You've Earned in Dollars for a Decade. The Indian Property System Between You and That Flat in Bengaluru Assumes You Already Know FEMA, TDS, and Form 128.

You've been watching the rupee slide past 90 to the dollar. You've done the math — your tech salary in San Jose or your AED package in Dubai buys a 3BHK in a gated community that would cost three times as much in your host country. Your parents are getting older. The retirement plan is taking shape. You've found a RERA-registered project in Gurugram or a waterfront apartment in Kochi, and the developer's NRI desk is already sending you floor plans and payment schedules. You're ready to wire the money. And then you discover that you can't send it directly from your Chase account to the developer — FEMA requires you to route funds through an NRE or NRO account. That the builder's brochure says "agricultural plot with villa" but NRIs are legally barred from buying agricultural land, plantation properties, or farmhouses. And that the Power of Attorney you planned to give your brother doesn't work unless it's notarized at the Indian Embassy, physically couriered to India, and adjudicated by the local Sub-Registrar — a process that takes weeks, not the "just sign here" your cousin described on a WhatsApp call.

You search online for help. SBI and HDFC publish NRI home loan pages that walk you through interest rates and EMI calculators — written and maintained by banks whose primary goal is to originate your mortgage, not to explain the TDS trap waiting for you when you eventually sell. CA firm blogs publish technically accurate articles on individual topics like Form 128 or the DTAA, but each article covers one regulatory slice in isolation, functions as an SEO lead-generation page for billable consultations at INR 10,000-25,000 per hour, and never integrates the FEMA compliance, tax planning, repatriation mechanics, and home loan strategy into a single actionable sequence. Reddit threads on r/IndiaInvestments and r/NRI contain real stories from real buyers — alongside advice that pre-dates the 2026 Form 128 transition, confuses NRE and NRO repatriation rules, and confidently states that you can claim Section 54 capital gains exemption while living abroad. The rules are more restrictive than that.

Here's the problem no free resource solves: India's NRI property purchase runs through five separate regulatory systems — FEMA governs what you can buy and how you pay, TDS under Section 195 determines how much of your sale proceeds get withheld at source (up to 14.95% of the gross value, not just your profit), the DTAA with your host country determines whether you're taxed twice on the same rental income, Form 15CA/15CB controls whether your bank will actually wire your money back out of India, and RERA is the only tool that lets you verify a developer's legitimacy from 8,000 miles away. Each system has its own forms, its own deadlines, its own penalties for non-compliance, and its own set of professionals who handle only their slice. No one connects them into a single transaction roadmap. The NRI who doesn't understand how these five systems interact doesn't just risk overpaying — they risk having lakhs of rupees trapped in India for months while they wait for a refund on TDS that was deducted on the gross sale value instead of the actual capital gain.

The Buying Property in India — NRI/OCI Guide is The Cross-Border Compliance Decoder. Not a bank's mortgage brochure or a CA's lead-generation article. It's a structured decision system that decodes every stage of the NRI property purchase — from opening the right NRE/NRO/FCNR account through FEMA-compliant fund routing, RERA developer verification, the sale agreement, stamp duty payment, Sub-Registrar registration, rental yield taxation, and eventual repatriation of proceeds — so you make each decision understanding the regulation behind it, the form that governs it, and the financial consequence of getting it wrong.

