,000 for removal, $15,000 or more for soil remediation if contamination is found, and immediate uninsurability if the tank fails provincial compliance standards. The guide mandates a Ground Penetrating Radar sweep before waiving conditions, details the compliance requirements for active above-ground tanks (double-wall construction, 12-gauge steel, concrete slab foundation, CSA-approved leak detection), and provides a step-by-step protocol for negotiating tank removal with the seller.

The Fastest Eviction System in Canada

30 to 35 days from first missed payment to Sheriff enforcement — for under $100 in total fees. If you have been a landlord in Ontario, you know the Landlord and Tenant Board backlog: 51-day average hearing delays, $2,000 in paralegal fees, and a Sheriff who takes another month to enforce. New Brunswick's Residential Tenancies Tribunal resolves non-payment evictions in an average of 5 days. The complete process — from serving the first notice to the Sheriff physically executing the order — takes approximately 30 to 35 days and costs less than $100 in administrative fees. The guide maps the exact step-by-step timeline, provides a side-by-side comparison with Ontario's system, and covers rent increase rules (3% annual cap, 6-month notice), security deposit obligations (you do not hold the deposit — it goes to a provincial fund), inherited tenancy protections, and the strict 7-day deadline for damage claims that most new landlords miss entirely.

The Two-Track Financing System

Why a New Brunswick credit union may approve you when a Big Six bank will not. Federally regulated banks apply the OSFI stress test and count only 50% to 80% of projected rental income. New Brunswick's provincially regulated credit unions — Omista, UNI Financial Cooperation, Brunswick Credit Union — operate under different rules. They may count up to 100% of net rental income, offer relationship-based underwriting, and are not bound by the federal stress test formula. With OSFI 2026 rules prohibiting cross-collateralization of personal income for investment properties, the credit union track becomes the critical financing pathway for scaling a portfolio. The guide explains both tracks, compares pre-approval strategies, and details the HELOC-funded down payment structure that uses Ontario or BC equity to acquire cash-flowing NB assets.

Tax Planning: CCA, Anti-Flipping, and the Capital Gains Inclusion Rate

The recapture trap that turns a tax deferral into a six-figure bill. The guide covers Form T776 rental income reporting, deductible expenses, the Capital Cost Allowance at 4% declining balance (and the strategic case for not claiming it), the anti-flipping rule that converts any sale within 12 months to fully taxable business income, the two-tier capital gains inclusion rate ($250,000 at 50%, above at 66.67%), and New Brunswick's provincial income tax brackets that stack on top of federal rates for combined marginal rates exceeding 50%.

Who This Guide Is For

This guide is for real estate investors targeting New Brunswick who:

- Are buying from Ontario or British Columbia and need to understand the RPTT assessment trap, the mandatory Registry-to-Titles conversion, and the "double tax" on non-owner-occupied properties before running cash flow projections — because the spreadsheet that works in your home province does not account for New Brunswick's localized closing costs and tax asymmetries

- Are OSFI 2026 refugees — investors who can no longer cross-collateralize personal income to qualify for investment mortgages — and need to find markets where rental income alone supports debt service, plus the credit union financing track that counts up to 100% of net rents

- Are targeting Saint John's high-yield, low-cost multi-unit buildings and need the deferred maintenance risk framework, the oil tank environmental due diligence protocol, and the capital expenditure budget that separates genuinely profitable distressed assets from money pits

- Are local New Brunswick investors scaling from one rental to a small portfolio and need the complete landlord compliance system — the 3% rent cap rules, the 6-month notice requirement, the security deposit fund process, and the 7-day damage claim deadline that automatically refunds the tenant if you miss it

- Are first-time landlords anywhere in Canada who want the confidence of knowing that New Brunswick's eviction system resolves non-payment disputes in 30 to 35 days for under $100 — not the 4-to-6-month nightmare you have heard about from Ontario

Why Not Free Resources?

Free information on New Brunswick real estate investing is available from multiple sources. Here is what each one actually delivers:

- CMHC Rental Market Reports provide vacancy rates, rent growth, and construction starts for Moncton, Saint John, and Fredericton. Essential data. What they do not do: explain how the RPTT assessment trap inflates your closing costs, how the Registry-to-Titles conversion adds weeks and hundreds of dollars to your timeline, how the "double tax" differential erodes your cash flow projections, or how to evaluate a property's oil tank compliance. The data is real. It is not a deal analysis.

- Service New Brunswick publishes the Residential Tenancies Act, the RPTT regulations, oil tank compliance guidelines, and property assessment lookup tools across multiple department websites. The information is authoritative and complete in isolation. The rent cap page does not link to the eviction timeline. The RPTT regulations do not mention the assessment trap for below-market purchases. The oil tank compliance standards are in a separate department's bulletins entirely. The information exists. The connections do not.

- Reddit (r/PersonalFinanceCanada, r/newbrunswickcanada, r/Moncton) is where current investors share unfiltered experiences — and where a 2022 post about the old provincial tax rate sits alongside 2025 forum anger about out-of-province speculators "bleeding us dry." Locals on r/newbrunswickcanada actively blame external investors for rent inflation and housing unaffordability. The signal is real. So is the hostility and the outdated information.

