You Found a Home in Iqaluit for $550,000. Nobody Mentioned That You Do Not Own the Land, the Appraisal Will Come in $80,000 Below the Sale Price, and Your Annual Operating Costs Are $17,100 on Top of the Mortgage.

You have been watching the Iqaluit market — checking Atiilu Real Estate, scrolling community Facebook groups, asking colleagues at the GN building whether they have heard of anything coming on. You know the prices are high. You know the inventory is thin. You may even know there are government programs that offer down payment help. What you probably do not know is that when you buy a home in Nunavut, you almost certainly do not own the land underneath it.

That is not a figure of speech. Nunavut municipalities retain ownership of all residential land and issue equity leases — typically 99 years — to homeowners. Your mortgage lender requires the remaining lease term to exceed your amortization by at least ten years (the "plus-ten" rule), and if the lease is too short, your financing falls apart. Meanwhile, the private resale market in Iqaluit has single-digit listings at any given time. Homes sell through word of mouth and Facebook before they reach Realtor.ca. Banks use replacement cost methodology for appraisals, which routinely produces valuations $50,000 to $100,000 below the actual sale price — and you cover that gap in cash. Construction costs run $550 to $650 per square foot. Heating fuel alone costs $4,000 per year. Electricity runs $0.75 per kWh before the NESP subsidy kicks in. There are no local home inspectors — you fly one from Ottawa or Edmonton for $2,500 to $4,000. And 80% of private rental stock in Iqaluit is monopolized by a single REIT, which means if your purchase falls through, your backup plan has a multi-year waitlist.

This is the most information-asymmetric housing market in North America. Every buyer is flying blind — navigating equity leases, forgivable government loans of up to $80,000, permafrost foundation engineering, Arctic operating costs, and a market so small that a single listing can attract every qualified buyer in the territory. No standard Canadian home buying guide addresses any of it. The CMHC workbook does not mention equity leases. The NHC website covers its own programs but not the private market. Reddit threads contain fragments scattered across years with no way to tell what is current. Until now.

The Nunavut First-Time Home Buyer Guide is an Arctic Buyer’s Navigation System — a structured decision framework that connects every Nunavut-specific land tenure rule, government program, permafrost risk, financing constraint, and operating cost into a single step-by-step roadmap from pre-approval through your first 30 days as a homeowner above the tree line.

What's Inside the Arctic Buyer’s Navigation System

The complete 13-chapter guide with two appendices, eight standalone printable worksheets, and a quick-start checklist — covering every stage from understanding what you actually own when you buy in Nunavut through closing and surviving your first Arctic winter:

Land Tenure and the Equity Lease System

The single biggest knowledge gap for every first-time buyer in Nunavut. Fee simple ownership is virtually nonexistent — municipal referendums have repeatedly voted against selling land to individuals. Instead, you buy the physical structure and lease the lot from the municipality through an equity lease, making payments against the municipal development cost over 15 to 20 years until your annual rent drops to $1 or $50 per year. The guide explains why a fully paid equity lease functions almost identically to freehold, how the "plus-ten" rule determines whether your mortgage gets approved, what happens when a lease term is too short, and how Commissioner’s Land parcels outside municipal boundaries work under a completely different system. It also covers the ballot draw process for acquiring a new municipal lot — weighted by years of residency and Inuit beneficiary status.

NHC Programs and Financial Assistance Stacking

Up to $80,000 in forgivable down payment assistance — plus five more programs most buyers never discover. The Nunavut Housing Corporation’s Nunavut Downpayment Assistance Program (NDAP) provides up to $80,000, forgiven over 10 years of continuous occupancy. The Nunavut Housing Assistance Program (NHAP) offers up to $250,000 for new construction. The Home Repair Program (HRP) covers up to $100,000 for existing homes. The Emergency Repair Program (ERP) provides $15,000 for urgent health and safety issues. The guide walks through every program’s eligibility requirements, application timelines, and forgiveness conditions — then shows how to stack NHC assistance with the federal FHSA ($40,000 lifetime, tax-free), the Home Buyers’ Plan ($60,000 RRSP withdrawal), and the $1,000 per month GN residency allowance for employees leaving staff housing. A couple combining FHSA, HBP, and NDAP can assemble over $200,000 in down payment capital.

