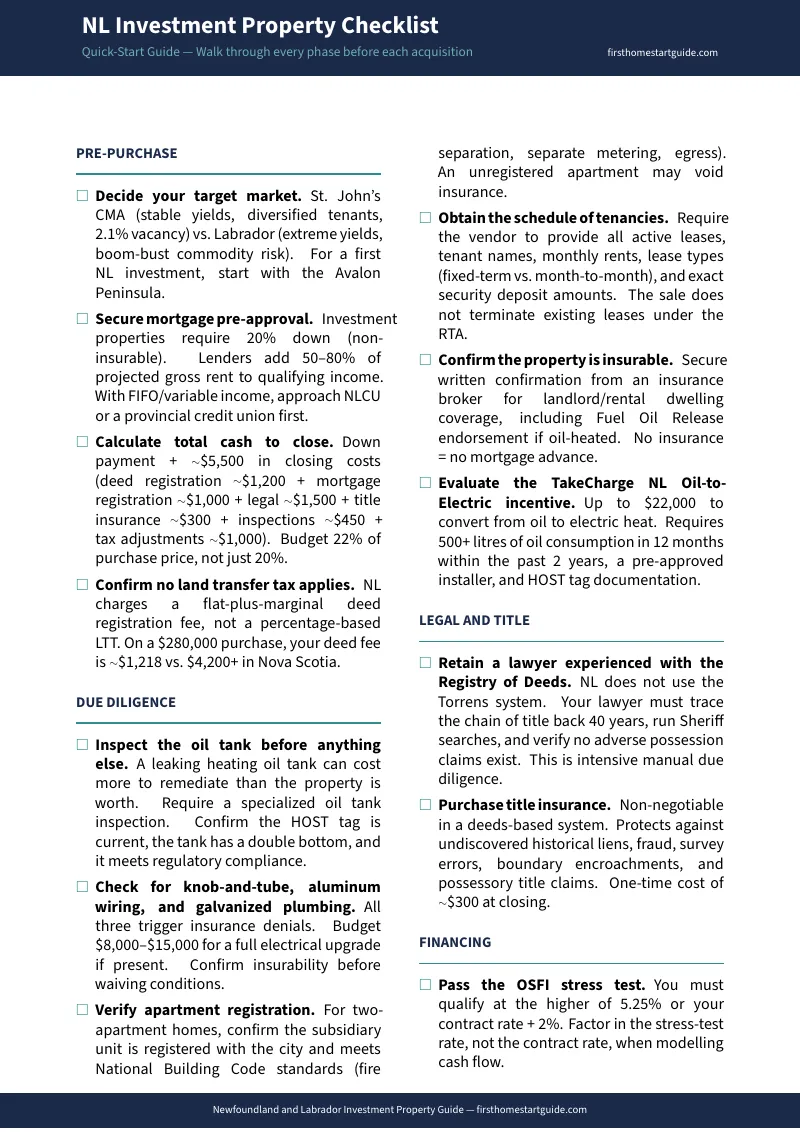

The Spreadsheet Says 10% Gross Yield. Newfoundland's Registry of Deeds, Oil Tank Liability, and Six-Month Rent Notice Period Will Determine Whether You Actually Collect It.

You found a duplex in Mount Pearl listed at $285,000 generating $2,600 per month in gross rent. Or a two-apartment home in Paradise where the vacancy rate is 2.1% and the price-to-rent ratio is half of what you'd pay in Halifax. Or a single-family in St. John's you plan to convert to a short-term rental for the summer tourism season — and the city has no STR licensing bylaw restricting non-owner-occupied listings. You've heard there's no land transfer tax, no rent caps, no foreign buyer restrictions. The numbers clear every hurdle. You're ready to deploy capital.

Then the province-specific reality arrives. Your lawyer isn't looking up a Torrens title certificate on a government database — Newfoundland and Labrador still operates under a Registry of Deeds system, which means they're manually tracing the chain of title back 40 years through the Conveyancing Act, running Sheriff searches for undisclosed liens, and telling you that title insurance isn't optional because the Crown does not guarantee the validity of your deed. Your home inspector flags the heating oil tank — a standard feature in NL's older housing stock — and your insurance broker tells you that if the tank can't pass a specialized inspection confirming its double-bottom status and HOST tag compliance, the property is uninsurable, which means your lender won't advance the mortgage. And your accountant explains that the "no rent caps" marketing line comes with a catch: the Residential Tenancies Act, 2018 requires six months' written notice for any rent increase on a month-to-month tenancy — meaning you can charge market rate, but you can't adjust to it for half a year after you decide to.