- Generic Canadian real estate investing blogs treat all of Atlantic Canada as one market. They mention "low prices in the Maritimes" without differentiating Moncton's balanced growth from Saint John's high-risk deferred maintenance environment. They do not address the dual land registration system, the RPTT assessed value calculation, or the credit union financing track. They want clicks. They do not tell you what acquiring and operating a New Brunswick rental property actually involves.

This guide fills the integration gap — the space between knowing New Brunswick has low prices and high yields, and understanding the complete matrix of transfer tax calculations, title conversion costs, property tax asymmetries, tenant regulations, environmental liabilities, and financing structures that determine whether those yields actually survive contact with reality. It is the analysis an independent advisor with no properties to sell would give you, structured as a permanent reference you own.

— Less Than One Hour of Your NB Real Estate Lawyer's Time

A real estate lawyer in New Brunswick charges $800 to $1,500 for a standard investment property closing. A building inspection costs $400 to $600. A GPR oil tank sweep costs $150 to $350. Soil remediation from a single undiscovered buried tank starts at $15,000. An RPTT miscalculation based on assessed value rather than purchase price costs you hundreds at closing. A missed 7-day security deposit claim deadline costs you one full month of rent.

This guide does not replace your real estate lawyer, your property inspector, or your accountant. But it gives you the complete transfer tax architecture, the title conversion process, the property tax differential analysis, the oil tank due diligence protocol, and the tenant management framework that ensure you walk into every professional meeting knowing exactly what to ask, exactly what to budget, and exactly what liabilities to avoid — instead of discovering them in real time with capital already committed.

If it prevents a single RPTT miscalculation, catches an oil tank liability before closing, or helps you structure your first rent increase correctly under the 3% cap, it pays for itself before you have finished reading it.

30-day money-back guarantee. If the guide does not make your New Brunswick investment analysis clearer and your acquisition due diligence stronger, you pay nothing.

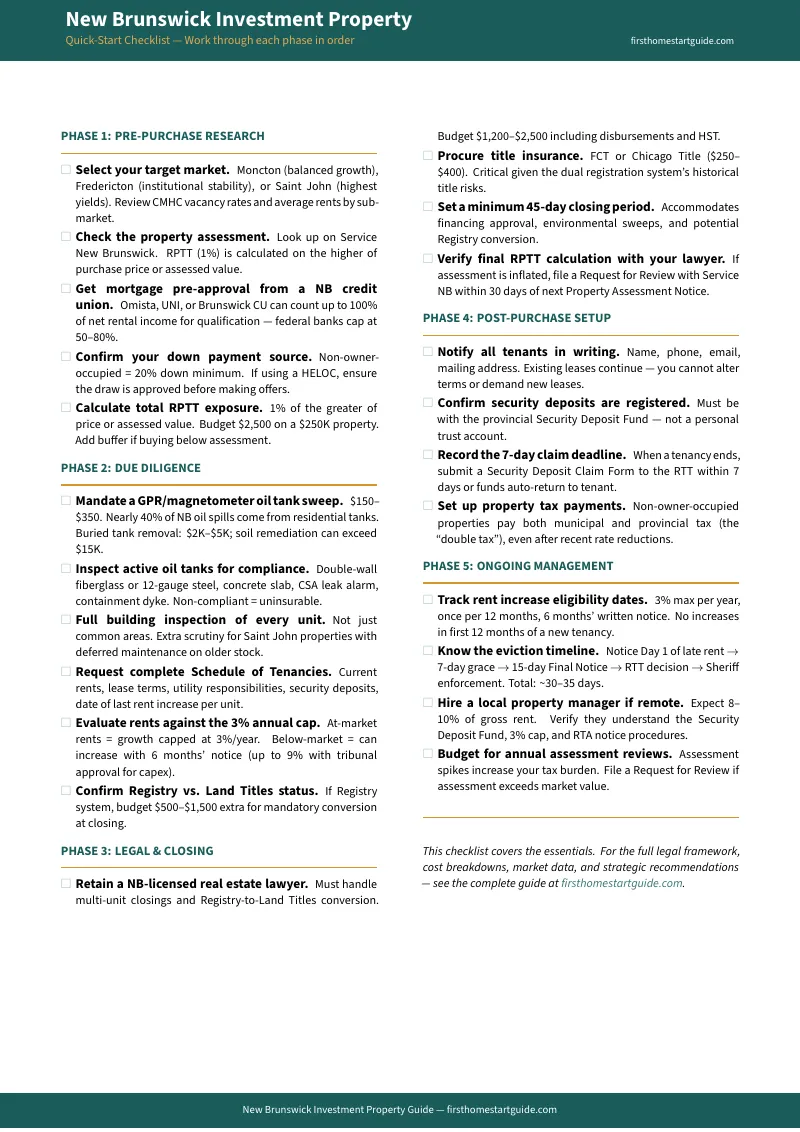

Download the free New Brunswick Quick-Start Home Buying Checklist to see the step-by-step action plan covering RPTT calculations, Registry vs. Land Titles identification, oil tank inspection requirements, and the eviction timeline. When you are ready for the full operating manual — the complete guide plus the closing cost worksheet and investment property checklist — the complete toolkit is here.

New Brunswick's yields are real. So are the assessment traps, the title conversion costs, the tax asymmetries, and the buried oil tanks. Make sure you know all four before you wire the deposit.