You Found Your Dream Apartment in Lisbon. The Portuguese System That Governs Your Purchase Just Changed Every Rule You Researched.

You've spent months on this. You've compared Algarve villa prices against Silver Coast new-builds, watched YouTube walkthroughs of Cascais penthouses, run a Wise transfer calculator at 2 AM to check the exchange rate on a €350,000 apartment. You've read that Portugal offers a favorable tax regime for new residents. You've seen agency blogs still describing the NHR program as a reason to relocate. Three things have changed since you started researching — and any one of them can cost you tens of thousands of euros.

First: the Non-Habitual Resident regime closed to general applicants on December 31, 2023. Its replacement, IFICI, applies almost exclusively to scientific researchers, higher education professors, and highly qualified professionals in certified R&D sectors — not retirees, not digital nomads, not most remote workers. Your pension income won't be taxed at a flat 10%. It'll be taxed at progressive rates from 13.25% to 48%.

Second: €22,500 in transfer tax on a €300,000 property. Under the progressive IMT scale that Portuguese residents pay, the same property costs roughly €10,747 — an effective rate of about 3.6%. As a non-resident buyer in 2026, you pay a flat 7.5%. The difference — nearly €12,000 — goes to the Autoridade Tributária before the notary will execute your deed. And here's what no agency blog mentions: you can recover that difference if you become a registered Portuguese tax resident within 24 months. But only if you know the refund mechanism exists, understand the application process, and hit the deadline.

Third: you find the property, agree on a price, and sign the CPCV — the Contrato Promessa de Compra e Venda, Portugal's binding promissory contract. You transfer a 10-20% deposit. Not into an escrow account held by a neutral third party. Directly into the seller's personal bank account. If the seller defaults, Portuguese law says they owe you double. But collecting double from a newly formed shell company — a Sociedade por Quotas with €1,000 in registered capital and no parent company — means hiring a Portuguese litigator and spending years in civil court. If you default because the bank undervalued the property and your mortgage fell through, you lose the entire deposit. The "subject to financing" clause you assumed would protect you? Portuguese sellers in competitive markets regularly reject it.

None of this means Portugal is the wrong decision. The lifestyle case — safety, climate, healthcare access, EU residency pathway — is stronger than ever now that speculative visa buyers have left the market. But the gap between what you've researched and what actually happens when you sign has never been wider.

You search for help. Idealista and Imovirtual have the listings but zero transactional guidance — no explanation of CPCV deposit risk, no mention of the Licença de Utilização requirement, no warning about the 7.5% IMT. Engel & Völkers and Sotheby's publish polished regional guides that systematically minimize the risks to avoid losing potential clients. Law firm blogs cover IFICI eligibility or AIMI thresholds in precise technical isolation — one concept per article, each functioning as an SEO funnel for consultations billed at €200-400 per hour. And on r/PortugalExpats, you'll find a thread from last month where someone confidently states that the CPCV deposit is refundable if financing falls through, three people agree, and nobody corrects them. It is not refundable.

Here's the problem no free resource solves: Portugal's property transaction runs on a system where the notário is a state-appointed neutral, not your advocate; where your deposit goes directly to the seller with no escrow; where the tax regime that attracted you no longer exists for most applicants; and where exemptions, refund mechanisms, and strategic workarounds exist at every stage — but only if you know they're there and activate them before you sign.

The Buying Property in Portugal — Expat Guide is The Full-Disclosure Framework. Not a lifestyle article about finding your dream villa in the Algarve. It's a structured decision system that maps every stage of the Portuguese property purchase — from NIF application through CPCV negotiation, IMT calculation, bank valuation, and escritura — telling you what agency blogs, property portals, and commission-driven agents deliberately leave out, so you make each decision understanding the 2026 regulation that governs it and the financial consequence of getting it wrong.

