You Modelled 6.5% Gross Yield on a Two-Bed in Manchester. But You Didn't Know That Section 24 Pushes Your Effective Tax Rate Past 50%, That the 5% SDLT Surcharge Costs You £15,000 on a £250,000 Property Before You Collect a Single Month's Rent, That the Renters' Rights Act Means You Can Never Issue a No-Fault Eviction Again, or That Every Property You Own Must Hit EPC C by 2030 or Face £30,000 in Fines.

You found a two-bedroom terraced house in Salford projecting 6.8% gross yield. Or a three-bed semi in Birmingham where the agent's listing promises 7.2% returns. Or a student HMO in Leeds where the per-room maths look solid at a 9% cap rate. You talked to your mortgage broker. You lined up the 25% deposit. You ran the numbers on a spreadsheet your colleague forwarded. You're ready to make an offer.

Then England happens. Your accountant runs the Section 24 calculation and reveals that your £15,000 gross rental profit generates £5,000 in tax -- because HMRC taxes the full rental income at 40% and hands you back a 20% credit on the mortgage interest only, producing an effective tax rate of 50% on your actual commercial profit. You close on the Manchester terrace and discover the 5% SDLT surcharge cost you £15,000 at completion -- capital that earns no return and took years to save. You get a difficult tenant who stops paying rent, and the Renters' Rights Act means Section 21 no longer exists -- you cannot evict without proving specific grounds under Section 8, a process that takes months through the courts while you service the mortgage from your salary. And when you try to raise the rent to cover your rising costs, you discover that increases are now limited to once per year via the statutory Section 13 process, where tenants can challenge you at a First-tier Tribunal for free.

Here is what no single free resource explains: England layers Section 24's 50%+ effective tax rate for higher-rate taxpayers on top of a 5% SDLT surcharge that drains £8,000 to £40,000 in capital at acquisition, on top of a Renters' Rights Act that abolished Section 21 no-fault evictions and restricts rent increases to once per year via tribunal-challengeable Section 13 notices, on top of a mandatory EPC C rating by October 2030 with a £10,000 cost cap per property and £30,000 fines for non-compliance, on top of ICR stress tests requiring 125% to 145% rental coverage at a 5.5% to 6% hypothetical rate that reject mortgages on half the properties in Southern England, on top of Capital Gains Tax at 18% to 24% with a 60-day reporting deadline and a £3,000 annual exemption that barely covers inflation, on top of Right to Rent penalties of £10,000 per unauthorised occupant for a first breach. Each of these has cost real English landlords tens of thousands because the information existed -- scattered across HMRC guidance notes, legislation.gov.uk, the Property Hub forum, Reddit threads on r/uklandlords, r/HousingUK, and r/UKPersonalFinance, mortgage broker brochures, and £100-to-£300-per-hour accountant consultations -- but nobody had assembled it into a single investment framework calibrated to how England actually works in 2026.

The England Property Investment Guide is a Section 24 Survival Manual -- not a motivational overview of English property, but a structured reference that maps every England-specific tax mechanism, regulatory constraint, ownership structure, financing stress test, and regional market into a process you work through before your deposit is committed. It replaces months of cross-referencing HMRC technical guidance, Renters' Rights Act provisions, PRA stress-test rules, and forum threads with a single guide that tells you exactly what the numbers should look like, exactly what to verify, and exactly where English property deals go wrong.