Here's what no single resource explains: Newfoundland and Labrador layers a zero-LTT cost advantage (deed registration fees of roughly $2,200 on a $280,000 purchase versus $6,475 or more in Ontario) against a pre-Torrens legal framework where every title requires intensive manual due diligence, an aging housing stock where a single leaking oil tank can generate remediation costs exceeding the property's value, a Residential Tenancies Act that gives landlords unlimited rate-setting power but restricts their timing with the longest notice period in the country, a resource-driven economy where St. John's vacancy rates sit at 2.1% while Labrador City oscillates between housing shortages and mass vacancy on a 10-year commodity cycle, and a short-term rental environment where St. John's has no municipal restrictions but the provincial Tourist Accommodations Act requires formal registration and monthly occupancy reporting. Each of these has cost real investors five to six figures because the information existed — scattered across Service NL regulations, the Registry of Deeds CADO database, CMHC vacancy surveys, and local property management forums — but nobody had assembled it into a single underwriting system calibrated to this province.

The Newfoundland and Labrador Investment Property Guide is a Newfoundland Investor Underwriting System — not a motivational overview of Atlantic Canadian real estate, but a structured due diligence framework that maps every NL-specific financial trap, regulatory restriction, and tax integration mechanic into a process you work through before you commit capital. It replaces months of cross-referencing Registry of Deeds procedures, RTA notice periods, oil tank insurance requirements, and CMHC reports with a single reference that tells you exactly what to verify, exactly what the numbers should look like, and exactly where deals go wrong in this province.

What's Inside the Newfoundland Investor Underwriting System

A comprehensive guide, a standalone due diligence checklist, and three printable worksheets (transaction costs calculator, deed registration fee reference, and property inspection checklist) — covering every stage from market selection through post-purchase setup, built specifically for the regulatory mechanics and economic structure that make Newfoundland and Labrador different from every other province:

Zero-LTT Capital Advantage Analysis

Newfoundland and Labrador's biggest structural edge is what you don't pay at closing. Instead of a percentage-based land transfer tax, the province charges a flat-plus-marginal deed registration fee: $100 base plus $0.40 per $100 of value above $500, with mortgage registration fees capped at $5,000 by statute. On a $280,000 duplex with a $224,000 mortgage, your combined registration fees total roughly $2,200 — compared to $6,475 or more for the same purchase in Ontario, or $8,000 in BC's Property Transfer Tax. The guide quantifies exactly how much capital this frees up per deal, how the fee structure scales across different price points, and what NL charges instead — title insurance, legal fees, property tax adjustments, and the dual registration fee mechanic (one for the deed, one for the mortgage) — so your closing cost model reflects reality, not just the marketing line.

Registry of Deeds Legal Framework

This is the single most important structural difference between NL and every western Canadian province. Newfoundland and Labrador does not use the Torrens system. There is no government-guaranteed certificate of title, no "mirror principle" reflecting current ownership, no "curtain principle" that lets you skip historical searches. Your lawyer must trace the root of title back a minimum of 40 years through the Registry of Deeds, run Sheriff searches for outstanding judgments and liens, and verify that no adverse possession claims exist against the property. Title insurance is not optional — it permanently protects against historical defects, fraud, survey errors, and boundary encroachments that a manual deed search might miss. The guide explains how the CADO (Companies and Deeds Online) database works for post-1982 records, what requires physical searches for pre-1982 records dating to 1825, and why this system makes your choice of real estate lawyer a higher-stakes decision than in any Torrens jurisdiction.

Oil Tank Inspection and Environmental Liability

Due to historically cheap heating oil and a near-complete absence of natural gas infrastructure, a significant portion of NL's older housing stock relies on oil heat. A ruptured or leaking domestic heating oil tank can saturate soil and bedrock, generating remediation costs that can easily exceed the property's total value. Insurance providers in NL refuse to underwrite properties with older, non-compliant, or uninspected oil tanks — and without insurance, your lender will not advance mortgage funds. The guide covers the specialized oil tank inspection process (HOST tag verification, double-bottom status, regulatory compliance), the Fuel Oil Release endorsement you need on your property insurance, and the TakeCharge NL Oil-to-Electric Conversion Rebate — up to $22,000 to permanently eliminate the environmental liability by converting to electric heat.

Residential Tenancies Act, 2018 — Rent Strategy

NL's tenancy law gives landlords something Ontario and BC landlords don't have: unlimited rent-setting power with no permanent percentage cap. But it regulates the timing more strictly than most investors expect. You cannot raise rent during the first 12 months. After that, increases are limited to once per 12-month period. Month-to-month tenancies require six months' written notice — the longest in the country. Fixed-term leases cannot be increased mid-term under any circumstances. And removing previously included utilities counts as a rent increase, triggering the same notice and frequency rules. The guide maps every notice period, explains the security deposit cap (three-quarters of one month's rent, held in an interest-bearing trust account), covers the full eviction process through Service NL's Residential Tenancies Board, and shows how to structure lease terms that maximize your operational flexibility within the statutory constraints.

