You Chose the Simplified Method Because It Was Easy. It Cost You $1,400.

You have a home office. You work from it every day. Tax season arrives, and you check the "$5 per square foot" box because it takes thirty seconds. Your 200-square-foot office gives you a $1,000 deduction. Done. Easy. You file and move on with your life.

Then you run the real numbers. Your rent is $2,100 a month. Electricity, internet, and renter's insurance add another $280. Your office takes up 15% of your apartment. Under the actual expense method, your deduction is $4,284 — not $1,000. That's $3,284 you left on the table. And because you're self-employed, that missing deduction cost you income tax and self-employment tax. The total overpayment: roughly $1,400 in a single year.

The simplified method exists because the IRS assumes you don't want to do the math. TurboTax doesn't warn you. Your accountant enters whatever numbers you hand them. Nobody sits you down and says: "Here is what each method actually produces for your specific housing costs, and here is which one you should pick."

That's what this guide does. The Home Office Tax Deduction Guide is a Multi-Country Deduction Optimization System — 14 chapters covering the US, Canada, Australia, and the UK, with the actual formulas, jurisdiction-specific rules, documentation templates, and long-term tax trap warnings that no free blog post, no tax software, and no $300/hour CPA appointment will walk you through in one place.

What's Inside the Multi-Country Deduction Optimization System

14 chapters, a quick-start checklist, and 11 standalone worksheets and templates. Each chapter solves a specific problem that remote workers and self-employed professionals face at tax time — not generic tax advice, but the exact rules, calculations, and documentation standards for your country. The standalone tools include a Simplified vs. Regular Comparison Worksheet, Square Footage and Apportionment Worksheet, Expense Tracking Worksheet, Depreciation Worksheet, Business Usage Log, Audit Defense Checklist, S-Corp Accountable Plan Template, Monthly Expense Report, T2200 Request Template (Canada), Rent-to-Company Lease (UK), and a Pre-Audit Preparation Checklist.

