Scotland's Blind Bidding System Is Built to Extract Every Pound You've Saved. This Guide Maps Every Trap Before You Walk In.

You've found the flat. It's a two-bed in Leith, listed at "Offers Over £185,000." The Home Report valuation says £195,000. You check ESPC's sold prices and discover that properties in Leith Links sell for 106.4% of valuation on average. So to win, you'll probably need to bid around £207,000. Your mortgage offer is based on the valuation — £195,000 at 90% LTV — which means the lender will advance £175,500. Your deposit covers £19,500. But your bid is £12,000 above valuation, and the bank will not finance that premium. You need £31,500 in cash. Not £19,500. And no one told you until the closing date was 48 hours away.

You search online for guidance. Mygov.scot explains the buying process in procedural steps that assume you already understand what a closing date is, what missives mean, and why concluded missives are legally binding in a way that exchange of contracts in England is not. ESPC's buyer guides are written by the solicitor-estate agents who list properties — professionals who earn their fee from the seller and whose primary interest is a completed sale, not your negotiating position. MoneySavingExpert covers mortgages brilliantly but treats Scotland as a sidebar to the English process, mentioning LBTT in a paragraph and missives not at all. Reddit's r/HousingUK has real stories from Scottish buyers, except half the advice comes from English buyers describing a completely different legal system — and the closing date tactics from six months ago may not apply to a market where Edinburgh properties now sell at an average of 101.5% of valuation.

Here's the core problem: Scotland's property system is fundamentally different from England's — sealed bids you cannot see, solicitor-estate agents who act for both sides of the market, missives that become legally binding before you've finished arranging your mortgage — and there is no single resource that maps the financial mechanics, the legal exposure, and the tactical decisions across the entire process in one place. You are navigating a blind auction with incomplete information, and every free guide you find was written by someone with a financial interest in you bidding higher.

The Scotland First-Time Buyer Guide is a Scotland Buyer Decision System. Not a summary of LBTT rates or a glossary of Scottish legal terms. It's a structured decision framework that maps every financial trap in the blind bidding process, every cash-gap scenario between valuation and winning bid, every legal commitment point from noting interest through concluded missives — so you make each decision knowing the full cost, the full risk, and the full picture, before you write a number on a sealed envelope.

What's Inside the Scotland Buyer Decision System

The complete guide plus eight standalone printable worksheets — covering every stage from mortgage-in-principle through settlement day, plus fillable tools you print, bring to solicitor appointments, and use on closing date night:

Blind Bidding Decision Framework

Scotland's sealed bid system means you write a number without knowing what anyone else has offered. Bid too low and you lose the property. Bid too high and you've paid thousands more than the next highest offer — money that comes directly from your savings because the mortgage lender will not finance anything above the Home Report valuation. The guide maps the valuation cash gap at every bid increment: at a £200,000 valuation with 90% LTV, bidding at valuation costs you £20,000 in cash. Bidding 6% over costs £32,000. Bidding 12% over costs £44,000. It covers how to read ESPC sold-price data to calibrate your bid, when "Offers Over" pricing signals a closing date versus a negotiation, how to set your walk-away ceiling before emotions enter the room, and the tactical difference between being the only bidder and competing against four others on a Friday closing date.

LBTT and the Joint-Purchase Trap

Scotland's Land and Buildings Transaction Tax gives first-time buyers relief on the first £175,000 — saving a maximum of £600. That's it. England's equivalent saves up to £5,000. But the real trap is the joint-purchase rule: if you buy with a partner who has ever owned property anywhere in the world, you lose all first-time buyer relief. Not their share — all of it. A joint purchase at £200,000 where one partner previously owned a flat in London means you pay £1,100 instead of £500 in LBTT. And if your non-first-time-buyer partner is buying a second property, the Additional Dwelling Supplement of 8% — increased from 6% in December 2024 — applies to the entire purchase price. On a £200,000 property, that's £16,000 in tax. The guide maps every scenario: sole purchase, joint purchase, ADS liability, reclaim windows, and the exact ownership history rules that Revenue Scotland applies.

