Your Bank Said You Can Afford It. The Stress Test Says You Can't.

You earn CHF 180,000. You have CHF 250,000 in savings. You found a CHF 1.2 million apartment in Seefeld. Your colleague bought last year. Your landlord just raised the rent again. Everything points to buying.

Then the bank runs the stress test. Not at today's SARON rate — at a hypothetical 5%. Your CHF 1.2 million apartment requires a minimum gross household income of CHF 200,000 just to qualify. Your bonus compensation gets a haircut. Your stock-based compensation is excluded entirely. You are told to come back when you have a larger down payment or a higher base salary.

This is normal in Switzerland. It is also entirely navigable — if you understand how the system actually works.

The stress test is one of at least six mechanisms that make Swiss property structurally different from anywhere else you have bought property. The Lex Koller law dictates whether you can legally buy based on your passport and permit — not your wealth. The two-tranche mortgage splits your loan into a portion you never repay and a portion you must repay within 15 years. Your pension fund (Pillar 2) can fund your down payment, but withdrawing it versus pledging it has radically different tax and retirement consequences. The Eigenmietwert — a tax on fictional rental income from your own home — is being abolished in 2029, which will eliminate your mortgage interest deduction and force a complete rethinking of how much debt to carry. And crossing a cantonal border can change your closing costs by CHF 50,000.

The problem is not a lack of information. UBS publishes mortgage calculators. The government site ch.ch explains Lex Koller. Reddit threads debate Pillar 2 withdrawal versus pledging. But no single resource connects these systems into a coherent framework — and the interactions between them are where the costly mistakes happen.

The Switzerland Expat Property Guide is a Swiss Buyer's Regulatory Framework: the legal eligibility rules, mortgage mechanics, pension strategy, cantonal tax arbitrage, transaction sequence, and condominium due diligence in one document — so you can run the stress test yourself before the bank runs it for you, structure your Pillar 2 decision with actual tax consequences modelled, and close without discovering the Schuldbrief fee or the Erneuerungsfonds liability after you have already signed the reservation agreement.

