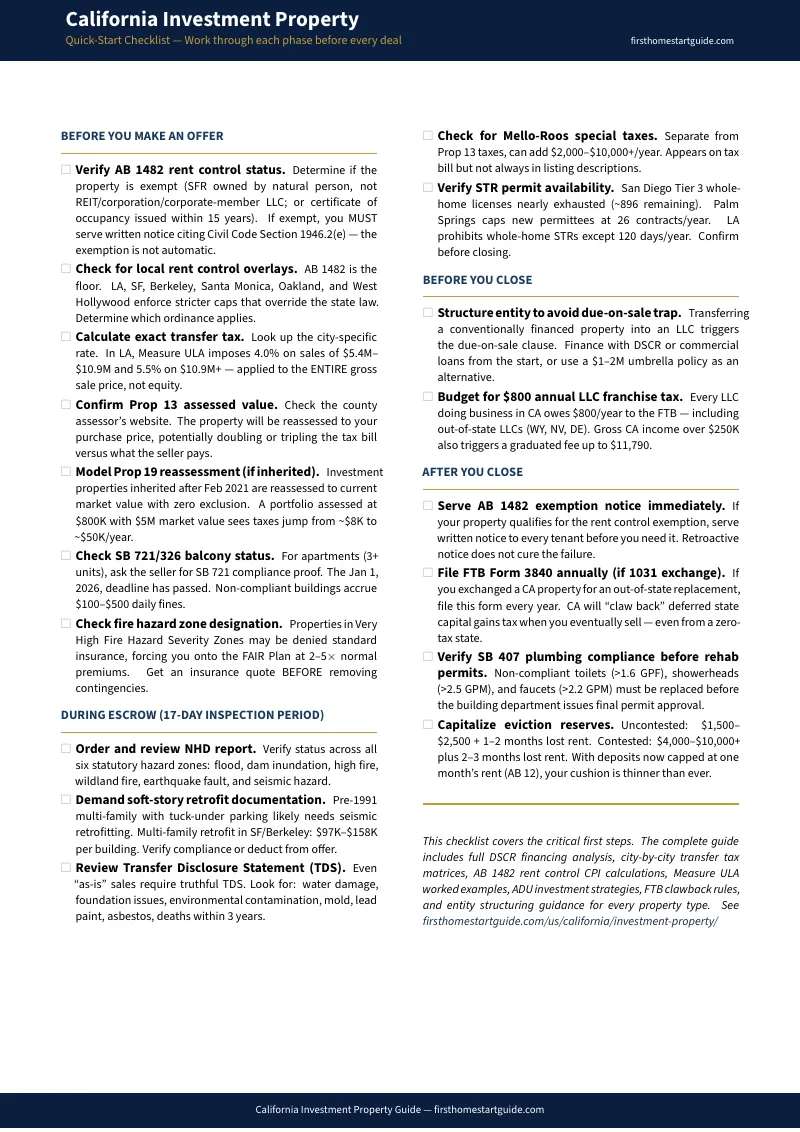

The Numbers Work. AB 1482 Exemption Traps, Measure ULA, and FTB Clawback Rules Will Make Sure They Don't.

You found a duplex in Sacramento projecting 5% gross yield with positive cash flow at 75% LTV. Or a 12-unit building in the City of Los Angeles with rents 15% below market. Or a single-family home in San Diego listed below replacement cost in a neighborhood where rents have climbed 30% in three years. The cap rate works. The DSCR clears. You're ready to wire earnest money.

Then you discover the LA building triggers Measure ULA at sale — a 4% tax on the gross price, not your equity, producing a $240,000 liability on a $6 million exit where your actual equity is $1.5 million. The Sacramento duplex is a 2013 build that just lost its 15-year rolling AB 1482 exemption, and you never served the required Civil Code Section 1946.2(e) notice, so the state treats you as fully subject to rent caps, just-cause eviction, and mandatory relocation assistance — retroactively. The San Diego home came from a family trust, and Proposition 19 reassesses every inherited investment property to current market value with no cap and no exception, turning the seller's $4,000 annual tax bill into your $15,000 overnight.

