You Cannot Use an English Buying Guide in Northern Ireland

You have googled "how to buy a first home UK" and found guides that explain Help to Buy, council tax bands, and licensed conveyancers. None of that applies here. Northern Ireland has its own shared-ownership scheme with its own price caps and eligibility traps. It has domestic rates instead of council tax — calculated on 2005 property valuations through a system that exists nowhere else in the UK. It has an archaic land registration system where your solicitor might tell you the property has "unregistered title" — a phrase that sounds alarming but is a normal feature of Northern Irish land law dating from 1708.

You have checked the Co-Ownership website but cannot figure out whether the £210,000 cap (rising to £215,000 in April 2026) will actually cover any property worth buying. You have read about stamp duty changes in the media but cannot work out whether they affect you (they almost certainly do not — the average NI house price sits well below the £300,000 threshold). You have been told you need a solicitor, not a conveyancer, but nobody has explained why — or warned you about the Regional Property Certificate bottleneck that delays most NI transactions.

The Northern Ireland Property Navigation System is a complete, jurisdiction-specific roadmap that replaces generic UK advice with the exact schemes, legal processes, tax rules, and neighbourhood realities you need to buy confidently in Northern Ireland.

What Makes This Different

Free guides give you bullet points. Government websites give you legal language. Mortgage broker blogs give you lead-generation content dressed up as advice. None of them map the complete NI buying journey — from working out whether Co-Ownership is right for you, through navigating unregistered land and ground rent redemption, to understanding why your domestic rates bill will be different from what any English friend pays in council tax.

This guide connects every piece: the financial schemes, the legal process, the tax system, the neighbourhood dynamics, and the hidden costs — in the order you actually encounter them.