What's Inside The Full-Disclosure Framework

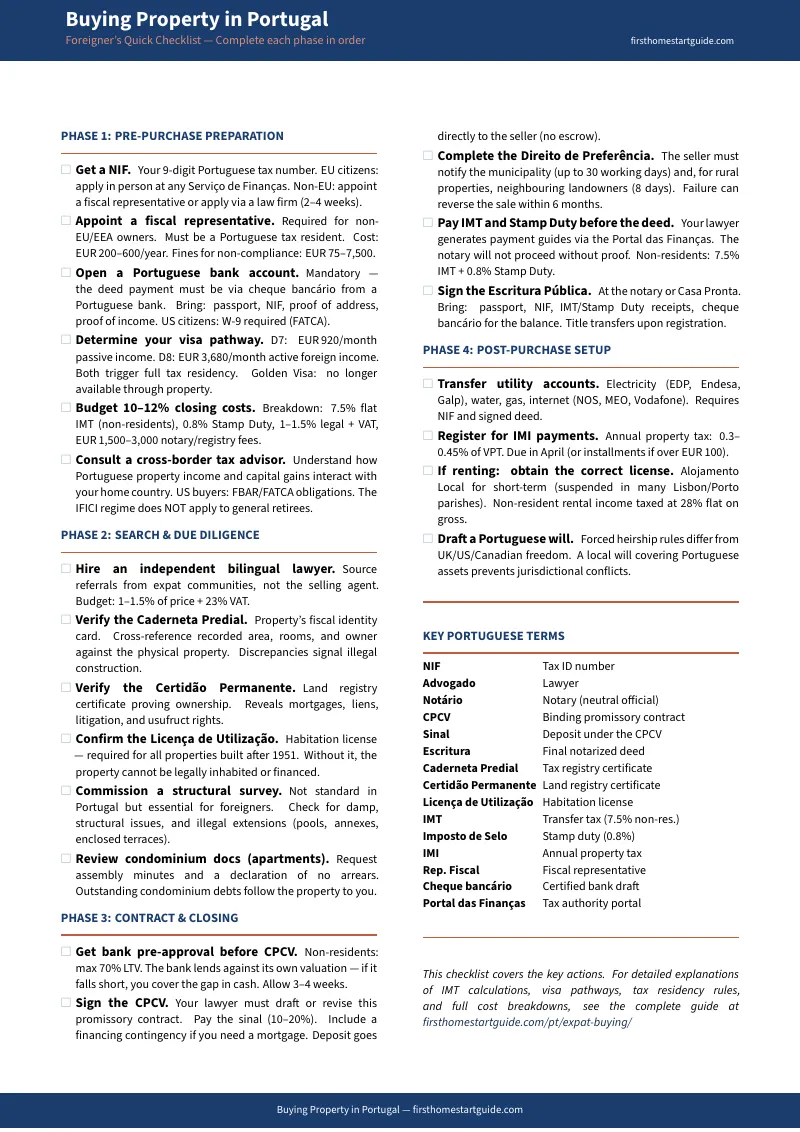

A comprehensive 66-page PDF guide, a quick-start checklist, and 6 standalone printable tools — instant download, 8 PDFs total. Covering every stage from obtaining your NIF through key collection, organized in the order you'll encounter each decision: taxes and costs first, then deposit protection, then visa and residency, then financing, then legal due diligence, then regional selection, then ongoing ownership:

IMT Transfer Tax Navigator

The flat 7.5% IMT rate for non-residents is the single largest new cost in the 2026 Portuguese buying process — and the area where strategic planning saves the most money. On a €300,000 property, a resident buying a primary home pays roughly €10,747. A non-resident pays €22,500. The guide breaks down the full progressive scale versus the flat rate, quantifies the exact delta at every price point, and maps the two primary escape routes: declaring Portuguese tax residency within 24 months of purchase to claim a refund of the difference, or placing the property on the residential rental market for at least 36 months within five years (subject to the €2,300 monthly rent cap). It covers Stamp Duty (Imposto de Selo at 0.8%), the young buyer exemption for residents aged 18-35 on properties up to €330,539, and the exact payment sequence — because IMT and Stamp Duty must be paid before the notary will execute the deed. This is what protects you from paying €12,000 more than you need to.

CPCV Deposit Shield

The Contrato Promessa de Compra e Venda is where most foreign buyers' money is most exposed. The guide explains exactly how the deposit works: 10-20% of the purchase price, transferred directly to the seller's account with no independent escrow. If the buyer defaults, the deposit is forfeited. If the seller defaults, the seller owes double — but enforcement requires civil litigation, and recovery depends on the seller's actual ability to pay. It covers the "subject to financing" clause that sellers regularly reject, the tactical sequence for securing bank pre-approval and completing the physical valuation before signing the CPCV (a three-to-four-week process during which the property remains on the open market), how to evaluate seller counterparty risk, and the specific CPCV clauses your independent advogado should insist on — including valuation contingencies, completion deadlines, and penalty structures. This is what protects your deposit.

NHR/IFICI Reality Check

The original NHR regime — 10% flat tax on foreign pensions, broad exemptions on dividends and capital gains — closed to general applicants on December 31, 2023. Existing holders are grandfathered. The replacement, IFICI, is marketed as "NHR 2.0" but eligibility is restricted to scientific researchers, higher education professors, and highly qualified professionals (Level 6 or 8 European Qualifications Framework) in certified start-ups or state-recognized R&D sectors. A small number of qualified professionals outside academia may also be eligible under specific conditions — the guide maps the full eligibility criteria. For those who don't qualify, it covers the standard progressive IRS rates (13.25% to 48%), the annual proof-of-eligibility deadline (January 15), and the strategic tax planning implications for retirees, remote workers, and investors whose relocation math was built on assumptions that no longer hold. This is what prevents you from relocating based on a tax regime you can't access.

