The Coastal Affordability Play Falls Apart When You Hit the Land Cap, the Title System That Doesn't Guarantee Ownership, and the Rent Control That Never Resets

You found a PEI waterfront cottage listed at $380,000 — a price that wouldn't buy a parking spot in Vancouver. Or a Charlottetown duplex at $375,000 with two units renting at $1,900 each in a market with 1.7% vacancy. You ran the numbers against your home province and the yield looked extraordinary. Then you planned to list the cottage on Airbnb during peak summer season at $3,500 per week and hold the duplex as a stable long-term rental, resetting rents to market rate whenever a tenant moves out.

Then Province-specific reality arrived. Your waterfront cottage has 170 feet of shore frontage. Under the Lands Protection Act, non-residents cannot acquire property with more than 165 feet of shore frontage without explicit government approval from the Island Regulatory and Appeals Commission. The application fee is the greater of $550 or 1% of the purchase price. The property must be marketed to local Islanders for 90 days before your application will even be considered. Approval is not guaranteed — Canadian citizens have been denied. And if approved, you typically cannot subdivide the land for ten years.

Your Charlottetown Airbnb plan is dead on arrival. The City of Charlottetown requires short-term rental operators to use their principal residence — you must live there year-round. Operating without a permit carries fines of $250 to $1,000 per day. And the federal government now denies all income tax deductions for non-compliant short-term rentals — meaning you pay tax on gross revenue, not net profit. On $60,000 in summer rental income with $45,000 in carrying costs, the difference is $27,000 in tax instead of $6,750.

Your duplex rent-reset strategy fails because PEI's rent control is unit-bound. When a tenant moves out, the rent stays. You cannot raise it for the next tenant. The previous tenant's exact rent must be disclosed in the new lease. The 2026 maximum annual increase is 2.0%, and even after a formal hearing where you expose your entire financial ledger to government scrutiny, the absolute ceiling is 5.0% total. In 2023, the province froze increases at 0% despite severe inflation — demonstrating this cap is a political instrument that can be tightened at any time.

Here's what no single resource explains: Prince Edward Island layers the strictest non-resident land ownership law in Canada (a five-acre cap and 165-foot shore frontage limit enforced by a Commission that can deny purchases outright) against an antiquated Registry of Deeds system where the province does not guarantee your title (your lawyer must manually trace 40 years of ownership history), a non-resident property tax premium that costs you 70% more than a local investor holding the identical property, unit-bound rent control that follows the apartment forever and cannot be reset between tenants, municipal short-term rental bylaws that ban investor-owned Airbnbs in the capital, and coastal erosion on soft red sandstone cliffs that averages 30 centimetres per year and can claim 12 metres in a single storm. Each of these has cost real investors tens of thousands because the information was scattered across IRAC bulletins, the PEI Rental Office, municipal planning documents, and r/PEI threads — but nobody had assembled it into a single due diligence system calibrated to Prince Edward Island.

The Prince Edward Island Investment Property Guide is a PEI Investor Due Diligence System — not a generic Canadian real estate overview, but a structured regulatory navigation framework that maps every PEI-specific land restriction, title risk, tax penalty, rent control mechanism, and environmental hazard into a process you work through before you commit capital. It replaces months of cross-referencing IRAC applications, Residential Tenancy Act forms, CMHC vacancy reports, coastal erosion maps, and forum posts with a single reference that tells you exactly what to verify, exactly where the numbers break, and exactly which strategies work on the Island versus which ones don't.

What's Inside the PEI Investor Due Diligence System

A comprehensive guide, a standalone due diligence checklist, and three printable reference tools — covering every stage from residency assessment through post-purchase operations, built specifically for the regulatory mechanics and unique risks that make Prince Edward Island unlike any other Canadian province:

