Everyone Told You Newfoundland Has No Land Transfer Tax. Nobody Told You About the $3,300 Dual Registration Bill, the $5,000 Legal Fee, or the Oil Tank That Kills Your Mortgage on Closing Day.

You found a three-bedroom home in Mount Pearl listed at $310,000. Or a starter in Conception Bay South where the mortgage is less than the $1,400 you're paying in rent. Or a row house in downtown St. John's with a view of the harbour and a price that would barely buy a parking spot in Toronto. Your mortgage broker ran the stress test and you qualify. Your agent says move fast — well-priced homes are pulling 8 to 14 competing offers within 48 hours.

Then reality arrives. Your lawyer explains that Newfoundland doesn't use the Torrens title system that protects buyers in every other major province. Instead, they have to manually reconstruct the chain of ownership going back 40 years through the Registry of Deeds — tracing handwritten family transfers, unrecorded subdivisions, and Crown grants from the 1800s — and that's why legal fees here run $1,500 to $5,000 instead of the $1,200 you expected. The "no land transfer tax" turns out to mean a dual registration fee — one for the deed, one for the mortgage — calculated by a formula that extracts $2,700 to $3,300 on a standard purchase. The home inspector flags a 12-year-old outdoor oil tank, and your insurance broker tells you no company will bind a policy until it's replaced — which means your lender won't fund the mortgage, which means the entire transaction collapses four days before closing. And the basement has efflorescence creeping up the cinder block walls, which your contractor says is the beginning of a $5,000 to $15,000 waterproofing problem that every older St. John's home eventually develops.

Here's what nobody explains about buying in Newfoundland and Labrador: the sticker price is the lowest in Canada. The hidden costs are among the highest. NL's Registry of Deeds system forces your lawyer to become a historical investigator, reconstructing decades of title history that the government doesn't guarantee. The province charges registration fees on both your deed and your mortgage — a dual levy that adds $2,700 to $3,300 to closing costs that buyers budget as zero. Oil tanks that heat 40% of older homes carry catastrophic insurance and environmental liabilities — a single leak can trigger $100,000+ in soil remediation. The home inspection industry is entirely unregulated. Preserved wood foundations and post-and-pier supports in rural areas can make a home unmortgageable. And the NLHC First-time Homebuyers Program — the one provincial lifeline — uses an aggressive income sliding scale that penalizes you $500 for every $1,000 you earn above $85,000. Getting the affordability advantage right means getting all of it right — the savings and the structural risks — in a single framework.

The Newfoundland and Labrador First-Time Home Buyer Guide is the NL Closing Cost Matrix — not a motivational overview of Canadian homeownership, but a structured decision framework that maps Newfoundland's Registry of Deeds mechanics, dual registration fee calculations, oil tank and basement hazard protocols, government program stacking strategies, and the 30-to-45-day closing timeline into a system you work through before you sign anything. It replaces months of cross-referencing the CADO registry, NLHC program rules, TakeCharge NL eligibility criteria, CRA FHSA rules, and contradictory advice on r/newfoundland and r/StJohns with a single reference that tells you exactly what the province takes, exactly what you're entitled to, and exactly where first-time buyers lose thousands in Newfoundland.

