Your Broker Said "4% DLD Fee Is Standard." He Didn't Mention Abu Dhabi Charges Half That. Your Developer Said "Escrow Protected." He Didn't Show You How to Verify It.

You have found a one-bedroom apartment in Dubai Marina. AED 1.8 million. The broker is RERA-licensed, the developer's sales gallery is pristine, and the payment plan looks manageable — 10% now, 60% during construction, 30% on handover. You are ready to transfer the deposit.

Then three things happen. The "4% DLD fee" the broker quoted turns out to be just the registration fee — on top of that, you owe 2% agent commission plus VAT, a trustee fee, mortgage registration at 0.25% of the loan, and DEWA deposits. Your total closing costs hit AED 140,000 — money you had budgeted for furniture. The off-plan unit you signed for has an Oqood registration number, but when you search it in the DLD REST app, the escrow account listed in the developer's SPA does not match the one on file with the regulator. And the ready property you looked at as a backup has a sitting tenant whose lease runs until next March — and under UAE tenancy law, you cannot evict them without serving a 12-month notarized eviction notice, even though you just bought the place to live in.

Each of these traps is well-documented in Arabic legal gazettes and brokerage whitepapers. None of them are assembled in one English-language resource designed for a foreign buyer making their first UAE property purchase.

Here is what no free resource puts together: The UAE combines a zero-tax property regime with a regulatory system that operates on rules found almost nowhere else — a dual-emirate framework where Dubai charges 4% registration and Abu Dhabi charges 2% for the identical legal outcome, an escrow law that physically locks your deposit away from the developer until an independent engineer certifies construction progress, a tenancy regime where ownership of the title deed does not give you the right to occupy your own property, an off-plan registration system (Oqood) that creates a verifiable ownership record before the building exists, and a Golden Visa pathway that no longer requires a cash down payment but does require understanding which property values qualify. Each of these has cost expat buyers tens of thousands of Dirhams because the information existed in DLD circulars, RERA bulletins, and Arabic-language court rulings — but nobody had assembled it into one system designed for a foreign buyer navigating their first UAE property transaction.

The Buying Property in Dubai & UAE — Expat Guide is a UAE Property Protection System — not a market overview or a brokerage FAQ, but a structured reference that maps every foreign-buyer-specific cost, legal mechanism, and regulatory trap across Dubai, Abu Dhabi, and the Northern Emirates into a process you work through before you commit capital. It replaces months of cross-referencing PropertyFinder listings, broker meetings, Reddit threads, and Google-translated regulations with one resource that tells you exactly what to verify, exactly what the numbers should look like, and exactly where foreign buyers lose money in the UAE.

