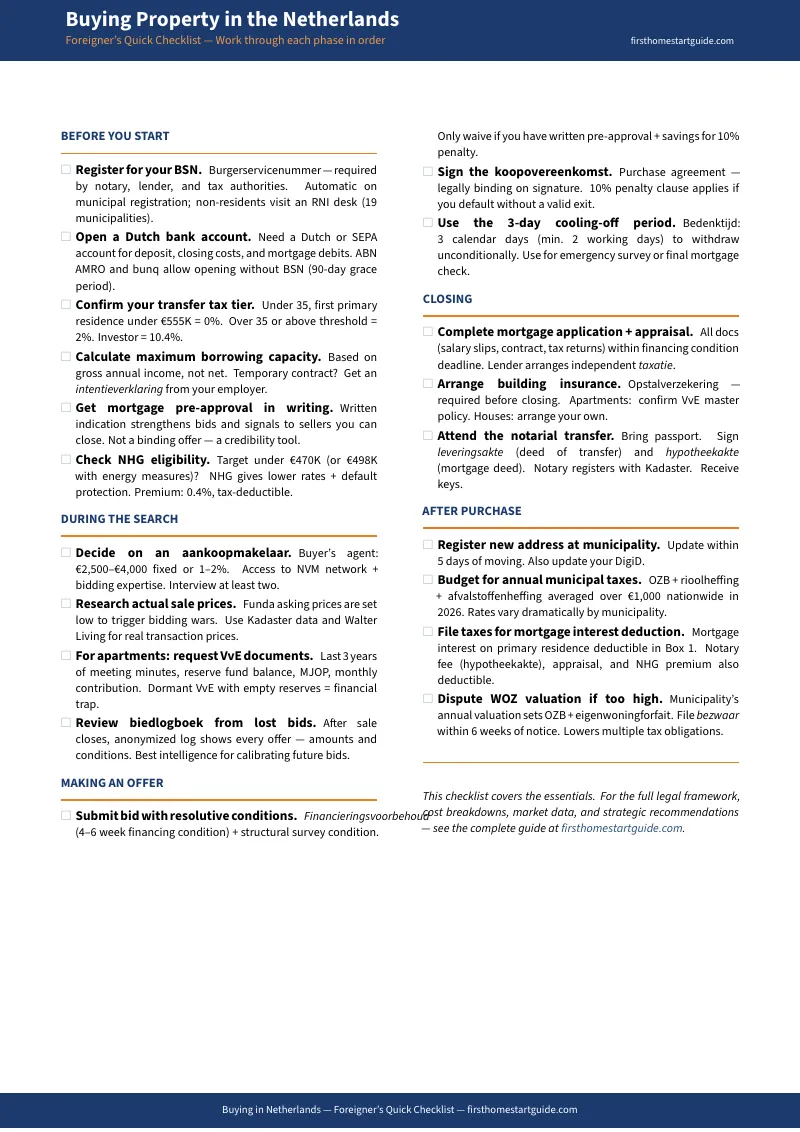

You've Read Every IamExpat Article. You've Browsed Funda for Months. You Still Don't Know Why Your 30% Ruling Barely Moves Your Mortgage, What the Biedlogboek Reveals About Your Lost Bids, or Whether That Apartment's VvE Is About to Collapse.

You're earning €80,000 at a tech company in Eindhoven, or €120,000 at a bank in Amsterdam, or €65,000 at an NGO in The Hague. You've been paying €2,000 a month in rent — €72,000 over three years gone with nothing to show for it. You've watched Funda listings vanish within days. You've run the mortgage calculator on Hypotheek.nl and it gave you a number, but you don't know if that number accounts for your 30% ruling, your temporary contract, or the fact that your employer hasn't given you a permanent one yet. You've asked your Dutch colleagues for help and they said "just get an aankoopmakelaar" — but they couldn't explain what blind bidding actually means, why the asking price is designed to mislead you, or how the biedlogboek works after you lose your seventh consecutive bid.

