The Previous Owner's Tax Bill Was $3,122. Yours Will Be $5,017.

You found a three-bedroom home in Dartmouth listed at $450,000. It looked right: new roof, decent yard, 20-minute ferry to downtown Halifax. The listing showed annual property taxes of $3,122. Your mortgage broker ran the numbers and said you could carry it. You made an offer, won the bidding war, and closed.

Seven months later, the Property Valuation Services Corporation (PVSC) sent your first assessment notice. Your property taxes were not $3,122. They were $5,017 --- an overnight increase of $1,895 per year, or $158 per month that you never budgeted for. Your real estate agent never explained it. Your lender did not model it. No website warned you.

The previous owner had held the home for twelve years under Nova Scotia's Capped Assessment Program (CAP), which limits annual assessment increases to the CPI. Their taxable assessment had crept to $280,000 while the market value climbed to $450,000. The moment you bought the home, the cap was removed. PVSC reset the taxable assessment to the full purchase price. You inherited the market value. The previous owner kept the tax savings.

That is the CAP trap. And it is just the first layer.

The problem is not that Nova Scotia is expensive --- with the Halifax median at $592,000, it remains less than Toronto or Vancouver. The problem is that Nova Scotia layers hidden liabilities on top of the purchase price that no other Canadian province combines in the same way. A flat 1.5% municipal Deed Transfer Tax with absolutely no first-time buyer exemption --- $6,750 in cash on a $450,000 home that cannot be rolled into your mortgage. An aging housing stock where insurance companies mandate oil tank replacement after 14 years regardless of physical condition --- and a buried tank with contaminated soil can cost $100,000+ to remediate. A pre-1960 urban core where knob-and-tube wiring kills your insurance application and collapses your mortgage. Suburban properties on septic systems and private wells where Nova Scotia's bedrock geology naturally produces hazardous levels of arsenic and uranium. And a coastal property regulatory framework thrown into chaos by the indefinite delay of the Coastal Protection Act.

The Nova Scotia First-Time Home Buyer Guide is a Hidden-Liability Defense System --- a structured walkthrough of every Nova Scotia-specific financial trap, environmental hazard, insurance barrier, and assistance program that determines whether your home purchase builds equity or quietly drains it. It replaces months of cross-referencing the PVSC website, Service Nova Scotia portals, credit union eligibility pages, dense municipal bylaws, and frantic Reddit threads about the CAP trap with a single reference that tells you exactly how much closing really costs, exactly what your post-purchase property taxes will be, and exactly which physical liabilities can bankrupt you in your first year of ownership.

