Your Bank Said "5% Down." Denmark Will Demand 20%. Your Agent Said "Ejerlejlighed." The Listing Was an Andelsbolig with a Toxic Swap.

You found an apartment in Copenhagen. 85 square meters, top floor, Frederiksberg address. The listing says 4,200,000 DKK. You have a permanent contract at Novo Nordisk, your CPR is registered, and your bank pre-approved financing at 80% LTV. You are ready to sign.

Then three things happen at once. The bank's credit committee overrides the pre-approval and demands 20% down — 840,000 DKK in liquid capital — because foreign buyers are flight risks and the 5% legal minimum is a fiction for anyone without a decade of Danish credit history. The 85-square-meter apartment in the listing turns out to be 73 square meters of actual living space — because the BBR area includes your share of the stairwell and the exterior walls, and the tinglyst area on the deed is 12 square meters smaller than what was advertised. And the property itself is not an ejerlejlighed at all. It is an andelsbolig — a cooperative share — which means no realkredit access, no market-rate appreciation, joint liability for the building's commercial debt, and a monthly boligafgift that embeds the cost of an interest rate swap the board entered in 2018.

Each of these traps is well-documented in Danish. None of them are explained in English in a single place.

Here is what no free resource assembles: Denmark combines Europe's most stable housing market with a property system that operates on rules found nowhere else — a covered bond mortgage where the interest rate is set by global investors and cannot be negotiated, a cooperative housing model where selling above the legal price cap is a criminal offence, a dual area measurement system that inflates every listing by 10-15%, a lawyer's reservation clause that saves you 1% of the purchase price but only if you insert it before signing, and a 5-year residency rule that bars most foreigners from buying at all. Each of these has cost expat buyers tens of thousands of kroner because the information existed in Tinglysningsretten rulings, Civilstyrelsen application forms, and Danish-language Reddit threads — but nobody had put it into one system designed for a foreign buyer making their first Danish property purchase.

The Buying Property in Denmark — Expat Guide is a Danish Property Navigation System — not a market overview or a relocation FAQ, but a structured reference that maps every foreign-buyer-specific restriction, financial mechanism, and legal trap in the Danish system into a process you work through before you commit capital. It replaces months of cross-referencing Boligsiden listings, bank advisor meetings, forum posts, and Google-translated legal documents with one resource that tells you exactly what to verify, exactly what the numbers should look like, and exactly where foreign buyers lose money in Denmark.

What's Inside the Danish Property Navigation System

An 11-chapter guide, a 20-item verification checklist, and a 50+ term Danish property glossary — covering every stage from eligibility confirmation to post-purchase tax registration, built specifically for foreign buyers navigating Denmark's unique legal and financial structures:

Foreign Ownership Rules — The 5-Year Rule, EU Exemptions, and the Civilstyrelsen Permit

The Acquisition of Property Act bars most foreigners from buying without five cumulative years of CPR-registered residency. EU/EEA citizens get an exemption — but only for a permanent dwelling, only with a signed declaration under criminal liability, and with a mandatory sell-within-six-months obligation if they leave before five years. Non-EU citizens must apply to the Department of Civil Affairs for each specific property, with a four-week processing time that puts them at a competitive disadvantage against local buyers. The guide maps every pathway — including the domicile assessment criteria the Land Registration Court uses when five years haven't been met.

Ejerlejlighed vs. Andelsbolig — The Trap That Costs Expats the Most

An ejerlejlighed is freehold ownership with full realkredit access and unlimited appreciation. An andelsbolig is a cooperative share with legally capped resale prices, no covered bond financing, higher-rate bank loans, and joint liability for the building's collective debt. The entry price of an andelsbolig looks 30-50% cheaper — but the monthly boligafgift can exceed what you would pay on a freehold apartment twice the purchase price, because it embeds the cooperative's commercial mortgage costs. The guide explains the andelskrone calculation, the maksimalpris formula, how to audit a cooperative's accounts for toxic interest rate swaps, and why browser-translating the association's bylaws is not due diligence.

