The Property Pencils Out on Paper. Colorado Will Make Sure It Doesn't in Practice.

You found a duplex in Colorado Springs that throws off 5% gross yield. Or a mountain cabin near Breckenridge with $60,000/year STR revenue projections. Or a new-build in a Thornton master-planned community where the developer's brochure shows property taxes at $2,800/year. The cap rate works. The DSCR clears 1.25. You're ready to wire earnest money.

Then reality shows up. The Thornton property sits inside a Title 32 metro district with 42 additional mills that add $1,700/year in taxes the listing never mentioned — and the subdivision is only 60% built out, meaning that levy can climb to the service plan maximum if absorption slows. The Breckenridge cabin is in Zone 3, where STR licenses are non-transferable and the waitlist runs 10 to 15 years — the seller's license dies at closing, and your $850,000 purchase just became a long-term rental earning $2,200/month in a market where you need $4,800 to break even. The Colorado Springs duplex comes with a 2% wind/hail deductible on a $400,000 dwelling, meaning the first hail claim costs you $8,000 out of pocket before insurance pays a dollar.

Here's what no single resource explains: Colorado layers state-level tax constraints (TABOR, dual assessment rates, Gallagher repeal), municipality-by-municipality STR regulations (Denver's primary residence mandate, Breckenridge's four-zone caps, Summit County's basin limits), an insurance market in crisis from hail and wildfire exposure, and mountain-specific due diligence traps (Regulation 43 septic, cesspool phase-outs, well permits, expansive clay soils) into a regulatory environment that punishes investors who apply national assumptions to Colorado-specific problems. Every one of these has cost real investors five to six figures because the information existed — scattered across county assessor websites, municipal code PDFs, and forum threads from 2019 — but nobody had assembled it into a single underwriting system.

The Colorado Investment Property Guide is a Colorado Investor Underwriting System — not a motivational overview of real estate investing, but a structured due diligence framework that maps every Colorado-specific financial trap, regulatory restriction, and environmental risk into a process you work through before you wire earnest money. It replaces months of cross-referencing county tax records, municipal STR ordinances, insurance carrier policies, and state legislation with a single reference that tells you exactly what to verify, exactly what the numbers should look like, and exactly where deals go wrong.

What's Inside the Colorado Investor Underwriting System

A 13-chapter guide, a standalone 20-item due diligence checklist, and 8 printable worksheets and reference cards — covering every stage from market selection through post-purchase setup, built specifically for the financial traps and regulatory complexity that make Colorado different from every other state:

Metro District Mill Levy Analysis

The single most common underwriting failure in Colorado real estate investing. Metro districts created under Title 32 add 30 to 50 mills on top of standard county and school levies — an additional $1,360 to $5,000+ per year on a $500,000 property that directly degrades your cap rate and DSCR. The guide covers how to identify active metro districts, calculate true tax liability using Colorado's dual assessment rates (6.8% local government, 7.05% school district), evaluate under-buildout escalation risk when subdivisions are less than 70% absorbed, and use HB 25-1219 disclosure requirements to verify exact dollar amounts before closing. Without this analysis, properties that pencil as cash-flow-positive become negative-yield liabilities once you account for the actual levy.

STR Regulatory Matrix by Jurisdiction

Colorado has no statewide STR framework — every municipality sets its own rules. Denver restricts STR licenses to primary residences with 185 days/year occupancy enforced through utility cross-referencing and private investigator surveillance. Breckenridge uses a four-zone cap system where Zone 3 licenses carry 10-15 year waitlists and are non-transferable on sale. Summit County imposes basin-level caps with several basins already over capacity. The guide maps license availability, zone caps, waitlist lengths, annual regulatory costs ($2,400+/year in Breckenridge), and the specific MTR and ADU workarounds that create legal paths to furnished rental income in restricted markets. Buying a mountain property for STR revenue without verifying license transferability first is how investors turn $850,000 acquisitions into $2,200/month long-term rentals.