What's Inside The Cross-Border Compliance Decoder

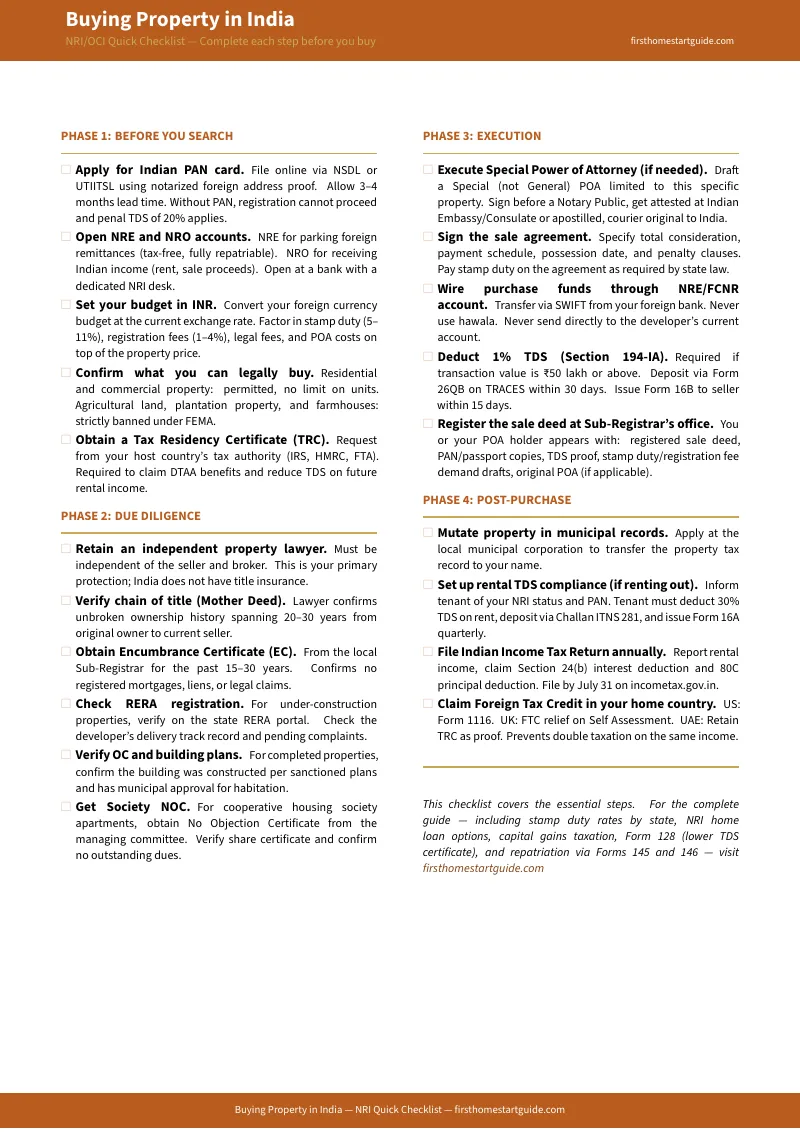

The complete guide plus 11 standalone printable references — covering every stage from NRE account setup through capital repatriation, with the FEMA provisions, Income Tax sections, TDS rates, DTAA articles, and RBI circulars that determine whether your transaction succeeds or your capital gets trapped. Print the standalone cards and take them to bank appointments, CA consultations, and Sub-Registrar visits:

FEMA Compliance Navigator

FEMA regulations under the Reserve Bank of India govern every rupee flowing in and out of your property transaction — and the most expensive mistakes happen before you've even seen a property. NRIs can freely purchase residential and commercial properties without RBI approval, but are absolutely barred from acquiring agricultural land, plantation properties, or farmhouses under Schedule IV of the Foreign Exchange Management (Non-Debt Instruments) Rules, 2019. The guide maps the three NRI banking channels: NRE accounts (fully repatriable, tax-exempt interest), NRO accounts (for Indian-sourced income like rent, with strict repatriation limits), and FCNR deposits (held in foreign currency for exchange-rate hedging). It covers the compliant fund routing sequence — foreign bank → NRE/NRO account → developer — because a direct wire from your Chase or Barclays account to a builder's local account is non-compliant and invites regulatory scrutiny. Cost of fixing a FEMA violation: months of CA consultations and potential RBI penalties. Cost of getting it right the first time: reading Chapter 3.