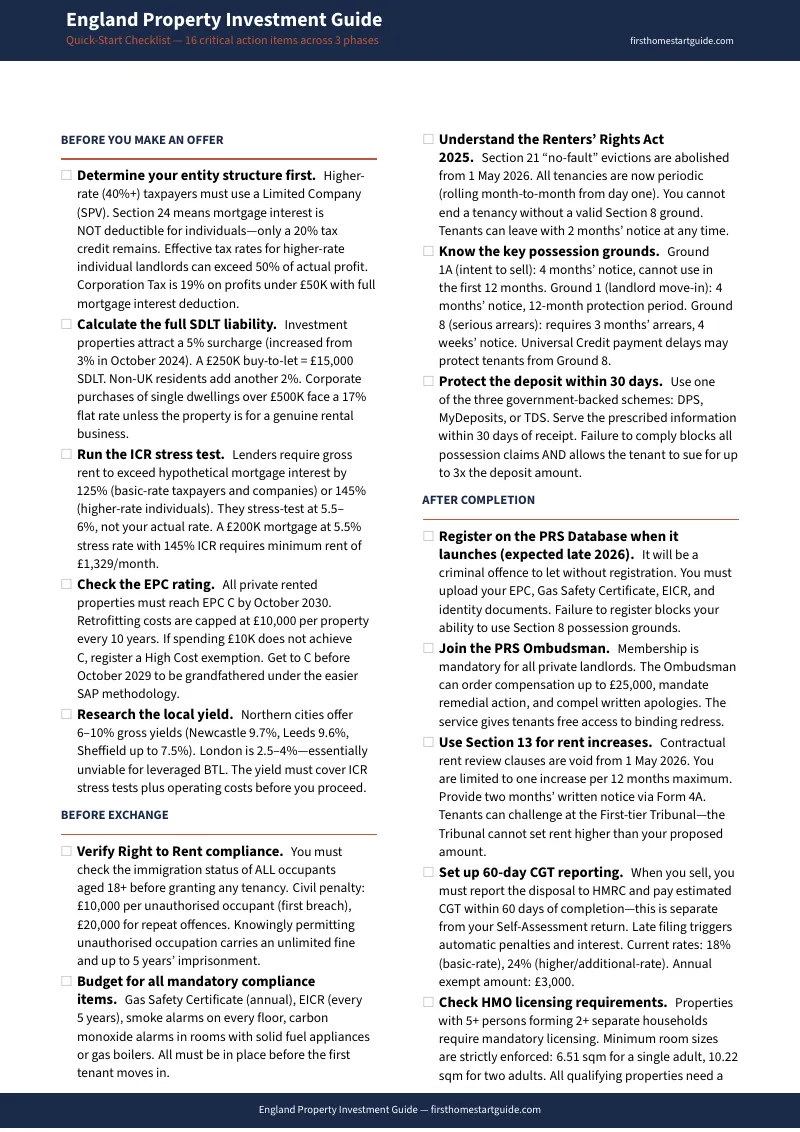

What's Inside the Section 24 Survival Manual

A comprehensive guide, a quick-start checklist, and 10 standalone worksheets and reference cards -- covering every stage from initial viability assessment through capital gains disposal, built specifically for the taxation, regulations, and market dynamics that make England one of the most hostile environments in the developed world for individual buy-to-let landlords:

The Section 24 Tax Stack -- Worked Examples at 40% and 45%

Section 24 of the Finance (No. 2) Act 2015 eliminated mortgage interest as a deductible expense for individual landlords. HMRC now taxes your full gross rental income at your marginal rate and gives you back a 20% basic-rate credit on the interest only. The guide breaks down exactly how this creates an effective tax rate of 50% for a 40% taxpayer earning £15,000 in gross rent with £5,000 in mortgage interest -- and how that rate climbs to 62.8% if interest costs rise to £8,000 while rent stays flat. It includes a worked example showing a higher-rate taxpayer on a £95,000 salary with £45,000 in portfolio rent, where HMRC's artificial income inflation pushes total taxable income past £100,000 and triggers the loss of the personal allowance -- creating a scenario where the tax owed on rental income exceeds the actual cash profit. For additional-rate taxpayers at 45%, the mismatch between the 45% charge and the 20% credit is even more severe. The guide also covers allowable deductions that still reduce the taxable quantum: letting agent fees, insurance, maintenance, ground rent, service charges, and the Replacement of Domestic Items Relief that replaced the old 10% Wear and Tear allowance -- including the strict like-for-like replacement rule that catches landlords who upgrade.