Insurance Crisis Underwriting

Colorado is a dual-catastrophe state: Front Range hail and mountain wildfire. Carriers have shifted to 1-2% percentage-based wind/hail deductibles — on a $400,000 dwelling, that's $8,000 out of pocket before insurance pays anything. In WUI zones (Evergreen, Conifer, the I-70 corridor), annual hazard premiums run $4,500 to $18,000, equivalent to the carrying cost of an additional $130,000 in mortgage debt. The guide breaks down RCV vs. ACV policy economics, Class 4 impact-resistant shingle discounts, FAIR Plan qualification and limitations ($750,000 cap, ACV-only, fire and wind only), DIC wraparound structuring, and your new rights under HB 25-1182 to challenge wildfire risk scores with documented mitigation. An insurance renewal that doubles your premium after year one isn't a surprise — it's a predictable event you should have underwritten from day one.

Mountain Due Diligence Protocol

Mountain and rural properties introduce physical and legal risks that don't exist in metro markets. Under updated Regulation 43, converting a residential cabin to an STR sleeping 8 guests can trigger mandatory septic system re-evaluation and a $15,000 to $30,000 advanced treatment installation — even without structural changes. Twenty-two Colorado counties require compulsory Transfer of Title septic inspections before closing. Cesspools are no longer grandfathered. The guide covers septic compliance by county, well permit verification with DWR, 48-hour continuous radon monitoring (Colorado is EPA Zone 1 — highest risk), and expansive clay soil inspection on the Fort Collins-to-Pueblo Front Range corridor where foundation stabilization runs $15,000 to $60,000. Skipping any one of these turns your inspection contingency period into a liability.

Property Tax Mechanics and TABOR Analysis

Colorado's property tax system is unlike any other state. The TABOR Amendment limits tax increases without voter approval — but de-Brucing votes have removed those limits in many districts, meaning your taxes can rise faster than you expect when values appreciate. The Gallagher Amendment repeal shifted assessment rate control to the legislature, which created the current dual-rate system. The guide walks through step-by-step tax calculations using actual assessment rates, the biennial reassessment cycle, and the formal protest process that saves many investors thousands per year on inflated valuations. Running your underwriting on estimated tax rates instead of actual mill levy breakdowns is how metro district surprises happen.

Colorado Landlord-Tenant Law and Eviction Framework

HB24-1098 eliminated no-cause lease terminations in Colorado. You must offer renewals by default and can only terminate for specific statutory grounds. The guide covers the cause-required eviction framework, security deposit rules, radon disclosure requirements under SB23-206 (landlords must mitigate within 180 days of tenant notice or face lease voidability), and habitability standards. Budget extra holding time and legal costs into your underwriting — this is not a landlord-friendly state for investors accustomed to month-to-month flexibility.

Market-by-Market Investment Analysis

Six metro markets dissected with median listing prices, median rents, gross yields, vacancy trends, and demand drivers: Denver Metro ($545k median, 3.55% yield, appreciation play), Colorado Springs ($460k, 4.22% yield, military demand), Fort Collins ($585k, 3.9% yield, university market), Boulder ($995k, 2.29% yield, building cap constrained), Grand Junction ($480k, 4.49% yield, Western Slope cash flow), and Pueblo ($285k, 5.58% yield, lowest entry point). Know which game you are playing before you deploy capital.

Financing, Tax Strategy, and Entity Structuring

Conventional, DSCR, second-home, FHA house hack, and hard money financing compared by down payment, rate, and qualification method. Cost segregation and bonus depreciation strategies for accelerated write-offs. The STR tax loophole (material participation reclassification to offset W-2 income). 1031 exchange mechanics. Colorado LLC formation, registered agent requirements, and the operational risk of a delinquent LLC — a Colorado LLC that fails to file its Periodic Report cannot initiate eviction proceedings, potentially trapping you with a non-paying tenant until the entity is brought current.