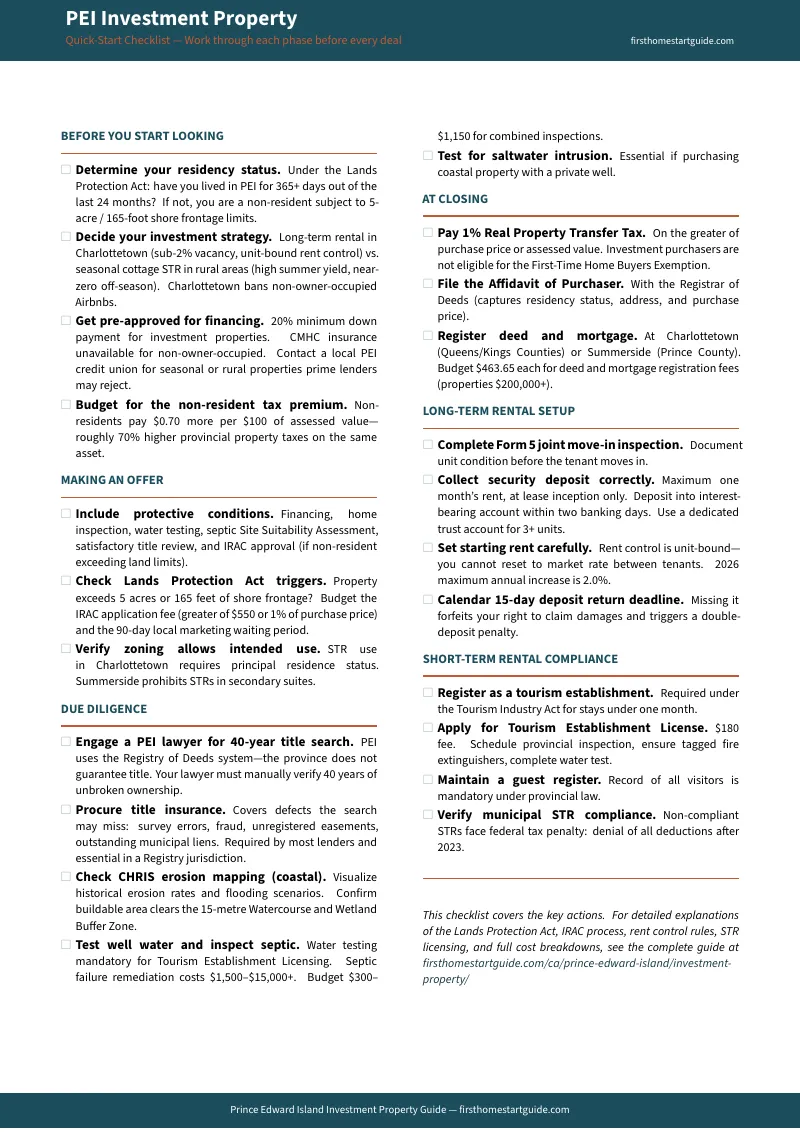

Lands Protection Act Navigation

The most restrictive land ownership law in Canada, and the first thing that stops mainland deals. The guide covers the precise residency definition (365 days in the preceding 24 months — not Canadian citizenship, which is irrelevant), the non-resident caps (5 acres aggregate, 165 feet of shore frontage measured along the general trend of the shoreline), the IRAC application process (fee formula, 90-day local marketing requirement, what the Commission evaluates, post-approval conditions including the 10-year subdivision prohibition that runs with the land), and why holding companies, family trusts, and nominee arrangements are ineffective — the Act's attribution rules calculate aggregate holdings through direct and indirect control, including shares held by anyone with more than 5% of voting interest.

Registry of Deeds Risk Assessment

Most Canadian investors come from Torrens jurisdictions where the province guarantees your title. PEI does not. The Registry of Deeds is a passive filing office — the government records documents but certifies nothing about ownership, boundaries, or encumbrances. Your lawyer must conduct a 40-year historical title search tracing every deed, mortgage, judgment, easement, and lien to verify unbroken ownership. The guide explains what this search covers, what it can miss (historical fraud, survey errors on shifting coastal boundaries, unregistered easements), why title insurance is a non-negotiable cost in a Registry jurisdiction, and how to budget for legal counsel that specializes in this system. Two Registry offices serve the province: Charlottetown (Queens and Kings Counties) and Summerside (Prince County).

Non-Resident Taxation Analysis

PEI financially penalizes non-resident ownership through a two-tier property tax system. Residents receive a Provincial Tax Credit of $0.70 per $100 of assessed value, reducing their effective rate from $1.70 to $1.00. Non-residents pay the full $1.70 — effectively 70% higher annual property taxes on the same asset. On a property assessed at $350,000, the annual premium is $2,450. The guide runs the math at multiple assessment values, factors this premium into cap rate and NOI projections, covers the 1% Real Property Transfer Tax (which investment purchasers cannot avoid since the First-Time Home Buyers Exemption requires 183 days of owner-occupancy), and addresses the federal Underused Housing Tax filing requirements for corporations and trusts.

Short-Term Rental Regulatory Map

The most fragmented STR landscape in Atlantic Canada, with rules that vary by municipality. Charlottetown has effectively banned investor-owned short-term rentals through a principal residence requirement — you must live at the property year-round, provide government ID matching the address, carry $2 million in commercial liability insurance, accept only one booking at a time, and remit a 3% Tourism Accommodation Levy. Summerside allows STRs in commercial zones but prohibits them in secondary suites. Stratford and Cornwall are actively developing new bylaws. The guide covers the provincial Tourism Establishment License process ($180, physical inspection, mandatory well water testing, guest register), each municipality's rules, and the federal CRA tax penalty that denies all deductions for non-compliant STRs — turning a net-loss cottage into a gross-revenue tax liability.

