You Found the Buenos Aires Apartment. You Ran the Numbers. Now You Need to Deliver $200,000 in Physical Cash to a Closing Table — and Nobody Will Tell You How.

You've watched the YouTube videos. You've read the Palermo walking tour blogs. You've done the currency math — your salary in Austin or London or Sydney buys a two-bedroom apartment in Recoleta that would cost four times as much back home. Buenos Aires prices dropped nearly 50% between 2018 and 2023, Milei's deregulation is pulling foreign capital back in, and local analysts project up to 40% price recovery in prime neighborhoods. The macroeconomic thesis is obvious. You're ready to buy.

Then you discover the operational reality. Argentine real estate transactions happen in physical US dollars. Not wire transfers. Not escrow accounts. Not bank-certified checks. Actual bills, counted by hand at a notary's desk. Your US bank won't wire the money because international transfers to Argentina trigger compliance flags — expats report accounts being frozen or permanently closed after a single wire attempt. The informal exchange houses (cuevas) offer better rates but operate entirely outside the legal system, and at least one has gone bankrupt overnight, vaporizing a buyer's entire purchase fund. The property listing says "$180,000" but the seller won't accept your money unless every bill is a post-2013 "cara grande" $100 note — older bills get rejected at the closing table or discounted 2-3%. And the notary system that governs the entire transaction has no equivalent in common-law countries. There is no title insurance. There is no standard escrow. There is an escribano público whose legal authority you need to understand before you sign anything.

You search for help. Free guides from expat blogs and real estate portals give you the basics: foreigners can buy urban property freely, you need a tax ID, the process goes reserva → boleto → escritura. Accurate and completely insufficient. None of them explain how to actually structure a six-figure capital transfer without getting your Chase or HSBC account closed. None of them walk through the difference between a cueva, a licensed exchange house, and a private financial network — or tell you how to vet which one won't disappear with your money. None of them explain that the chain of custody you establish today determines whether you can legally sell the property and repatriate the proceeds five years from now.

Here's the gap every free resource leaves open: Argentina's property market runs on a parallel financial infrastructure that no English-language guide maps end to end. The tax ID system changed in March 2026 — the CDI was eliminated, and foreign buyers now need a full CUIT obtained through an Argentine representative. The stamp tax rate varies by province from 1.5% to 4%. The boleto de compraventa locks you into a 30-50% cash deposit with forfeiture penalties. And the single question that keeps every foreign buyer awake — "how do I physically get $200,000 in approved US banknotes from my home country to a closing table in Buenos Aires without triggering a bank closure, getting robbed, or creating a legal liability that traps my capital in Argentina permanently" — gets answered with a shrug and a cueva recommendation. That's not a plan. That's a prayer.

The Buying Property in Argentina — Expat Guide is The Dollar Transit Playbook. Not a neighborhood tour or a market trends summary. It's a 15-chapter operational manual that maps every friction point between "I want to buy in Buenos Aires" and "the escritura is registered in my name" — with the capital movement strategies, legal mechanics, cost breakdowns, and due diligence frameworks that determine whether your transaction closes cleanly or collapses at the notary's desk.

What's Inside The Dollar Transit Playbook

A comprehensive guide covering 15 chapters and 2 appendices — plus a 20-item Quick Start Checklist and 8 standalone printable tools (worksheets, reference cards, and checklists you can bring to bank meetings, escribano appointments, and property viewings). Every chapter ties directly to a decision point where foreign buyers lose money, lose time, or lose their entire transaction:

Capital Movement Strategy — Three Legal Channels Compared

The single highest-anxiety decision in the entire purchase: how to get your USD from a regulated bank account in your home country to a closing table in Buenos Aires. The guide maps three channels — official bank wire (compliant but flagged by US/EU compliance), licensed exchange houses (the post-cepo legal alternative to cuevas), and offshore transfer through established real estate consultancies (domestic US-to-US wire that bypasses international flags entirely). Each channel gets a risk profile: compliance exposure, fee structure, physical security requirements, and chain-of-custody documentation for future resale. The chapter also covers how to pre-notify your bank, structure transfer amounts to reduce Suspicious Activity Report triggers, and why wiring directly to an Argentine bank account is the option most likely to result in funds "lost" between institutions for weeks.