The Realkreditlån — Denmark's Covered Bond Mortgage System

Danish mortgages are not bank loans. Mortgage credit institutions issue covered bonds matched to your loan — the bond yield is your interest rate, and it is non-negotiable. But the bidragssats (the administration margin layered on top) varies significantly between Nykredit, Realkredit Danmark, Nordea Kredit, and Totalkredit depending on your LTV ratio and loan structure. A 0.2% difference in bidragssats saves tens of thousands of DKK over the life of the loan. The guide covers fixed vs. variable (F1, F3, F5) loans, the callable bond mechanism that lets you buy back your own debt at a discount when rates rise, the bifurcated financing structure (realkredit up to 80% plus a bank loan for the gap), and why expats on the forskerordningen tax scheme lose all mortgage interest deductions.

The Callable Bond — Denmark's Hidden Financial Advantage

Fixed-rate Danish mortgages include a delivery option that exists almost nowhere else in the world. When global interest rates rise, the bonds funding your loan fall below par value. You can buy them back at market price and extinguish a large portion of your remaining debt in a single transaction. The guide explains how this works mechanically, when it makes strategic sense to exercise it, and why it fundamentally changes the risk profile of a fixed-rate loan compared to every other mortgage market.

The Buying Process — From Viewing to Deed Registration

The Danish purchase process operates on contingency clauses and statutory cooling-off periods that have no equivalent in Anglo-American systems. The advokatforbehold (lawyer's reservation) makes your signature conditional on your lawyer's approval — a free exit if problems are found. Without it, your only escape is the statutory six-day cooling-off period, which costs 1% of the purchase price. The guide walks through every step: the salgsopstilling (sales presentation), the tilstandsrapport and elinstallationsrapport (condition and electrical reports), the ejerskifteforsikring (change of ownership insurance and its "wear and tear" exclusion trap), the timeline from accepted offer to Tinglysning (deed registration), and the specific documents your lawyer must review.

BBR Area vs. Tinglyst Area — Why Every Listing Is Bigger Than the Apartment

Danish real estate agents are legally required to advertise using the BBR area — a gross measurement from exterior walls that includes a proportional share of communal stairwells and hallway landings. The tinglyst area recorded on your deed is the actual net living space, typically 10-15% smaller. A "100-square-meter" apartment is usually 85 square meters of usable space. The guide explains both measurement systems, how to find the tinglyst area before making an offer, and how to recalculate your price-per-square-meter on the number that actually matters.