What's Inside the UAE Property Protection System

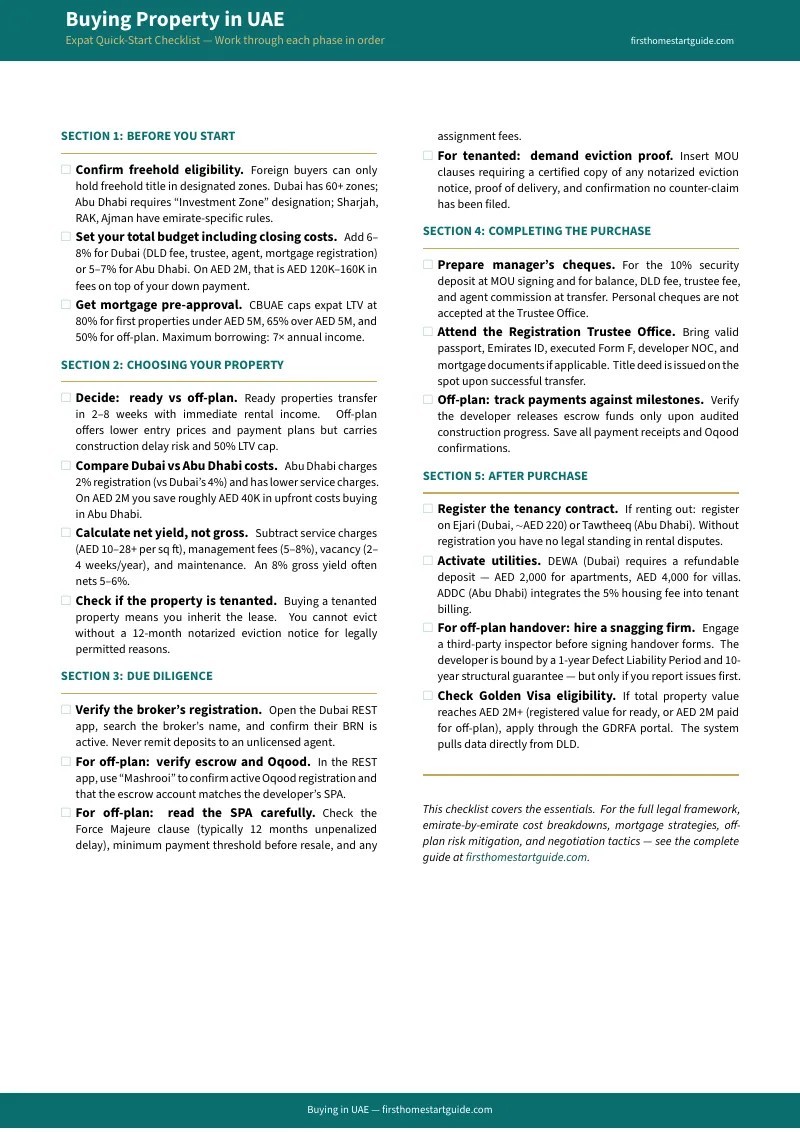

A 15-chapter guide and a 20-item verification checklist — covering every stage from freehold eligibility to post-purchase registration, built specifically for foreign buyers navigating the UAE's dual-emirate system:

Foreign Ownership Rules — Freehold Zones, Leasehold Limits, and the Emirate-by-Emirate Map

Foreign nationals can only buy freehold in designated zones — over 60 in Dubai, a growing list in Abu Dhabi's Investment Zones, and emirate-specific rules in Sharjah, RAK, Ajman, and Umm Al Quwain. Outside these zones, you are limited to 99-year leasehold or usufruct rights that restrict what you can do with the property. The guide maps every freehold zone by emirate and property type, explains the four ownership categories (freehold, leasehold, musataha, usufruct), and covers the legal distinctions that determine whether you own the land under your apartment or just the unit itself.

The Buying Process — Resale Properties (Form F to Title Deed in 2-8 Weeks)

Every Dubai resale begins with Form F — the digital MOU generated through the DLD REST app by a RERA-licensed broker. Paper contracts are void as of 2024. The guide walks through every step: the 10% security deposit, the developer NOC (including the AED 500-5,000 fee and the 5-business-day processing window), the mortgage valuation, the Registration Trustee Office transfer, and the moment the title deed is issued. For Abu Dhabi, it covers the parallel DARI platform process. Each step includes the specific documents you need, the fees you will pay, and the timeline you should expect.

The Buying Process — Off-Plan (The SPA, Payment Plans, and What "Completion" Actually Means)

Off-plan accounts for 65% of all UAE residential transactions, driven by staggered payment plans that eliminate the need for immediate full financing. But the Sale and Purchase Agreement contains clauses that determine your financial exposure if anything goes wrong — the Force Majeure clause (typically granting the developer 12 months of unpenalized delay), the minimum payment threshold before you can resell the contract, and assignment fees that can reach 2-4% of the property value. The guide dissects a standard SPA clause by clause, explains post-handover payment plans, and covers the specific protections and risks at each construction milestone.

Costs — Dubai vs. Abu Dhabi (The AED 40,000 Difference Nobody Advertises)

Dubai charges a 4% DLD registration fee. Abu Dhabi charges 2% through the DMT. On a AED 2 million property, that single difference saves you AED 40,000 — before you factor in Abu Dhabi's lower trustee fees, lower mortgage registration costs, and service charges that run 15-20% below comparable Dubai properties. The guide provides complete cost breakdowns for both emirates with worked examples at multiple price points, including the fees that brokers consistently forget to mention: DEWA/ADDC deposits, ejari/tawtheeq registration, property management setup costs, and the annual service charges that quietly erode your net yield.

