Seoul Rents Just Crossed ₩1.48 Million a Month. The Jeonse System That Used to Protect You Is Collapsing. And the Government Just Rewrote Every Rule for How Foreigners Buy Property.

You moved to Korea for a contract. Then you extended. Then you married, or started a business, or simply realized you weren't leaving. Somewhere along the way, your employer-subsidized housing disappeared, the jeonse deposit you relied on started looking like a fraud risk, and your monthly wolse climbed to a number that makes you question every financial decision you've made in this country.

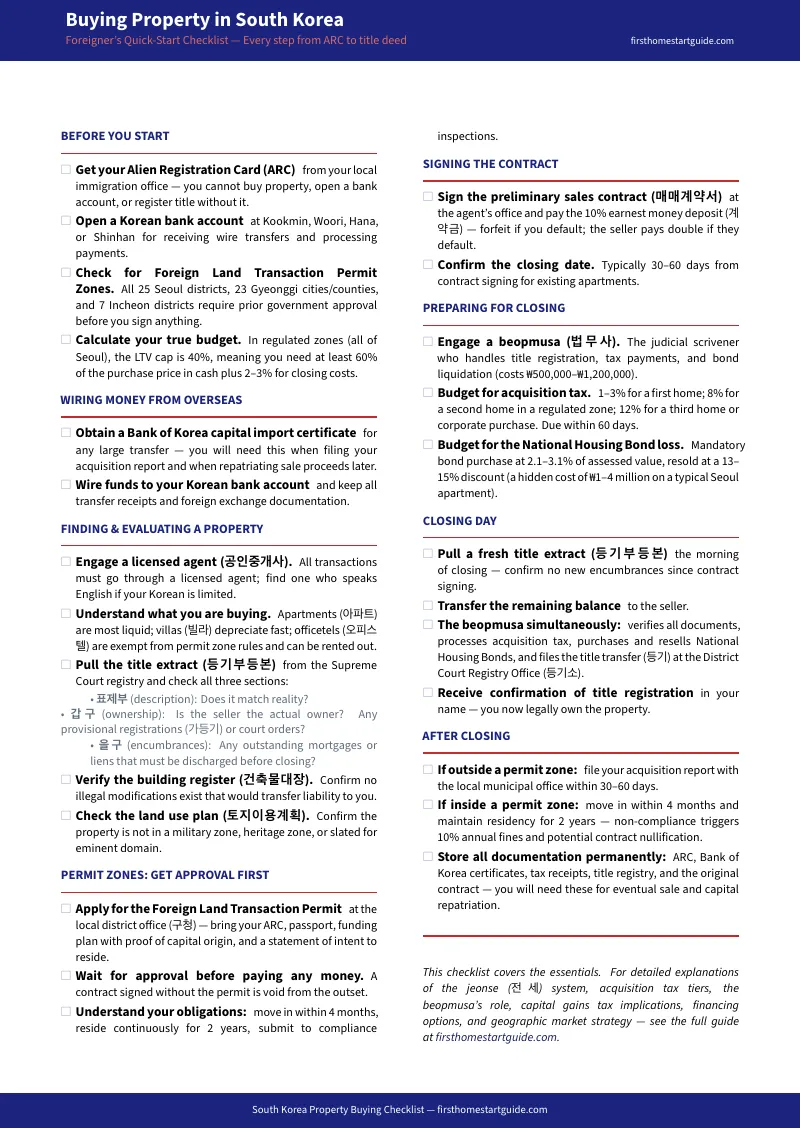

You start researching. Can you actually buy? Reddit says yes, but the threads are from 2023 — before the Foreign Land Transaction Permit Zone turned all of Seoul into a prior-approval regime. A Facebook group says foreigners need 60% cash because the LTV cap is 40%, but nobody can explain the Stressed DSR calculation that determines your actual loan ceiling. An international law firm quotes you $5,000 for "purchase assistance" — services that a ₩700,000 beopmusa already handles. And every source you find misses at least one of the regulatory changes from 2025 and 2026 that fundamentally altered how foreigners buy property in Korea.