SDLT Surcharge Calculations at Four Price Points

Since October 2024, the additional property SDLT surcharge stands at 5% across all tranches. The guide provides fully worked calculations at four acquisition price points: £150,000 (typical Northern terrace, £8,000 total SDLT), £250,000 (Midlands semi-detached, £15,000), £350,000 (commuter belt house, £25,000), and £500,000 (London apartment, £40,000). It covers the non-resident 2% surcharge for overseas investors, the 17% flat rate that applies when a corporate entity purchases a single dwelling above £500,000, the statutory relief that exempts genuine buy-to-let businesses from the 17% penalty, and the multiple dwellings strategy -- purchasing six or more residential units in a single transaction to access commercial SDLT rates capped at 5%. Every calculation uses the current 2026 progressive slice system so you can model SDLT as a precise capital drag before you make an offer.

Full Incorporation Cost-Benefit Analysis

Approximately 80% of new buy-to-let purchases now go through limited companies because Corporation Tax at 19% (small profits rate under £50,000) allows full mortgage interest deductibility -- the exact advantage Section 24 removed from individuals. But transferring an existing personally-held portfolio into a company triggers a cascade of costs: CGT on the gain at market value (18% or 24%), SDLT payable by the acquiring company at the 5% surcharge rates, early repayment charges on existing personal mortgages, refinancing at higher corporate rates, dual-representation solicitor fees, and RICS valuation fees. The guide provides a complete cost model and payback period calculation so you can determine whether the Corporation Tax savings over five, ten, and fifteen years justify the upfront transfer costs -- or whether holding in your personal name and managing the Section 24 burden is the less expensive path for your specific portfolio size and leverage.

Section 162 Incorporation Relief -- When HMRC Says Yes and When They Don't

Section 162 of the Taxation of Chargeable Gains Act 1992 allows landlords to defer CGT by rolling the gain into the base cost of newly issued company shares. But HMRC contests this relief aggressively. The guide covers the core requirement: your portfolio must qualify as a genuine commercial property business, not a passive investment. The benchmark is 20+ hours per week of active management -- rent collection, tenant communication, maintenance coordination, compliance administration. The guide explains what HMRC looks for, what documentation strengthens a claim, and why passive investors with a single managed property will almost certainly fail the test. It also covers the critical limitation: even if CGT is deferred, SDLT is still payable by the acquiring company on the full market value unless complex partnership incorporation structures are used.

ICR Stress Tests and the Deposit Sensitivity That Kills Southern Deals

Lenders assess buy-to-let mortgages through the Interest Coverage Ratio, not your personal income. Basic-rate taxpayers and limited companies typically face a 125% ICR requirement; higher-rate taxpayers face 145% or higher. The stress rate is not your actual mortgage rate -- it is a hypothetical rate of 5.5% to 6% designed to ensure the investment survives future rate shocks. The guide works through the maths: a £200,000 mortgage at a 5.5% stress rate generates £11,000 in hypothetical annual interest. At a 145% ICR, the property must produce at least £15,950 in annual rent -- £1,329 per month -- just to qualify for the loan. This stress test structurally excludes Southern England properties yielding 3.5% to 4.5% unless the investor injects significantly larger cash deposits. The guide covers top slicing (where personal income bridges the ICR gap), portfolio landlord underwriting rules (four or more mortgaged properties triggers whole-portfolio assessment), and how a single low-yielding property can block lending across your entire book.