Visa and Residency Roadmap

The Golden Visa no longer accepts real estate investments. The D7 passive income visa requires €920 per month (strictly passive — pensions, dividends, royalties); the D8 digital nomad visa requires €3,680 per month in active foreign-sourced income. Both require long-term accommodation in Portugal before approval, creating a chicken-and-egg scenario. Both trigger Portuguese tax residency. The guide maps each pathway with the exact 2026 income thresholds (including spouse and dependent add-ons), explains how the visa timeline intersects with the property transaction timeline, covers the fiscal representative requirement for non-EU/EEA residents (mandatory if you own property, with fines of €75 to €7,500 for non-compliance), and clarifies what buying property does and does not do for your immigration status.

Non-Resident Mortgage Playbook

Portuguese banks cap non-resident mortgages at 70% LTV — meaning a minimum 30% cash deposit plus 8-11% in closing costs. The strict 35% debt-to-income ratio includes all existing debt worldwide. Maximum loan terms are age-capped: a 60-year-old buyer limited to a 10-year term faces dramatically higher monthly payments that may breach the DTI threshold. The guide covers the four banks most experienced with non-resident applications — Caixa Geral de Depósitos, Santander Totta (advantageous for US buyers with existing Santander relationships), Bankinter (occasionally extends to 75% LTV for prime urban properties), and UCI (competitive long-term fixed rates, strong FATCA compliance) — with current rate ranges, EURIBOR indexing for variable rates, and the 0.5% cap on early repayment fees.

Due Diligence Decoder

Portuguese property transactions demand verification of three state-issued documents that must align with physical reality. The Caderneta Predial (Tax Registry Certificate) proves the property's fiscal identity and official tax value. The Certidão de Teor (Land Registry Certificate) proves ownership and reveals mortgages, liens, or pending litigation. The Licença de Utilização (Habitation License) certifies the property was built according to approved plans — and properties lacking it cannot be legally financed or converted to Alojamento Local tourist rentals. The guide explains how to read each document, what discrepancies to flag, why structural building surveys are not standard practice in Portugal (meaning you must commission one independently), and the specific risks foreign buyers face: swimming pools, annexes, and extensions built without municipal permission that transfer their legal liability — and potential demolition orders — to you.

Regional Market Intelligence

Portugal is not one market. Lisbon commands €5,000+ per square meter in prime neighborhoods with 4-6% annual appreciation. The Algarve averages €3,400-3,600/m² with luxury coastal zones hitting €9,000+. The Silver Coast offers €2,400-3,900/m² with towns like Caldas da Rainha at €2,401/m² — properties that would cost double in the Algarve. Emerging corridors like Setúbal (22.6% year-on-year appreciation), Coimbra (6.7% yields), and Braga (5.6% yields) offer entry points below the saturated urban cores. The guide covers price-per-square-meter data, yield profiles, lifestyle considerations, infrastructure quality, and expat community density for each region — so you allocate capital based on data, not agency marketing.

Annual Ownership Tax Guide

Beyond acquisition taxes, ongoing ownership costs include IMI (Municipal Property Tax) at 0.3-0.45% of the official tax value and AIMI (the "wealth tax") at 0.7% on aggregate residential property values exceeding €600,000 for individuals. The guide covers municipality-by-municipality IMI rate variations, AIMI calculation for portfolio holders, and the fiscal representative's role in annual tax compliance with the Autoridade Tributária.

Plus 6 Standalone Printable Tools

Every paid download includes standalone reference PDFs you can print and bring to meetings: a Transaction Costs Worksheet to calculate your total closing costs at any property price, a Due Diligence Checklist covering all three critical documents and structural survey items, a CPCV Protection Checklist for contract signing, a Bank Comparison Card with side-by-side mortgage terms from five Portuguese banks, a Regional Market Reference with price-per-square-metre data for 11 regions, and a Glossary of Portuguese Property Terms with 29 essential terms grouped by category.