You searched online for answers. IamExpat published a high-level overview that tells you mortgages exist and lists three types of transfer tax — but doesn't explain that the €555,000 starter threshold is absolute (one euro above it and you lose the entire exemption), or that the 0% rate is a one-time lifetime opportunity you can't reclaim. Expatica's mortgage page compares interest rates across banks — because Expatica is an advertising platform for mortgage brokers, not an educational resource. Reddit threads on r/Netherlands and r/Amsterdam contain real stories from real expats alongside advice that confuses gross and net underwriting, incorrectly claims the 30% ruling doubles your borrowing capacity, and recommends waiving the financing condition "because everyone does it" without mentioning the 10% purchase price penalty if your mortgage falls through.

Here's the problem no free resource solves: The Dutch property system runs through five separate mechanisms that expat-targeted content covers individually but never connects. The mortgage underwriting system evaluates your income differently than you expect — based on gross salary, making the 30% ruling nearly irrelevant for borrowing capacity. The blind-bidding system uses asking prices as psychological bait, not valuation anchors. The three-tier transfer tax system has an absolute €555,000 cliff that costs first-time buyers thousands if they miscalculate by a single euro. The VvE system makes every apartment purchase contingent on whether strangers in your building have been funding their maintenance reserves — and half of Dutch VvEs haven't. And the Box 1/Box 3 tax structure means your primary residence is a tax shelter that shields capital from a 36% assumed-return wealth tax, but only if you understand the mechanics before your 30% ruling expires. No single English-language guide integrates all five into a coherent buying sequence. The expat who doesn't understand how these systems interact doesn't just risk overpaying — they risk losing €40,000 in unnecessary transfer tax, getting locked into an apartment above a dormant VvE, or watching their global wealth get taxed at 6% assumed returns the day their ruling expires.

The Buying Property in the Netherlands — Expat Guide is The Dutch Property Decoder. Not a mortgage broker's lead-generation page or a relocation company's overview. It's a structured decision system that decodes every stage of the expat property purchase — from BSN registration and bank account setup through mortgage pre-approval, bidding strategy, koopovereenkomst negotiation, VvE health checks, notarial transfer, and post-purchase tax optimization — so you make each decision understanding the regulation behind it, the institution that governs it, and the financial consequence of getting it wrong.

What's Inside The Dutch Property Decoder

The complete guide plus 7 standalone printable tools — covering every stage from BSN registration to your first OZB bill, with the exact 2025/2026 figures, institution names, lender requirements, and tax thresholds that determine whether your transaction succeeds or your deposit gets trapped. Print the standalone tools and bring them to mortgage advisor appointments, property viewings, and notary sessions:

Dutch Mortgage Eligibility for Expats

Dutch mortgage underwriting is where most expats hit their first wall — and where the gap between what broker websites tell you and what actually happens at the bank is widest. The guide maps the exact eligibility criteria bank by bank: ABN AMRO and ING accept applications from day one with a highly skilled migrant visa; NIBC requires six months of documented Dutch employment; ASN Bank demands three years of continuous residency. For temporary contract holders, the intentieverklaring — a formal letter from your employer stating intent to offer a permanent contract — functions as a permanent contract for underwriting purposes. For flex workers who can't get an intentieverklaring, the arbeidsmarktscan (€125 algorithmic assessment of future earning capacity) can unlock NHG mortgage approval. For ZZP self-employed expats, most banks require three consecutive years of Dutch financial history, using an average of net profits. The guide also solves the banking paradox: you need a Dutch address to open a bank account but need a bank account to buy the home. ABN AMRO and bunq both offer a 90-day BSN grace period that breaks the deadlock.

The 30% Ruling — What It Actually Means for Your Mortgage

The most common misconception among highly skilled migrants, and the one every expat mortgage broker is incentivized to avoid correcting until the application is submitted. Dutch banks calculate maximum borrowing capacity based on gross annual income — not net income. Since the 30% ruling increases your net pay without changing your gross salary, it provides almost no advantage in securing a larger loan. Some progressive lenders do factor the ruling into their capacity algorithms, but conservative institutions either discount its value or ignore it entirely. The strategic question isn't whether the ruling helps your mortgage — it barely does. The strategic question is timing: the ruling tapers to 27% in 2027, the €262,000 annual income cap took effect in 2026, and the loss of partial non-resident Box 3 exemption means your global savings and investments will suddenly face an assumed return tax of up to 6% at a 36% rate. Buying before your ruling expires can lock capital into the tax-sheltered Box 1 environment. The guide models the exact scenarios.