The Cara Chica Problem — Sourcing the Right Bills

Argentine sellers systematically reject or discount pre-2013 US $100 bills — the "cara chica" (small face) notes without the blue security ribbon and enlarged Franklin portrait. This isn't a preference. It's a market convention rooted in decades of counterfeit currency trauma. Arriving at closing with $150,000 in perfectly legal but older-series bills can halt your entire transaction. The guide explains how to request specific bill series from your bank weeks before travel, the premium (if any) for cara grande notes, and what to do if your bank's vault doesn't carry enough new-series bills to cover your purchase amount. It also covers the inspection process at the closing table — how the escribano or a professional bill counter verifies each note, and what happens when individual bills are rejected.

The Escribano System Decoded

If you've bought property in the US, UK, or Australia, nothing in your experience prepares you for the escribano público. This isn't a notary who stamps documents — it's a legal professional with a law degree and post-graduate specialization who combines the roles of title agent, escrow officer, and tax withholder. The escribano conducts the title search, verifies there are no liens or unpaid utility bills, drafts the deed, and registers it with the Land Registry. But here's the critical nuance that free resources skip: the escribano serves the transaction and the state, not you. The guide explains why you still need a separate bilingual property lawyer to review the boleto terms, what the escribano's title study actually verifies (and what it doesn't), and how their fees are calculated — typically 1-2% of the property value.

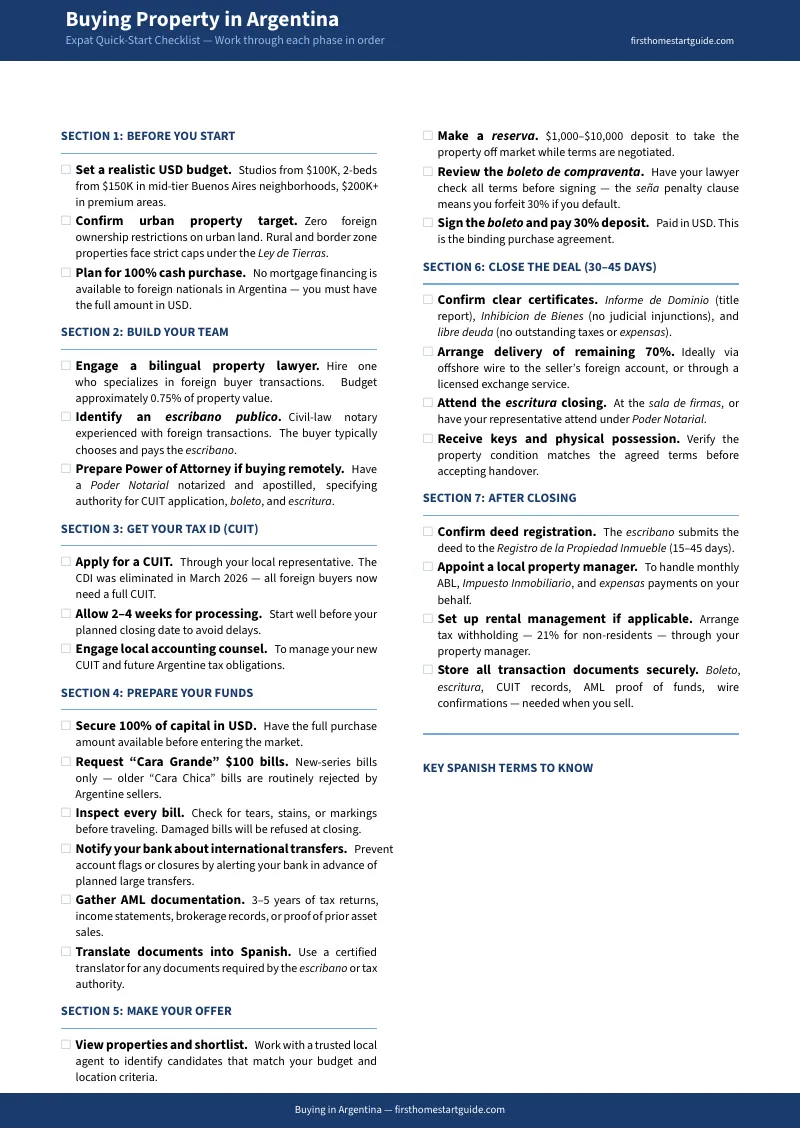

The Three-Stage Purchase Process — Reserva, Boleto, Escritura

Argentine property transactions follow a rigid sequence with escalating financial commitments at each stage. The reserva locks in your offer with a $1,000-$10,000 deposit. The boleto de compraventa — signed roughly two weeks later — commits you to a 30-50% cash payment and makes agent commissions due. Back out after the boleto, and you forfeit the entire deposit. If the seller defaults, they owe you double. The escritura finalizes the transfer weeks later, when you deliver the remaining 70% in physical USD. The guide covers each stage's legal consequences, the penalty clauses you need your lawyer to review, and the bureaucratic delays ("mañana culture") that routinely push timelines past the 30-60 day estimate that agents quote.