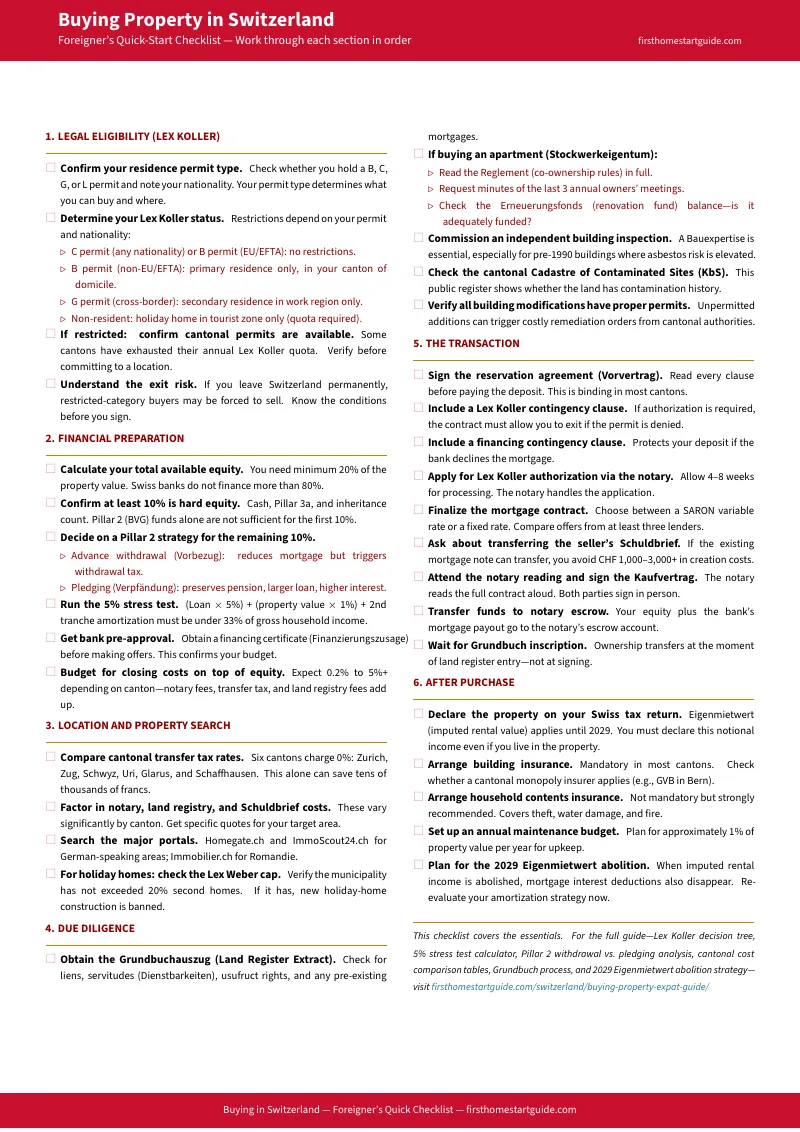

What's Inside the Swiss Buyer's Regulatory Framework

A 12-chapter guide covering every legal, financial, and procedural dimension of buying property in Switzerland as a foreigner — plus a 20-item verification checklist with quick-reference tables. Each chapter solves a specific problem that costs foreign buyers money, time, or their purchase eligibility:

The Lex Koller Permit Matrix — What You Can Actually Buy

C permit, B permit EU, B permit non-EU, G permit, non-resident — five categories with entirely different rights. Most expat blogs say "foreigners can buy." The guide maps the exact restrictions for each permit type: what property types are permitted, which cantons allow it, whether you can rent it out, and what happens to your property if you leave Switzerland permanently. Includes the proposed April 2026 revision that would force non-EU B permit holders to sell within two years of departure.

The 5% Stress Test — Decoded and Calculated

Swiss banks do not use the current interest rate to determine what you can afford. They apply a hypothetical 5% rate and require total housing costs to stay below 33% of gross household income. The guide provides the exact formula, walks through a worked example on a CHF 1 million property, explains how banks treat bonus compensation and foreign-sourced income, and shows you the minimum income threshold before you waste time applying.

The Two-Tranche Mortgage — Why the Swiss Carry Debt for Life

The first tranche (up to 65-67% LTV) has no mandatory repayment — ever. The second tranche (up to 80% LTV) must be repaid within 15 years. This structure is why Switzerland has a sub-1% mortgage default rate and why Swiss homeowners maintain large mortgages indefinitely. The guide explains the mechanics, the SARON variable rate environment (currently near 0%), and the strategic choice between SARON and fixed-rate contracts.

Pillar 2 Withdrawal vs. Pledging — The Decision That Shapes Your Retirement

Swiss law lets you use your pension fund to buy a home. But how you use it matters enormously. Withdrawing capital triggers immediate tax, permanently reduces your retirement benefits, blocks future voluntary purchases, and must be repaid if you sell. Pledging keeps the capital invested, avoids withdrawal tax, preserves deduction rights, but enlarges your mortgage and increases your stress test burden. The guide models both options with their tax consequences so you can make the decision with numbers, not guesswork.

Cantonal Cost Arbitrage — Where CHF 50,000 Disappears at the Border

Six cantons charge zero property transfer tax (Zurich, Zug, Schwyz, Uri, Glarus, Schaffhausen). Geneva charges 3%. Neuchatel charges 3.3%. The same CHF 1.5 million apartment costs under CHF 6,000 in total fees in Zurich and over CHF 60,000 in Geneva. The guide provides a canton-by-canton comparison of transfer taxes, notary fees, land registry fees, and Schuldbrief costs so you can calculate the total closing cost before you make an offer.

The Eigenmietwert Abolition — Why 2029 Changes Everything

Switzerland has taxed homeowners on the fictional rental value of their own home for decades. The September 2025 vote abolished it — but implementation is scheduled for 2029, and it comes with a devastating trade-off: the elimination of mortgage interest deductions at the federal level. The traditional strategy of keeping a large first-tranche mortgage indefinitely and using indirect amortization via Pillar 3a loses its fiscal advantage. The guide explains the timeline, the impact on financing strategy, and what financial advisors are recommending before the cutoff.

The Transaction Sequence — From Reservation to Grundbuch

The step-by-step process: financing certificate, offer, reservation agreement (with its asymmetric deposit risk), Lex Koller authorization if required, notary-drafted purchase contract, Schuldbrief registration, notarization, and Grundbuch inscription. Legal ownership transfers only at the moment of land registry inscription — not when you sign, not when you pay. The guide walks through each step with the documents required, the fees involved, and the timelines to expect.