Unit-Bound Rent Control Mechanics

This is the constraint that most fundamentally changes the math for long-term rental investors in PEI. Rent control follows the physical unit, not the tenancy. When a tenant leaves, you cannot raise the rent for the next one. You must disclose the previous tenant's exact rent in the new lease. The 2026 maximum annual increase is 2.0%, once per 12-month period, with three months' written notice using mandatory Form 8. Applying for an above-guideline increase requires Form 9 and Form 10 (full income and expense disclosure), a hearing before the Director, and faces a hard cap of 3% additional — making the absolute maximum possible rent growth 5.0% in any year. The guide covers the historical pattern of legislated caps (including the 2023 freeze at 0%), the anti-renoviction provisions (six months' notice, one month's rent compensation, tenant right of first refusal to return), the 15-day security deposit return deadline (miss it and you owe double), and why the traditional value-add renovation strategy is effectively neutralized in PEI.

Charlottetown Rental Market Intelligence

The fundamental demand thesis: Charlottetown's vacancy rate sits at 1.7%, driven by international immigration, interprovincial migration, UPEI enrollment, and healthcare sector employment. But CMHC's published averages ($936 one-bedroom median, $1,200 two-bedroom median) heavily weight subsidized and rent-controlled legacy leases. Actual market asking rents for vacant turnover units run $1,289+ for one-bedrooms and $1,900+ for two-bedrooms. The guide explains the gap, covers the UPEI student housing market ($930/month average student spend, 56% roommate rate, per-room rental model for multi-bedroom houses near campus), and why setting your initial rent correctly is the single most consequential decision in PEI — unit-bound control means you cannot catch up later.

Seasonal Cottage Financial Reality Check

Peak summer rates are genuine: $2,500 to $4,200 per week during July and August at 90-100% occupancy. But the guide stress-tests these numbers against twelve months of carrying costs — mortgage interest, non-resident property taxes, insurance for seasonal coastal properties, maintenance and winterization, utilities, licensing fees — that run year-round while occupancy drops to near zero outside the eight-week peak. Many cottages operate at a net cash-flow loss annually. The investment thesis relies on capital appreciation and personal use value, not rental income. The guide also covers the uninsurable environmental risks: coastal erosion averaging 30 cm per year on soft red sandstone (with major storms stripping metres in hours), the 15-metre Watercourse and Wetland Buffer Zone ($50,000 fines for violations), saltwater intrusion rendering private wells unusable, and septic system failure costs ranging from $1,500 for minor repairs to $15,000+ for full drain field restoration.

Financing Pathways

Investment properties require 20% minimum down (no CMHC insurance for non-owner-occupied), OSFI stress test qualification, and honest treatment of rental income in debt-service ratios. For long-term rentals, lenders count 50-80% of appraised market rent. For seasonal cottages, the picture changes dramatically: prime lenders classify properties as Type A (winterized, permanent foundation, year-round access) or Type B (seasonal, uninsulated, limited access). Type B properties face frequent rejection from prime lenders, especially when projected Airbnb income lacks multiple years of verified T776 documentation. The guide covers local PEI credit unions — Provincial Credit Union and East Coast Credit Union — that use relationship-based underwriting models with genuine flexibility for seasonal and rural assets that Bay Street algorithms cannot price.

Tax Planning and the CCA Trap

PEI's 2026 personal income tax system adds a new top bracket: income over $200,000 taxed at 20.0% provincially, reaching approximately 53% combined with federal rates. Capital gains inclusion rates have increased to 66.67% for individuals above $250,000 annually and for all corporations. The guide covers Capital Cost Allowance claiming strategy (4% Class 1 for residential buildings) and the recapture trap on disposition — a decade of CCA claims can create a devastating tax bill in the year of sale. It also quantifies the federal STR non-compliance penalty with specific worked examples showing the difference between tax on net profit versus gross revenue.

Standalone Printable Tools

Three reference tools you can print independently — fill in during due diligence, bring to your lawyer, or pin above your desk as a landlord:

- Closing Cost Worksheet — estimate every dollar you need to close on a PEI investment property, from the 1% Real Property Transfer Tax through Registry fees, 40-year title search legal costs, title insurance, and IRAC application fees for non-residents exceeding the land limits

- Rent Control Quick Reference — unit-bound rent control rules, the 2026 allowable increase cap, Form 8/9/10 above-guideline hearing process, security deposit deadlines (15-day return window, double penalty for missing it), and eviction protocols including the six-month renovation notice and tenant right of return

- STR Compliance Checklist — provincial Tourism Establishment License steps, Charlottetown principal residence ban with all municipal requirements, Summerside zone-based rules, and the federal CRA non-compliance penalty with a worked tax calculation example