Mortgages for Expats — CBUAE Caps, LTV Limits, and the 50% DBR Rule

The Central Bank caps expat financing at 80% LTV for first properties under AED 5 million, drops to 65% above that threshold, and limits off-plan mortgages to 50% LTV. Your total debt burden — all loans, credit cards, and the proposed mortgage — cannot exceed 50% of gross monthly income, with a maximum borrowing cap of 7x annual salary. The guide covers fixed vs. variable rates, the pre-approval process, how banks calculate your qualifying income (bonus, rental income, and overseas earnings are treated differently), and the specific documentation requirements that trip up foreign applicants.

Off-Plan Risks — Escrow Verification, Developer Due Diligence, and Your Legal Protections

The escrow system mandated by Law No. 8 of 2007 means your deposit sits in a project-specific account that the developer can only draw from in tranches, verified by independent engineers against actual construction milestones. But this only protects you if the escrow account is real. The guide provides the exact steps to verify escrow compliance, Oqood registration, and developer legitimacy through the DLD REST app — including how to use the Mashrooi service to confirm that the project's escrow account number matches the one in your SPA before you wire a single Dirham.

The Golden Visa — The 2026 Rules, the 1+1 Strategy, and What Actually Qualifies

The UAE removed the mandatory AED 1 million cash down payment requirement. Eligibility for the 10-year visa now requires AED 2 million in total property equity — and the properties can be off-plan, mortgaged, or split across multiple units. The guide explains how two AED 1 million apartments in mid-tier communities can secure your visa while delivering higher blended rental yields than a single AED 2 million luxury unit, covers the GDRFA application process, and clarifies which property valuations the system actually uses (registered value for ready properties, total amount paid for off-plan).

Renting Out Your Property — Ejari, Tawtheeq, DTCM Permits, and Yield Calculations

An 8% gross yield is not an 8% net yield. Annual service charges (AED 10-28+ per square foot in Dubai), property management fees (5-8%), vacancy periods, maintenance reserves, and DTCM licensing fees for short-term rentals collectively reduce your actual return by 2-3 percentage points. The guide provides the net yield calculation framework, covers the legal requirements for both long-term (Ejari in Dubai, Tawtheeq in Abu Dhabi) and short-term rentals, and explains the DTCM holiday home permit process for Airbnb-style operations.

The Tenant Eviction Trap — 12-Month Notice, Special Succession, and Your MOU Clauses

Buying a tenanted property does not give you the right to move in. Under Tenancy Law No. 26 of 2007, evicting a sitting tenant requires a 12-month notarized eviction notice served for legally permitted reasons — personal use or sale. But the "special succession" principle means that if the previous owner already served a valid eviction notice, you inherit the remaining timeline. The guide provides the exact MOU clauses to insert that make your purchase contingent on the seller providing proof of a pre-existing eviction notice, and covers the RDSC dispute process if the tenant challenges the eviction.

Common Mistakes — The Errors That Cost Expat Buyers the Most

Paying the full 4% DLD fee when the seller agreed to split it — but the MOU says "buyer pays." Budgeting for purchase price only and running short on closing costs. Buying in a trending community at a hype premium when an adjacent area offers better yields. Ignoring the resale market entirely because the payment plan looks attractive. Skipping the snagging inspection because the developer said "everything is covered under warranty." Each mistake is explained with the specific financial consequence and the prevention step.

