You Moved to PEI for the Affordable Housing. Then a $345,000 Oil Spill Cleanup Bill Arrived Because Nobody Told You to Check the Tank Tag.

You found a three-bedroom home in Charlottetown listed at $385,000. Or a century farmhouse on five acres outside Montague with a view of the Brudenell River. Or a starter home in Summerside where property taxes haven't increased since 1995 because the city owns its own electric utility. Your mortgage broker ran the stress test and you qualify. Your agent says the market is moving. You're ready to write an offer.

Then the details start surfacing. Your lawyer informs you that as an out-of-province buyer, you're legally classified as a non-resident under the Lands Protection Act — and that 25-acre hobby farm you fell in love with exceeds the 5-acre cap by a factor of five. You need IRAC and Executive Council approval just to complete the purchase, and meanwhile the province charges you an extra 20 cents per $100 of assessed value in non-resident property tax. The first-time buyer transfer tax exemption exists, but you can't claim it at closing because you haven't lived in PEI for six months yet — so you're paying the full 1% upfront, $4,000 in cash you didn't budget for, and filing for a refund after 183 consecutive days of occupancy with a notarized Declaration form. Your title search comes back from the lawyer's office, and instead of a clean certificate of title guaranteed by the province, you receive a 40-year historical chain-of-deeds trace through handwritten metes-and-bounds descriptions — because PEI doesn't use the Land Titles system. If a fraudulent transfer or unregistered easement from 1987 surfaces, you have no government guarantee.

And the oil tank. You moved in, called your insurance company, and learned that the steel tank in the basement was manufactured in 2008, has no government identification tag on the vent pipe, and is classified as an uninsurable liability. Your insurer demands immediate replacement with a fiberglass tank — $4,000 to $6,000 — or they'll cancel your homeowner's policy entirely. You look up what happens when an uninsured oil tank leaks: a family in PEI suffered a 1,100-litre spill into their clay basement. The provincial government organized remediation. The bill was $345,000, secured by a lien on their home.

Here's what makes PEI different from every other Canadian province, and why mainland assumptions will cost you: PEI enforces the Lands Protection Act — the most aggressive provincial land restriction in Canada — capping non-residents at 5 acres and 165 feet of shore frontage. PEI runs an antiquated Registry of Deeds system where title is established by a 40-year historical trace, not a government guarantee. PEI's Real Property Transfer Tax exemption for first-time buyers requires six months of prior provincial residency or two years of PEI tax filing — interprovincial migrants pay the full 1% upfront and wait for a refund. PEI's Down Payment Assistance Program caps eligible purchases at $350,000, but the provincial benchmark price is now $378,900 — meaning most Charlottetown properties exceed the program threshold. PEI homes run on heating oil with strict environmental regulations, and an untagged or expired tank creates an immediate insurance crisis. PEI relies entirely on groundwater, and agricultural nitrate contamination and PFAS "forever chemicals" make well water testing a non-negotiable condition of purchase. And PEI's rural septic systems are categorized by soil percolation — a Category 3 lot means $15,000 to $25,000 for a raised mound system that nobody mentioned during showings. Getting PEI right means navigating all of it — the legislation, the infrastructure, and the environmental risk — in a single framework.

The Prince Edward Island First-Time Home Buyer Guide is an Island Buyer Protection System — not a generic Canadian homeownership overview, but a structured decision framework that maps PEI's unique legislation, environmental hazards, rural infrastructure requirements, and financial program stacking strategy into a system you work through before you sign anything. It replaces months of cross-referencing IRAC application forms, provincial environmental regulations, CMHC stress test calculators, CRA FHSA rules, and conflicting advice from r/PEI and r/PersonalFinanceCanada with a single reference that tells you exactly what restrictions apply, exactly what inspections are non-negotiable, and exactly where first-time buyers lose money in PEI.

What's Inside the Island Buyer Protection System

An 18-chapter guide and a printable step-by-step checklist — covering every stage from building your down payment through your first year as a homeowner, built specifically for the provincial laws, environmental hazards, and rural infrastructure that make PEI unlike any other province in Canada:

The Lands Protection Act — What Non-Residents Cannot Buy

Every other province lets you buy any property you can afford. PEI does not. If you haven't resided on the Island for 183 days or more per year, you're legally classified as a non-resident — and without IRAC and Executive Council approval, you cannot purchase more than 5 acres or 165 feet of shore frontage. The guide explains the exact residency definition, the application process and fees, the penalties for non-compliance, the additional 20-cent-per-$100 non-resident property tax, and the timeline for establishing residency so you can purchase freely. If you're a remote worker moving from Ontario or a cross-border buyer who becomes tax-resident in the United States, this chapter prevents your purchase from being halted by your own lawyer.