Regional Yield Analysis -- Manchester, Birmingham, Leeds, Sheffield, London

The guide provides data-driven profiles of the five primary English investment corridors. Manchester: average property price £256,644, average yield 5.61%, top yields up to 7.8% in the broader region, driven by the £2.5 billion Bee Network and the 15,000-home Victoria North regeneration scheme. Birmingham: yields of 5.44% on average, 6% to 9% in city-centre postcodes like B1 and B5 and student areas like Selly Oak, with HS2 Curzon Street and Digbeth regeneration underpinning demand. Leeds: top postcodes achieving 9.6% gross yields, student demand in Headingley at 6.5% to 8%, financial district apartments at 6% to 7.5%. Sheffield: average price £220,445 -- 24.5% below the national average -- with yields up to 7.5% in S3 city-centre postcodes. London: prime central at 2.5% to 4%, viable only in Outer East boroughs like Newham and Barking where new-build stock reaches 5% to 6.5%. The guide includes gross-to-net compression analysis showing how a headline 7% yield compresses to 3% to 4% after management fees, insurance, void allowance, EPC costs, and the Section 24 tax stack.

Renters' Rights Act 2025 -- What Changed on 1 May 2026

The guide covers the full operational impact of the Act's Phase 1 provisions. Section 21 no-fault evictions are abolished entirely. All tenancies have converted into rolling periodic tenancies -- no more fixed-term ASTs. Tenants can leave with two months' notice at any time. Landlords can only recover possession through reformed Section 8 grounds: Ground 1A (intent to sell) requires four months' notice and cannot be used in the first twelve months, Ground 1 (landlord or family occupation) has the same restrictions, Ground 8 (serious rent arrears) now requires three months of arrears instead of two and a four-week notice period, and Universal Credit delays are excluded from the arrears calculation. Rent increases are restricted to once per year via the statutory Section 13 process -- landlords issue Form 4A with two months' notice, and tenants can challenge at a First-tier Tribunal where the Tribunal cannot set a rent higher than what the landlord proposed, meaning tenants face zero financial risk in disputing every increase. Bidding wars are banned. The guide covers deposit protection deadlines, gas safety certificates, EICR requirements, smoke and carbon monoxide alarm obligations, and the cascading civil penalties from £4,000 to £40,000 for non-compliance.

Phase 2: The PRS Database and Landlord Ombudsman

Anticipated for late 2026, the Act introduces a mandatory Private Rented Sector Database. It will be a criminal offence to market or let a property without registration. Landlords must pay an annual fee and upload compliance documentation -- EPCs, Gas Safety certificates, EICR, identity verification. Simultaneously, all landlords must join a new Private Landlord Ombudsman providing tenants with binding redress without court intervention, with powers to order compensation up to £25,000. The critical enforcement mechanism: failure to register on the PRS Database prevents a landlord from using any Section 8 possession grounds. The guide covers what documentation to prepare, what the registration process will require, and how to audit your portfolio for database readiness before the deadline.

EPC C by October 2030 -- The £10,000 Cost Cap and the 2029 Methodology Switch

Every private rented property in England must achieve a minimum EPC rating of C by 1 October 2030. Over 52% of current PRS stock falls below this standard. The guide covers the £10,000 cost cap (inclusive of VAT, reduced from the initially proposed £15,000): if you spend £10,000 on qualifying improvements and the property still fails to reach C, you can register a ten-year High Cost exemption. For properties valued under £100,000, a proportional 10% Property Value Adjustment cap applies -- a £70,000 terrace requires only £7,000 in spend before exemption. The critical timing issue: in 2029, the assessment methodology switches from SAP to the more demanding Home Energy Model (HEM). Properties that achieve a C rating under the current SAP methodology before October 2029 are grandfathered in as compliant for up to ten years. This creates a strong financial incentive to retrofit now rather than wait. The guide covers the removal of the blanket heritage exemption for listed buildings, the extension to HMOs and short-term lets, and the £30,000 fines per property per breach for non-compliance.