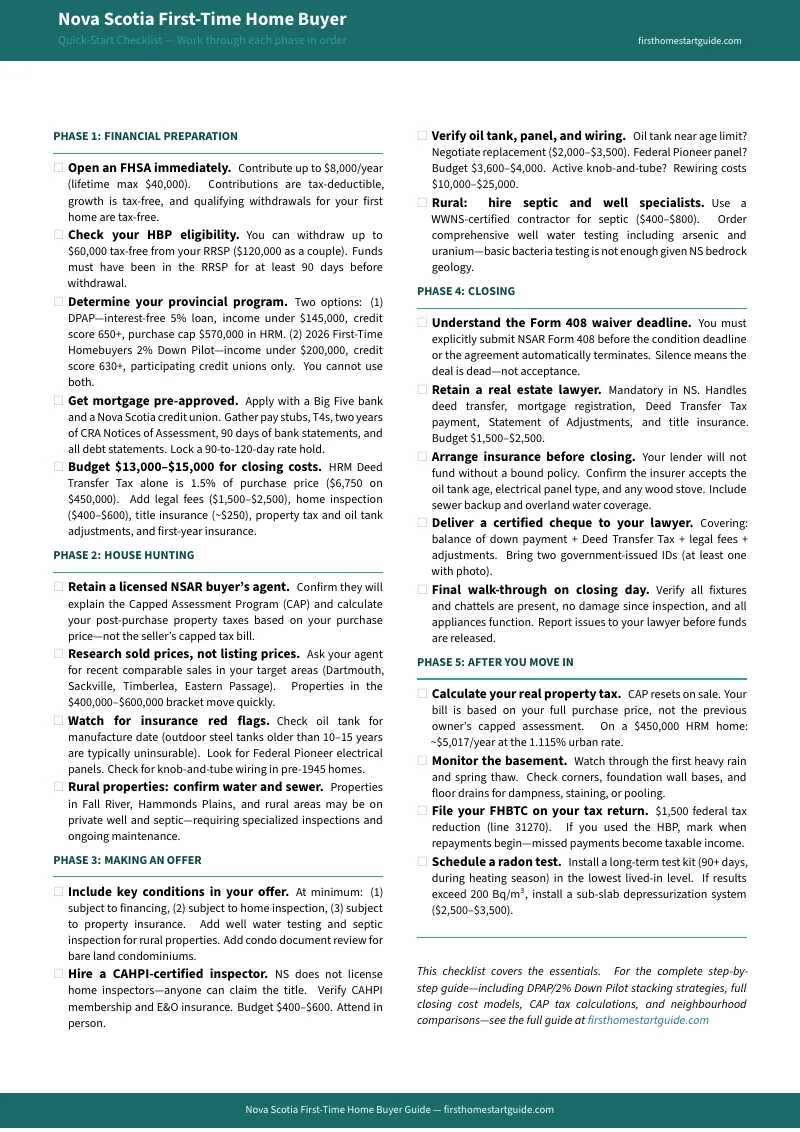

A 15-chapter guide, a 20-item quick-start checklist, and 3 standalone printable tools --- covering the CAP trap assessment reset, the HRM Deed Transfer Tax with no exemptions, the 2% Down Payment Pilot through Nova Scotia credit unions, the DPAP interest-free loan, FHSA + HBP stacking strategies, oil tank insurance mandates, knob-and-tube wiring remediation costs, septic and well water due diligence, coastal erosion regulatory chaos, and regional market intelligence across Halifax, Dartmouth, Eastern Passage, Lower Sackville, Bedford, Truro, Cape Breton, and the South Shore. Five printable files:

- guide.pdf --- The full 15-chapter guide

- checklist.pdf --- Quick-start home buying checklist (20 items across 5 phases)

- closing-cost-worksheet.pdf --- Fillable closing cost breakdown with urban and rural examples

- due-diligence-checklist.pdf --- Bring to every property viewing --- oil tank, electrical, septic, well water, and coastal risk items

- property-tax-calculator.pdf --- CAP uncapping math on one page --- calculate your real post-purchase tax bill before you make an offer

What's Inside the Hidden-Liability Defense System

A comprehensive 15-chapter guide with a quick-start checklist --- covering every stage from financial preparation through your first year of ownership, built specifically for the financial traps, environmental hazards, and regulatory complexity that make Nova Scotia fundamentally different from every other Canadian province:

The CAP Trap Decoded

Generic Canadian home buying guides tell you to check the MLS listing for property tax estimates. In Nova Scotia, that number is a financial trap. The Capped Assessment Program limits annual assessment increases to the CPI for existing homeowners (2.6% for 2026). But the cap resets to full market value the moment the property is sold. The guide gives you the mathematical breakdown: how a home assessed at $280,000 under the cap jumps to $450,000 at the purchase price, how that translates to a $1,895/year increase you never budgeted for, how to use the PVSC website to calculate your real post-purchase tax bill before you draft an offer, and the 30-day Request for Review appeal window. You stop relying on the seller's tax bill and start calculating your own.