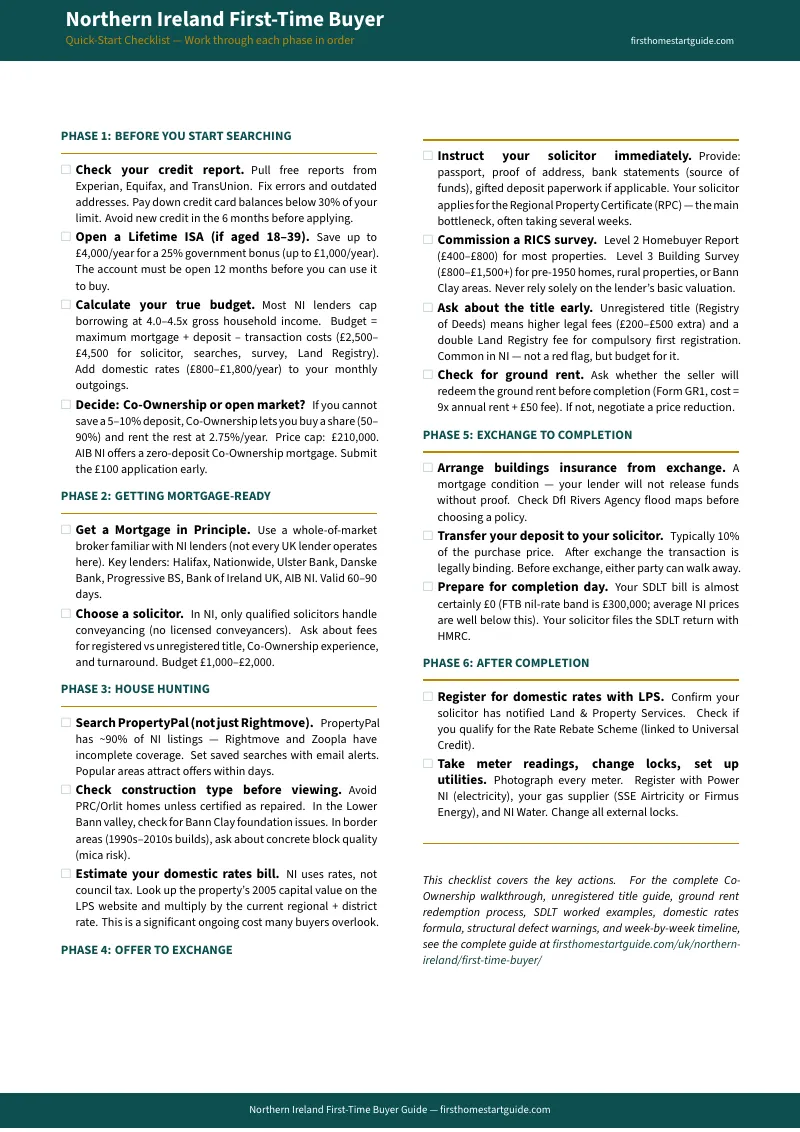

What's Inside

Co-Ownership: Everything the Official Website Doesn't Tell You

How the 50–90% equity split works in practice. The 2.75% annual rent on Co-Ownership's share — calculated and shown in monthly figures at realistic NI price points. Staircasing mechanics (5% minimum increments, valuation fees, no early repayment penalties from Co-Ownership). The zero-deposit AIB NI mortgage and which other lenders are compatible (Danske Bank, Progressive Building Society, Bank of Ireland). The £6,000 repair threshold that disqualifies properties after survey — and the repeated survey failures that burn applicant cash. The "squeezed middle" trap: earning too much for Co-Ownership but not enough to save a deposit while paying £1,000+ in monthly rent.

Stamp Duty: Why the Media Panic Does Not Apply to You

Post-April 2025 first-time buyer rates: 0% on the first £300,000. Worked calculations at £195,000, £250,000, and £350,000 showing that most NI purchases owe nothing. The £500,000 cliff edge. The joint purchase trap that wipes out all relief if one buyer has ever owned property. The 5% additional dwelling surcharge.

Domestic Rates: The Tax System England Doesn't Have

How your bill is calculated (2005 capital value × regional rate + district rate). Why two identical houses in different council areas pay different amounts. How to look up any property's capital value on the LPS website before you buy. The rate rebate scheme for Universal Credit recipients. Your legal obligation to register with Land & Property Services after completion — and why not registering creates arrears, not exemption.

Unregistered Land and the Registry of Deeds

Why Northern Ireland still operates two land recording systems — the modern Land Registry (state-guaranteed title) and the 1708 Registry of Deeds (which merely records that a document exists). What happens when you buy an unregistered property: compulsory first registration, ACE maps from LPS, double Land Registry fees, and 8–18 months of administrative processing. Why this is completely normal and not a reason to panic — your ownership is legally protected from the moment your solicitor lodges the application.

Ground Rent Redemption

Many older NI properties carry ground rents or fee farm grants. The Ground Rents Act (NI) 2001 gives you the right to buy these out using Form GR1 (cost: nine times the annual ground rent plus a £50 fee). How to serve notice via Form GR2, obtain a Certificate of Redemption, and achieve clean freehold title. Whether to negotiate vendor redemption before completion or handle it yourself afterwards.

The Conveyancing Process — NI-Specific

Why only qualified solicitors (regulated by the Law Society of Northern Ireland) can handle property transactions here — no licensed conveyancers, no online conveyancing factories. The 42–70 day timeline. AML identity checks. Regional Property Certificates from the centralised RPCU in Fermanagh — the single biggest bottleneck in NI conveyancing. Statutory Charges Register, EJO, and Bankruptcy searches. Exchange and completion mechanics (often same-day in NI). The gazumping risk window. Typical fees: £1,000–£2,000 for solicitor, £90–£122 for RPC, £30–£50 for Statutory Charges, £35–£75 for EJO/Bankruptcy.