Who This Guide Is For

This guide is for real estate investors targeting Prince Edward Island who:

- Are mainland Canadians evaluating PEI's coastal affordability and need to understand the Lands Protection Act non-resident land cap, the IRAC application process, the Registry of Deeds title risk, and the non-resident property tax premium before deploying capital into a province whose regulatory framework is designed to protect Island land from exactly their investment thesis

- Are planning a waterfront cottage purchase for seasonal tourism income and need the honest financial stress test — peak summer rates against twelve months of carrying costs, coastal erosion risk assessment using the CHRIS mapping tool, well and septic due diligence requirements, and the financing reality for seasonal Type B properties that prime lenders routinely reject

- Are targeting Charlottetown long-term rentals and need to understand unit-bound rent control (rent follows the apartment forever, you cannot reset between tenants), why your initial rent is irreversible, the above-guideline increase hearing process with its 5% hard ceiling, and the six-month anti-renoviction eviction timeline that neutralizes value-add renovation strategies

- Are evaluating UPEI student housing near campus and need the per-room rental model economics, the eight-month academic lease cycle, the $930/month average student housing spend, and vacancy dynamics in a 1.7% market

- Planned an Airbnb strategy in Charlottetown and need to understand why it is functionally illegal for non-owner-occupiers, what the daily fines and federal tax penalties look like, and where on the Island investor-owned short-term rentals are still viable

- Need the IRAC application walkthrough — the 1% fee calculation, the 90-day local marketing waiting period, the post-approval conditions, and why corporate structures do not work around the attribution rules — before risking $6,000+ in non-refundable application fees

Why Not Free Resources and Forums?

Free information on PEI real estate investing exists. Here's what it actually delivers:

- IRAC and provincial government websites provide the raw legislation and application forms. They do not explain the practical investment implications of the 165-foot shore frontage measurement method (following the general trend of the shoreline, which catches irregular lots), the historical approval and denial patterns, or how post-approval conditions like the 10-year subdivision restriction affect your exit strategy and resale buyer pool. You get statutory text without strategic context.

- Local real estate agent "non-resident guides" summarize the 5-acre limit and the transfer tax. They are lead-generation tools, not investment analysis. They rarely cover unit-bound rent control mechanics, the Form 9 above-guideline hearing process, the federal STR non-compliance tax penalty, the non-resident property tax premium calculation, or coastal erosion risk assessment. They tell you PEI is beautiful and affordable; they do not tell you where the numbers break.

- Reddit threads (r/PersonalFinanceCanada, r/PEI) contain genuinely valuable experience reports — including Canadian citizens who were denied land purchases and landlords navigating the Rental Office. But advice mixes 2020 rent freeze rules with 2024 rate adjustments, pre-Charlottetown-STR-ban operating tips, and financing guidance from mainland provinces that does not translate to PEI's Registry system or seasonal cottage underwriting. Sorting current from outdated requires cross-referencing every claim against the latest legislation.

- National Canadian investing courses teach cap rates, DSCR ratios, and value-add strategies calibrated to provinces with Torrens title systems, vacancy decontrol rent resets, and 1% land transfer taxes. Applying these frameworks to a province where the government doesn't guarantee your title, rent control never resets, the land transfer tax exemption requires 183 days of occupancy, and the Lands Protection Act can block your purchase entirely is how investors model returns that never materialize.

This guide fills the PEI-specific gap — the space between knowing how to analyze a rental property in general and knowing how to underwrite one in a province where non-resident land caps can block acquisitions, the title system provides no government guarantee, rent control is permanently attached to the physical unit, the capital city bans investor-owned Airbnbs, the coastline is eroding under your investment, and non-resident property taxes run 70% higher than what locals pay. It is the analysis that would take a PEI real estate lawyer, a Registry title specialist, a provincial tax accountant, and a CMHC analyst to assemble — structured as a reference you own permanently.

— Less Than One Hour of the Legal Counsel You'll Need Anyway

A PEI real estate lawyer charges $2,000 or more for the 40-year title search alone. An IRAC application fee on a $400,000 property costs $4,000. The non-resident property tax premium runs $2,450 per year, every year. A single above-guideline rent increase hearing requires hours of financial documentation preparation. A non-compliant Airbnb operation costs $250 to $1,000 per day in municipal fines plus denial of all federal tax deductions.

This guide costs less than one hour of the professional fees you will pay during closing. It covers the regulatory framework, financial traps, and operational requirements that determine whether your PEI investment generates stable returns or becomes an expensive lesson in provincial exceptionalism.

30-day money-back guarantee. If the guide does not cover a PEI-specific regulatory requirement, tax mechanism, or investment risk that materially affects your acquisition decision, email for a full refund.