TDS & Capital Gains Decoder — Including Form 128

The single most paralyzing financial trap for NRI property owners, and the one that every bank and developer conveniently omits from their marketing. When you eventually sell your Indian property, the buyer must deduct TDS under Section 195 — not on your profit, but on the entire sale consideration. Sell a flat for INR 5 Crore that you bought for INR 4.5 Crore, and your actual gain is INR 50 Lakh. But the buyer is legally mandated to deduct up to 14.95% on the full INR 5 Crore — nearly INR 75 Lakh withheld when your actual tax liability is a fraction of that. Without intervention, you file an ITR and wait months or years for a refund. The guide explains the solution: the new Form 128 (which replaced Form 13 in April 2026), filed through the TRACES portal, which gets an Assessing Officer to certify your actual tax liability so the buyer deducts TDS at the correct lower rate. It also covers the 2026 Budget reform that abolished the TAN requirement for resident buyers — they now use PAN-based challans, removing a compliance barrier that previously froze NRI secondary market transactions. Plus: the removal of indexation benefits, the 12.5% LTCG base rate for properties held over 24 months, and the STCG slab-rate exposure for shorter holdings.

Repatriation Playbook — Form 15CA & 15CB

The question that keeps every NRI investor awake at 2 AM in their timezone: "If I put INR 2 Crore into Indian real estate, can I actually get it back out?" The answer is yes — but only if you follow the RBI's bureaucratic wire-transfer protocol exactly. Sale proceeds and accumulated rental income sit in your NRO account, which permits repatriation of up to USD 1 million per financial year under the Liberalised Remittance Scheme. But the Authorized Dealer bank will not process the outward remittance without Form 15CB — a certificate issued by a practicing Indian Chartered Accountant confirming the source of funds, full tax compliance, and applicable DTAA provisions. Then you file Form 15CA (Part C for amounts over INR 5 Lakh) on the Income Tax e-filing portal as your formal declaration. Only with both the 15CA acknowledgment and the 15CB certificate will the bank release the international wire. The guide covers the full documentation chain, the CA engagement process, the penalty structure (INR 1 Lakh per form for incorrect submission), and the timeline from NRO account to your foreign bank.

DTAA Shield — Eliminating Double Taxation on Rental Income

If you're buying for rental yield, Indian tax law hits you immediately: your tenant must deduct TDS at 31.2% (30% base plus 4% health and education cess) from the first rupee of rent — no threshold exemption. On a monthly rent of INR 1,00,000, that's INR 31,200 withheld before you see a paisa. And then the IRS, HMRC, or CRA may tax the same income again in your country of residence. India has signed DTAAs with over 90 nations to prevent this. The guide explains how to obtain a Tax Residency Certificate from your host country's tax authority, submit it with Form 10F to your Indian tenant, invoke treaty provisions to reduce the withholding rate (to 15% under the India-US DTAA, for example), and then claim Foreign Tax Credits in your home-country filing to offset the Indian tax already paid — eliminating double taxation entirely. The chapter covers treaty mechanics for the five major NRI corridors: US, UK, Canada, UAE, and Singapore.

Power of Attorney Protocol

You're in California or Dubai. The Sub-Registrar's office is in Pune. Someone has to sign the sale deed in person. The legal mechanism is a Special Power of Attorney — drafted to grant exact, limited powers for one specific property transaction, not the sweeping General PoA that your well-meaning uncle is suggesting. The guide covers the four-step execution sequence: drafting with precise property and transaction details, mandatory notarization at the Indian Embassy or Consulate in your country of residence, physical courier of the original attested document to India, and local adjudication and stamping by the District Registrar (stamp duty rates vary by state). It explains why a General PoA is dangerous, how to structure revocation clauses, and the specific powers to include or exclude so your representative can execute the deed without being able to sell or mortgage the property independently.

NRI Home Loan Comparison Engine

Leveraged buying is standard NRI financial engineering — preserve your foreign currency buffer while deploying Indian bank capital at 7.15%-8.70% interest rates. The guide compares current offerings from SBI, HDFC, ICICI, and Bajaj Housing Finance across four dimensions: interest rate bands, loan-to-value ratios (typically 75-80% for NRIs vs. 80-90% for residents), maximum tenure, and the strict NRE/NRO/FCNR repayment channel requirements. It covers eligibility criteria (valid passport, OCI/PIO status, 1-3 years continuous overseas employment, active NRI banking relationship), the Section 80C and 24(b) tax deductions available on principal and interest, and the documentation package required. No bank comparison site gives you this alongside the FEMA routing rules and TDS implications — because they're selling you the mortgage, not the complete financial picture.