The Deed Transfer Tax With No Exemptions

Unlike Ontario (which rebates up to $4,000), British Columbia (which exempts purchases under $500,000), or PEI (which offers a first-time buyer exemption), Nova Scotia charges every buyer the full municipal Deed Transfer Tax with zero relief. In Halifax, the rate is a flat 1.5% of the purchase price --- $6,750 on a $450,000 home, $7,500 on $500,000, $8,550 on $570,000. This is unmortgageable cash due at your lawyer's office before you receive the keys. The guide includes a quick-reference tax table, the Provincial Non-Resident Deed Transfer Tax (escalated to 10% as of April 2025), the six-month relocation exemption for interprovincial migrants, and the advanced strategy of using FHSA tax refunds to fund the DTT.

Down Payment Program Navigator

Nova Scotia lacks a broad provincial grant, but it offers two targeted programs that most buyers misunderstand or miss entirely. The guide maps both against their eligibility matrices: the 2% Down Payment Pilot (credit unions only --- CUA, East Coast, Coastal Financial, Valley --- income under $200,000, credit score 630+, purchase cap $570,000 in HRM), which reduces the upfront cash requirement by 60% and bypasses CMHC insurance premiums entirely through a provincial deficiency guarantee. The Down Payment Assistance Program (DPAP --- interest-free 5% loan, income under $145,000, credit score 650+, repayable over 10 years). You cannot combine them. The guide tells you which one fits your profile and how to stack either with the FHSA ($8,000/year, $40,000 lifetime) and HBP ($60,000 per person, $120,000 per couple).

The Oil Tank Liability

Heating oil remains a primary energy source across Nova Scotia. Insurance companies --- not heating technicians --- dictate tank lifespans: 14 years for steel, 20 for fibreglass, with some providers enforcing 10-year limits. If your prospective home has a steel tank that is 13 years old, you will be forced to replace it within a year to maintain coverage. Above-ground replacement runs $1,500 to $2,500. But the catastrophic risk is buried tanks: removal and basic remediation costs $3,000 to $5,000, and contaminated soil or groundwater cleanup can reach six figures. Standard home insurance explicitly excludes pollution from fuel oil. The guide shows you how to read the ULC manufacture label, what to negotiate with the seller, and when to walk away.

Pre-1960 Housing Stock Hazards

The Halifax Peninsula and downtown Dartmouth contain dense concentrations of heritage homes with knob-and-tube wiring. Insurance companies will outright deny coverage for any home with active knob-and-tube circuits. Without an insurance binder, your mortgage collapses. Rewiring costs $10,000 to $25,000. Mid-century homes with aluminum wiring and Federal Pioneer panels present distinct fire hazards --- $3,600 to $4,000 to upgrade. Galvanized steel and lead service pipes require immediate, costly replacement. The guide tells you exactly what to look for during showings (ceramic insulators in the basement, the Federal Pioneer label on the panel) and what each remediation costs so you can price it before your money goes hard.

Septic Systems and Well Water

As Halifax prices push first-time buyers into Sackville, Fall River, and Hammonds Plains, they encounter private well water and septic systems for the first time. A general home inspector cannot adequately assess either. Complete septic replacement costs $3,000 to $25,000. The guide covers WWNS-certified contractor requirements, the pump-out and dye test ($400 to $800), surface pooling indicators, and leach field failure signs. For well water, Nova Scotia's unique bedrock geology produces hazardous levels of arsenic and uranium --- basic bacteria testing is dangerously insufficient. The guide specifies the comprehensive panel required and what to do if results exceed safe limits.

Coastal and Environmental Risk Assessment

Hurricane Fiona demonstrated that coastal Nova Scotia is increasingly exposed to severe weather. The province spent years drafting the Coastal Protection Act, then abruptly delayed implementation and shifted responsibility to individual municipalities. Halifax enforces a 3.8-metre elevation setback above CGVD28. Other municipalities use horizontal setbacks. Some have nothing. The guide maps the current regulatory patchwork, explains flood insurance premiums, and gives you the risk assessment framework for evaluating waterfront and near-coastal properties --- including the long-term erosion data that determines whether your investment will outlast your mortgage.