Transaction Cost Calculator — The Real Number Is 7-12% Above the Property Price

Free guides quote the property price. Your actual cost includes agent commissions (3-4% plus 21% VAT — paid by both buyer and seller), escribano fees (1-2%), stamp tax (2.5% in Buenos Aires City, up to 4% in Buenos Aires Province), property registry inscription (~0.35%), and an independent bilingual lawyer (~0.75%). The guide includes worked examples for a typical Buenos Aires apartment showing the total all-in cost, which line items are negotiable, and which are fixed by law. It also covers the seller-side ITI abolition, how the 2024 repeal affects market liquidity, and what the blanqueo tax amnesty means for the supply of motivated sellers.

The 2026 CUIT Overhaul — Your Tax ID Changed

Most English-language guides still reference the CDI — a simplified tax ID that foreign buyers used for one-off transactions. It was eliminated in March 2026 by ARCA General Resolution 5803/2025. Foreign buyers must now obtain a full CUIT through a designated Argentine representative. The guide covers the new application process, the role of the "Administrador de relaciones apoderado," the 2-4 week timeline you need to budget, and why your escribano should handle this as part of their service scope.

Due Diligence Framework and Anti-Money Laundering Compliance

The escribano's mandatory title study is one layer of due diligence. Your own verification goes further: informe de dominio (property domain report), certificado catastral (cadastral certificate), verification that utility bills and expensas (building maintenance fees) are current, and anti-money laundering documentation proving the legal origin of your funds. The guide lists the red flags that should make you walk away from a deal — unreleased liens, discrepancies between catastral and title records, pressure to skip the boleto stage — and the AML documentation package you need to prepare as a foreign buyer importing capital.

Neighborhood Pricing Map — Budget Tiers from $100K to $700K+

A $100,000 budget buys a studio in Villa Lugano or an older unit in Recoleta needing renovation. $150,000-$220,000 reaches a quality two-bedroom in Caballito, Flores, or Palermo. $300,000-$500,000 opens newer construction with amenities in Belgrano, Nunez, and Colegiales. $700,000+ enters the luxury tier in Palermo Chico and Puerto Madero. The guide includes per-square-meter pricing across Buenos Aires neighborhoods, the house vs. apartment price gap ($2,450/sqm average for apartments vs. $1,825/sqm for houses), and an honest assessment of which neighborhoods hold their dollar value regardless of political cycles — critical information for buyers worried about the next election.

8 Standalone Printable Tools — Included

Every purchase comes with standalone reference PDFs designed to be printed and used in the field — at the bank, the escribano's office, or during property viewings:

- Capital Movement Comparison — Side-by-side of the three legal channels with risk profiles, fees, and chain-of-custody implications

- Transaction Cost Worksheet — Fill in your target property price and calculate every line item of closing costs

- Cara Chica Reference Card — Which bills are accepted, which are rejected, and what to tell your bank teller

- Due Diligence Checklist — Every verification item to confirm before signing the escritura, plus red flags

- Neighborhood Pricing Reference — Per-square-meter rates and budget benchmarks across Buenos Aires

- CUIT Application Roadmap — The new tax ID process step-by-step (CDI eliminated March 2026)

- Purchase Process Timeline — Reserva → Boleto → Escritura with deposits, penalties, and timelines

- Argentine Real Estate Glossary — 36 essential Spanish terms with plain-English translations

Who This Guide Is For

This guide is for foreign nationals buying property in Argentina who:

- Are buying their first Argentine property and need the entire transaction mapped — from CUIT application through capital movement, escribano engagement, reserva-boleto-escritura sequence, and deed registration — so they understand what happens at each stage, what it costs, and what the penalty is for getting it wrong