What's Inside the NL Closing Cost Matrix

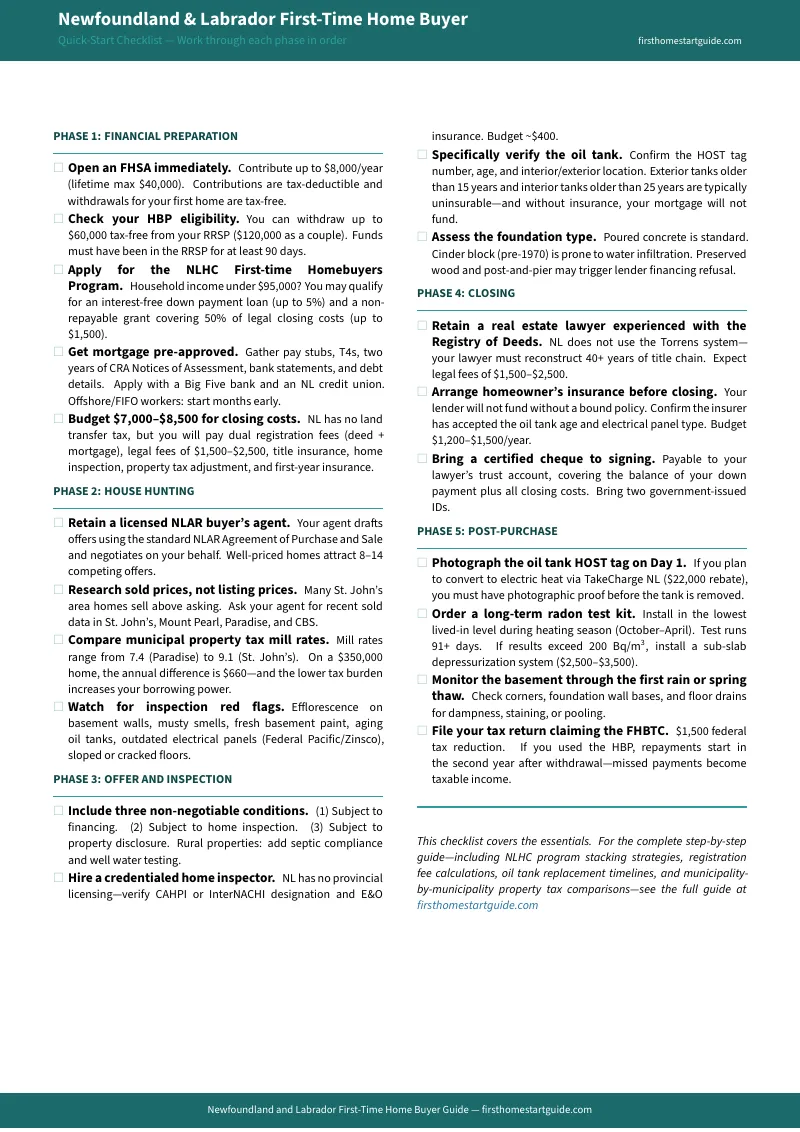

A 10-chapter guide, a printable step-by-step checklist, and 6 standalone worksheets — covering every stage from building your down payment through your first 90 days as a homeowner, built specifically for the provincial rules and market dynamics that make Newfoundland different from every other province:

The Dual Registration Fee Formula — The Math That Proves "No Land Transfer Tax" Is a Myth

Every realtor and national news outlet repeats the same line: Newfoundland has no land transfer tax. The guide shows you the reality. The Registration of Deeds Act charges $100 base plus $0.40 per $100 of value, applied separately to both the property deed and the mortgage instrument, each capped at $5,000. On a $320,000 home with 5% down: $1,378 for the deed, $1,363 for the mortgage — $2,741 total that you budgeted as zero. On a $400,000 home: $3,377. The guide provides worked examples at every common NL price point so you know the exact dollar amount before your lawyer calculates it.

The Registry of Deeds — Why Your Lawyer Costs Double and Your Title Needs Insurance

Most Canadian provinces guarantee your ownership through a Torrens system. Newfoundland does not. The Registry of Deeds is a repository of unverified claims — the registrar records documents but does not confirm their legal validity. Your lawyer must trace an unbroken chain of conveyances going back 40 years through the CADO system, paper records dating to 1825, intestate deaths, unrecorded family transfers, and adverse possession claims requiring sworn affidavits from elderly neighbours. The guide explains what this means for your legal fees ($1,500 to $2,500 for standard titles, $3,000 to $5,000 for complex ones), why title insurance at $250 to $400 is non-negotiable, and how missing Crown grants and adverse possession issues can delay your closing by weeks.

The FHSA + HBP + NLHC Stacking Strategy

Newfoundland offers no provincial first-time buyer grant and no land transfer tax rebate. The NLHC First-time Homebuyers Program provides an interest-free down payment loan (up to 5% of the purchase price) and a $1,500 legal fee grant — but the income sliding scale cuts your loan by $500 for every $1,000 you earn above $85,000, and the program caps out entirely above $95,000. The guide maps the sliding scale at every income level, explains the 10% variance policy for buying above the $350,000 regional cap, shows how to stack the FHP with the federal FHSA ($40,000 lifetime, no repayment) and HBP ($60,000 per person from RRSPs), and calculates exactly how a buyer earning $70,000 can enter the market with near-zero personal savings — provided they start the FHSA early enough.