Here's what no single resource tells you: California layers a statewide rent control regime (AB 1482) where the exemption requires a specific written notice that most landlords never serve, municipal transfer taxes that can consume 16-24% of your actual equity on exit (Measure ULA in LA, 5.6% cliffs in Santa Monica, 2.61% flat rates in Berkeley), a Proposition 19 inheritance framework that eliminates the tax basis transfer for every investment property without exception, a Franchise Tax Board clawback that tracks your deferred capital gains through every 1031 exchange in perpetuity via Form 3840 — even if you move to a zero-tax state, and city-by-city rent control overlays (LA RSO, SF, Berkeley, Santa Monica, West Hollywood, Oakland) that override the state baseline with caps as low as 3-4%. Every one of these has cost real investors five to six figures because the information existed — scattered across county assessor websites, the DRE publications page, FTB form instructions, municipal housing department portals, and BiggerPockets threads mixing pre-2020 advice with current law — but nobody had assembled it into a single underwriting system.

The California Investment Property Guide is a California Investor Regulatory Navigation System — not a motivational overview of Golden State real estate, but a structured framework that maps every California-specific tax trap, transfer cost, compliance deadline, and regulatory restriction into a process you work through before you wire earnest money. It replaces months of cross-referencing FTB forms, county assessor databases, municipal housing ordinances, and outdated forum posts with a single reference that tells you exactly what to verify, exactly what the numbers should look like, and exactly where deals go wrong.

What's Inside the California Investor Regulatory Navigation System

A 12-chapter guide and a quick-start due diligence checklist — covering every stage from pre-acquisition analysis through ongoing compliance, built specifically for the tax structures, transfer costs, and regulatory complexity that make California different from every other state:

The Appreciation vs. Cash Flow Paradox

Every investing forum hammers the same mantra: a property must cash-flow from day one or it's a bad deal. By that standard, most of California looks terrible — San Diego gross yields sit at 3-4.8%, San Francisco hovers near 4-5%, Los Angeles barely touches 6%. The guide reframes the analysis around total return (appreciation + mortgage paydown + tax benefits + eventual cash flow), identifies the interior markets where cash flow works right now (Bakersfield at 5.4%, Fresno at 6.0%, Sacramento at 5.0%), and provides an honest California-vs-Sunbelt comparison table that quantifies why California's 150-250% historical 20-year appreciation dwarfs the Sunbelt's 60-100% — and why that matters more than year-one cash flow for investors with adequate reserves.

The Acquisition Process — Escrow, Timeline, and Closing Mechanics

California is an escrow state — no attorney required. The guide covers the standard 30-45 day timeline from the CAR Residential Purchase Agreement, the active contingency system where missed deadlines don't automatically cancel your deal (the seller must serve a Notice to Buyer to Perform first), the 17-day inspection window with every item you need to complete during it (TDS review, NHD report, SB 721/326 balcony compliance, Phase I ESA), and the vesting options for investors — individual name, revocable trust (protected from due-on-sale), LLC (triggers due-on-sale), and TIC for syndications.

Financing — DSCR Loans, Hard Money, Jumbo Loans

DSCR loans have become the dominant financing tool for portfolio investors because they ignore personal W-2 income entirely. The guide covers the DSCR formula with a worked Sacramento duplex example showing how adding an ADU shifts a 0.81 DSCR (disqualifying) to 1.15 (qualifying), the 2026 conforming loan limit ($832,750 baseline, $1,249,125 in high-cost counties), hard money bridge loan terms for fix-and-flip (8.5-12% interest, 90% purchase LTV, 12-18 month terms), cross-collateralization strategies for near-zero-down acquisitions, and no-ratio DSCR loans for coastal appreciation plays where negative leverage is the starting position.