Who Qualifies and Who Doesn't

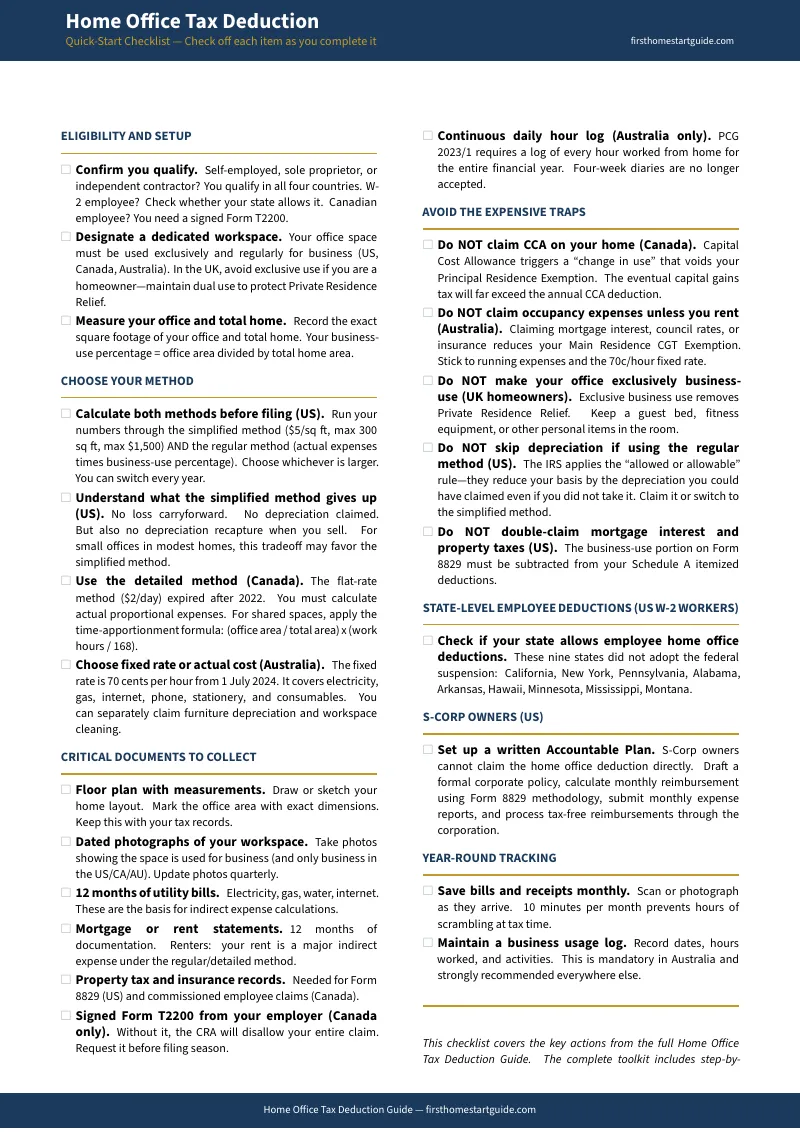

The eligibility rules are different in every country, and getting them wrong means your entire claim gets rejected. Self-employed in the US? You qualify. W-2 employee in the US? You don't — at the federal level. But nine states still let you claim home office expenses on your state return, and most people don't know that. Canadian employee? You need a signed Form T2200 from your employer, and without it, the CRA disallows everything. This chapter gives you a country-by-country matrix so you know exactly where you stand before you spend a minute on paperwork.

Simplified vs. Regular Method — The Decision That Costs People Thousands

Every country offers a simple flat-rate option and a complex actual-cost option. The flat-rate is always easier. It's also almost always smaller. This chapter runs both calculations side by side — US ($5/sq ft vs. Form 8829), Canada (detailed method with time apportionment), Australia (70 cents/hour vs. actual running costs), UK (flat monthly bands vs. proportional expenses) — so you can see exactly how much each method puts back in your pocket. You're not locked into one method. You can switch every year. But you need to know what you're giving up.

How to Calculate Your Home Office Deduction

The business-use percentage formula. Direct expenses vs. indirect expenses. How to split mortgage interest between Form 8829 and Schedule A without double-claiming. The Canadian shared-space calculation that factors in both floor area and hours worked per week. The Australian requirement to keep a utility bill for every category of expense you claim. Step-by-step, with the actual arithmetic, not "consult a professional."

What You Can and Can't Deduct — By Jurisdiction

A line-by-line breakdown of deductible expenses in each country. Mortgage interest is deductible in the US but not in Canada for employees. Rent is deductible everywhere except for UK employees. Furniture depreciation is handled differently in every jurisdiction. Internet is fully deductible in some countries and partially deductible in others. This chapter is the reference table you keep open next to your tax return.

The Exclusive Use Rule and Its Exceptions

The IRS doesn't require a separate room with a door. A clearly defined corner with a dedicated desk is enough. But a dining table you also eat dinner on? That fails the test. A guest bedroom with a desk and a bed? That fails too — unless you're in the UK, where mixing personal and business use in the same room actually protects your capital gains exemption. The two statutory exceptions (daycare facilities and inventory storage) that let you bypass exclusive use entirely.

S-Corp Accountable Plans (US)

S-Corp owners can't take a home office deduction on Schedule C or Form 1120S. But they can have their corporation reimburse their home office expenses tax-free through an Accountable Plan under IRC Section 280A. This chapter walks through drafting the plan document, setting up monthly expense reports, processing reimbursements through your corporate bank account, and keeping the arrangement off your W-2. Most CPAs don't set this up proactively. It saves S-Corp owners thousands per year.

State-Level Employee Deductions (US)

The federal deduction is gone for W-2 employees. But California, New York, Pennsylvania, and six other states still allow home office expenses on state returns. California even requires employers to reimburse remote work costs under Labor Code Section 2802 — and if they don't, you can claim them on Schedule CA. New York lets you itemize on Form IT-196 using pre-2018 federal rules. This chapter covers each state's specific forms, thresholds, and documentation requirements.

Canada — Form T2200, the Detailed Method, and the CCA Trap

The flat-rate COVID method is dead. Every Canadian claiming home office expenses now needs to use the detailed method with a signed T2200. This chapter covers the shared-space formula (area percentage × time percentage), the difference between salaried and commissioned employee deduction limits, and the critical warning: do not claim Capital Cost Allowance (depreciation) on your home. It triggers a "change in use" that voids your Principal Residence Exemption and creates a capital gains tax bill when you sell.

Australia — ATO Fixed Rate Method, PCG 2023/1, and the CGT Trap

The ATO's revised fixed rate (70 cents per hour) covers electricity, internet, phone, stationery, and consumables — but you must keep a continuous daily log of every hour worked from home. Four-week representative diaries are no longer accepted. And if you're a homeowner, claiming occupancy expenses (mortgage interest, council rates) reduces your Main Residence CGT Exemption. The capital gains tax hit when you sell will dwarf years of small deductions. This chapter shows you the safe path: running expenses only, with the documentation that survives an ATO review.