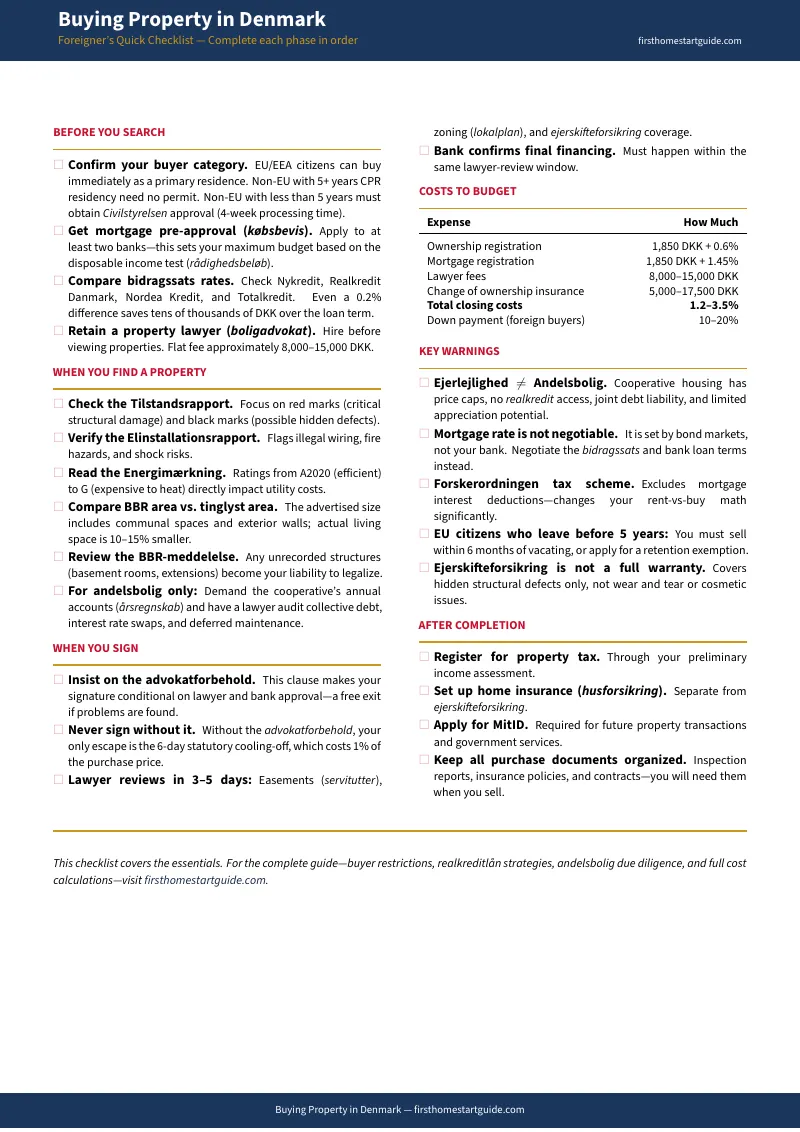

Costs — Everything You Will Actually Pay

Tinglysningsafgift: 1,850 DKK + 0.6% of the purchase price for the deed, plus 1,850 DKK + 1.45% of the mortgage amount for the mortgage registration. Lawyer fees: 8,000-15,000 DKK. Ejerskifteforsikring (your half): 5,000-17,500 DKK. Bank valuation fee. Moving costs. Total closing costs: approximately 1.2% to 3.5% of the purchase price — plus the 10-20% down payment that banks actually require from foreign buyers. The guide breaks down every cost with formulas and worked examples at multiple price points.

Property Taxes — Ejendomsværdiskat, Grundskyld, and the 2024 Reforms

Denmark's dual property tax system charges both a property value tax (ejendomsværdiskat, ~0.51% on the first 9.2 million DKK) and a land tax (grundskyld, varying by municipality). The 2024 reform introduced new market-based valuations that changed many homeowners' tax bills significantly. The guide covers both taxes with calculation examples, the automatic deductions that reduce your liability, the specific implications for foreign buyers, and why expats on the forskerordningen cannot deduct mortgage interest — a detail that fundamentally changes the rent-vs-buy calculation.

Market Overview — Where Foreign Buyers Are Actually Buying

Greater Copenhagen dominates, but the guide maps five distinct markets with current price levels, buyer demographics, and practical considerations: Copenhagen city centre (4,000,000+ DKK apartments, highest competition, lowest inventory), Frederiksberg (premium addresses, family-oriented, international schools nearby), Østerbro and Nørrebro (younger professionals, more inventory, strong transport links), Aarhus (Denmark's second city, university-driven demand, lower entry points), and North Zealand (villas and houses, the Novo Nordisk corridor, car-dependent). Each market is analysed for the specific advantages and risks it presents to foreign buyers.

Rent vs. Buy — The Breakeven Calculation for Expats

The Copenhagen rental market demands massive upfront deposits (three months' rent plus three months' prepaid rent) and monthly costs that frequently exceed equivalent ownership costs once realkredit rates and tax deductions are factored in. But the breakeven horizon depends on transaction costs, expected duration of stay, mortgage structure, and whether you qualify for interest deductions. The guide provides the complete calculation framework with worked examples for a three-year, five-year, and ten-year horizon — including the scenario where forskerordningen eliminates your deductions entirely.

Common Mistakes — The Errors That Cost Expat Buyers the Most

Buying an andelsbolig without auditing the cooperative's debt. Negotiating the bond interest rate instead of the bidragssats. Assuming ejerskifteforsikring covers wear and tear. Signing without the advokatforbehold. Relying on BBR area for value calculations. Failing to get multiple bank quotes because "the bank handles financing for free." Misunderstanding the forskerordningen exclusion. Each mistake is explained with the specific financial consequence and the prevention step.

50+ Danish Property Terms — Glossary

Every Danish term you will encounter in the buying process — from advokatforbehold to årsregnskab — defined in plain English with context for how it affects your purchase. Print it and bring it to every meeting with your bank, lawyer, and estate agent.