RERA Remote Verification System

The fear of investing in a stalled or fraudulent project from 8,000 miles away is legitimate — and RERA is the mechanism that solves it, if you know how to use it. The guide walks through the state-specific RERA portal audit process: verifying project registration status, reviewing developer financial disclosures, checking for pending litigations or complaints, and confirming construction progress against promised timelines. It covers MahaRERA (Maharashtra), UP-RERA, HRERA (Haryana/Gurugram), and K-RERA (Karnataka/Bengaluru) — the four portals that matter for NRI buyers targeting tier-1 cities. Plus: how to cross-reference marketing brochures with hard RERA data, what the Occupation Certificate and Completion Certificate mean for your possession timeline, and the complaint mechanism if your developer defaults.

State-by-State Stamp Duty & Registration Calculator

Stamp duty in India is not one number — it varies dramatically by state, buyer category, and property type. Maharashtra charges 5% plus a 1% metro surcharge in Mumbai. Delhi ranges from 4-6% depending on gender. Karnataka offers a 2% reduction for women buyers. The guide includes a state-by-state breakdown for the top NRI destination states — Maharashtra, Delhi NCR, Karnataka, Telangana, Tamil Nadu, and Kerala — covering base rates, surcharges, registration fees (typically 1%), the TDS obligation on purchases over INR 50 Lakh, the circle rate (ready reckoner rate) vs. market value distinction, and the penalty structure for underdeclaration. Understanding these costs before you negotiate the purchase price — not after — is the difference between budgeting accurately and discovering a 6-figure shortfall at the Sub-Registrar's office.

Who This Guide Is For

This guide is for NRIs and OCIs buying property in India from abroad who:

- Are buying their first Indian property and need the entire cross-border transaction mapped — from NRE/NRO account setup through FEMA-compliant fund routing, RERA developer verification, sale agreement, stamp duty, Sub-Registrar registration, and ongoing rental management — so they understand what happens at each stage, which regulation governs it, and what the penalty is for non-compliance

- Are based in the US and need to understand how the IRS's worldwide-income taxation interacts with Indian TDS, how to claim Foreign Tax Credits under the India-US DTAA, and how RSU vesting and bonus deployment strategies affect their Indian investment structure

- Are based in the UAE and need to maintain their Tax Residency Certificate to shield their Indian assets from domestic taxation, while treating Indian real estate as the mandatory repatriation fallback that their fragile employment-tied visa status demands

- Are based in the UK, Canada, Australia, or Singapore and need the specific DTAA mechanics, repatriation protocols, and home-country tax credit strategies that apply to their corridor

- Want to buy for rental yield and need to understand the 31.2% TDS on rent, the DTAA-based reduction mechanism, the Tax Residency Certificate and Form 10F process, and the net yield calculation after Indian and home-country taxes

- Are buying for aging parents and need to navigate the gated community, senior living, and medical proximity considerations alongside the FEMA and registration mechanics

- Plan to sell eventually and need to understand the Form 128 process, the 12.5% LTCG rate, the removed indexation benefit, the PAN-based challan reform, and the full 15CA/15CB repatriation chain before they buy — not when they're scrambling to extract capital

- Need to appoint a representative in India and want a properly structured Special Power of Attorney with limited powers, Embassy notarization, and state-specific adjudication — not the General PoA that exposes them to unauthorized transactions

- Want every FEMA provision, every Income Tax section, every TDS rate, every DTAA article, every RBI circular, and every state stamp duty rate in one document — so they walk into NRI banking appointments, CA consultations, and Sub-Registrar offices with the same structural understanding as someone who's done this three times before

Why Not Free Resources?