Oil Tank Protocol — The Hazard That Kills Transactions

Oil-fired heating remains dominant in older NL homes, and approximately 40% of all domestic oil spills in Canada originate from residential heating tanks. A single leak can trigger soil remediation exceeding $100,000. Insurers refuse to bind policies on exterior tanks older than 15 years and interior tanks older than 25 years — and without a bound insurance policy, your mortgage lender will not fund. The guide provides a complete oil tank assessment protocol: HOST tag verification, age limit thresholds by insurer type, replacement costs ($2,000 to $4,000 for the tank plus $500 to $1,000 for environmental disposal), and a tactical roadmap for the TakeCharge NL Oil-to-Electric rebate program — including the three eligibility traps that disqualify most first-time buyers (the 500-litre fuel consumption record requirement, the electric baseboard exclusion, and the 200-amp panel upgrade float).

Basement Water Infiltration — The Structural Risk in Every Older Home

The combination of St. John's aging housing stock, severe North Atlantic precipitation, relentless freeze-thaw cycles, and historical construction that lacked modern waterproofing membranes makes basement water infiltration endemic. The guide details the warning signs to spot during showings (efflorescence, fresh paint, running dehumidifiers), the repair cost spectrum (interior crack injection at $600 to $1,500 per fracture, sub-slab drainage systems at $5,000 to $10,000, full exterior excavation at $10,000 to $15,000+), and why the densely packed urban core often makes exterior excavation physically impossible — forcing buyers toward specialized interior systems.

Property Taxes by Municipality — The $660 Annual Difference That Changes Where You Buy

Mill rates range from 7.4 in Paradise to 9.1 in St. John's. On a $350,000 home, the annual tax difference between downtown St. John's and Paradise is $660 — $55 per month that directly affects your GDS ratio and borrowing power under the stress test. The guide includes current mill rates, water and sewer fees, and total annual tax calculations for St. John's, Mount Pearl, Paradise, and CBS, so you can compare the true cost of ownership before you choose a municipality.

Foundation Types and Financing Risk — From Poured Concrete to Post-and-Pier

NL homes feature a wider range of foundation types than most Canadian markets. Poured concrete (post-1980) is standard and financeable. Cinder block (pre-1970) is porous and water-prone. Preserved wood foundations are viewed as high-risk by lenders and may trigger financing refusal. Post-and-pier and floating foundations in rural areas trigger CMHC's "Type B" seasonal property classification — stricter lending criteria, higher premiums, lower loan caps, and sometimes outright refusal. The guide maps each foundation type to its financing implications so you know before you make an offer whether the property is mortgageable.

Who This Guide Is For

This guide is for first-time home buyers in Newfoundland and Labrador who:

- Are buying their first home in St. John's, Mount Pearl, Paradise, or CBS and need to understand the true closing costs — dual registration fees, inflated legal fees, title insurance, and oil tank liabilities — that the "no land transfer tax" marketing hides

- Work in offshore oil and gas, rig mechanics, or FIFO mining in Labrador and need to navigate the two-year income averaging requirement, variable income underwriting, and the deliberate strategy of buying below borrowing capacity to hedge against the next commodity crash

- Are returning to Newfoundland from Alberta or Ontario — or migrating from the mainland for the first time — and assume the process mirrors the Torrens system, standardized inspections, and straightforward land transfer taxes they left behind

- Earn under $95,000 and need to thread the NLHC First-time Homebuyers Program sliding scale with the FHSA and HBP to assemble a full down payment from near-zero savings

- Are looking at older homes in the urban core or rural properties outside the CMA and need to assess oil tank insurance risk, basement waterproofing costs, foundation financing complications, and septic system compliance before they waive a single condition

Why Not Free Tools and Government Websites?