NHG (Nationale Hypotheek Garantie) 2026 Strategy

The NHG is a state-backed mortgage guarantee that eliminates the bank's default risk — meaning NHG-backed mortgages carry interest rates 0.15% to 0.6% lower than non-guaranteed loans. That's a saving of €150 to €600 per year for every €100,000 borrowed. In 2026, the standard NHG limit is €470,000 (up from €450,000 in 2025), extending to €498,200 if you finance energy-saving measures like solar panels, heat pumps, or advanced insulation. The one-time premium is 0.4% of the mortgage amount, and it's tax-deductible in Box 1. Expats with valid residence permits and euro-denominated income are fully eligible. The strategic implication: properties priced between €420,000 and €470,000 attract the most ferocious bidding wars, because every domestic first-time buyer is stretching their offer to the NHG ceiling. Understanding where your target property sits relative to the NHG limit determines your bidding strategy.

Overdrachtsbelasting — The Three-Tier Transfer Tax

The Dutch government uses transfer tax as a policy lever — subsidizing young first-time buyers while punishing speculative investors. Buyers under 35 purchasing a primary residence up to €555,000 in 2026 pay 0%. Buyers 35 or older, or buying above the threshold, pay 2% on the full purchase price. Investors, buy-to-let purchasers, and parents buying for children pay 10.4%. The trap: the €555,000 threshold is absolute. A property valued at €555,001 doesn't cost you 2% on the €1 excess — it costs you 2% on the entire €555,001, which is €11,100 in transfer tax instead of zero. The exemption is also one-time and must be formally declared at the notary. Expats qualify regardless of nationality, as long as the property is their primary residence. The guide includes a transfer tax decision tree that maps your age, property value, and purchase intent to the correct rate.

The Blind Bidding System and Biedlogboek Intelligence

The single most traumatic experience for expat buyers, and the one where informational asymmetry does the most damage. The vraagprijs (asking price) on Funda.nl is set artificially low to trigger a bidding war — in Amsterdam, 71% of properties sell above asking price. Bids are submitted blind; you cannot see competing offers. The breakthrough tool is the biedlogboek (digital bidding logbook): after every sale, the selling agent must publish an anonymized log of all bids received, including amounts and conditions. This post-sale data is the single most valuable intelligence you can gather before your next bid. The guide explains how to systematically analyze biedlogboek data from comparable properties, how to calculate the overbidding premium for your target neighborhood, and the critical trade-off between waiving resolutive conditions (which makes your bid more competitive) and retaining the financing condition (which protects you from a 10% purchase price penalty if your mortgage is denied). It also provides an objective analysis of whether hiring an aankoopmakelaar (buyer's agent) at €2,500 to €4,000 is worth the cost, based on their NVM network access and pre-market listing visibility.

VvE Health Check System

If you're buying an apartment, the Vereniging van Eigenaars (homeowners' association) matters more than the physical inspection. Half of Dutch VvEs cannot fund their own maintenance reserves. A dormant (slapende) VvE with empty reserves means one catastrophic roof failure or foundation problem triggers an emergency assessment of tens of thousands of euros per owner. Mortgage lenders scrutinize VvE health during underwriting — a poorly managed VvE can result in immediate mortgage rejection. The guide includes a seven-point VvE due diligence checklist: KvK registration verification, MJOP (Multi-Year Maintenance Plan) audit, reserve fund adequacy check against the 0.5% rebuild value statutory minimum, insurance coverage review, meeting minutes analysis (looking for deferred maintenance, inter-neighbor conflicts, and unpaid debts), monthly contribution benchmarking (€161 average for a 70 sq m apartment in 2026), and professional management status. Complete this checklist before making any offer on any apartment.

Box 1 vs Box 3 Tax Strategy

The most sophisticated strategic decision in the Dutch expat property landscape, and the one that no mortgage broker website covers because it's not their business. Your primary residence sits in Box 1 — the eigenwoningforfait (0.35% of WOZ value) is added to taxable income but heavily offset by the hypotheekrenteaftrek (mortgage interest deduction). Your savings and investments sit in Box 3, where the government taxes an assumed return (6% for investments in 2026) at a flat 36% rate — regardless of your actual returns. While you hold the 30% ruling, you enjoy partial non-resident status that exempts global assets from Box 3. When the ruling expires, every euro in savings and investments becomes suddenly visible. The strategic play: converting taxable Box 3 assets (stock portfolios, savings) into a Dutch primary residence (Box 1) before the ruling's expiration. The guide models this transition with worked financial examples showing the exact tax savings.