Here's what no free resource puts together in one place: Korea's property system runs on Korean-language registries, prior-approval mandates in regulated zones, a 40% LTV cap that forces you to produce 60% of the purchase price in cash, acquisition tax tiers that jump from 1% to 8% to 12% depending on how many properties you own, a capital gains tax cliff that pushes effective exit rates above 82%, and a title system where your legal name is transliterated into Hangul on a registry that most foreigners have never seen, let alone understood. The protections exist — the deunggi-bu deungbon title system is absolute, the beopmusa registration process is ironclad, the reciprocity framework covers most Western nationalities — but only if you know how to activate them before you sign.

The Buying Property in South Korea — Expat Guide is The Regulatory Decoder. Not a lifestyle article about expat life in Gangnam. It's a structured decision system that maps every stage of the Korean property purchase — the ARC prerequisites, the permit zone application, the jeonse-vs-buying financial comparison, the contract mechanics, the beopmusa title transfer, and the post-closing compliance obligations — so you make each decision understanding the legal mechanism behind it, the actual cost, and the consequence of getting it wrong.

What's Inside The Regulatory Decoder

The complete guide plus 9 standalone printable tools — covering every stage from bureaucratic preparation through closing day, with the Korean legal terms, tax rates, LTV calculations, and regulatory deadlines that determine whether your purchase succeeds or collapses:

The Jeonse Collapse Calculator

The single most important financial decision facing long-term expats in Korea, and the one that every English forum gets wrong. Jeonse deposits of ₩300–500 million once let you live rent-free — until the "Villa King" fraud scandals wiped out ₩2.28 trillion in tenant deposits and interest rate hikes destroyed the gap-investing model that propped the whole system up. By Q1 2025, monthly wolse accounted for 64.6% of all new Seoul leases. Average monthly rents crossed ₩1.48 million. The guide provides a year-by-year cost comparison: jeonse deposit risk exposure versus wolse cash burn versus mortgage servicing costs at current rates. For a long-term resident paying ₩1.48 million per month in wolse, the math on buying becomes obvious — the guide shows you exactly where the breakeven point falls based on your down payment, interest rate, and holding period.

Permit Zone Navigator

In August 2025, the government designated all 25 Seoul districts, 23 Gyeonggi cities and counties, and 7 Incheon districts as Foreign Land Transaction Permit Zones. If you're buying residential property anywhere in the Seoul Metropolitan Area, you need government approval before you sign a contract or pay a single won in earnest money. The guide maps the complete permit application process: which documents you need (ARC, passport, capital origin proof, residency intent statement), where to file (your local gu-cheong district office), the approval timeline, the 4-month move-in mandate, and the 2-year continuous residency requirement. A contract signed without the permit is void from the outset under Article 11 of RETA. The guide also covers the areas outside the permit zone — Busan, Daejeon, Sejong — where the post-transaction reporting system still applies and investment flexibility is significantly greater.

Acquisition Tax Decoder

Foreign buyers model their closing costs at 1–2% based on home-country logic. Korea's acquisition tax starts at 1–3% for a first home, jumps to 8% for a second home in a regulated zone, and hits 12% for a third or any corporate purchase. On a ₩1 billion apartment, the difference between "first home" and "second home" is ₩50–70 million in tax before you've paid a single won in legal fees. The guide breaks down every tier — base rate by property value, rural special tax, local education surtax — with worked examples at ₩500 million, ₩1 billion, and ₩1.5 billion. It also covers the May 2026 Capital Gains Tax cliff: the surcharge suspension expired permanently, pushing effective exit rates to 82.5% for multi-home sellers. The guide shows you how to calculate your full transaction cost — acquisition plus holding plus disposal — before you commit.