Missives: The Point of No Return

In England, nothing is binding until exchange of contracts — buyers and sellers can walk away at any point, and roughly a third of deals collapse. In Scotland, concluded missives are a binding contract. Withdrawal after conclusion is a material breach carrying severe financial penalties. This sounds like it protects you, and in some ways it does — no gazumping. But it also means that if your mortgage falls through after missives conclude, if the survey reveals problems you missed in the Home Report, or if your personal circumstances change, you are legally committed. The guide explains exactly when missives conclude, what conditions your solicitor should insist on before conclusion, how to structure suspensive conditions that protect you, and the specific scenarios where buyers have been trapped by missives that concluded faster than they expected.

Home Report Decoder

The Home Report is mandatory in Scotland, paid for by the seller, and free for you to access — saving £400 to £800 compared to England where buyers commission their own surveys. But "free" doesn't mean "simple." The report uses a Category 1/2/3 rating system: Category 1 means no immediate action, Category 2 means repair or replacement needed, and Category 3 means urgent repair required. A single Category 3 item can trigger a mortgage retention — where the lender withholds part of your loan until repairs are completed, leaving you scrambling for cash at settlement. The report must be less than 12 weeks old when the property is listed, and most lenders won't accept one older than 3 months. The guide covers how to read every section, which Category 2 items are genuinely minor and which signal £10,000+ problems, how the valuation figure interacts with your bid strategy, and what to do when the Energy Performance Certificate rating drags the property into a different lending category.

Tenement Flat Risk Assessment

Forty percent of Scottish housing stock is tenement flats. Buy one, and you inherit shared maintenance obligations under the Tenement Management Scheme — where a majority vote of owners can commit you to repairs costing thousands of pounds, and if one owner refuses to pay, the remaining owners must cover the shortfall. Property factors must be registered under the Property Factors (Scotland) Act 2011, but registration doesn't mean competence or fair pricing. The guide covers how to check the property factor's track record before you bid, how to read the Title Deeds and Deed of Conditions for maintenance obligations, the Notice of Potential Liability mechanism that follows non-paying owners, and the specific questions to ask your solicitor about common repairs funds, roof responsibility, and shared close maintenance — before you discover at your first owners' meeting that the building needs £8,000 in roof repairs and you owe a quarter of it.

LIFT Shared Equity and Scheme Strategy

The Low-cost Initiative for First Time Buyers provides government equity of 10% to 40% of the purchase price — no interest, no rent on the government's share. It sounds ideal. In practice, LIFT is subject to annual budget cycles and periodic closures, with strict regional price thresholds that vary by local authority area. The First Home Fund closed in 2021. Help to Buy Scotland closed. LIFT's Open Market scheme remains, but competition is intense and the application window can shut without warning. The guide covers current eligibility criteria, the regional price caps, how to staircase out in 5% increments at current market value, and the realistic timeline for securing LIFT funding — including what to do when your preferred property is above the local threshold and whether splitting your deposit strategy between LIFT and conventional purchase makes financial sense.

Total Purchase Cost Calculator and Affordability Worksheets

Conveyancing fees in Scotland typically run 0.5% to 1% of the purchase price — around £1,200 for a £200,000 property. Add LBTT, Land Registry fees, removal costs, and the potential valuation cash gap, and your total non-deposit outlays at £200,000 reach approximately £2,386 before you've moved a single box. The guide tallies every cost into a single worksheet, calculates your mortgage capacity at 4.5x income, models deposit requirements at 95%, 90%, and 85% LTV, and shows you the stress-tested monthly repayments at 2% above your fixed rate — so you know your true all-in figure before you note interest on a single property.