Who This Guide Is For

This guide is for real estate investors targeting Colorado markets who:

- Are analyzing a Colorado property and need to verify whether the deal actually works once you account for metro district mill levies, actual insurance costs, and municipality-specific STR restrictions — not the generic tax and revenue assumptions that work in Texas or Florida

- Are under contract and the title commitment just revealed a metro district encumbrance, a septic system that needs Transfer of Title inspection, or an STR license that doesn't transfer — and need to understand the financial implications before your inspection contingency expires

- Plan to operate short-term rentals in mountain markets and need to verify license availability, zone caps, waitlist lengths, and annual regulatory costs before making an offer on a property whose entire ROI thesis depends on STR revenue

- Just received an insurance renewal with a 2% wind/hail deductible or a $12,000 WUI premium and need to restructure coverage (FAIR Plan, DIC wraparound, Class 4 shingle discounts, HB 25-1182 mitigation credits) before the numbers stop working

- Are house-hacking or building an ADU in Denver and want to understand the legal path to furnished rental income within city limits without violating the primary residence STR mandate

- Want every Colorado-specific regulation, tax calculation, and due diligence requirement in one reference — instead of assembling it from county assessor websites, municipal code PDFs, and BiggerPockets threads that may have been accurate two legislative sessions ago

Why Not Free Tools and Forums?

Free information on Colorado real estate investing exists across dozens of sources. Here's what it actually delivers:

- BiggerPockets forums are where someone in a 2021 thread says Breckenridge STR licenses transfer on sale, someone in 2023 says they don't, and a moderator links to a town ordinance that's been amended twice since. You'll find genuinely useful experience reports mixed with advice predating HB24-1098 (cause-required eviction), the Gallagher repeal, Regulation 43 updates, and the HB 25-1219 metro district disclosure law. Sorting current from outdated takes longer than reading a guide that has already done it.

- County assessor websites give you mill levy rates for a specific parcel. They don't calculate how the dual assessment rate system (6.8% vs. 7.05%) affects your total tax liability, don't flag metro district under-buildout escalation risk, and don't tell you that a de-Bruced district can capture unlimited revenue growth when values appreciate. You get the data without the analysis that determines whether the deal works.

- National investing books and courses teach cap rate, DSCR, and 1031 mechanics that apply everywhere. They don't mention TABOR, metro districts, non-transferable STR licenses, percentage-based hail deductibles, Regulation 43 septic triggers, or cause-required eviction. Applying national frameworks to Colorado-specific problems is how investors lose five figures on their first deal.

- Pre-licensing courses focus on passing the Colorado real estate exam, not on investment underwriting. They cover agency law and contract procedures. They don't cover mill levy analysis, DSCR calculations, insurance structuring, or the STR regulatory matrix that determines whether your revenue projections are legal.

This guide fills the Colorado-specific gap — the space between knowing how to analyze a rental property in general and knowing how to underwrite one in a state where metro district taxes, STR license caps, dual-catastrophe insurance, and mountain due diligence requirements can each independently turn a profitable deal into a losing one. It's the analysis that would take a Colorado-specialized real estate attorney, a property tax consultant, and an insurance broker to assemble — structured as a reference you own permanently.

— Less Than One Metro District Tax Surprise

A single metro district mill levy you failed to catch adds $1,700 to $5,000 per year to your carrying costs — every year you own the property. An insurance renewal with a percentage-based hail deductible creates $8,000 in unexpected out-of-pocket exposure on the next storm. A non-transferable STR license in Breckenridge Zone 3 can erase $40,000 to $60,000 in projected annual revenue the day you close. A Regulation 43 septic upgrade on a mountain STR conversion runs $15,000 to $30,000.