Structural Risks That Make NI Properties Unmortgageable

Bann Clay (diatomaceous earth in the Lower Bann valley — properties built without piled foundations will not be financed). PRC/Orlit homes (approximately 200 in NI — defective concrete construction from the post-war era). Mica and defective blocks (pyrrhotite risk in border-area properties built in the 1990s–2010s). How to check construction type before you waste money on surveys.

Belfast Neighbourhoods and the Geography of Division

Peace lines and interface areas in North and West Belfast — what they mean in practice for commuting, daily life, and property values. Cross-community areas that command premiums: Botanic Quarter, Ballyhackamore, Belmont Road, Stranmillis. Commuter towns: Lisburn, Bangor, Newtownabbey, Carryduff. The SEAG transfer test and why school catchment areas work differently in NI (grammar school admission is academic, not geographic). The border effect on prices in Newry and Derry/Londonderry.

Cross-Border ROI Buying

How the 20% sterling haircut works when you earn in GBP but buy in the Republic. The 4× income cap at 90% LTV. A worked example showing how a £35,000 salary translates to a maximum ROI loan of just €128,800. EUR/GBP exchange rate risk over months of conveyancing. The requirement for an ROI-licensed solicitor. When Donegal makes financial sense — and when it does not.

The NI Mortgage Market

Which UK lenders actually operate here (and which quietly exclude the BT postcode). Income multiples of 4.0–4.5×. Agreement in Principle. Co-Ownership-compatible lenders compared. Valuation retentions — when lenders withhold funds until repairs are completed — and how to bridge the cash gap.

Complete Cost Worksheet and Week-by-Week Timeline

Every cost beyond the deposit, line by line. Solicitor fees, RPC, Statutory Charges, surveys, Land Registry (standard and double for first registration), Co-Ownership admin fees, buildings insurance, domestic rates estimate. Plus a phased timeline from "deciding to buy" through mortgage preparation, house hunting, offer, conveyancing, and keys.

Who This Guide Is For

- Co-Ownership applicants who need to understand the £210,000 cap, the zero-deposit option, the 2.75% rent calculation, staircasing costs, and the property condition requirements — with worked monthly cost comparisons

- The "squeezed middle" — people earning too much for Co-Ownership but unable to save a traditional deposit while paying £1,000+ rent — who need a realistic plan to bridge the gap

- Anyone using a UK-wide guide and getting confused by references to council tax, Help to Buy, licensed conveyancers, and other English-only concepts that do not apply in Northern Ireland

- Belfast buyers who need honest neighbourhood guidance on peace lines, cross-community areas, and how community geography affects property values

- Border-area buyers considering the Republic of Ireland who want to understand the sterling haircut, EUR transaction risk, and cross-border mortgage realities before committing

- NIHE tenants weighing the House Sales Scheme discount against open-market buying via Co-Ownership

Why Free Guides Fall Short

The NI Direct website explains the House Sales Scheme in dense bureaucratic language that tells you what a ground rent is but not whether you should redeem it before or after completion. PropertyPal publishes excellent market reports — for estate agents and investors, not first-time buyers trying to figure out how domestic rates will affect their monthly budget. Mortgage broker blogs explain how to get an AIP but never mention that some UK lenders quietly exclude the entire BT postcode from their lending criteria.

Free resources are fragments. This guide is the complete map — with every scheme, legal process, tax calculation, cost line item, and neighbourhood reality connected in the order you actually encounter them.

100% Satisfaction Guarantee

If the guide does not deliver what this page promises, email [email protected] for a full refund. No conditions, no time limit.

— Less Than One Property Viewing's Petrol

You will spend more driving to viewings than this guide costs. One avoided survey on a PRC home saves you £400–£800. One correct domestic rates estimate prevents months of budget miscalculation. Understanding the Co-Ownership property condition requirements before you bid prevents repeated survey failures at £120 each.

Download the free Northern Ireland Quick-Start Home Buying Checklist to see the 18-step action plan. When you are ready for the complete system — with worked cost calculations, scheme comparisons, conveyancing timelines, and neighbourhood maps — get the full guide.