You Can Afford a Home in England. The Process Is Designed to Make You Think You Can't.

You've done the maths. Salary times 4.5, minus deposit, and you can afford a two-bed flat in a reasonable commuter town. So you start looking. Within a week you've learned that the stamp duty nil-rate threshold dropped to £300,000 in April 2025, adding thousands in cash you didn't budget for. Your Lifetime ISA — the one you've been patiently filling for three years — has a £450,000 property cap, and if you exceed it by a single pound, you lose the entire government bonus plus 6.25% of your own savings. The flat you liked is leasehold with ground rent that doubles every 15 years, and two mortgage brokers have already told you that makes it unmortgageable.

You search online for help. Own-your-home.gov.uk explains the First Homes Scheme in language that could put a conveyancer to sleep. MoneySavingExpert's 53-page guide covers mortgages brilliantly but barely touches leasehold risk or the exchange-completion gap where 30-35% of all English property deals collapse. Reddit's r/HousingUK is full of real stories, except the stamp duty advice from six months ago is now wrong because the thresholds changed. Estate agent guides tell you to "move quickly" — because they represent the seller and earn nothing unless you complete. And every bank guide conveniently steers you toward their own mortgage products.

Here's the core problem: England's home buying system runs on two stages — exchange and completion — and nothing is legally binding until you exchange contracts. That means you can spend £2,000 to £4,000 on solicitor fees, surveys, and searches, have the seller accept a higher offer the day before exchange, and lose everything. Gazumping is perfectly legal. So is pulling out for no reason at all. And there is no single resource that maps the financial traps, the legal risks, and the tactical decisions across the entire 8-to-16-week process in one place.

The England First-Time Buyer Guide is an England Buyer Decision System. Not a summary of government schemes or a checklist of steps. It's a structured decision framework that maps every financial trap, every legal risk point, and every tactical choice from mortgage-in-principle through key collection — so you make each decision with the full picture, not a patchwork of forum threads and conflicting professional advice.

What's Inside the England Buyer Decision System

The complete guide plus standalone printable worksheets — covering every stage from scheme selection through completion day, plus fillable tools you print, bring to mortgage appointments, and share with your solicitor:

Post-2025 Stamp Duty Decision Framework

Since April 2025, the first-time buyer nil-rate band dropped from £425,000 to £300,000, and the maximum eligible property price fell from £625,000 to £500,000. Buy a property for £500,000 and you pay £10,000 in stamp duty. Buy one for £501,000 and you lose all first-time buyer relief — paying £15,050 under standard rates instead. That's a £5,050 penalty for a £1,000 price difference. The guide maps every threshold, every cliff edge, and every negotiation scenario so you know exactly when to push the seller down and when to walk away. Including how stamp duty interacts with your deposit, your LISA, and your maximum borrowing capacity.

Lifetime ISA Trap Analysis

The LISA's £450,000 property cap creates a brutal penalty zone. If you've saved £32,000 and received £8,000 in government bonuses, your balance is £40,000. Buy a property for £455,000 and you pay a 25% penalty on the entire balance — losing all £8,000 in bonuses plus £2,000 of your own money. The guide covers exactly when to use your LISA, when to withdraw penalty-free, and the legitimate workarounds buyers use to stay under the cap — including the fixtures and fittings apportionment approach, its limits, and why most solicitors refuse to inflate chattel valuations because HMRC treats it as tax evasion.

Leasehold Risk Assessment Toolkit

Most affordable flats in England are leasehold. A starting ground rent of £500 that doubles every 10 years reaches £16,000 per year by year 50. If the ground rent exceeds 0.1% of the property's value, mainstream lenders refuse to touch it. If it exceeds £250 per year outside London, the lease can legally convert to an Assured Shorthold Tenancy — giving the freeholder the right to repossess for unpaid rent. The guide covers the exact mortgageability thresholds, how to read a lease for escalating ground rent clauses, service charge volatility, the EWS1 fire safety certificate trap, and the ex-council major works risk where bills of £30,000 to £100,000 arrive without warning because councils cannot legally build sinking funds.

Shared Ownership Reality Check

Shared Ownership is marketed as a stepping stone. In practice, you pay mortgage, rent, and service charges simultaneously — with rent indexed to inflation on an upward-only basis. Despite owning 25% of the property, you're responsible for 100% of all maintenance and repairs. Staircasing to full ownership is priced at current market value, not what you originally paid — meaning your salary must outpace property prices just to stay even. And selling requires a RICS valuation, an 8-week housing association priority period, and a restricted buyer pool that can leave properties unsold for years. The guide models the true cost of Shared Ownership over 5, 10, and 15 years so you can see whether it's a bridge to ownership or a financial trap.