Condominium Due Diligence (Stockwerkeigentum)

Most expats buy apartments, which means entering a condominium association governed by Swiss co-ownership law. The guide covers what to audit before signing: the Reglement (co-ownership rules), AGM minutes, the Erneuerungsfonds balance (a depleted renovation fund means sudden five-figure special assessments), building inspection priorities for pre-1990 buildings (asbestos), and the cadastre of contaminated sites check.

Who This Guide Is For

- Expats with B or C permits in Zurich, Geneva, Basel, or Zug who have hit "rent fatigue" after 5-7 years and need to understand the complete legal and financial framework — Lex Koller eligibility, stress test qualification, Pillar 2 strategy — before approaching a bank or making an offer

- Dual-income tech, pharma, or finance households earning CHF 150,000-300,000 who can pass the stress test but need to understand the two-tranche structure, SARON vs. fixed-rate trade-offs, and the Eigenmietwert abolition's impact on long-term financing strategy

- Non-EU professionals on B permits who face the strictest Lex Koller restrictions — primary residence only, no rental, potential forced sale on departure — and need to understand exactly what they are legally permitted to do before committing CHF 200,000+ in equity

- Anyone comparing cantons who wants to see the full cost picture — transfer taxes, notary fees, ongoing wealth and income tax — and make location decisions based on numbers, not assumptions

Why Free Resources Leave You Exposed

Bank websites (UBS, ZKB, PostFinance) publish mortgage calculators and basic guides, but their content is designed to sell financing products. They do not warn you about the asymmetric reservation deposit, the Eigenmietwert abolition's impact on amortization strategy, or the Lex Koller restrictions for B permit holders. The calculator tells you what you can borrow — not whether you should.

The government site ch.ch provides legally accurate Lex Koller overviews, but it does not model the financial consequences of Pillar 2 withdrawal versus pledging, compare cantonal closing costs, or explain the Schuldbrief transfer trick that saves thousands in registry fees.

Expat forums (Reddit, English Forum Switzerland) are full of real experience but also full of outdated advice, confused permit categories, and anecdotes that do not generalise. The anxiety is real. The solutions are unreliable.

This guide bridges the gap: the complete regulatory framework translated into step-by-step procedures, with exact formulas, canton-by-canton comparisons, and worked examples that tell you what to do — not just what the law says.

What You Get

8 PDFs — the complete guide, quick verification checklist, and 6 standalone printable worksheets and reference cards:

- The full Guide — 12 chapters covering Lex Koller eligibility, the two-tranche mortgage, the 5% stress test, Pillar 2 withdrawal vs. pledging, cantonal cost arbitrage, the step-by-step buying process, condominium due diligence (Stockwerkeigentum), the Eigenmietwert abolition, holiday home quotas, and ongoing tax and maintenance obligations

- The Quick Checklist — 20 verification items grouped by phase (Legal Eligibility, Financial Preparation, Location and Property Search, Due Diligence, The Transaction, After Purchase) with the key decision points and reference tables from the guide

- 5% Stress Test Calculator — Fill in your property price, equity, and income to see whether you pass the bank's affordability test before you apply

- Cantonal Cost Comparison — Transfer taxes, notary fees, and total closing costs for every canton — with a worked example showing the CHF 50,000+ gap between Zurich and Geneva

- Lex Koller Permit Matrix — One-page reference card showing exactly what each permit type can buy, rent, and keep if you leave Switzerland

- Pillar 2 Decision Worksheet — Withdrawal vs. pledging side-by-side with fill-in fields for your personal numbers, tax consequences, and retirement impact

- Purchase Timeline — Week-by-week roadmap from bank pre-approval to Grundbuch inscription, with documents and fees at each step

- Stockwerkeigentum Audit Checklist — Everything to verify before buying a Swiss apartment: Reglement, AGM minutes, renovation fund balance, asbestos risk, contaminated sites

The free checklist covers what to verify. The full guide and standalone worksheets cover how — with the legal framework, financial modelling, cantonal comparisons, and worked examples that turn a checklist item into an executable decision.

Satisfaction Guarantee

If the guide does not give you a clearer understanding of Swiss property law and mortgage mechanics than everything you have read online combined, email [email protected] and we will make it right.

A single mistake in Swiss property — failing the stress test after paying the reservation deposit, withdrawing Pillar 2 when pledging would have saved you thousands in tax, buying in Geneva when Vaud would have halved your closing costs — costs more than a consultation with a financial advisor. The guide costs less than one hour of a Swiss mortgage broker's time and covers the full scope of what you need to know before you hire one.