Regional Market Analysis

Three distinct NL markets dissected with current pricing, rental yields, vacancy trends, and demand drivers. St. John's CMA ($250,000-$350,000 duplexes, 2.1% vacancy, diversified tenant base across government, healthcare, Memorial University, and offshore oil FIFO workers). Labrador City (extreme yields during iron ore booms, extreme vacancy during busts, 10-year commodity cycles, structural risk from municipal anti-camp policies). Happy Valley-Goose Bay (near-zero vacancy, government and military tenants, $8 billion federal commitment to 5 Wing Goose Bay, chronic shortage of private rental housing). The guide explains which markets match which strategies — and which markets will destroy leveraged investors who can't tolerate extended vacancy.

Short-Term Rental Under the Tourist Accommodations Act

St. John's is one of the most permissive STR environments in Canada. There are no municipal STR bylaws, no principal-residence restrictions, and no licensing regime — investors can freely operate non-owner-occupied properties as year-round short-term rentals. The only requirements are provincial registration under the Tourist Accommodations Act (display your registration number on all listings), monthly occupancy reporting, and the 4% municipal accommodation tax. The guide covers the full provincial registration process, platform compliance requirements (Airbnb and VRBO must delist non-registered properties), seasonal revenue patterns across St. John's and coastal tourism hotspots, and how STR revenue compares to long-term rental yields in the same markets.

Tax Strategy — CCA, Recapture, Anti-Flipping, and HST Rebates

Net rental income stacks on top of NL's provincial tax brackets, which peak at 19.8% on income above $282,000 — producing a combined federal-provincial marginal rate nearing 54% at the top. The guide covers the Capital Cost Allowance (Class 1, 4% declining balance) as an income-sheltering tool, the recapture risk when you sell (all previously claimed CCA is taxed at 100% of your marginal rate, not the capital gains rate), the federal 12-month anti-flipping rule that converts your profit from a capital gain to fully taxable business income, and the HST rebate mechanics — including the 100% federal and provincial Purpose-Built Rental Housing rebate for qualifying new construction and the standard NRRP rebate of up to $12,600 per unit for smaller projects.

Two-Apartment Home Registration and Municipal Requirements

Two-apartment homes are the primary investment vehicle in NL — and the subsidiary unit must be registered with the municipality and meet National Building Code standards for fire separation, separate metering, and egress. An unregistered apartment exposes you to enforcement action and may void your insurance. The guide covers registration requirements, the inspection standards that determine compliance, water tax obligations for multi-unit properties, and how to verify registration status before you submit an offer.

Financing and Credit Union Strategy

Investment properties require 20% down under OSFI Guideline B-20, with all borrowers stress-tested at the higher of 5.25% or contract rate plus 2%. The guide covers rental income qualification mechanics (lenders add 50-80% of projected gross rent to qualifying income), the Labrador appraisal gap (remote appraisals routinely come in below purchase price due to lack of comparable sales), and why NL's credit union network — particularly the Newfoundland and Labrador Credit Union (NLCU) — is a strategic financing alternative for investors with FIFO or variable resource-sector income that Schedule A banks won't touch.

Who This Guide Is For

This guide is for real estate investors targeting Newfoundland and Labrador markets who:

- Are based in Ontario, BC, or the Maritimes and evaluating NL's price gap — where you can acquire a cash-flowing duplex for less than a one-bedroom condo in Toronto — but need to understand the Registry of Deeds framework, oil tank liability, and provincial tenancy law before you deploy capital 3,000 kilometres from home

- Are local NL earners in the offshore oil sector, mining, healthcare, or government using high T4 income to build a rental portfolio and need to understand how NL's provincial tax brackets interact with rental income, CCA claiming strategy, and the recapture risk before you scale beyond your first property

- Plan to purchase a two-apartment home or convert a single-family into a duplex and need to verify municipal registration requirements, National Building Code compliance, fire separation standards, and water tax obligations before committing to a property that may have an unregistered subsidiary unit

- Want to operate short-term rentals in St. John's or NL's coastal tourism markets and need to confirm Tourist Accommodations Act registration requirements, municipal accommodation tax obligations, seasonal revenue patterns, and how the provincial framework compares to the restrictive STR regimes in Toronto, Vancouver, and Halifax

- Are evaluating Labrador's resource markets and need an honest, data-backed assessment of the boom-bust commodity cycle, the structural risks created by anti-camp municipal policies, the appraisal gap problem with remote financing, and the conditions under which Labrador City or Happy Valley-Goose Bay delivers extraordinary returns versus catastrophic vacancy

- Want every NL-specific regulation, tax calculation, and due diligence requirement in one reference — instead of assembling it from Service NL tenancy forms, the CADO database, CMHC vacancy surveys, TakeCharge NL program details, and local property management forums that may predate the RTA 2018 overhaul

Why Not Free Tools and Forums?