Exchange-Completion Survival Strategy

England's two-stage system — where nothing is binding until exchange of contracts — means you can spend months and thousands of pounds on a purchase that collapses overnight. The guide maps the entire 8-to-16-week conveyancing timeline, identifies the five bottleneck points where delays typically cluster, explains how to manage your chain position, and covers the tactical decisions that reduce your exposure to gazumping, gazundering, and chain collapse. Including when to instruct your solicitor, when to commission surveys, how to sequence spending to minimise sunk-cost risk, and whether Home Buyers Protection Insurance is worth the premium.

Mortgage Capacity and Affordability Worksheets

Your maximum borrowing at 4.5x income. Your deposit requirement at different LTV ratios — and the interest rate premium you pay at 95% versus 90% versus 85% LTV. The stress test at 2% above your fixed rate. The 28% gross income affordability threshold. The guide calculates every number and shows you where single buyers on the median English salary of £39,300 hit the affordability wall — and what strategies exist to close the gap, from joint-income applications to regional targeting.

The Full Cost of Buying — Beyond the Deposit

Solicitor fees from £960 to £1,800. Conveyancing search bundle at £200 to £400. Home survey from £300 to £700. Mortgage valuation at £300 to £500. Land Registry fees from £100 to £295. Stamp duty calculated to the pound. The guide tallies every cost into a single worksheet so you know your true all-in figure before you make an offer — because discovering a £3,000 shortfall after your offer is accepted is how deals collapse and deposits evaporate.

Who This Guide Is For

This guide is for first-time buyers in England who:

- Are earning enough to service a mortgage but find that the 4.5x income cap, stamp duty cash requirements, and deposit LTV thresholds create a gap between what they can repay monthly and what the system will lend them

- Have been saving into a Lifetime ISA and now realise that properties in their target area are close to or above the £450,000 cap — and need to understand the penalty maths before making a decision they can't reverse

- Are looking at flats and need to know whether a leasehold property is a viable purchase or a long-term liability — before they spend £2,000 on conveyancing for a home that turns out to be unmortgageable

- Are considering Shared Ownership because it's the only way onto the ladder in their area, but want an honest financial model of what they'll actually pay over 10 years — not the housing association's marketing brochure

- Have read enough forum horror stories about gazumping, chain collapses, and exchange falling through to know that the English system has risks they need to manage, not just hope won't happen

- Want every transaction cost, every legal milestone, and every decision point mapped in one document — so they walk into solicitor meetings, mortgage appointments, and viewings knowing exactly what to expect at each stage

Why Not Free Resources?

Free information on buying your first home in England is everywhere. Here's what each source actually delivers:

- Own-your-home.gov.uk covers the First Homes Scheme and Shared Ownership with civil-service precision. What it doesn't cover: the leasehold risks buried in the lease you'll actually sign, the stamp duty cliff edges that can cost you £5,000 for a £1,000 price difference, or the exchange-completion gap where a third of deals die. The rules are there. The decisions those rules force you to make are not.

- MoneySavingExpert publishes a genuinely excellent 53-page first-time buyer guide — the best free resource available. It covers mortgages, fees, and the basic buying steps with trademark clarity. Where it stops: it doesn't model the long-term cost of Shared Ownership, doesn't explain how ground rent clauses render flats unmortgageable, and doesn't map the sunk-cost decision tree across the conveyancing timeline. It tells you what things cost. It doesn't tell you which costs to incur at which stage to minimise your risk of losing money on a deal that collapses.

- Reddit (r/HousingUK, r/UKPersonalFinance) is where real buyers share unfiltered experience — and where stamp duty advice from before April 2025 still circulates alongside current rules. You'll find someone who completed in six weeks and someone with an identical profile stuck at eight months. The signal is real. So is the noise. And no one cross-references their anecdote against the regulatory framework that determines whether it applies to your situation.

- Estate agent guides are written by professionals whose income depends on you completing a purchase. Their advice to "act quickly" and "show commitment early" serves the seller's timeline, not your financial protection. They will never tell you to slow down, question a lease, or walk away from a chain that looks unstable.

- Bank and lender guides (Halifax, Nationwide, Barclays) explain the home buying process clearly — through the lens of their own mortgage products, their own insurance add-ons, and their own conveyancing referral partnerships. The advice is accurate. The product recommendations are not independent.

