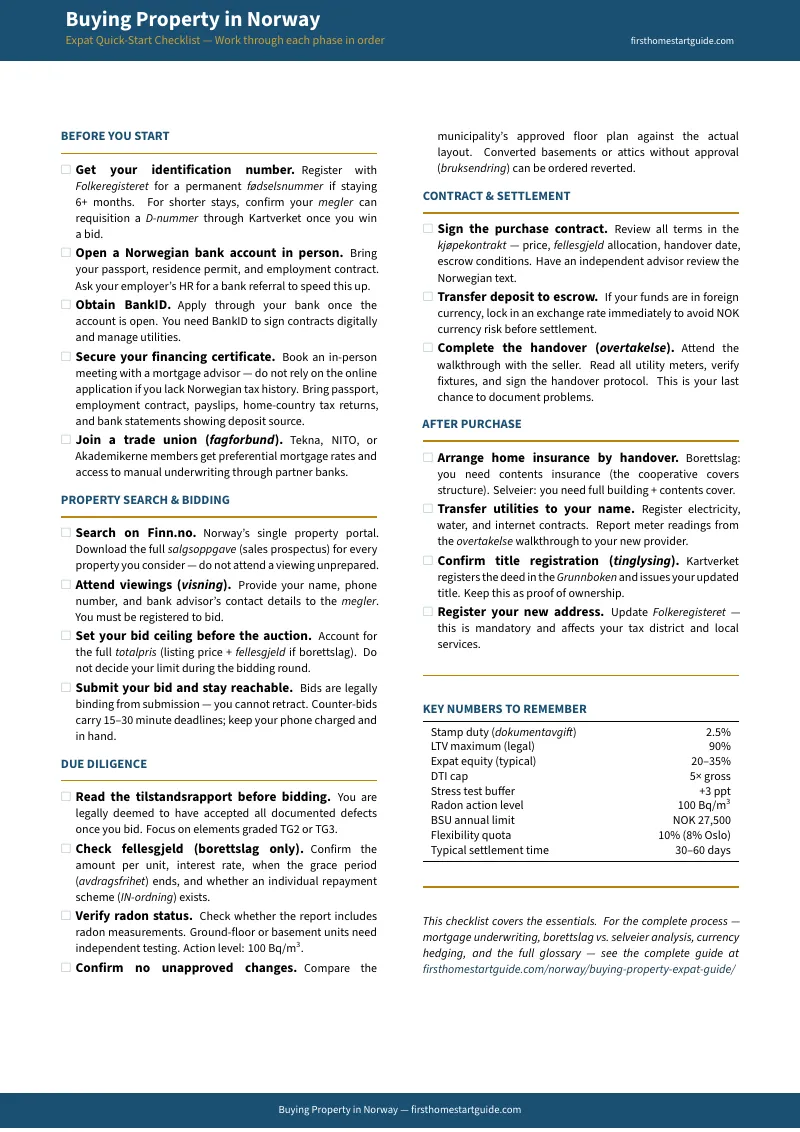

You Found a Two-Bedroom Apartment on Finn.no for NOK 3,500,000. Nobody Explained the NOK 800,000 in Hidden Fellesgjeld, the Legally Binding Bid You Cannot Withdraw, or Why Your Bank Rejected Your Mortgage Before a Human Even Looked at It.

You have scrolled through hundreds of Finn.no listings in Oslo, Bergen, and Stavanger. You have converted NOK to your home currency and decided the numbers finally make sense. You have read the Life in Norway blog post about buying a house and come away with a rough sense of the steps involved. And you have probably assumed that because Norway has no legal restrictions on foreigners buying property, the rest of the process must be straightforward.

It is not. Norway layers a legally binding auction system where a single SMS constitutes an irrevocable contract, two entirely different ownership structures with different tax obligations and subletting rights, a cooperative housing model that hides hundreds of thousands of kroner in shared debt behind a low purchase price, banks that automatically reject mortgage applications from anyone without a Norwegian tax assessment history, a mandatory technical inspection report written in Norwegian that you are legally deemed to have read and understood before bidding, and a property transfer system that runs entirely through the estate agent with no independent solicitor protecting your interests. The Life in Norway article does not cover any of this in operational detail. The megler's brochure skips the parts that would slow down a sale. The Reddit threads about mortgages as a foreigner are a mix of outdated advice and contradictory experiences with no way to tell which applies to your visa type.