Who This Guide Is For

- Expats living in the UAE considering their first property purchase — whether you are buying a family apartment to stop paying escalating rent or deploying capital for investment returns, and need to understand the complete legal and financial framework before engaging a broker

- Foreign investors buying remotely from outside the UAE — the entire purchase can be executed digitally through the REST app and a registered POA, but you need to know exactly which verifications to run and which documents to demand before wiring funds to a country you may not have visited

- Buyers evaluating Dubai vs. Abu Dhabi — who have seen the headline yields in Dubai but need a clear-eyed cost comparison showing how Abu Dhabi's lower registration fees and service charges can deliver superior net returns

- Off-plan buyers — who are attracted by payment plans and pre-construction pricing but need to independently verify escrow compliance, developer track records, and SPA terms before committing to a multi-year payment schedule

- Golden Visa applicants through property — who need to understand the current eligibility rules, which property values count, and how to structure purchases to meet the AED 2 million threshold while maximizing rental yield

Why Free Resources Leave You Exposed

Bayut, PropertyFinder, and Betterhomes publish excellent market reports — average prices per square foot, gross yield heatmaps, demographic trends. These are lead-generation tools designed to funnel you toward a specific brokerage's listings. They will highlight a community's 8% gross yield but will not show you the service charge schedule that reduces it to 5.5%. They will state that off-plan purchases are "RERA regulated" but will not walk you through the five-minute REST app verification that confirms whether a specific project's escrow account actually exists.

YouTube channels from Dubai brokerages provide valuable community walkthroughs and market commentary. They are sales vehicles for their own listings, incentivized to emphasize opportunity and minimize risk. They will never tell you that the community they are promoting has higher service charges than its competitor ten minutes away, or that the specific developer they are partnered with has a history of handover delays.

Reddit (r/dubai, r/dubairealestate) provides unfiltered peer sentiment — real buyers sharing real mistakes. But crowdsourced advice mixes accurate current information with outdated pre-2024 regulations, confuses Dubai law with Abu Dhabi law, and cannot replace a structured verification process that tells you exactly what to check in what order.

A property lawyer consultation in Dubai runs AED 1,500-3,000 per hour. This guide costs less than the trustee office fee and covers the complete scope of what you need to know before you hire one.

What You Get

8 PDFs — the complete guide, quick-start checklist, and 6 standalone printable tools you bring to every meeting:

- The full Guide (15 chapters) — freehold zones across all seven emirates, the resale buying process, the off-plan buying process, complete cost breakdowns for both Dubai and Abu Dhabi, expat mortgage rules, off-plan risk mitigation with escrow verification steps, Golden Visa eligibility and strategy, rental yield calculations, the tenant eviction trap and how to avoid it, selling procedures, common mistakes, market seasonality, and your legal protection checklist

- The Quick Checklist — 20 verification items grouped by purchase phase (Before You Start, Choosing Your Property, Due Diligence, Completing the Purchase, After Purchase) with the specific numbers, thresholds, and decision points for each step

- Dubai vs Abu Dhabi Cost Comparison Worksheet — side-by-side fillable worksheet for DLD/DMT fees, trustee costs, mortgage registration, and total closing costs with a worked example on a AED 2M property

- Off-Plan Verification Card — step-by-step REST app verification process, escrow account cross-referencing, and red-flag indicators to check before wiring any deposit

- Golden Visa Eligibility Checker — property value worksheet, ready vs off-plan qualification rules, the 1+1 strategy, required documents checklist, and GDRFA application steps

- Mortgage Affordability Calculator — income and debt inputs, CBUAE LTV reference table, DBR calculation, maximum borrowing, and conventional vs Islamic comparison

- Net Yield Calculator — gross-to-net yield worksheet covering service charges, management fees, vacancy, insurance, and maintenance with a worked example

- UAE Real Estate Glossary — every regulatory body, ownership type, transaction term, digital platform, and financial acronym you will encounter during the buying process

The free checklist covers what to verify at each stage. The full guide covers how — with the legal context, cost calculations, worked examples at multiple price points, and the specific verification procedures that turn each checklist item into an informed decision.

Satisfaction Guarantee

If the guide does not give you a clearer understanding of the UAE property system than everything you have read online combined, email [email protected] and we will make it right.

A single mistake in the UAE — paying the full DLD fee when the seller agreed to split, skipping escrow verification on an off-plan unit, buying a tenanted property without an eviction notice in place, or budgeting with gross yield instead of net — costs more than a full consultation with a Dubai property lawyer. The guide costs less than the DLD trustee office fee and covers the complete scope of what you need to know before you hire one.