Property Tax — Proposition 13, Proposition 19, and Reassessment Traps

Proposition 13 caps annual assessed value increases at 2% — but reassessment to current market value occurs on any change in ownership. The guide covers how Proposition 19 eliminated the intergenerational investment property transfer exclusion entirely (a portfolio with $800,000 assessed value and $5 million market value gets reassessed to $5 million on the day of inheritance, spiking the annual tax bill from $8,000 to $50,000), debunks the LLC myth (county assessors trace beneficial ownership through corporate structures), explains Mello-Roos special tax districts that add $2,000-$10,000+ annually to your tax bill, and maps the specific entity changes and improvement triggers that cause reassessment.

Rent Control — AB 1482, CPI Calculations, and Municipal Overlays

AB 1482 caps rent increases at 5% + regional CPI (maximum 10%) and imposes just-cause eviction requirements. The guide includes the complete 2025-2026 CPI table by county (San Diego 8.8%, LA/Orange 8.0%, SF/San Mateo/Marin 6.3%), the AB 1482 exemption decision flowchart (new construction, SFH/condo ownership structure, REIT exclusion), the written notice requirement under Civil Code Section 1946.2(e) that nullifies the exemption entirely if you fail to serve it, the municipal overlay matrix (LA RSO, SF, Berkeley, Santa Monica, West Hollywood, Oakland, San Leandro) where local caps as low as 3-4% override the state baseline, and the security deposit rules after AB 12 (one month maximum, with a two-month small landlord exception).

Evictions — Unlawful Detainer Process, Costs, and Timeline

The full Unlawful Detainer process mapped step by step: 3-day notice service, $435 filing fee, 5-day tenant response window (personal service) or 10 days (substituted service), the 4-6 week uncontested timeline versus the 2-3 month contested timeline, real cost breakdowns ($1,500-$2,500 uncontested, $4,000-$10,000+ contested), no-fault eviction relocation assistance requirements under AB 1482, and city-specific relocation payments that range from $8,000 to $22,000+ per tenant in Los Angeles. Plus the Ellis Act restrictions that prevent re-renting at market rates for five years after withdrawal.

Transfer Taxes — Measure ULA, City-by-City Matrix

The most dangerous underwriting blind spot in California real estate. The guide includes the complete city transfer tax matrix (LA Measure ULA at 4.0-5.5% on gross sale price, Culver City's marginal system, Berkeley's 2.61% flat rate above $1.6M, Santa Monica's 5.6% cliff above $8M, Oakland's progressive structure, San Francisco's steeply tiered rates up to $75/$1,000), a worked Measure ULA example showing how a $6M sale with $4.5M mortgage produces a $240,000 tax that consumes 16% of your actual equity, and strategic responses for properties approaching the $5.4M threshold.

Tax Strategy — Capital Gains, 1031 Exchanges, and FTB Clawback

California taxes all capital gains as ordinary income at rates up to 13.3% — no preferential long-term rate. The guide covers Form 593 real estate withholding (3.33% of gross sale price withheld at closing, with the alternative withholding election that can cut the cash flow hit in half), the 1031 exchange mechanics and deadlines, and the FTB clawback via Form 3840 that tracks California-source deferred gains in perpetuity. Move to Texas, 1031 into Florida, exchange again into Nevada — the original California gain follows you until you cash out. Plus cost segregation strategies, Real Estate Professional Status qualification (750-hour threshold), and Delaware Statutory Trust terminal exchange vehicles.

Due Diligence — Environmental, Seismic, SB 721/326, NHD Reports

The complete 17-day inspection period checklist: Natural Hazard Disclosure report interpretation (six statutory hazard zones including fire and seismic), the California insurance crisis (FAIR Plan premiums at 2-5x standard rates for fire zones, with fire-only coverage requiring a separate DIC policy), mandatory seismic soft-story retrofit costs ($3,000-$7,000 for single-family up to $158,500 for large multi-family), SB 721/326 balcony inspection requirements (the January 2026 deadline has passed and non-compliant properties accrue $100-$500 daily fines), Phase I/II environmental assessments, and SB 407 plumbing fixture replacement mandates.