Who This Guide Is For

- Expats with permanent contracts in Copenhagen or Aarhus who have decided to buy but need to understand the complete system before engaging a lawyer — the ownership restrictions, the mortgage structure, the cost breakdown, and the specific traps that catch foreign buyers who rely on their bank advisor's reassurance that "everything is standard"

- EU/EEA citizens buying their first Danish property who qualify for the exemption but need to understand exactly what the declaration to the Land Registration Court commits them to — including the six-month sell obligation if they leave before five years

- Non-EU citizens navigating the Civilstyrelsen permit who need to know what documentation to prepare, how long processing takes, and how to structure the purchase agreement to accommodate the four-week delay without losing the property

- Couples debating ejerlejlighed vs. andelsbolig who have seen attractive cooperative prices and need a clear-eyed comparison of total cost of ownership, financing options, appreciation potential, and the specific risks buried in the cooperative's collective debt structure

- Anyone on the forskerordningen (researcher tax scheme) whose rent-vs-buy calculation is fundamentally different because they cannot deduct mortgage interest — and who needs to know exactly how that changes the breakeven horizon before committing to a purchase

Why Free Resources Leave You Exposed

LifeinDenmark.borger.dk outlines the legal framework — the five-year rule, the EU exemption conditions, the sommerhus restrictions. It does not explain the bidragssats, the andelsbolig debt trap, the BBR-vs-tinglyst discrepancy, or the advokatforbehold strategy. It is a government portal designed to state the law, not to help you navigate a 4-million-kroner transaction.

ExpatFinance.dk and similar English-language sites cover the realkredit system in useful detail. But they are structured as article collections, not as a sequential buying process — you read about the callable bond feature without understanding where it fits in your decision timeline, or how it interacts with your expected length of stay and the forskerordningen exclusion.

Reddit (r/dkfinance, r/copenhagen, r/NewToDenmark) and Facebook groups provide real-time anecdotal validation — someone posts their bank's bidragssats offer and asks if it is fair. But crowdsourced advice regularly confuses ejerlejlighed with andelsbolig financing terms, cites pre-2024 tax rules, and cannot replace a structured checklist for the specific sequence of verifications a foreign buyer must complete.

Buyer's agents (Bomae, Købersmægler) provide full-service handholding for 25,000-33,000 DKK. This guide costs less than one hour of a Copenhagen property lawyer's time and gives you the framework to evaluate whether you need a buyer's agent at all — and if you do, to verify their advice against the actual rules rather than trusting a single source.

What You Get

The complete guide, quick checklist, and standalone printable tools — everything you need to verify your purchase before you sign:

- The full Guide (11 chapters) — foreign ownership rules, ejerlejlighed vs. andelsbolig, the realkreditlån system, the buying process, all costs, taxes, market overview, transaction timeline, rent vs. buy calculation, common mistakes, and your action plan

- The Quick Checklist — 20 verification items grouped by purchase phase (Before You Search, When You Find a Property, When You Sign, Costs to Budget, Key Warnings, After Completion) with the specific numbers, thresholds, and decision points for each step

- Danish Property Terms Glossary — 35 essential terms grouped by category (Legal & Process, Financial & Mortgage, Property Types, Taxes, Documents) — print and bring to every meeting

- Transaction Cost Worksheet — fillable worksheet for calculating closing costs, down payment, and annual property costs with Danish-specific line items and formulas

- Purchase Timeline — landscape milestone tracker from pre-approval to deed registration with target and actual date columns — track every step of your 12-16 week purchase

The free checklist covers what to verify at each stage. The full guide covers how — with the legal context, financial calculations, and worked examples that turn each checklist item into an informed decision.

Satisfaction Guarantee

If the guide does not give you a clearer understanding of the Danish property system than everything you have read online combined, email [email protected] and we will make it right.

A single mistake in Denmark — buying an andelsbolig with toxic debt, missing the advokatforbehold, budgeting with BBR area instead of tinglyst area, or failing to compare bidragssats rates — costs more than a full consultation with a property lawyer. The guide costs a fraction of one hour of a Copenhagen boligadvokat's time and covers the complete scope of what you need to know before you hire one.