Who This Guide Is For

This guide is for first-time buyers in Scotland who:

- Are facing their first closing date and have no idea how much to bid above the Home Report valuation — or whether they can afford the cash gap between their bid and what the mortgage lender will actually advance

- Are buying with a partner and need to know whether their partner's previous property ownership anywhere in the world wipes out their LBTT first-time buyer relief entirely — before they submit an offer that assumes they're getting it

- Are looking at tenement flats in Edinburgh, Glasgow, or Dundee and need to understand shared maintenance liabilities, property factor obligations, and the Tenement Management Scheme before they commit to a building with a £12,000 roof repair bill waiting to be voted on

- Are relocating from England and assume the Scottish system works like the one they've read about — only to discover there's no gazumping but also no cooling-off period, no exchange-completion gap, and a binding missive process that moves faster than they expect

- Are considering LIFT shared equity and want to know whether the scheme is realistically available for their target area and price range, or whether they're planning around funding that may be closed by the time they're ready to apply

- Want every transaction cost, every legal commitment point, and every bidding decision mapped in one document — so they walk into solicitor meetings, mortgage appointments, and closing dates knowing exactly where they stand instead of discovering the cash gap at 5pm on a Friday

Why Not Free Resources?

Free information on buying your first home in Scotland is everywhere. Here's what each source actually delivers:

- Mygov.scot explains the steps of buying a home in Scotland with government clarity — noting interest, making an offer, concluding missives, settlement. What it doesn't cover: the valuation cash gap that turns a £20,000 deposit into a £32,000 cash requirement when you bid 6% above valuation. Or the joint-purchase LBTT trap. Or how to read a Home Report's Category 2/3 ratings to determine whether the building has a problem that will trigger a mortgage retention. It describes the process. It doesn't map the financial decisions the process forces you to make.

- ESPC buyer guides are written by the solicitor-estate agents who list Edinburgh, Lothian, Fife, and Borders properties. The guides are professional and accurate. They're also written by firms whose revenue depends on properties selling at or above valuation — the same firms that set the "Offers Over" prices, manage the closing dates, and represent both buyers and sellers across the market. Their advice on how much to bid is not independent. It can't be.

- MoneySavingExpert covers mortgages, deposits, and government schemes with characteristic thoroughness — for England. Scotland gets a brief section noting that LBTT replaces Stamp Duty and that the buying process is different. It doesn't model the blind bidding cash gap, doesn't explain missive risk, doesn't cover tenement maintenance, and doesn't mention the joint-purchase LBTT trap. If you're buying in Scotland, it covers about 40% of what you need to know.

- Reddit (r/HousingUK, r/Scotland) has real experiences from Scottish buyers — closing date stories, solicitor recommendations, bidding war outcomes. Half the responses come from English buyers describing a system that doesn't apply north of the border. The Scottish-specific advice is often excellent but never cross-referenced against current LBTT rates, current LIFT availability, or current market conditions that determine whether Edinburgh's 101.5% average over-valuation applies to the specific neighbourhood you're looking at.

- Solicitor-estate agent guides (Slater Hogg, Thorntons, Gilson Gray) provide competent overviews of the conveyancing process from firms that want you to instruct them. The advice is sound. The perspective is that of a firm whose business model depends on transaction volume, not on buyers who decide — after proper analysis — to wait, bid lower, or walk away.

This guide fills the decision gap — the space between knowing that Scotland uses sealed bids and understanding exactly how much to bid, with what conditions, at what cash cost, and at what point you become legally committed. It's the analysis an independent advisor with no listing fees, no commission, and no auction to manage would give you, structured as a permanent reference you own.

— Less Than Your Solicitor's Registration Fee

Conveyancing fees for a £200,000 property run around £1,200. Your LBTT liability starts at £500. The valuation cash gap on an average Edinburgh bid can add £12,000 to £24,000 in cash you didn't plan for. A single tenement roof repair vote can commit you to thousands of pounds in shared costs.