Market Analysis — Best Submarkets, STR vs. LTR, ADU Strategy

Three submarket categories analyzed with realistic yield expectations: coastal appreciation plays (3-5% gross yield, negative cash flow, equity-building), suburban balanced markets (Sacramento, Long Beach, 5-7% yield), and interior cash-flow markets (Bakersfield, Fresno, 7-9% yield). Plus the complete STR regulatory breakdown by city (San Diego's Tier 3 cap at 1% of housing stock with only ~896 licenses remaining, Palm Springs' 32-contract annual limit, LA's host-present-only rule, SF's 90-day unhosted cap), the ADU strategy with a worked Long Beach case study showing a garage conversion that shifts gross yield from 4.8% to 6.3% while creating $20,000-$70,000 in forced equity, and the mid-term rental arbitrage (30-60% premium over LTR with zero STR permit requirements).

Property Management, Entity Structure, and LLC Considerations

Tenant screening standards after AB 12 security deposit caps (one month maximum), mandatory Section 8 voucher acceptance under SB 329, habitability requirements and repair-and-deduct rights, the $800 annual LLC franchise tax that applies even to out-of-state LLCs holding California property, the graduated gross receipts fee (up to $11,790 for LLCs with $5M+ income), the due-on-sale clause problem with LLC transfers and four specific workarounds, and a complete quick reference table of every key statute, form, and code section you need across all 12 chapters.

Plus 8 Standalone Printable Tools

Print these and keep them in your deal folder: an AB 1482 Exemption Decision Flowchart (five questions to determine rent control status), a City-by-City Transfer Tax Matrix with a worked Measure ULA example, a Rent Control Reference Card with 2025–2026 CPI tables and municipal overlays, a DSCR Calculator Worksheet for running the numbers on any deal, a 17-Day Inspection Checklist covering every California-specific escrow item, an FTB Clawback Tracker for annual Form 3840 filings, an Entity Structure Decision Guide comparing individual, trust, and LLC ownership, and a Statute Quick Reference with every key code section and form.

Who This Guide Is For

This guide is for real estate investors targeting California markets who:

- Are analyzing a California property and need to verify whether the deal actually works once you account for the correct municipal transfer tax rate, the AB 1482 rent cap and CPI calculation for their specific county, the Proposition 13 reassessment triggers, and the insurance costs that never appear in the seller's operating history

- Are under contract on a multi-family property and need to know whether it is subject to AB 1482, a local rent control overlay, or both — and what happens if you fail to serve the Section 1946.2(e) exemption notice before the tenant's first rent increase

- Are deploying capital from out of state and need to understand the $800 annual franchise tax for any LLC doing business in California (even one formed in Wyoming or Delaware), the 3.33% withholding on gross sale price at closing, the DSCR loan qualification process, and the FTB Form 3840 clawback that follows your capital gains across state lines indefinitely

- Are evaluating a 1031 exchange out of California into a landlord-friendly state and need to understand why the FTB's jurisdiction over your deferred gain never expires, what Form 3840 requires annually, and what triggers the clawback

- Plan to operate short-term rentals and need city-by-city clarity on permit caps (San Diego's Tier 3 is nearly full), annual contract limits (Palm Springs), host-presence requirements (LA, SF), and the mid-term rental alternative that avoids every STR restriction

- Want every California-specific regulation, tax calculation, transfer cost, environmental hazard, and compliance requirement in one reference — instead of assembling it from FTB forms, county assessor databases, municipal housing portals, DRE publications, and forum posts that still cite pre-2021 Prop 19 rules

Why Not Free Tools and Forums?

Free information on California real estate investing exists across hundreds of sources. Here's what it actually delivers:

- BiggerPockets and Reddit forums are where someone in a 2021 thread recommends forming a Wyoming LLC to hold California rental property for "asset protection and tax savings" — without mentioning that California requires foreign LLC registration and charges the $800 annual franchise tax regardless of where the LLC was formed, meaning you pay fees to both states. Someone else claims their single-family rental is exempt from AB 1482 without mentioning the written notice requirement that makes the exemption legally void if you never serve it. You'll find useful experience reports mixed with advice that predates Proposition 19's elimination of the investment property transfer exclusion, the AB 12 security deposit cap, and the Measure ULA threshold adjustments. Sorting current from outdated takes longer than reading a guide that has already done it.