The Complete Closing Cost Model

Every dollar, itemized. The guide runs a line-by-line breakdown for a $450,000 HRM purchase: CMHC insurance premiums at four down payment tiers, the $6,750 Deed Transfer Tax, legal fees ($1,500 to $2,500), title insurance (~$250), home inspection ($400 to $600), property tax adjustment (~$1,500), oil tank fuel adjustment (~$800), and first-year homeowner insurance ($1,200 to $1,800). Urban total: $13,000 to $15,000 beyond the down payment. Rural total: add $800+ for septic, well water, and oil tank inspections. None of it can be rolled into your mortgage.

The NSAR Offer Mechanics

Nearly every residential transaction in Nova Scotia uses the standardized NSAR Agreement of Purchase and Sale. The guide decodes the critical Form 408 active waiver deadline --- silence does not mean acceptance in Nova Scotia, it means the deal is dead. If you fail to submit Form 408 before the condition deadline, the agreement automatically terminates. The guide covers essential subject clauses (financing, inspection, insurance), rural-specific conditions for well water and septic, and the negotiation leverage points that protect your deposit while keeping you competitive.

Regional Market Intelligence

What $450,000 buys varies dramatically across Nova Scotia. The guide covers 11 areas with April 2026 pricing: Halifax Peninsula ($550,000 to $800,000+, heritage stock, high maintenance risk), Dartmouth ($400,000 to $600,000, ferry access, the affordability harbour side), Eastern Passage ($400,000 to $700,000, coastal living, 20-minute commute), Lower Sackville ($350,000 to $550,000, highest square footage per dollar in HRM), Timberlea, Bedford and Fall River (suburban, some well/septic), Truro ($250,000 to $400,000, well below HRM pricing), Cape Breton ($150,000 to $300,000, most affordable), Bridgewater and the South Shore, and the Annapolis Valley. Each area includes buyer profiles, infrastructure considerations, and specific risks.

Standalone Printable Tools

Every paid download includes 3 standalone tools you can print and bring to your lender meeting, home viewing, or lawyer appointment:

- Closing Cost Worksheet --- fillable breakdown with worked urban and rural examples, CMHC premiums at four down payment tiers, and the DTT calculation

- Due Diligence Checklist --- oil tank manufacture date verification, electrical panel brand check, knob-and-tube detection, septic indicators, well water testing requirements, and coastal risk items

- Property Tax Calculator --- the CAP uncapping formula, PVSC assessment lookup instructions, urban and rural tax rates, and worked examples showing the exact difference between the seller's capped taxes and your uncapped taxes

Who This Guide Is For

- Long-term Nova Scotia residents paying $1,800 to $2,268/month in Halifax rent, targeting the $400,000 to $600,000 bracket on a minimum 5% down payment, who need to extract maximum value from the 2% Down Pilot and FHSA + HBP stacking because the province offers almost nothing for first-time buyers --- and who need the exact DTT cash requirement and CAP trap calculation before they can accurately model what they can afford

- Interprovincial migrants from Ontario and BC who see a $500,000 Dartmouth home and think "deal" without understanding that it may sit on a 13-year-old oil tank, contain knob-and-tube wiring that kills their insurance application, or come with a capped property tax assessment that will double the year after they close --- and who face a 10% Provincial Non-Resident Deed Transfer Tax if they purchase before physically relocating

- Atlantic Immigration Program newcomers and international graduates settling in Nova Scotia to fill healthcare, trades, and childcare shortages, who need the entire Canadian home buying process explained from scratch --- stress test mechanics, CMHC insurance, the FHSA --- alongside the Nova Scotia-specific regulatory layer and credit union pilot programs designed for lower down payments

- Remote knowledge workers retaining urban salaries while buying into the maritime lifestyle, who are well-capitalized but routinely misjudge ongoing costs --- particularly the CAP trap, which adds $1,500 to $2,000/year to their property tax bill the moment they close, and the oil tank and septic maintenance requirements that do not exist in the urban centres they came from

Why Not Free Tools and Forums?