The core problem: Norway's property market is one of the most digitised and transparent in Europe — but every English-language resource covers one fragment without connecting it to the rest. There is no single resource that explains how fellesgjeld changes the true cost of a borettslag apartment, how to navigate the budrunde without making a legally binding mistake, how to get a Norwegian mortgage when automated credit systems reject you on sight, how to decode a tilstandsrapport written for Norwegian building standards, or how your visa type and residency horizon should determine whether you buy freehold or cooperative. Until now.

The Buying Property in Norway — Expat Guide is the Norway Property Acquisition System — a structured decision framework that connects every ownership structure, financing pathway, bidding mechanic, and technical due diligence step into a single English-language roadmap from finansieringsbevis through overtakelse.

What's Inside the Norway Property Acquisition System

The complete 63-page guide, seven standalone printable tools, and a quick-start checklist — covering every stage from securing your financing certificate through collecting the keys, with the decision frameworks and worked examples you need to navigate the fastest property market in Scandinavia:

Borettslag vs. Selveier Decision Framework

The ownership choice that determines your tax bill, your subletting rights, and your total acquisition cost. Norway has two fundamentally different ownership structures, and choosing the wrong one for your situation can cost you hundreds of thousands of kroner or lock you out of renting your property when you leave. Selveier (freehold) gives you full ownership registered in the land registry, unrestricted subletting rights, and complete autonomy — but imposes a 2.5% dokumentavgift on the full purchase price, payable upfront in cash. Borettslag (cooperative) exempts you from that tax entirely but saddles you with shared joint debt (fellesgjeld) that can double the true acquisition cost, restricts subletting to two or three years with board approval, and exposes you to monthly cost increases when interest-only grace periods expire. The guide maps both structures against your residency horizon, visa type, and exit strategy so you choose the model that matches your actual timeline — not the one with the lowest sticker price on Finn.no.

Fellesgjeld Risk Calculator

The hidden debt that makes a NOK 2,000,000 apartment actually cost NOK 3,500,000. When a cooperative lists a low purchase price (innskudd), the price you see on Finn.no is only the equity portion. The fellesgjeld — the building's collective mortgage allocated to your unit — sits in the salgsoppgave, often buried in the financial details. The guide teaches you to calculate the total acquisition cost (innskudd plus your share of fellesgjeld), evaluate whether the cooperative has an IN-ordning that lets you pay down your share, identify cooperatives still in interest-only grace periods where monthly costs will spike when amortisation begins, and stress-test your monthly felleskostnader against interest rate increases — the same increases that caught thousands of Norwegian buyers off guard after 2022.

Expat Mortgage Strategy

Why your bank rejected you automatically — and how to get approved through manual underwriting. Norway's automated credit systems rely on registered tax assessments from Skatteetaten. If you have lived in Norway for less than 12 to 18 months, you do not appear in these registers. Your application is rejected before a human reviews it — even if you earn NOK 1,000,000 and hold a permanent employment contract. The guide walks through the manual underwriting pathway: which documents to prepare (employment contract, payslips, home-country tax returns, proof of deposit origin for AML compliance), how joining a professional trade union like Tekna or NITO gives you access to preferential rates and manual risk assessment through collective agreements, the realistic equity requirements banks impose on different visa categories (10% legal minimum versus the 20% to 35% actually demanded of temporary residents), and how to secure your finansieringsbevis before you start searching.

Budrunde Bidding System

How to compete in a transparent auction where every bid is legally binding and there is no cooling-off period. Norwegian property bidding is nothing like what you have experienced in other countries. There is no "subject to contract" phase. There is no private negotiation. There is a single viewing, usually one hour on a Sunday, followed by an SMS-driven auction the next morning where the agent broadcasts every bid to every participant in real time. Your bid — submitted by text message, email, or the agent's portal — becomes a binding contract the moment the seller accepts it. Walk away and you are liable for the difference if the property resells for less. The guide covers the regulatory timeline (minimum acceptance windows, initial bid deadlines), how to set a hard ceiling before the adrenaline starts, how to read the salgsoppgave to identify risks before you bid, and the verification call your bank advisor will receive from the megler to confirm your financing is real.