Capital Gains Tax at 18% and 24% -- 60-Day Reporting and Spousal Transfers

The guide walks through a complete disposal calculation: gross sale price less disposal costs, acquisition cost, stamp duty and legal fees at purchase, qualifying enhancement expenditure, and the £3,000 annual personal exemption. It covers the rate structure -- 18% for basic-rate taxpayers, 24% for higher and additional-rate taxpayers -- and how adding the gain to your regular taxable income can push you across the threshold mid-calculation. It explains Principal Private Residence relief apportionment for investors who originally lived in the property, the effective elimination of Letting Relief (now restricted to concurrent occupation with the tenant), and the strict 60-day reporting deadline: you must report the disposal and remit estimated tax to HMRC within 60 days of completion via a separate online account, entirely independent of your Self-Assessment return. Missing the deadline triggers immediate penalties and accruing interest. The guide also covers spousal transfers on a no-gain-no-loss basis to pool annual exemptions and utilise lower tax bands.

HMO Licensing and Multi-Unit Strategy

For investors targeting the higher yields required to survive the 2026 landscape, the guide covers HMO mandatory licensing rules: any property housing five or more individuals from two or more separate households sharing amenities requires a licence, regardless of the number of storeys. It details minimum room sizes (6.51 sqm for a single adult, 10.22 sqm for two), amenity ratios, and the penalties for operating without a licence. It covers the strategic migration from standard single-family buy-to-lets toward HMOs and multi-unit freehold blocks as the primary vehicles for generating cash flow that survives the Section 24 tax stack, the 5% SDLT surcharge, and the ICR stress test simultaneously.

Compliance Timeline: October 2024 Through October 2030

The guide includes a single chronological reference mapping every regulatory milestone: October 2024 SDLT surcharge increase to 5%, April 2025 threshold changes, May 2026 Renters' Rights Act Phase 1 commencement, late 2026 PRS Database and Ombudsman rollout, 2029 EPC methodology switch from SAP to HEM, and October 2030 EPC C hard deadline. Each date includes the specific compliance action required and the penalty for missing it, so you can build a regulatory calendar for your portfolio rather than discovering deadlines after they have passed.

Who This Guide Is For

This guide is for property investors targeting English residential rental property who:

- Are higher-rate (40%) or additional-rate (45%) taxpayers who need to understand exactly how Section 24 pushes the effective tax rate past 50% on their actual commercial profit -- and whether incorporation into a limited company produces a net saving after CGT, SDLT, refinancing costs, and extraction taxes are modelled

- Are accidental landlords who retained a previous home and now face Renters' Rights Act compliance obligations they never anticipated -- including the abolition of Section 21, the Section 13 rent review process, PRS Database registration, and the EPC C mandate

- Own one to three properties in their personal name and are evaluating whether to expand through a limited company, incorporate the existing portfolio, or exit the market -- and need the full cost-benefit analysis to make that decision with real numbers instead of forum opinions

- Are first-time investors with £50,000 to £250,000 in capital who need to determine whether buy-to-let generates a viable post-tax return in 2026 after modelling the SDLT surcharge, ICR stress test, Section 24 tax stack, management fees, EPC compliance costs, and void periods

- Need England-specific guidance -- not generic UK advice that conflates English SDLT with Scottish LBTT, English Renters' Rights Act provisions with Scottish tenancy law, or English EPC deadlines with Welsh regulations

Why Not Free Tools and Forums?

Free information on English property investment exists. Here is what it actually delivers:

- Property Hub Forum provides one of the most active UK landlord communities, with genuine operational experience from portfolio landlords, letting agents, and mortgage brokers. It is excellent for anecdotal strategy and peer validation. It does not provide worked Section 24 calculations calibrated to your tax band, does not model SDLT at specific price points, and does not walk you through the full incorporation cost-benefit analysis with payback periods. You get experienced opinions without the financial framework to test them against your specific numbers.

- NRLA (National Residential Landlords Association) publishes accurate, legally reviewed guidance on landlord obligations, tenancy law, and compliance checklists. It is a membership-funded advocacy body designed to inform landlords of their rights and lobby for favourable legislation. It does not provide investment viability analysis, regional yield comparisons, or the tax modelling that determines whether a deal works after Section 24. You get compliance guidance without the financial strategy.