Free information on Newfoundland home buying exists across dozens of sources. Here's what it actually delivers:

- CMHC and federal mortgage guides explain the FHSA and HBP as separate programs. They assume a Torrens title system that doesn't exist in Newfoundland, calculate closing costs that don't include the dual registration fee, and provide no guidance on how the NLHC FHP stacks with federal programs or how its income sliding scale affects your specific down payment math.

- The NLHC website explains the First-time Homebuyers Program in detail — income thresholds, the variance policy, the sworn Affidavit requirement. It does not explain how the program's 6-to-8-week processing time interacts with a 30-day closing, how to bridge the funding gap if you need to float costs, or how to combine the FHP with the FHSA and HBP to maximize your total down payment.

- TakeCharge NL documents the $22,000 oil-to-electric rebate. It does not warn you about the 500-litre fuel consumption trap that disqualifies vacant homes, the electric baseboard exclusion, or the critical requirement to photograph the HOST tag before the old tank is removed — the single most common reason buyers lose the entire rebate.

- r/newfoundland and r/StJohns threads are where buyers share the unvarnished truth — $5,000 legal fees, $1,000 just to haul away a fiberglass tank, 8 to 14 competing offers on every move-in-ready home. But Reddit advice is mixed with outdated information predating the $60,000 HBP increase, the FHSA launch, and current mill rate changes. Sorting current from expired requires cross-referencing every claim.

- Realtor blogs market Newfoundland's affordability without mentioning the Registry of Deeds mechanics, the oil tank insurance cliff, the $15,000 basement waterproofing bill, or the foundation types that make rural homes unmortgageable. Their business model depends on you buying, not on you understanding what it actually costs after closing.

This guide fills the Newfoundland-specific gap — the space between knowing the province is affordable and knowing how to buy here without walking into a Registry of Deeds shock, an oil tank insurance collapse, a basement remediation crisis, or a government program you should have applied to six months earlier. It's the analysis that would take a real estate lawyer, a mortgage broker, an environmental inspector, and a tax accountant to assemble — structured as a reference you own permanently.

— Less Than One Hour of Your NL Real Estate Lawyer's Time

A single oil tank replacement with environmental disposal runs $2,500 to $4,000. A basement waterproofing job on an older St. John's home costs $5,000 to $15,000. A missed FHSA contribution year is $8,000 in tax-deductible room you can never reclaim. A miscalculated closing budget that ignores the dual registration fee creates a $2,700 to $3,300 cash shortfall on the day you need to sign. An unused NLHC legal fee grant is $1,500 in non-repayable money you never applied for. An oil tank HOST tag photo you forgot to take before removal voids a $22,000 TakeCharge rebate.

This guide doesn't replace your lawyer or your mortgage broker. But it gives you the registration fee math, the program stacking strategy, the oil tank protocol, and the closing cost matrix that ensure you capture every dollar of provincial and federal assistance, avoid every hidden liability, and understand every cost before you sign — instead of discovering them at the lawyer's office, during the insurance application, or when the spring thaw floods your basement.

If it catches a single oil tank insurance problem, captures a single government program you would have missed, or prevents a single uninformed purchase on a property with a defective foundation, it pays for itself before you finish reading it.

30-day money-back guarantee. If the guide doesn't sharpen your buying strategy and protect your closing costs in Newfoundland's market, you pay nothing.

Your download includes 8 PDFs: the full 10-chapter guide, the quick-start checklist, plus 6 standalone worksheets you can print and use independently — the Registration Fee Calculator (dual deed + mortgage formula), Program Stacking Worksheet (FHSA + HBP + NLHC FHP), Oil Tank Assessment Checklist, Closing Cost Worksheet, Property Tax Comparison by Municipality, and Home Inspection Red Flag Guide.

Download the free Newfoundland and Labrador Quick-Start Home Buying Checklist to see the step-by-step action plan covering saving, searching, making an offer, closing, and moving in. When you're ready for the full registration fee calculations, program stacking strategy, and oil tank protocol, the complete guide is here.

Newfoundland gives you the most affordable housing in Canada. This guide makes sure you keep that advantage — and don't lose it to the costs nobody warned you about.