The Beopmusa Playbook

The single most expensive mistake foreigners make is hiring an international law firm for ₩5–7 million when the entire title registration — deunggi transfer, lien clearance, tax payment, National Housing Bond processing — is legally handled by a beopmusa (judicial scrivener) for ₩500,000–₩1,200,000. The beopmusa is a licensed specialist whose sole mandate is the property registry. They are not a lawyer and don't charge lawyer rates. The guide explains exactly what the beopmusa does on closing day, how to find a bilingual one, what to verify independently before closing, and why paying ₩5 million to an international firm for the same service is burning money. It also covers the role of the budongsan (licensed real estate agent), the legally capped brokerage fees (0.4–0.7% depending on transaction value), and how to structure the agent-beopmusa relationship so nothing falls through the cracks.

Foreign Capital Transfer System

You cannot wire ₩500 million from your overseas account into a Korean retail bank without triggering anti-money laundering flags and potential account freezes. The Foreign Exchange Transactions Act governs every dollar that enters Korea for property purchases. The guide walks through the complete capital import process: obtaining the Bank of Korea certificate, documenting the origin of funds, choosing between direct wire and phased transfers, and preserving every receipt for the acquisition report you must file within 30–60 days. For overseas Koreans (gyopo) on F-4 visas, it covers the additional complications — family fund transfers, inheritance capital, and the paradox of holding a heritage visa while being classified as a "non-resident foreigner" for lending purposes.

The Deunggi Title System

Your property ownership in Korea is recorded in the deunggi-bu deungbon — the certified title extract maintained by the Supreme Court. The guide teaches you how to read all three sections: the pyoje-bu (property description), the gap-gu (ownership history — where you confirm the seller actually owns what they're selling and check for provisional registrations or court orders), and the eul-gu (encumbrances — outstanding mortgages, liens, and rights that must be discharged before closing). Your legal name appears in Hangul, transliterated from your ARC. The guide explains why this is legally bulletproof — your Hangul name is permanently cross-referenced with your ARC number and passport in the national database — and how to pull a fresh deunggi-bu deungbon on closing morning to confirm no new encumbrances appeared overnight.

Geographic Strategy Guide

Seoul apartments averaged ₩1.45 billion by mid-2025, with new completions projected to drop 48% in 2026. But Korea is not just Seoul. The guide covers the investment calculus for Busan (lower barriers, stronger rental yields, outside the permit zone), Jeju (special autonomous province with its own regulations), Sejong (the administrative capital with government-worker demand), and the satellite cities in Gyeonggi province where LTV restrictions still apply but prices sit 40–60% below central Seoul. It also covers property types: apartments (아파트) for maximum liquidity and appreciation, villas (빌라) which depreciate fast and resell poorly, and officetels (오피스텔) which are exempt from the permit zone residency mandate and can be rented out immediately — the only residential-adjacent property type in the SMA where buy-to-let still works.

Who This Guide Is For

This guide is for foreign buyers and expats purchasing property in South Korea who:

- Are long-term residents — English teachers, corporate expats, trailing spouses, or business owners — watching their wolse climb every year and realizing that buying is now financially cheaper than renting for anyone planning to stay more than 3–4 years

- Are overseas Koreans (gyopo) on F-4 visas who assumed their heritage status would give them preferential mortgage access — and discovered that banks classify them as non-resident foreigners for lending purposes, applying the same 40% LTV cap and Stressed DSR calculation as standard expats

- Need to understand the Foreign Land Transaction Permit Zone system before signing anything — including which areas require prior approval, what the 4-month move-in and 2-year residency mandates mean in practice, and what happens if you fail a compliance inspection

- Are ready to buy but need the entire cost structure mapped — acquisition tax tiers, beopmusa fees, National Housing Bond losses, brokerage commissions, capital gains tax exposure — so nothing surprises them between contract and closing

- Need to transfer overseas capital into Korea and want the Foreign Exchange Transactions Act process explained step by step — Bank of Korea certificates, origin-of-funds documentation, and the acquisition report deadline

- Want the complete purchase process in one document — ARC prerequisites, permit application, property search, deunggi-bu deungbon verification, contract signing, beopmusa engagement, closing day execution, and post-closing compliance — so they walk into every appointment understanding the mechanism behind each step

Why Not Free Resources?