The Real Property Transfer Tax — Why You Pay 1% Upfront and How to Get It Back

PEI charges 1% of the greater of the purchase price or assessed value on every property transfer. First-time buyers can claim an exemption — but only if they've lived in PEI continuously for six months before closing, or filed PEI income taxes for two of the past six years. Interprovincial migrants buying and moving simultaneously do not qualify at closing. The guide walks through the exact upfront cost at multiple price points, the 183-day occupancy requirement for the refund, the notarized Declaration and formal Request for Refund forms, and the math that tells you how much extra liquid cash to hold at closing. On a $400,000 home, that's $4,000 in additional funds your mortgage broker never mentioned.

The Registry System — Why Your Title Has No Government Guarantee

Ontario, BC, and New Brunswick use Land Titles systems where the government guarantees your ownership. PEI still runs a Registry of Deeds system governed by the Investigation of Title Act. Your lawyer must trace the title back 40 years through a chain of conveyances described in written metes-and-bounds — not mathematically guaranteed survey coordinates. Hidden defects, unregistered easements, unpaid municipal taxes, and fraudulent transfers from decades past can surface and jeopardize your ownership. The guide explains why title insurance is a non-negotiable safeguard in PEI, what it covers (survey errors, forced removal of structures, historical fraud), and how a one-time premium protects you for as long as you own the property.

Oil Tank Hazards — The $345,000 Mistake You Can Spot in 30 Seconds

PEI homes heat with fuel oil at rates that would seem archaic in western Canada, and the province enforces strict Environmental Protection Act regulations on every tank. All tanks must be tagged with a government identification number, pitched at a specific slope, and installed by a licensed technician. Steel tanks are being phased out — replacements must be non-metallic fiberglass. Standard home insurance rarely covers oil spills automatically. The guide provides a step-by-step tank inspection protocol you can perform during any property viewing: check the data plate for manufacture date and material, verify the government tag on the vent pipe, assess age limits by material type (steel: 15 years, fiberglass: 20+ years), and understand the insurance questionnaire your insurer will require before issuing a policy.

Well Water Testing — Nitrates, PFAS, and the Tests You Must Demand

PEI relies entirely on groundwater. The province's intensive potato farming industry has created chronic nitrate contamination in rural aquifers. A Hazelbrook family recently found PFAS "forever chemicals" in their well at twenty times Health Canada's threshold. Urban buyers assume potable water is a guaranteed utility. In rural PEI, you are solely responsible for testing, treating, and maintaining your private well. The guide specifies exactly which tests to demand (bacterial: total coliform and E. coli; chemical: nitrates, ammonia, chloride, alkalinity), the cost (~$135 plus HST through PEI Analytical Laboratories), the testing frequency recommended by the province, and how to make a satisfactory well water test a binding condition in your purchase agreement.

Septic System Economics — Why a $250,000 Property Can Carry a $25,000 Hidden Cost

Rural PEI properties use on-site septic systems, and the system's cost is dictated by a soil percolation test that categorizes the lot into Category 1, 2, or 3. A Category 1 system costs $5,000 to $12,000. A Category 3 designation — poor soil drainage — requires a raised mound system costing $15,000 to $25,000. PEI does not universally mandate a septic inspection before property transfer. The guide explains how to request the percolation category, demand a pump-out and inspection by a certified professional before removing conditions, evaluate the age and maintenance history of the existing system, and budget for the replacement cost if the drain field is failing.

Coastal Erosion and Buffer Zones — What You Cannot Build on Your Own Land

Properties along PEI's red sandstone coastline face accelerating erosion from climate change and storm surges. Provincial legislation prohibits development, tree cutting, or heavy equipment operation within 15.2 metres (50 feet) of any coastline or body of water. If you buy a coastal property intending to build an extension, a deck, or a stairway to the beach, and that footprint falls within the buffer zone, you are legally prohibited. The guide maps the setback regulations, secondary restrictions on structures without foundations, and the due diligence required before purchasing any waterfront lot.