Permafrost Foundations and Arctic Due Diligence

The engineering reality that determines your maintenance costs for every year you own the home. Nunavut properties sit on one of three foundation systems: screw piles (steel helicals driven into permafrost), space frames (elevated steel grillages that allow airflow beneath the structure to keep permafrost frozen), or thermosyphon-assisted foundations (passive cooling devices that stabilize ground temperatures). Each system has different inspection requirements, failure modes, and long-term maintenance profiles. The guide covers what to look for, what questions to ask, how to evaluate pile integrity in continuous permafrost versus the warmer margins, and why flying in a certified inspector from the south ($2,500 to $4,000) is not optional — it is the most important money you spend in the entire transaction.

The $17,100 Annual Operating Cost Budget

The expense that turns an affordable mortgage into an unaffordable home. A typical Nunavut home costs roughly $17,100 per year to operate: heating fuel at approximately $4,000, electricity at roughly $0.75 per kWh (with the NESP subsidy covering 50% of the first 700 to 1,000 kWh per month), trucked water delivery at approximately $1,750, and property taxes averaging $8,650 in Iqaluit. The guide breaks down each cost line with current rates, explains the difference between utilidor-serviced and trucked-water lots (a difference of thousands per year), and maps the 32% gross debt service rule with Arctic operating costs factored in — so you know your true borrowing ceiling before you start searching.

Financing in a Market Where the Rules Are Different

Six lenders, replacement cost appraisals, and the gap you cover in cash. The northern lending landscape is extremely compressed: FNBC, RBC, CIBC, TD, and one or two credit unions. Rate competition is limited. Appraisers use replacement cost methodology because comparable sales barely exist, which systematically produces valuations below actual market prices. The guide explains the OSFI stress test with Nunavut-specific examples, how CMHC insurance works on equity lease properties, how to prepare for and negotiate around the appraisal gap, and why you need $20,000 to $50,000 in cash reserves above your down payment.

Building New vs. Buying Existing

The sealift window, $550 to $650 per square foot, and why timing determines your budget. Construction materials arrive by sealift once per year during the summer shipping window. Missing the sealift means air freight at catastrophic premiums or waiting another year. Building new in Nunavut costs $550 to $650 per square foot — a 1,200 square foot home runs $660,000 to $780,000 before the lot. The guide covers modular housing options, the sweat equity approach where owners contribute labour to reduce costs, and the NHAP program that provides up to $250,000 for new construction.

The Closing Process

No land transfer tax — but Land Titles Tariffs, legal fees, and equity lease transfers still require preparation. Nunavut charges no land transfer tax, saving you thousands compared to Ontario or B.C. But the closing still involves Land Titles Tariffs ($2.00 per $1,000 for property transfer, $1.00 per $1,000 for mortgage registration), legal fees ($2,500 to $4,000 through firms like Cooper Regel North or Morrison Law), equity lease transfer approval from the municipality, and confirmation that all property taxes and water bills are current. The guide maps every line item so the final invoice holds no surprises.

Eight Standalone Printable Tools

Print them, bring them to appointments, post them on your fridge. Every standalone works as its own document — no need to flip through the full guide during a meeting or inspection:

- Arctic Operating Cost Worksheet — fillable budget with current Iqaluit rates for heating fuel, electricity, trucked water, property taxes, and a GDS ratio calculator. Bring to your mortgage broker.

- Closing Cost Worksheet — every line item from legal fees to Land Titles Tariffs, with an appraisal gap reserve calculator. Bring to your lawyer.

- Arctic Inspection Checklist — what your fly-in inspector must evaluate: pile foundations, fuel tank, heat tape, cistern, sewage, roof, insulation. Bring to the inspection.

- Seasonal Maintenance Calendar — four-season Arctic maintenance schedule plus emergency reference. Post on your fridge.

- NHC Program Reference Card — all territorial and federal programs (NDAP, NHAP, HRP, ERP, FHSA, HBP) with amounts, terms, and eligibility on one page. Bring to your NHC meeting.