This guide doesn't replace your real estate attorney or your CPA. But it gives you the mill levy analysis framework, insurance structuring strategies, STR regulatory matrix, and mountain due diligence protocol that ensure you identify every Colorado-specific risk before you're contractually committed — instead of discovering them on your first tax bill, your first insurance renewal, or your first denied STR license application.

If it catches a single metro district levy, prevents a single insurance structuring mistake, or saves you from buying a property whose STR license doesn't transfer, it pays for itself before you've finished reading it.

30-day money-back guarantee. If the guide doesn't sharpen your underwriting and protect your capital in Colorado's regulatory environment, you pay nothing.

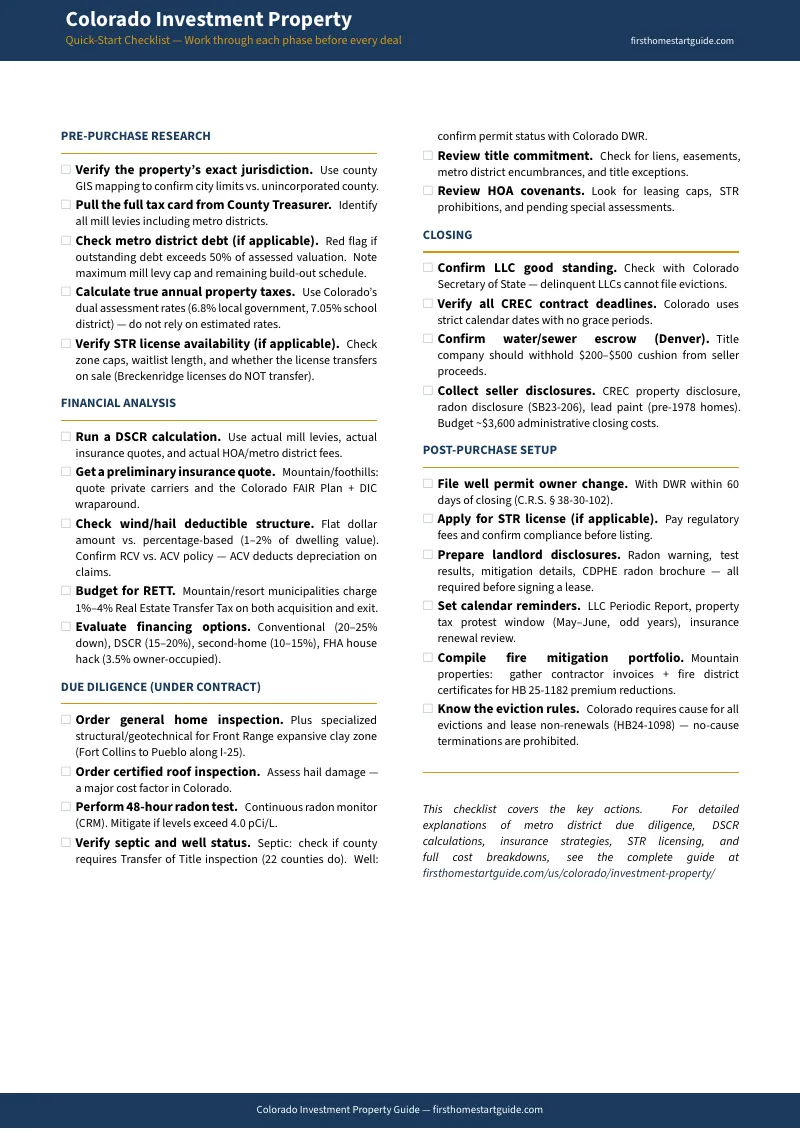

Download the free Colorado Quick-Start Checklist to see the 20-item due diligence framework covering pre-purchase research, financial analysis, under-contract inspections, closing, and post-purchase setup. When you're ready for the full metro district analysis, STR regulatory matrix, insurance crisis underwriting, and 13-chapter investment system, the complete guide is here.

The deal looks good on the spreadsheet. This guide tells you whether Colorado agrees.