This guide fills the decision gap — the space between knowing the steps exist and understanding which decisions to make at each step, in which order, to protect your money and maximise your position. It's the analysis an independent advisor with no products to sell would give you, structured as a permanent reference you own.

— Less Than One Set of Conveyancing Searches

A single conveyancing search bundle runs £200 to £400. Your solicitor's legal fees start at £960. A home survey costs £300 to £700. Stamp duty on a £350,000 property is £2,500 in cash you cannot add to your mortgage.

This guide doesn't replace your solicitor or your mortgage broker. But it gives you the stamp duty calculations, LISA penalty analysis, leasehold risk assessment, affordability worksheets, and transaction strategy that ensure you walk into every appointment, every viewing, and every negotiation knowing exactly where you stand — instead of discovering expensive traps in real time.

If it prevents a single stamp duty cliff-edge mistake, catches a single unmortgageable lease clause, or stops you spending £3,000 on a deal that was always going to collapse, it pays for itself before you've finished reading it.

30-day money-back guarantee. If the guide doesn't make your home buying process clearer and your financial position stronger, you pay nothing.

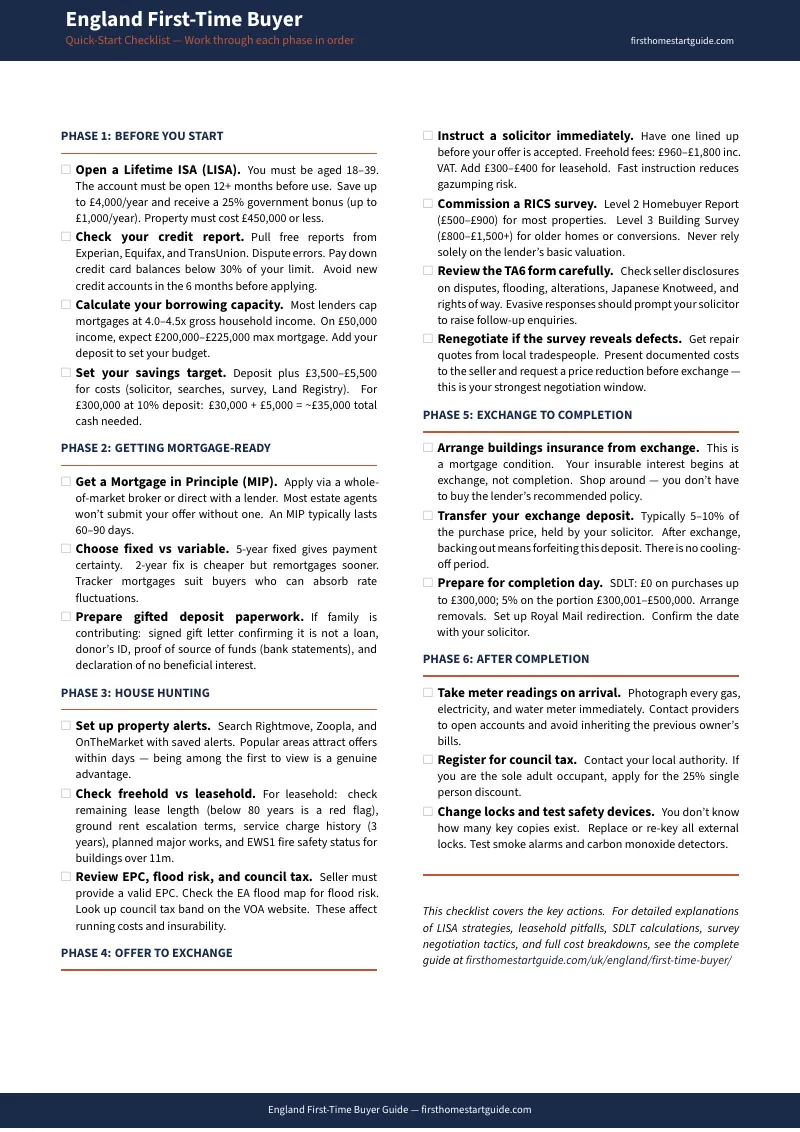

Download the free Quick-Start Checklist to see the step-by-step action plan covering stamp duty calculations, LISA eligibility, leasehold red flags, and the conveyancing timeline. When you're ready for the full decision system — complete with affordability worksheets, Shared Ownership cost models, and the exchange-completion survival strategy — the complete guide is here.

You've saved the deposit. Now stop the system from taking it.