Free information on NRI property buying is abundant. Here's what each source actually delivers:

- Bank NRI desks (SBI, HDFC, ICICI) publish comprehensive home loan pages with interest rate tables, EMI calculators, and eligibility criteria — maintained by institutions whose revenue comes from originating your mortgage. The loan comparison data is accurate and current. What they don't cover: the TDS withholding trap on future sales, the Form 128 mechanism to prevent gross-value deduction, the 15CA/15CB repatriation protocol, or the DTAA strategies that determine your actual net rental yield. You get excellent top-of-funnel mortgage marketing designed to capture your home loan application, not to protect your cross-border tax position.

- CA and law firm blogs (ClearTax, Tax2win, NCA Agrawal) publish technically precise articles on individual topics — Form 128, DTAA provisions, Section 195 TDS. Each article is accurate in isolation and functions as an SEO lead-generation page for consultations at INR 10,000-25,000 per hour. What they don't provide: a single integrated roadmap that connects FEMA fund routing, TDS planning, DTAA treaty invocation, NRI banking channels, RERA verification, and repatriation mechanics into one actionable sequence. You get expert fragments designed to demonstrate competence, not to replace it.

- Reddit and community forums (r/IndiaInvestments, r/NRI, NRI Money Clinic on YouTube) contain genuine experiences from diaspora buyers — alongside advice that pre-dates the April 2026 Form 128 transition, confuses NRE and NRO repatriation rules, recommends routing funds through relatives' accounts ("it'll be fine"), and claims that Section 54 capital gains exemption works identically for NRIs and residents. Some of these people closed smoothly. Some of them have INR 75 Lakh trapped in a TDS refund cycle. Both stories are true. Neither tells you which outcome applies to your transaction.

- Developer NRI sales desks offer dedicated relationship managers, virtual tours, and "NRI-friendly payment plans" — funded by the 2-3% brokerage commission built into your purchase price. The good ones handle registration logistics smoothly. But their incentive is to close the sale this quarter, not to optimize your TDS position for a sale five years from now, structure your PoA to limit your representative's authority, or ensure your rental income is treaty-protected from double taxation.

This guide fills the structural gap — the space between knowing that NRIs can buy property in India and understanding exactly how the five regulatory systems interact at each stage, what form governs each step, what the deadline is, and what the financial penalty is for missing it. It's the analysis an independent cross-border advisor with no mortgage to originate and no commission to earn would give you, structured as a permanent reference you own.

— Less Than One Hour of an NRI Tax Consultant's Time

A Chartered Accountant specializing in NRI taxation charges INR 10,000-25,000 per consultation. A property lawyer's retainer for a single transaction starts at INR 50,000. The TDS deducted on the gross sale value of an INR 5 Crore property — instead of on the actual capital gain — is nearly INR 75 Lakh trapped in the refund cycle. A single FEMA-non-compliant fund transfer can trigger RBI scrutiny and months of remediation.

This guide doesn't replace your CA or your property lawyer. But it gives you the FEMA compliance navigator, the TDS decoder with Form 128 strategy, the DTAA shield for rental income, the repatriation playbook, the PoA protocol, and the state-by-state stamp duty calculator that ensure you walk into every bank appointment, every CA consultation, and every Sub-Registrar office understanding the regulatory mechanism behind each step — instead of discovering how India's cross-border property system works by leaving lakhs on the table.

If it prevents a single gross-value TDS deduction by guiding you to file Form 128, catches a single FEMA routing violation before you wire funds, or identifies the DTAA provision that halves your rental income withholding, it pays for itself before you've finished reading it.

30-day money-back guarantee. If the guide doesn't make the NRI property transaction clearer and your cross-border tax position stronger, you pay nothing.

Download the free NRI Quick Checklist to see the step-by-step action plan covering NRE/NRO account setup, FEMA compliance, RERA verification, TDS planning, and the repatriation timeline. When you're ready for the full Cross-Border Compliance Decoder — complete with the Form 128 strategy, DTAA shield, PoA protocol, home loan comparison, and state-by-state stamp duty calculator — the complete guide is here.

You've earned the money abroad. Now decode the regulatory system that stands between you and putting it to work in India.