Tilstandsrapport Decoder

How to read a Norwegian technical inspection report and spot the red flags that cost NOK 150,000 to NOK 300,000. Under the 2022 amendments to the Avhendingsloven, you are legally deemed to have read and accepted the tilstandsrapport before you bid. This report uses a standardised condition grading system (TG0 through TG3) that is entirely unfamiliar to foreign buyers. The guide explains what each grade means, which elements to focus on (wet-room membrane age, drainage integrity, radon levels, unapproved structural conversions), the NOK 10,000 statutory deductible for post-purchase defect claims, and the specific red flags in Norwegian construction — including bathroom membranes rated TG2 or TG3 (NOK 150,000 to NOK 300,000 renovation), foundation drainage failures, radon concentrations above DSA action levels, and basement conversions completed without bruksendring approval that the municipality can order you to revert.

D-nummer and BankID Navigation

The administrative deadlock that can stall your purchase for months. You need a D-nummer to register property. You need BankID to sign digital contracts and set up utilities. Both take weeks to months to obtain after arrival. The guide maps the application timeline, explains how to manage the gap period (keeping services running under the previous owner's name, interim insurance arrangements), and identifies the steps you can complete before the D-nummer arrives so administrative delays do not derail your transaction.

Residency Horizon Decision Matrix

Whether buying makes financial sense depends entirely on how long you are staying. For expats on short-term postings under three years, the combination of dokumentavgift (2.5% on freehold), megler commissions on resale (1.0% to 2.5%), mortgage registration fees, and moving costs means you need substantial price appreciation just to break even. For five-year-plus residents, the equity accumulation historically far outweighs transaction costs. The guide provides a framework matched to your visa type, residency status, and exit flexibility — so you make the buy-versus-rent decision based on your actual numbers, not assumptions from a market you do not fully understand yet.

Standalone Printable Tools

Every paid download includes these standalone reference sheets — designed to print and use during the actual buying process:

- Ownership Structure Comparison — Side-by-side comparison of borettslag, selveier, and boligsameie with decision criteria matched to your situation

- Fellesgjeld Risk Calculator — Fillable worksheet for calculating total acquisition cost, stress-testing monthly costs, and evaluating cooperative debt risk

- Mortgage Document Checklist — Every document to prepare before your bank meeting, plus the trade union strategy and AML compliance checklist

- Budrunde Quick Reference — Bidding rules, auction timeline, and strategy reminders to keep next to your phone during the live auction

- Tilstandsrapport Decoder — Condition grade reference table, red flag cost estimates, and the 2022 law changes — use alongside the Norwegian inspection report

Who This Guide Is For

This guide is for foreign nationals and expats buying property in Norway who:

- Are working in oil and gas, technology, finance, healthcare, or academia and earning enough to qualify for a Norwegian mortgage — but have been rejected by automated credit systems because they lack a local tax assessment history, and need a clear pathway through manual underwriting with the right documentation

- Are EU/EEA professionals who have settled in Norway for two or three years and are ready to buy — but remain confused by the difference between borettslag and selveier, unsure how fellesgjeld affects total acquisition cost, and unclear on which ownership structure matches their subletting needs and long-term plans

- Are non-EEA skilled workers on temporary residence permits who are unsure whether they can get a mortgage at all, how their visa duration affects bank risk assessments, and what equity percentage they will realistically need

- Have experienced the budrunde and lost — either by hesitating because they did not understand the bidding rules, by overbidding because the process moved faster than they expected, or by walking away from properties because they could not read the tilstandsrapport and did not want to make a legally binding bid on something they could not evaluate

- Are considering buying in Oslo, Bergen, Stavanger, or Trondheim and want to understand the local market dynamics, typical price levels, and the structural risks specific to Norwegian construction before they commit

- Are on fixed-term academic contracts of three to five years and need to calculate whether the transaction costs of buying and reselling will exceed the cost of renting — a calculation that depends on ownership structure, dokumentavgift exposure, and subletting restrictions they have not been able to find clearly explained in English

Why Not Free Resources?