Financial Program Stacking — Every Dollar Available to PEI Buyers

The FHSA ($8,000/year, $40,000 lifetime, tax-deductible in, tax-free out), the HBP ($60,000 per person, 90-day seasoning, 15-year repayment), the Home Buyers' Tax Credit ($10,000 credit), the provincial DPAP (up to 5% of purchase price, max $17,500, interest-free for 10 years) — a couple can assemble up to $200,000 in tax-advantaged down payment capital plus $17,500 in provincial assistance. But the DPAP caps at $350,000 purchase price and $110,000 household income, which now excludes most Charlottetown properties. The guide maps the optimal contribution sequence, the program interactions, and the inventory strategies for finding DPAP-eligible homes in a market where the benchmark exceeds the cap.

Seasonal Worker Mortgage Qualification

If you work in tourism, fishing, or agriculture, standard paystubs will not get you a mortgage. Lenders reject standard Employment Insurance as qualifying income. But cyclical seasonal workers who document a strict two-year pattern of employment followed by EI benefits can qualify — and PEI seasonal workers may receive up to 5 additional weeks of regular EI benefits. The guide details the exact documentation required, how to present your income history to risk-averse underwriters, and the lenders (including PEI credit unions) most experienced with seasonal income patterns.

Who This Guide Is For

This guide is for first-time home buyers in Prince Edward Island who:

- Are relocating from Ontario, BC, or Nova Scotia and don't realize that PEI's Lands Protection Act restricts non-residents to 5 acres and 165 feet of shore frontage — and that the transfer tax exemption requires six months of prior residency they don't have yet

- Are local PEI residents earning around the Charlottetown average of $46,160 and need to stack every available program — FHSA, HBP, HBTC, and DPAP — while navigating a $350,000 program cap in a market where the benchmark is $378,900

- Are newcomers arriving through the Atlantic Immigration Program or Provincial Nominee Program and need to understand how residency status affects down payment requirements, mortgage insurance eligibility, and non-resident property tax assessments

- Are seasonal workers in tourism, fishing, or agriculture who need the specific documentation strategy that converts cyclical EI benefits into mortgage-qualifying income

- Are buying a rural property and need due diligence protocols for oil tanks, well water contamination, septic percolation categories, and coastal erosion buffer zones — hazards that most Canadian home buyers have never encountered

Why Not Free Tools and Government Websites?

Free information on PEI home buying exists across dozens of sources. Here's what it actually delivers:

- CMHC and federal government websites explain the FHSA and HBP as separate programs in a national context. They don't cover the DPAP's $350,000 price cap, the Lands Protection Act residency requirements, or any PEI-specific legislation. You get program descriptions without the provincial reality that determines whether you actually qualify.

- PEI government portals publish accurate information on the DPAP, the transfer tax, environmental tank regulations, and well water testing. But the information is siloed across the Department of Finance, the Department of Environment, IRAC, and multiple other agencies — written in dense bureaucratic language with no chronological narrative. Finding the transfer tax refund process requires visiting one site; understanding the Lands Protection Act requires visiting another; learning about oil tank regulations requires a third. There is no single journey from "I want to buy" to "I've closed."

- Reddit threads on r/PEI and r/PersonalFinanceCanada are where real buyers share real experiences — oil tank horror stories, bidding war frustrations, well water anxiety, and Lands Protection Act confusion. The information is unfiltered, frequently outdated, and mixed with advice that predates the enhanced $60,000 HBP, the current benchmark price, and the latest DPAP thresholds.

- Local brokerage and law firm websites provide market summaries and rudimentary legal overviews. They systematically avoid publishing deep-dive explanations of severe liabilities — the 40-year title trace, oil tank insurance denials, septic cost surprises — likely because their business model depends on you hiring them, not educating yourself.

This guide fills the PEI-specific gap — the space between knowing PEI is affordable and knowing how to buy here without triggering a Lands Protection Act violation, inheriting an uninsurable oil tank, contaminating your family's drinking water, or paying $25,000 for a septic system that should have been the seller's problem. It's the analysis that would take a real estate lawyer, a mortgage broker, an environmental consultant, and a septic contractor to assemble — structured as a reference you own permanently.

— Less Than One Hour of Your PEI Real Estate Lawyer's Time

A single oil tank leak on an uninsured property costs $50,000 to $345,000 in remediation. A Category 3 septic replacement runs $15,000 to $25,000. The Real Property Transfer Tax on a $400,000 home is $4,000 that interprovincial buyers must pay upfront. A missed FHSA contribution year is $8,000 in tax-deductible room you can never reclaim. An undetected Lands Protection Act violation can halt your closing entirely.