Who This Guide Is For

This guide is for expats and foreign professionals buying property in the Netherlands who:

- Are highly skilled migrants on the 30% ruling who need to understand that Dutch banks use gross income for mortgage calculations — and need to plan their purchase timing strategically before the 2027 taper to 27% eliminates their Box 3 exemption and exposes their global wealth to assumed-return taxation

- Hold a temporary or flex contract and have been told by banks that they cannot get a mortgage — and don't know that the intentieverklaring from their employer or a €125 arbeidsmarktscan can unlock NHG mortgage approval

- Have lost multiple bids and feel completely shut out of the market — and need to understand the blind-bidding system, how to use biedlogboek data from comparable sales, and when waiving the financing condition is a calculated risk versus financial recklessness

- Are buying an apartment and have no idea how to evaluate a VvE — whether the association's reserves are adequate, whether the MJOP is current, or whether they're about to inherit a dormant VvE that will hit them with a five-figure emergency assessment within their first year

- Are part of a bi-national couple (one Dutch, one foreign partner) where the foreign partner needs to fully understand the financial and legal process — especially when mortgage documents, VvE meetings, and notary deeds are conducted entirely in Dutch

- Are non-EU professionals (American, British, Indian, post-Brexit) navigating the intersection of visa status, BSN registration, and Dutch banking — and need to know exactly which lenders accept their employment profile, how the RNI registration changes in 2026 affect their timeline, and whether buying property grants residency (it doesn't)

- Are weighing rent vs. buy for a 3-5 year stay and need the actual break-even math — sunk rental costs vs. closing costs vs. capital appreciation vs. Box 1 tax shelter benefit — not "it depends" advice from a forum thread

— Less Than One Month's Parking Space Rent in Amsterdam

An aankoopmakelaar charges €2,500 to €4,000. A single mortgage advisory session costs €500 to €800. Missing the €555,000 transfer tax threshold by one euro costs you €11,100 in unnecessary tax. Losing a bid because you didn't understand the biedlogboek costs you months of additional rent at €2,000+ per month. A dormant VvE emergency assessment costs tens of thousands.

The guide costs a fraction of any single mistake it prevents. Download tonight, start your mortgage pre-approval process tomorrow.

Why Not Free Resources?

IamExpat and Expatica provide high-level overviews that tell you mortgages exist and transfer tax has three tiers. They don't explain the absolute €555,000 cliff, the arbeidsmarktscan mechanism, the biedlogboek analytics, or the Box 1 vs Box 3 tax strategy. Their content is structurally limited by the advertising model — they exist to drive clicks to mortgage broker advertisements, not to provide the forensic depth required by a buyer committing €400,000+ to a Dutch asset.

Mortgage broker websites (Expat Mortgages, A&O Finance, Hypotheek Visie) publish technically accurate content about interest rates and maximum borrowing capacity — because they want to originate your loan. They will not teach you how to evaluate a VvE, debate the strategic timing of buying before your 30% ruling expires, or explain why waiving the financing condition on your seventh bid is a gamble that could cost you 10% of the purchase price. They're selling financing, not market literacy.

Reddit threads and Facebook groups contain real stories from real expats — alongside advice that confuses NHG limits from different years, incorrectly claims the 30% ruling doubles mortgage capacity, and recommends waiving conditions "because everyone does it" without understanding that a failed unconditional purchase triggers a penalty equal to the price of a luxury car.

This guide connects the mortgage system, the bidding system, the tax system, the VvE system, and the regulatory system into one coherent decision framework — with the exact 2025/2026 figures, institution names, and strategic trade-offs that determine whether you buy successfully or burn through €50,000+ in avoidable costs.

Download the free checklist to get the 20-step buying sequence. Get the full guide to understand every regulation, every institution, every financial trap, and every strategic opportunity in the Dutch property market — before you submit your first bid.