Free information on buying property in Korea as a foreigner is everywhere. Here's what each source actually delivers:

- Reddit and expat Facebook groups (r/Living_in_Korea, r/korea, "Expats in Korea") contain real stories from real buyers — alongside advice from 2023 that pre-dates the Foreign Land Transaction Permit Zone, debates about whether you need a dojang (name stamp) that were resolved years ago, and confidently stated LTV percentages that changed when the government tightened mortgage regulations in October 2025. You'll find someone who closed smoothly in Busan and someone who lost their earnest money in Seoul. Both stories are real. Neither tells you which regulatory regime applies to your property.

- InterNations and expat portals publish overviews of the housing process in clear English — covering jeonse, wolse, and the basic purchase steps. What they don't cover: the permit zone system, the 2-year residency mandate, the acquisition tax cliffs for multi-home buyers, the Stressed DSR calculation that determines your actual loan amount, or the capital gains tax cliff that makes timing your exit a six-figure decision. The information is correct as far as it goes. It stops before the complexity that costs money.

- International law firms (Korean-based practices targeting expats) publish precise articles on individual topics — the permit zone rules, the acquisition tax structure, the beopmusa versus attorney question. Each article is accurate in isolation and designed to demonstrate expertise you'll need to pay $3,000–$5,000 to access for your specific transaction. What they don't provide: a single integrated roadmap that connects the permit application, the capital transfer, the tax calculation, and the closing process into one actionable sequence.

- Korean proptech platforms (Naver Real Estate, Zigbang, Dabang, KB Real Estate) are the definitive data sources for listings, zoning, and valuations — and they are aggressively monolingual. Browser translation produces rough, often misleading renderings of highly technical legal terms. Misinterpreting a jeonse liability flag or a deunggi encumbrance status on Naver Real Estate can cost you your entire deposit.

This guide fills the structural gap — the space between knowing that foreigners can buy property in Korea and understanding exactly how the system works at each stage, what the 2025–2026 regulations changed, what your actual costs will be, and what happens to your money when you miss a deadline or sign without a permit. It's the analysis a bilingual advisor with no commission to earn would give you, structured as a permanent reference you own.

— Less Than Half an Hour of a Seoul Law Firm's Time

An international law firm in Seoul charges $3,000–$5,000 for purchase assistance on a single residential transaction. A beopmusa handling the actual title registration costs ₩500,000–₩1,200,000. The 10% earnest money deposit you're protecting in the contract is ₩50–100 million on a typical Seoul apartment. A single acquisition tax miscalculation — assuming 1% when your situation triggers 8% — is a ₩50–70 million surprise on closing day.

This guide doesn't replace your beopmusa or your bilingual real estate agent. But it gives you the permit zone navigator, the acquisition tax decoder, the jeonse-vs-buying calculator, the capital transfer playbook, and the deunggi verification system that ensure you walk into every appointment, every viewing, and every contract signing understanding the mechanism behind each step — instead of discovering how Korean real estate regulation works by losing money to it.

If it saves you from hiring an international law firm for services a beopmusa already covers, catches an acquisition tax tier you didn't expect, or prevents a permit zone violation that triggers 10% annual fines and contract nullification, it pays for itself before you've finished reading it.

30-day money-back guarantee. If the guide doesn't make the Korean property transaction clearer and your financial position stronger, you pay nothing.

Download the free Quick Checklist to see the step-by-step action plan covering ARC prerequisites, permit zone verification, budget calculation, deunggi-bu deungbon checks, contract signing, and closing day execution. When you're ready for the full Regulatory Decoder — complete with the jeonse collapse calculator, acquisition tax decoder, beopmusa playbook, capital transfer system, and geographic strategy guide — the complete guide is here.

You've decided to stay in Korea. Now decode the regulatory system that stands between you and the keys.