Free information on buying a home in Nova Scotia exists. Here is what it actually delivers:

- CMHC gives you excellent macroscopic data on national housing trends and federal program outlines. It will not warn you about a Halifax oil tank lifespan mandate, calculate the HRM Deed Transfer Tax, or explain why the MLS-listed property tax figure is a trap. You get federal policy descriptions without the provincial specificity required to navigate the Maritimes.

- Service Nova Scotia and PVSC websites technically contain the raw information on the Deed Transfer Tax, the Capped Assessment Program, and coastal bylaws. It is written in dense bureaucratic legalese that requires prior subject-matter expertise to decode. These portals offer policy descriptions, not practical consumer advice. The CAP page explains the program mechanics --- it does not tell you how to calculate your post-purchase tax bill or warn you that the seller's listed taxes are irrelevant.

- Credit union landing pages detail the 2% Down Pilot eligibility criteria clearly. They are top-of-funnel mortgage lead-generation tools, not comprehensive educational resources. They will not help you decide between the 2% Pilot and DPAP, explain the FHSA stacking strategy, or warn you about the closing costs that sit on top of whatever down payment program you choose.

- Reddit threads (r/Halifax, r/NovaScotia, r/PersonalFinanceCanada) contain genuine warnings about the CAP trap from buyers who were blindsided. They are mixed with outdated program details, incorrect DTT calculations, agents defending the status quo, and advice from provinces with entirely different tax structures. Sorting current from dangerous takes longer than reading a guide that already did it.

- Real estate brokerage blogs offer polished neighbourhood profiles, staging tips, and market statistics that cast the market in a perpetually positive light. They rarely address failing septic dye tests, lead pipes, the formulation of the Deed Transfer Tax, or the CAP uncapping math that determines whether a buyer can actually afford the home after the first year. Agents are incentivized to close transactions, not to help you calculate whether the seller's listed property tax is a reliable indicator of your future cost.

This guide fills the Nova Scotia-specific gap --- the space between knowing how to buy a home in Canada and knowing how to buy one in a province where the Capped Assessment Program resets your property taxes overnight, there is no first-time buyer relief on the Deed Transfer Tax, an aging oil tank triggers an insurance mandate that cannot be deferred, and Nova Scotia's bedrock geology means a basic well water bacteria test is dangerously insufficient. It is the risk analysis that would take a Nova Scotia real estate lawyer, a PVSC assessment analyst, and a licensed oil tank and septic contractor to assemble --- structured as a reference you own permanently.

--- Less Than a Single Month's CAP Trap Tax Increase

A single consultation with a Nova Scotia real estate lawyer runs $200 to $400 per hour. Failing to calculate the CAP uncapping on a $450,000 home means discovering a $158/month property tax increase seven months after closing, with no recourse. Buying a home with a 14-year-old steel oil tank means $1,500 to $2,500 in mandatory replacement within a year --- or losing your insurance coverage entirely. Missing the FHSA contribution window means losing the tax refund that could have covered your Deed Transfer Tax.

This guide does not replace your real estate agent, your lender, or your lawyer. But it gives you the CAP trap calculator, the closing cost model, the down payment program navigator, the oil tank and septic inspection framework, and the regional market intelligence that ensure you identify every Nova Scotia-specific liability before your money goes hard --- instead of discovering them when the PVSC assessment notice arrives in the mail.

If it prevents a single CAP trap surprise, catches a single oil tank insurance mandate, or alerts you to well water contamination risks before you waive your inspection conditions --- it pays for itself before you finish reading it.

30-day money-back guarantee. If the guide does not sharpen your Nova Scotia home buying analysis and protect your capital, you pay nothing.

Download the free Nova Scotia Quick-Start Home Buying Checklist to see the step-by-step framework covering pre-approval, due diligence management, inspections, and closing. When you are ready for the full CAP trap calculator, closing cost model, down payment program navigator, and the complete 15-chapter guide, the full toolkit is here.

Nova Scotia's hidden-liability landscape rewards buyers who calculate it in advance and punishes those who trust listing data. This guide makes sure you're on the right side.