Who This Guide Is For

This guide is for foreign buyers and expats purchasing property in Portugal who:

- Are buying their first Portuguese property and need the entire transaction mapped — from NIF application through CPCV negotiation, IMT payment, bank valuation, and escritura — so they understand what happens at each stage, what it costs, and where the system diverges from what they expect

- Have found a property and need to know, before they sign the CPCV, how much their deposit is truly at risk, whether a financing contingency is realistically achievable, and what their total closing costs will be under the 7.5% non-resident IMT rate

- Planned their relocation around NHR tax benefits and now need to understand what IFICI offers (and doesn't), what standard progressive IRS rates mean for their income, and whether the financial case for Portugal still holds under 2026 tax rules

- Are American, British, Canadian, South African, or Australian and need the D7 or D8 visa pathway mapped alongside the property transaction — including income thresholds, the accommodation requirement, and the fiscal representative obligation

- Are financing with a Portuguese mortgage and need to understand the 70% LTV cap, the 35% DTI ratio, the age-capped loan terms, and which banks handle non-resident applications most effectively

- Want every transaction cost, every tax rate, every legal deadline, and every procedural requirement in one document — so they walk into advogado meetings, bank appointments, and notário signings understanding exactly what's happening and why

Why Not Free Resources?

Free information on buying property in Portugal as a foreigner is everywhere. Here's what each source actually delivers:

- Idealista and Imovirtual have every listing in Portugal — and zero guidance on the CPCV deposit mechanics, the 7.5% IMT rate, or the Licença de Utilização requirement. You can find a €300,000 apartment in Lisbon in ten minutes. What you can't find on any portal: how much of the €30,000 CPCV deposit you'll recover if your mortgage is denied. The answer is zero, but the portals don't tell you that.

- Agency blogs and relocation services produce polished regional guides that explain the process at a high level and emphasize lifestyle opportunity — maintained by businesses whose revenue depends on closing transactions. What they consistently minimize: the counterparty risk in the CPCV, the frequency of unlicensed construction, the real financial impact of the 7.5% IMT, and the practical reality that IFICI doesn't apply to most relocating professionals. Full-service relocation agencies charge €5,000-15,000 for end-to-end support — this guide gives you the structural understanding to evaluate whether that service is worth it for your specific situation.

- Portuguese law firm websites publish technically precise articles on individual topics — IMT calculation, IFICI eligibility, fiscal representative requirements. Each article covers one concept in isolation and functions as a lead-generation page for consultations at €200-400 per hour. What they don't provide: a single integrated roadmap connecting the tax, legal, banking, immigration, and due diligence tracks into one sequence you can follow from start to finish.

- On Reddit and Facebook expat groups, you'll find genuine experiences from real buyers alongside threads where someone asks whether the CPCV deposit is refundable if their mortgage falls through, three people say yes, and nobody posts the correction. You'll find advice that still references NHR as available, confuses D7 and D8 income thresholds, and recommends skipping the structural survey because "the notário handles everything." The notário does not handle structural surveys.

This guide fills the structural gap — the space between knowing that Portugal has a notário system and understanding how the 2026 tax rules, deposit mechanics, mortgage limits, and visa pathways actually interact at each stage of your specific transaction. It's the analysis an independent advisor with no commission to earn would give you, structured as a permanent reference you own.

— Less Than Half an Hour of a Portuguese Lawyer's Time

An independent advogado charges €2,000-5,000 for legal due diligence on a single transaction. The fiscal representative you're legally required to appoint costs an annual retainer. The CPCV deposit you're protecting is €30,000-60,000 on a mid-market property. The IMT difference between the flat 7.5% and the progressive rate on a €300,000 property is nearly €12,000. The cost of navigating all of this through conflicting free resources, outdated forum threads, and commission-driven agency blogs? Months of confusion and decisions made on incomplete information.

This guide doesn't replace your advogado or your fiscal representative. But it gives you the IMT navigator, the CPCV deposit shield, the NHR/IFICI reality check, the mortgage playbook, and the due diligence decoder that ensure you walk into every appointment, every viewing, and every contract signing understanding the 2026 rules — instead of discovering how Portuguese property law works by losing money to it.

If it identifies the 24-month residency path that recovers €12,000 in IMT overpayment, catches a missing Licença de Utilização before you sign the CPCV, or prevents a deposit forfeiture by securing bank pre-approval before the promissory contract, it pays for itself before you've finished reading it.

30-day money-back guarantee. If the guide doesn't give you a clearer, more confident understanding of the Portuguese property transaction, you pay nothing.

Download the free Quick Checklist to see the step-by-step action plan covering NIF application, IMT calculation, CPCV deposit protection, visa pathway selection, and the transaction timeline from first viewing to escritura.

When you're ready for the full guide — the complete Full-Disclosure Framework with the IMT navigator, CPCV deposit shield, NHR/IFICI reality check, mortgage playbook, due diligence decoder, and regional market intelligence — the complete guide is here.

You've found the property. Now understand the system that governs your purchase — before you sign.