- Equity Lease Verification Checklist — what to verify on any listing: lease term, plus-ten rule, municipal accounts, foundation type, fuel tank. Bring when viewing properties.

- Program Stacking Worksheet — calculate your total down payment capital from NDAP, FHSA, HBP, and savings, with monthly cost projection and NDAP forgiveness timeline.

- Staff Housing Transition Reference — for GN employees: comparison table, six-step transition timeline, and financial summary.

Who This Guide Is For

This guide is for first-time buyers in Nunavut who:

- Are relocating to Iqaluit for a Government of Nunavut, federal, or Inuit organization position and transitioning from staff housing to private ownership — and need to understand equity leases, the plus-ten financing rule, and how the $1,000 per month GN residency allowance factors into your affordability calculation

- Have been renting in Iqaluit and are ready to build equity instead of paying into Northview REIT’s portfolio — but need a clear map of NDAP eligibility (requires one year of continuous Nunavut residency), FHSA and HBP stacking, and how to navigate a market with single-digit listings

- Are Inuit beneficiaries exploring the transition from NHC public housing to private ownership through the Nunavut Housing Corporation’s homeownership programs — and need to understand the ballot draw process for lot acquisition, NDAP forgiveness conditions, and how to combine territorial and federal assistance

- Are considering building a new home through NHAP or a modular construction approach — and need to understand the sealift window, construction timelines, foundation engineering requirements, and the $550 to $650 per square foot cost reality

- Work in Rankin Inlet, Cambridge Bay, or Arviat where the private market is even smaller — and need the community-specific guidance on what is available, how lot acquisition works outside Iqaluit, and which NHC programs apply in smaller hamlets

Why Not Free Resources?

Free information on buying a home in Nunavut exists. Here is what each source actually delivers:

- CMHC “Homebuying Step by Step” workbook provides solid financial planning tools — debt ratio calculators, mortgage insurance tables, credit score explanations. What it does not do: mention equity leases, explain why you do not own the land under your house, address the appraisal gap problem, account for $17,100 in annual Arctic operating costs, or acknowledge that the “compare listings and make competitive offers” framework assumes a market with more than single-digit listings. The national framework is generic. The Nunavut realities are absent.

- Nunavut Housing Corporation website publishes program details for NDAP, NHAP, HRP, ERP, and the Tenant-to-Owner Program — each on its own page in policy language with no guidance on how to combine NHC assistance with federal FHSA and HBP programs, no explanation of how NDAP forgiveness conditions interact with your mortgage, and no connection to the private market realities of actually finding and closing on a property. The programs are among the most generous in Canada. Navigating them is not straightforward.

- Local real estate agents and Atiilu Real Estate have genuine Iqaluit market knowledge — from the perspective of professionals who earn a commission when you buy. They will help you find a listing. They will not explain why the equity lease on the half-duplex has 65 years remaining and whether that clears the plus-ten rule on a 25-year amortization, why the appraisal will likely come in below your offer price, or how to budget for permafrost foundation maintenance over the next decade.

- Reddit and community Facebook groups are where northern buyers share real experiences — and where advice about Iqaluit circa 2021 sits next to advice from 2026, where one person’s successful NDAP application used eligibility criteria that have since changed, and where “just call NHC” is the standard response to questions that deserve structured analysis. Valuable fragments with no framework to connect them.

This guide fills the navigation gap — the space between knowing Nunavut has equity leases, government programs, and extreme operating costs, and understanding how they all interact across a single home purchase. It is the analysis an independent advisor with no properties to sell would give you, structured as a permanent reference you own.

— Less Than a Single Day of Flying an Inspector North

Flying a home inspector from Ottawa to Iqaluit costs $2,500 to $4,000. The appraisal gap on a typical purchase can run $50,000 to $100,000. NDAP provides up to $80,000 in forgivable assistance that most eligible buyers either do not know about or apply for too late. A single missed detail on an equity lease — a term that falls short of the plus-ten rule — kills your mortgage approval.