This guide doesn't replace your lawyer or your mortgage broker. But it gives you the legislative navigation, the environmental due diligence protocols, the financial program stacking strategy, and the rural infrastructure framework that ensure you understand every restriction, budget for every cost, and catch every hazard before you sign — instead of discovering them at the lawyer's office, on your first insurance call, or when the well water test comes back positive for nitrates.

If it catches a single oil tank red flag, prevents a single Lands Protection Act surprise, captures a single tax exemption you would have missed, or saves you from a single $25,000 septic replacement, it pays for itself before you finish reading it.

30-day money-back guarantee. If the guide doesn't sharpen your buying strategy and protect your investment in PEI's market, you pay nothing.

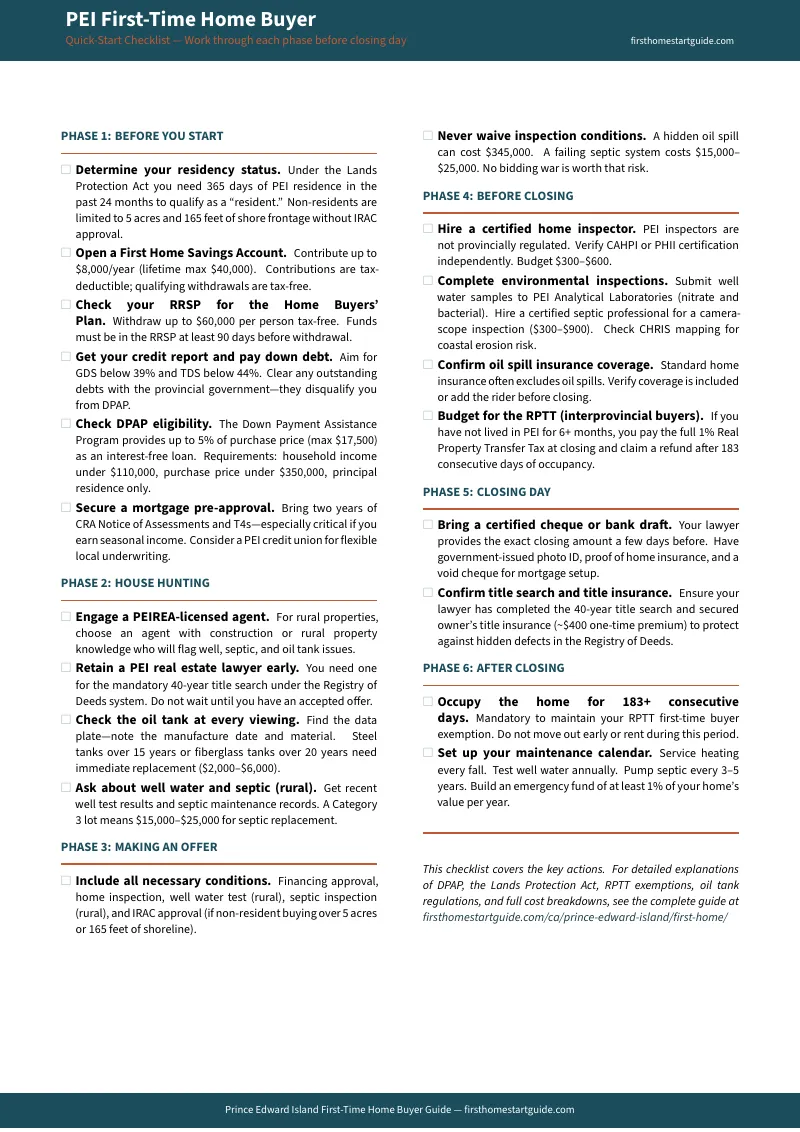

Your download includes 5 PDFs: the full 18-chapter guide covering every PEI-specific law, hazard, and financial program, a quick-start checklist with 20 action items organized across six phases, a fillable Closing Cost Worksheet with a worked Charlottetown example, a Due Diligence Checklist to print and bring to every property viewing (oil tank, well water, septic, coastal erosion, and Lands Protection Act checks), and a Transfer Tax Reference Card with the exemption pathways and refund process.

Download the free Prince Edward Island Quick-Start Home Buying Checklist to see the step-by-step action plan covering every phase of buying your first PEI home. When you're ready for the full legislative navigation, environmental due diligence protocols, and financial program stacking strategy, the complete guide is here.

PEI has the most affordable home prices in Atlantic Canada. This guide makes sure you keep that advantage — and don't lose it to legislation, infrastructure, or environmental liability you didn't know existed.