- Reddit (r/uklandlords, r/HousingUK, r/UKPersonalFinance) contains genuine frustration from landlords confronting Section 24 for the first time, panicking about the Renters' Rights Act, and debating incorporation. The experiences are real, but the advice is fragmented, frequently legally inaccurate, and heavily shaped by individual grievance. Sorting current 2026 law from pre-reform advice, and correct tax calculations from confidently wrong ones, takes longer than reading a guide that has already done it.

- YouTube property gurus produce content designed to generate leads for high-ticket mentorship programmes and sourcing services costing £2,000 to £10,000. The content is optimistic by design -- presenting property investment as reliably profitable motivates course sales. They rarely model the 50%+ effective tax rate for higher-rate taxpayers, rarely quantify the full incorporation cost cascade, and almost never address the Renters' Rights Act operational burden in detail. You get motivation without the maths that determines whether the deal actually works.

- Accountants and specialist property tax advisors provide bespoke, highly accurate financial structuring advice at £100 to £300 per hour. An accountant advises on tax structure but rarely covers Renters' Rights Act operational procedures, regional yield analysis, SDLT relief strategies, or EPC compliance timelines. For an investor at the research stage, paying £600 for two hours of advice before knowing whether the investment is even viable is capital deployed against the wrong problem.

This guide fills the England-specific gap -- the space between knowing how to invest in property generally and knowing how to invest in a country where Section 24 creates a 50%+ effective tax rate for higher-rate taxpayers, SDLT surcharges drain £8,000 to £40,000 at acquisition, the Renters' Rights Act has abolished no-fault evictions and restricted rent increases to a tribunal-challengeable annual process, every property must hit EPC C by 2030 or face £30,000 fines, and ICR stress tests at 145% reject mortgages on properties yielding below 5.5%. It is the analysis that would take a property tax specialist, a Renters' Rights Act compliance advisor, and a buy-to-let mortgage broker to assemble -- structured as a reference you own permanently.

-- Less Than One Hour of a Property Tax Advisor

A specialist property tax advisor in England charges £100 to £300 per hour. A single accountant consultation to review your Section 24 position costs £300 to £900. Miscalculating your SDLT liability by overlooking the 5% surcharge costs £8,000 to £40,000 in unexpected capital at completion. Failing to conduct a Right to Rent check carries a £10,000 civil penalty per unauthorised occupant on a first breach. Purchasing a property with a D-rated EPC without budgeting for the retrofit means £7,000 to £10,000 in unplanned capital expenditure before the 2030 deadline. A contested eviction under the reformed Section 8 grounds costs months of mortgage payments, insurance, and council tax with zero rental income while you wait for a court hearing.

This guide does not replace your tax advisor or your solicitor. But it gives you the Section 24 tax calculation framework, every allowable deduction, the full SDLT surcharge tables, the incorporation cost-benefit model, the ICR stress test mechanics, the Renters' Rights Act compliance procedures, the EPC C timeline and exemption strategy, the CGT disposal calculation with 60-day reporting, and the regional yield data that ensure you identify every England-specific risk before your deposit is committed -- instead of discovering them on your first Self-Assessment return, your first attempted eviction, or your first rent review.

If it prevents a single SDLT miscalculation, catches a single Section 24 effective rate that turns your deal cash-flow negative, or shows you that the headline 7% yield your agent quoted compresses to 3.2% after the tax stack and operating costs, it pays for itself before you have finished reading it.

30-day money-back guarantee. If the guide does not sharpen your underwriting and protect your investment in England's tax and regulatory environment, you pay nothing.

Download the free England Quick-Start Home Buying Checklist to see the action plan covering pre-purchase due diligence, tax structure evaluation, and compliance requirements. When you are ready for the full Section 24 analysis, SDLT calculations, incorporation framework, Renters' Rights Act procedures, and regional market data, the complete guide is here.

The spreadsheet says the deal works. This guide tells you whether HMRC, the Renters' Rights Act, and the ICR stress test agree.