- California Department of Real Estate (DRE) publications provide the statutes, the "California Tenants" guide, and the Real Estate Law reference book. They are written in legalese for licensing exam preparation, not for investors underwriting deals. You'll find the text of Civil Code Section 1946.2 but not a decision flowchart that tells you whether your specific property qualifies for the AB 1482 exemption based on its construction date, ownership structure, and whether you've served the required notice. The rules are there. The analysis that tells you whether to buy or walk is not.

- Nolo's California Landlord's Law Book is the industry standard for tenant relations and eviction procedure — 500+ pages of compliance guidance on lease preparation, security deposits, habitability standards, and discrimination law. But it is entirely defensive. It tells you how to manage a property you already own. It does not teach you how to underwrite a deal in Culver City's marginal transfer tax system, how to calculate the AB 1482 rent cap using the correct regional CPI for your county, how to structure entities to avoid Proposition 19 reassessment, or how to evaluate DSCR loan terms against hard money bridge financing for a fix-and-flip. You get the operating manual without the acquisition strategy.

- Real estate licensing courses teach agency law, fiduciary duty, and generic real estate finance. Investors take these to save on agent commissions, then discover the curriculum covers nothing about DSCR lending, cost segregation studies, Measure ULA avoidance strategies, Form 3840 clawback obligations, or multi-family syndication structures. You graduate with a license and zero operational knowledge of how California's tax and regulatory environment affects your actual return on invested capital.

- National investing books and courses teach cap rate, DSCR, and 1031 exchange mechanics that apply everywhere. They don't cover AB 1482's county-specific CPI calculations, the Measure ULA gross-value trap, Proposition 19's absolute elimination of investment property transfer exclusions, the FTB's perpetual clawback jurisdiction, California's insurance crisis in fire zones, or the ADU strategy that is the dominant method for forcing cash flow in expensive coastal markets. Applying national frameworks to California-specific problems is how investors lose six figures on their first deal.

This guide fills the California-specific gap — the space between knowing how to analyze a rental property in general and knowing how to underwrite one in a state where Measure ULA, AB 1482 exemption traps, Proposition 19 reassessment, the FTB clawback, municipal rent control overlays, and city-by-city transfer taxes can each independently turn a profitable deal into a losing one. It's the analysis that would take a California real estate attorney, a CPA with FTB specialization, and an insurance broker to assemble — structured as a reference you own permanently.

— Less Than One Filing Fee

A Measure ULA miscalculation on a $6 million LA building produces a $240,000 tax liability you never budgeted for. A single AB 1482 exemption notice you failed to serve triggers mandatory rent rollbacks, relocation assistance, and potential triple-damages lawsuits. A Proposition 19 reassessment on an inherited portfolio can spike your property tax from $8,000 to $50,000 in a single day. An FTB Form 3840 you forgot to file accelerates your deferred capital gains plus penalties and interest — even if you left California years ago.

This guide doesn't replace your California real estate attorney or your CPA. But it gives you the AB 1482 exemption decision flowchart, the city-by-city transfer tax matrix, the Proposition 19 reassessment analysis, the FTB clawback rules, and the due diligence checklist that ensure you identify every California-specific risk before you're contractually committed — instead of discovering them on your first compliance notice, your first tax filing, or your first eviction hearing.

If it catches a single transfer tax miscalculation, prevents a single AB 1482 exemption failure, or saves you from buying a property with an unresolved seismic retrofit obligation, it pays for itself before you've finished reading it.

30-day money-back guarantee. If the guide doesn't sharpen your underwriting and protect your capital in California's regulatory environment, you pay nothing.

Download the free California Quick-Start Home Buying Checklist to see the due diligence framework covering pre-acquisition verification, closing and tax compliance, post-closing obligations, and ongoing operations. When you're ready for the full AB 1482 analysis, transfer tax matrix, Proposition 19 strategy, FTB clawback rules, and 12-chapter investment system, the complete guide is here.

The deal looks good on the spreadsheet. This guide tells you whether California agrees.