Free information on buying property in Norway as a foreigner exists. Here is what each source actually delivers:

- Life in Norway offers warm, accessible articles about the house-buying experience with genuine personal perspective. What it does not do: provide granular breakdowns of fellesgjeld risk calculations, explain how the 2022 Avhendingsloven amendments changed buyer liability, walk through manual underwriting strategies for different visa categories, or teach you how to decode a tilstandsrapport's condition grades. The narrative is helpful. The technical depth a foreign buyer needs to avoid six-figure mistakes is not there.

- Finn.no is where every property in Norway is listed and where you will spend most of your search time. But Finn is a transactions platform, not an educational one. It does not explain the difference between the innskudd you see in the listing and the total acquisition cost including fellesgjeld. It does not teach you how the budrunde works. It does not help you evaluate the tilstandsrapport attached to the salgsoppgave. It shows you what is for sale. It does not prepare you to buy it.

- Huseierne (Norwegian Homeowners Association) publishes excellent legal and practical guidance — in Norwegian. For a newly arrived expat navigating their first Norwegian property purchase, content that requires fluent Norwegian to understand is functionally inaccessible at the moment they need it most.

- Megler (estate agent) portals publish buying guides that describe the process from the perspective of professionals who earn their commission from the seller. They explain the steps clearly. They do not explain the fellesgjeld traps, the tilstandsrapport red flags that should make you walk away, or the underwriting strategies that get foreign buyers approved when automated systems say no. They will help you through the process. They will not help you avoid overpaying or buying problems.

- Reddit (r/Norway, r/oslo) is where expats share real mortgage experiences and bidding war stories — and where advice from 2023 sits next to current regulations, where one poster's DNB rejection contradicts another's Nordea approval, and where "just join Tekna" is repeated without context about why it works or who it applies to. The experiences are genuine. The signal-to-noise ratio makes it dangerous to base a multi-million-kroner decision on anonymous forum posts.

- Relocation company guides provide basic checklists that cover the high-level steps without explaining the mechanics of the budrunde, the financial structure of cooperative housing, or how to evaluate a technical inspection report. They are designed to orient you. They are not designed to protect your capital.

This guide fills the navigation gap — the space between knowing Norway has two ownership types, a fast bidding process, and strict lending rules, and understanding how they all interact across a single property purchase. It is the analysis an independent advisor with no properties to sell would give you, structured as a permanent reference you own.

— Less Than Half the Dokumentavgift Filing Fee

The dokumentavgift alone on a NOK 4,000,000 freehold apartment is NOK 100,000. A single missed red flag in the tilstandsrapport can mean NOK 150,000 to NOK 300,000 in bathroom renovation. Buying a borettslag apartment without calculating the fellesgjeld can mean discovering that your NOK 2,500,000 purchase actually costs NOK 4,000,000 when the shared debt is included. One legally binding bid submitted in the heat of a budrunde without understanding the rules can lock you into a contract you cannot exit.

This guide does not replace your megler, your bank advisor, or your building surveyor. But it gives you the ownership structure decision framework, the fellesgjeld risk assessment, the manual underwriting strategy, the budrunde preparation system, and the tilstandsrapport decoder that ensure you walk into every conversation knowing exactly what to ask, exactly what to calculate, and exactly what to never accept at face value — instead of learning expensive lessons in real time.

If it prevents a single fellesgjeld surprise, catches a tilstandsrapport red flag you would have missed, or helps you navigate manual underwriting to get the mortgage automated systems denied, it pays for itself before you have finished reading it.

30-day money-back guarantee. If the guide does not make your Norway property purchase clearer and your financial position stronger, you pay nothing.

Download the free Buying in Norway — Foreigner's Quick Checklist to see the step-by-step action plan covering ownership structure selection, financing requirements, bidding process rules, and key Norwegian terms you need to know. When you are ready for the full acquisition system — the complete guide plus five standalone printable tools with every decision framework, worked example, and red flag identifier — the complete toolkit is here.

You moved to Norway for the opportunity. Now make sure the property you buy does not cost you twice.