This guide doesn't replace your solicitor. But it gives you the blind bidding calculations, LBTT analysis, missive risk framework, Home Report decoder, tenement liability assessment, and total cost worksheets that ensure you walk into every appointment, every viewing, and every closing date knowing exactly where your money goes — instead of discovering the cash gap when it's too late to adjust.

If it prevents a single over-bid where you pay £8,000 more than the next highest offer, catches a single tenement maintenance trap before you're committed, or stops you losing LBTT relief because of a joint-purchase rule you didn't know existed, it pays for itself before you've finished reading it.

30-day money-back guarantee. If the guide doesn't make your home buying process clearer and your financial position stronger, you pay nothing.

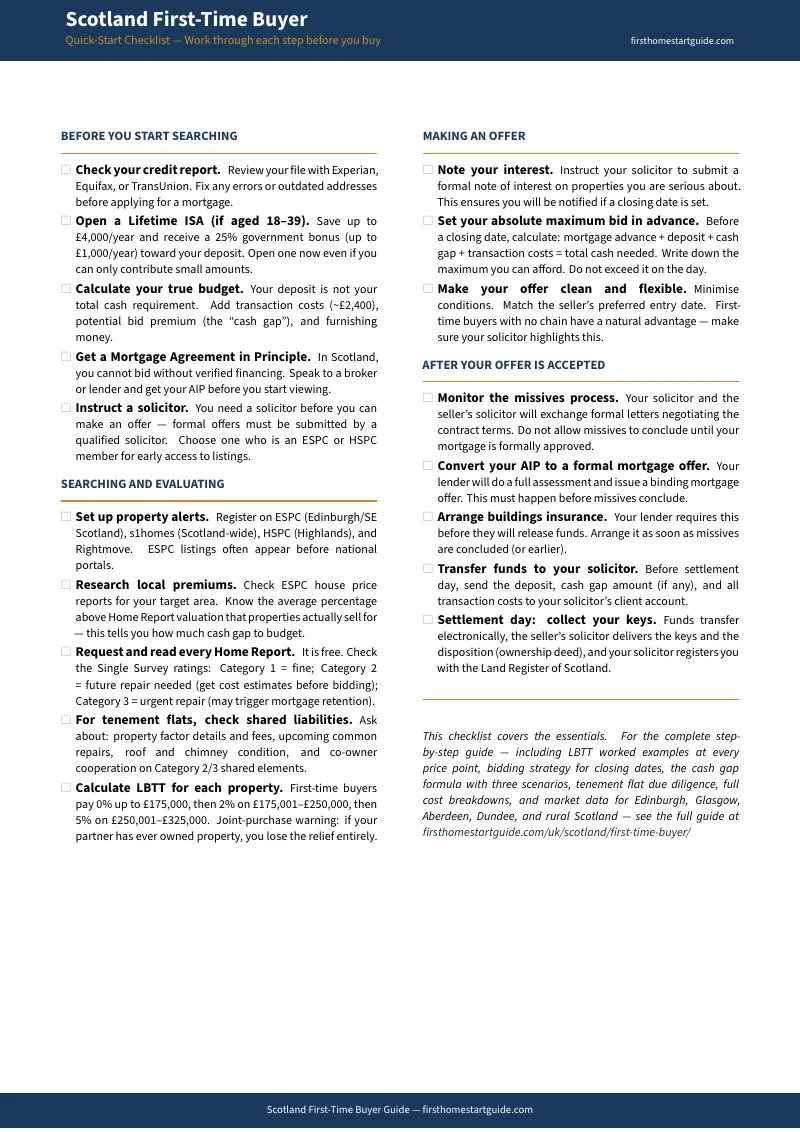

Download the free Quick-Start Checklist to see the step-by-step action plan covering LBTT calculations, blind bidding essentials, Home Report ratings, and the missive timeline. When you're ready for the full decision system — complete with bidding worksheets, tenement risk assessment, LIFT scheme analysis, and the cash-gap calculator — the complete guide is here.

You've saved the deposit. Now stop the sealed bid system from taking more than it should.