- Are based in the US and need to move six figures in USD to Buenos Aires without triggering a Suspicious Activity Report, getting their bank account closed, or creating a chain-of-custody gap that traps their capital in Argentina permanently

- Have found a property they want to buy and need to understand whether their cash — the specific bills in their bank's vault — will be accepted at closing, or whether they'll arrive with $200,000 in perfectly legal tender that the seller refuses to take

- Want to buy for rental income and need to understand the 21% non-resident withholding tax, ABL and Impuesto Inmobiliario obligations, expensas, and the practical logistics of managing a property from another continent

- Are watching the Milei-era market recovery and want to understand the mechanics well enough to close a deal at current prices — not spend six months reading Reddit threads while the window moves

- Plan to sell eventually and need to establish the legal chain of custody on their funds today so repatriation isn't blocked by an audit five years from now

Why Not Free Resources?

Free information on buying Argentine property is everywhere. Here's what each source actually delivers:

- Expat blogs and real estate portals (Live and Invest Overseas, ExpatFocus, Global Property Guide) publish accurate overviews: foreigners can buy freely, you need a tax ID, the process has three stages. What they skip: the capital movement options, the cara chica rejection risk, the 2026 CDI-to-CUIT transition, and every detail that determines whether your transaction actually closes. You get a sanitized summary designed to make Argentina seem accessible, not to prepare you for the closing table.

- YouTube channels (The Wandering Investor, mgni_brokers) produce excellent macroeconomic analysis — Milei's reforms, neighborhood comparisons, price recovery projections. The best ones are genuinely informative. What they don't provide: a single structured document you can hand to your escribano, lawyer, and bank officer that covers the CUIT application, fund transfer structuring, due diligence checklist, and cost calculator in one operational reference. You get expert insight optimized for watch time, not for a $200,000 closing.

- Reddit and expat forums (r/BuenosAires, r/expats, ExpatsBA) contain real stories from real buyers — alongside advice that predates the 2026 CUIT overhaul, casually recommends wiring to a cueva without mentioning counterparty risk, and confidently states that the dolar blue is "totally safe" without addressing the chain-of-custody implications for future resale. Some of these buyers closed smoothly. Some had their US bank accounts shut down. Both outcomes are documented. Neither tells you which applies to your situation.

- Local boutique agencies (BuySellBA, The Latinvestor) provide the most nuanced free content and offer genuine full-service transaction support — for a commission built into your purchase price. The good ones are worth their fee. But their published guides cover the steps you'll take with their help, not the independent due diligence framework you need to verify their work.

This guide fills the operational gap — the space between knowing that foreigners can buy property in Argentina and understanding exactly how to move capital, vet your legal team, structure the boleto, verify the title, and close the escritura without losing your deposit, your bank account, or your ability to sell the property later. It's the analysis an independent advisor with no commission to earn and no cueva to recommend would give you, structured as a permanent reference you own.

— Less Than the Fee a Cueva Charges on $5,000

A cueva charges 3.5-4% on every dollar it converts — that's $7,000-$8,000 on a $200,000 transfer. A bilingual property lawyer costs 0.75% of the purchase price. The boleto deposit you forfeit if you back out after signing ranges from $54,000 to $90,000. A US bank account closure doesn't just lose you the wire — it disrupts your entire financial life.

This guide doesn't replace your escribano or your property lawyer. But it gives you the capital movement strategies, the bill-sourcing protocol, the CUIT application roadmap, the transaction cost calculator, and the due diligence framework — as standalone printable tools you can bring to every meeting — so you walk in understanding the system instead of discovering how Argentine real estate works by losing money at each stage.

If it prevents a single rejected wire transfer by restructuring your capital movement, catches a single cara chica rejection before you arrive at closing, or identifies a single boleto clause your lawyer should renegotiate, it pays for itself before you've finished the first chapter.

30-day money-back guarantee. If the guide doesn't make the Argentine property transaction clearer and your capital movement safer, you pay nothing.

Download the free Foreigner's Quick Checklist to see the step-by-step action plan covering CUIT application, fund preparation, team assembly, offer execution, and post-closing compliance. When you're ready for the full Dollar Transit Playbook — the 15-chapter guide plus 8 standalone printable tools including the capital movement comparison, transaction cost worksheet, cara chica reference card, and neighborhood pricing reference — the complete kit is here.

The apartment exists. The price is right. The only question is whether you can close the deal without the system closing you out first.