United Kingdom — HMRC Simplified Expenses, Rent-to-Company, and Private Residence Relief

Sole traders can use HMRC's flat monthly rates (£10, £18, or £26 depending on hours worked), but those only cover heating, light, and power — broadband, phone, rent, and council tax still need to be calculated separately. Limited company directors can charge rent to their own company for using a room as an office, reducing corporation tax. But if that room is used exclusively for business, you lose Private Residence Relief on that portion of the home. The fix: keep the room dual-use. This chapter includes the formal rental agreement structure and the dual-use documentation checklist.

Documentation and Audit-Proofing Your Claim

Floor plan sketches with measurements. Dated photographs of your workspace. 12 months of utility bills. A daily work-from-home log. A written Accountable Plan policy. The specific records each tax authority requires, what format they accept, and how long you need to keep them. The goal isn't just to claim the deduction — it's to claim it in a way that holds up if your return gets selected for review.

Depreciation Recapture and Long-Term Tax Traps

US homeowners who use the regular method must depreciate the business-use portion of their home. When they sell, that depreciation is "recaptured" and taxed at up to 25% — even if they never actually claimed the deduction. The IRS applies the "allowed or allowable" rule: if you could have claimed it, they reduce your basis as if you did. Canada's CCA trap works the same way. Australia's occupancy expense trap costs homeowners their CGT exemption. This chapter explains all three traps and shows you when the simplified method or running-expenses-only approach is the smarter long-term play.

Common Mistakes and Myths Debunked

No, claiming a home office does not automatically trigger an audit. No, you don't need a separate room with a door. No, the simplified method isn't always "safer." Yes, you can deduct your home office if you also rent a co-working space part-time. Fourteen myths that cost taxpayers money or scare them out of legitimate claims, debunked with the actual statute or ruling.

Year-Round Tracking and Record-Keeping System

A monthly tracking framework for expenses, hours, and documentation. What to log and when. How to organize digital receipts. The end-of-year reconciliation process that turns 12 months of records into the numbers you enter on your tax forms. Built so you spend five minutes a month during the year instead of eight hours in March.

Who This Guide Is For

- Freelancers and independent contractors who want to stop defaulting to the simplified method and claim their actual expenses

- Self-employed professionals and sole proprietors filing Schedule C, Form T2125, or as sole traders who need the calculation formulas for their specific country

- S-Corp owners who don't have an Accountable Plan set up and are leaving tax-free reimbursements on the table

- W-2 employees in California, New York, Pennsylvania, and other non-conforming states who don't realize they can still claim home office expenses at the state level

- Canadian remote workers navigating the detailed method after the flat-rate option expired

- Australian home-based workers who need to understand the CGT trap before claiming occupancy expenses

- UK limited company directors who want to rent a room to their own company without losing Private Residence Relief

Why Free Tools Get This Wrong

IRS Publication 587 is 34 pages of dense regulatory text with zero worksheets, zero calculators, and zero warnings about depreciation recapture. It tells you the rules exist. It doesn't help you apply them.

TurboTax and H&R Block are data-entry systems. They ask you to type in your home office expenses. They don't tell you which method produces a larger deduction. They don't warn you that depreciation recapture will cost you $12,000 when you sell your house in 15 years. They don't cover Canada, Australia, or the UK at all.

Blog posts from NerdWallet and Bench.co give you a 600-word overview of the simplified method and tell you to "consult a tax professional." They don't cover S-Corp Accountable Plans, state-level employee deductions, the Canadian time-apportionment formula, or the Australian CGT trap.

A CPA charges $150–$400 per hour. Most of them enter the summary numbers you provide. They don't proactively compare methods, build your documentation file, or set up an Accountable Plan unless you specifically ask. And one hour of their time costs more than this entire guide.

This guide fills the gap between "read the tax code yourself" and "pay a professional to do it for you." It gives you the formulas, the step-by-step calculations, the jurisdiction-specific rules, and the documentation templates — everything you need to claim your full deduction correctly and defend it if questioned.

Satisfaction Guarantee

If the guide doesn't help you identify at least one additional deduction or one documentation gap you weren't aware of, email us and we'll refund you in full. No forms. No time limit.

Get the Guide

Download the free quick-start checklist to see if you're making the most common mistakes. Or get the full Home Office Tax Deduction Guide for — 14 chapters, four countries, and the actual formulas your tax software doesn't show you.