This guide does not replace your real estate lawyer, your mortgage broker, or your home inspector. But it gives you the equity lease verification framework, the NHC program stacking strategy, the Arctic operating cost budget, and the due diligence checklist that ensure you walk into every appointment knowing exactly what to ask, exactly what to budget, and exactly what to never skip — instead of discovering Nunavut’s hidden rules in real time.

If it helps you stack NDAP with the FHSA and HBP to assemble your full down payment, catches an equity lease with insufficient remaining term before your offer goes firm, or prevents you from budgeting for a mortgage without accounting for $17,100 in annual operating costs, it pays for itself before you have finished reading it.

30-day money-back guarantee. If the guide does not make your Nunavut home buying process clearer and your financial position stronger, you pay nothing.

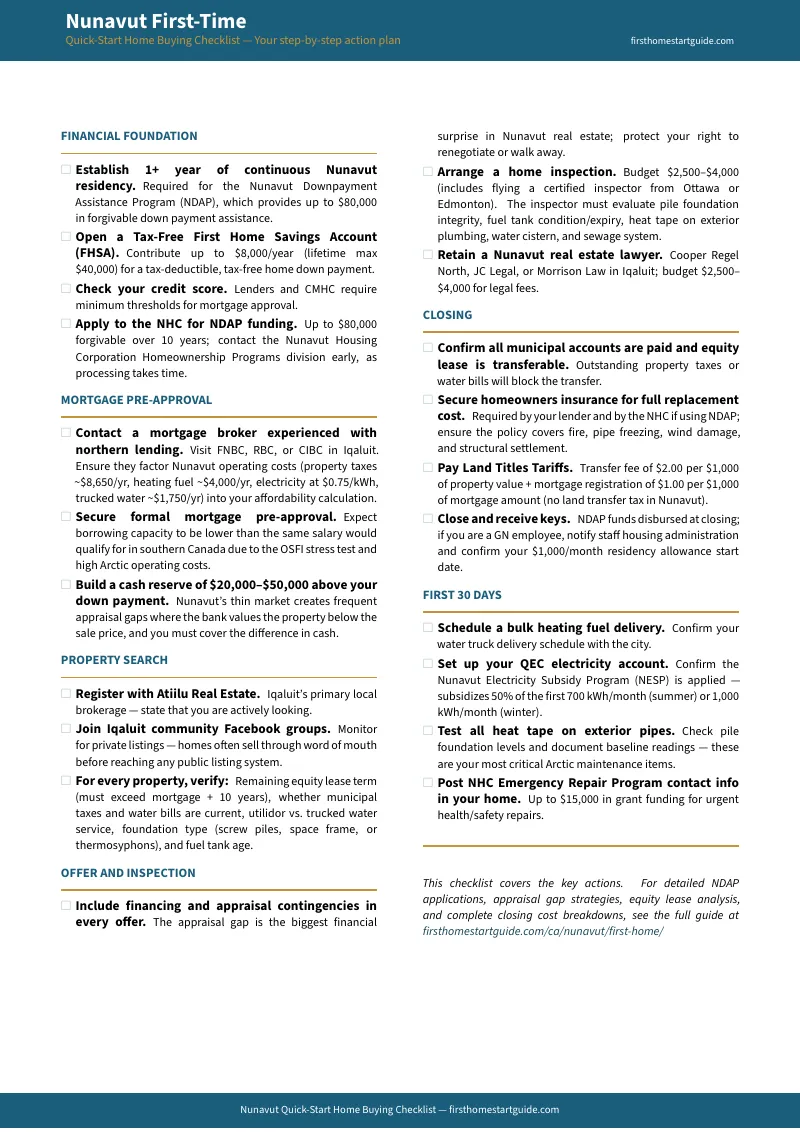

Download the free Nunavut Quick-Start Home Buying Checklist to see the 21-item action plan covering financial preparation, NDAP eligibility, mortgage pre-approval with Arctic costs factored in, property search protocols, and closing steps. When you are ready for the full navigation system — the complete 13-chapter guide with NHC program stacking, equity lease analysis, permafrost foundation guidance, and the Arctic operating cost budget — the complete toolkit is here.

You are buying in the most unique housing market in North America. Make sure you understand its rules before you sign.