Free information on Newfoundland and Labrador real estate investing exists. Here's what it actually delivers:

- Reddit forums (r/PersonalFinanceCanada, r/RealEstateCanada) are where someone in a 2021 thread says NL has "no rent control," someone in 2023 corrects that the province had temporary pandemic-era caps, and a third poster links to a Service NL page that may or may not reflect the current post-cap regulatory framework. You'll find genuinely useful experience reports from NL landlords mixed with advice that predates the RTA 2018 overhaul, confuses the Registry of Deeds system with Torrens title, or generalizes mainland Canadian rules to a province with fundamentally different legal mechanics. Sorting current from outdated takes longer than reading a guide that has already done it.

- Service NL forms and tenancy guides give you the statutory notice periods, security deposit rules, and eviction procedures. They don't explain how the six-month rent increase notice period interacts with your cash flow modelling, how the three-quarters-of-one-month security deposit cap compares to other provinces, or how the interest-bearing trust account requirement works in practice. You get the regulatory inputs without the operational strategy that determines whether your tenancy structure actually optimizes for NL's specific framework.

- National investing books and courses teach cap rate, DSCR, and rental yield analysis that applies everywhere. They don't cover NL's Registry of Deeds system, the oil tank environmental liability that can make a property uninsurable and unmortgageable, the six-month rent increase notice period, the Tourist Accommodations Act registration requirements, or the TakeCharge NL Oil-to-Electric rebate that can eliminate a five-figure environmental risk while forcing equity appreciation. Applying national frameworks to NL-specific structures is how investors model a deal under the wrong legal and insurance assumptions.

- CMHC reports and provincial housing data provide vacancy rates, rental rate tracking, and market trends. They don't integrate those numbers into an underwriting framework that accounts for the Registry of Deeds closing process, oil tank insurability requirements, two-apartment home registration compliance, the Labrador commodity cycle, or the provincial tax brackets that determine how much of your rental income you actually keep. You get the data points without the system that connects them.

This guide fills the Newfoundland-specific gap — the space between knowing how to analyze a rental property in general and knowing how to underwrite one in a province where a pre-Torrens legal framework, oil tank environmental liability, the longest rent increase notice period in the country, and a resource-driven economy with wildly divergent regional risk profiles can each independently turn a profitable deal into a losing one. It's the analysis that would take an NL real estate lawyer, a provincial tax accountant, and a local property manager to assemble — structured as a reference you own permanently.

— Less Than One Oil Tank Inspection

A specialized oil tank inspection in St. John's runs $200 to $400. Environmental remediation for a leaking tank starts at $15,000 and routinely exceeds $50,000. A real estate lawyer's closing fees in NL run $1,200 to $1,800 — and if your lawyer misses a defect in the 40-year title chain, the consequences are permanent. A two-apartment home with an unregistered subsidiary unit can trigger municipal enforcement action and void your insurance coverage. A rent increase issued without the required six months' written notice is automatically invalid under the RTA, costing you six months of revenue you thought you'd locked in.

This guide doesn't replace your real estate lawyer or your property inspector. But it gives you the Registry of Deeds framework, oil tank due diligence protocol, RTA strategy, regional market analysis, and tax integration breakdown that ensure you identify every NL-specific risk before you're contractually committed — instead of discovering them on your first title search surprise, your first insurance denial, or your first invalid rent increase notice.

If it catches a single title issue, prevents a single oil tank insurance denial, or saves you from issuing an invalid rent increase notice on a six-figure acquisition, it pays for itself before you've finished reading it.

30-day money-back guarantee. If the guide doesn't sharpen your underwriting and protect your capital in Newfoundland and Labrador's regulatory environment, you pay nothing.

Download the free Newfoundland and Labrador Quick-Start Investment Property Checklist to see the due diligence framework covering pre-purchase research, oil tank inspection, title search requirements, financing, and post-purchase setup. When you're ready for the full Registry of Deeds playbook, RTA strategy, regional market analysis, and tax integration system, the complete guide is here.

The deal looks good on the spreadsheet. This guide tells you whether Newfoundland agrees.