Your Pre-Approval Means Nothing Until You Know the Mill Rate

You got pre-approved for $400,000. You found a home in your price range. Then your lender ran the numbers for that specific town and told you the property tax escrow alone pushes your debt-to-income ratio past the limit. You are disqualified — not because of the home price, but because of a mill rate you did not know existed until this moment.

This happens constantly in Connecticut. A home in Greenwich generates $3,371 in annual property taxes. The exact same home in Hartford generates $19,306. That is a $15,935 difference on identical purchase prices, and it is the single variable that determines whether your mortgage gets approved or denied. No national home buying guide covers this. No online calculator gets it right. And your real estate agent is not going to walk you through the 70% assessment formula while you are standing in an open house.

Then there is the rest of what makes Connecticut unlike any other state: the attorney you are legally required to hire, the underground oil tanks that can turn a $4,000 removal into a $60,000 environmental remediation, the crumbling pyrrhotite foundations in Eastern Connecticut that cost $150,000 to replace, the conveyance tax that makes sellers refuse to negotiate, the heating oil reimbursement that nobody mentions until you are sitting at the closing table writing an unexpected check for $1,000, and the CHFA assistance programs where the eligibility rules changed in 2024 and most websites have not caught up.

The Connecticut Closing Cost Navigator

The Connecticut First-Time Home Buyer Guide is not a generic home buying overview with Connecticut sprinkled on top. It is a closing cost navigator built specifically for the state's 169-municipality tax maze, the attorney-closing mandate, and the environmental hazards that exist nowhere else in the country in this combination.

National guides tell you to "get pre-approved and make an offer." This guide tells you to calculate the mill rate for every town you are considering, verify your CHFA eligibility by planning region, schedule a tank sweep within 48 hours of contract execution, check whether you are buying inside the 20-mile pyrrhotite radius around Stafford Springs, and budget an extra $500 to $1,000 for the heating oil proration that will appear on your closing statement without warning. The difference between these two approaches is the difference between closing on time and watching your deal collapse three days before the mortgage contingency deadline.

What's Inside

The Mill Rate Decision Framework — the 70% assessment formula explained once, clearly, with worked examples showing the true monthly cost at every major Connecticut mill rate from Washington (10.85) to Hartford (68.95). Side-by-side comparison tables so you can model five towns before you tour a single house. Includes special taxing districts, the motor vehicle mill rate cap spillover that silently raises your real estate taxes, and the 5-year revaluation cycle that can spike your assessment overnight.

CHFA Stacking Strategy — how to combine a CHFA first mortgage with the Down Payment Assistance Program (up to $15,000) or the Time to Own forgivable loan (up to $25,000 at 0% interest, forgiven over 10 years) to create effective near-zero-down financing. The 2024 policy change that eliminated DAP + TTO stacking, the income limits and sales price limits by planning region, the Targeted Area rate reduction, and the eHome America course requirement that causes last-minute closing delays when you leave it until the end. Plus municipal grants most buyers do not know exist: HouseHartford ($40,000), New Haven ($20,000), Bridgeport ($15,000), and SmartMove/HDF (up to 25% of the purchase price at 3%).

The Environmental Inspection Sequence — which inspections to order based on your specific property (oil heat history, year built, proximity to Stafford Springs, private well, septic system, flood zone), what each costs, how to schedule all of them simultaneously within a 10-to-15-day contingency window, and the walk-away thresholds. The UST cost escalation from $300 tank sweep to $60,000+ contamination remediation. The pyrrhotite testing protocol and CRCOG reimbursement program. Well water testing for arsenic, uranium, and radon — and why FHA loans require proof of 3-5 GPM flow. The septic regulatory gap that means nobody will tell you the system is failing unless you hire the right inspector.

Complete Closing Cost Breakdown — every line item on a Connecticut closing statement: attorney fees by region, title insurance rates, MERS recording fees, tax escrow calculations using your town's actual mill rate, the heating oil proration procedure, and the conveyance tax brackets that explain why your seller will not negotiate the way you expect. A worked example on a $450,000 purchase showing how CHFA TTO plus seller concessions reduces out-of-pocket costs below $10,000.

Regional Market Intelligence — five distinct Connecticut markets with different strategies for each. Fairfield County for NYC relocators (high prices, low mill rates, $977,500 conforming limit). Hartford metro for CHFA-heavy buyers (affordable prices, devastating mill rates, municipal grant stacking). New Haven for house hackers (multi-family CHFA financing, Yale economy). Eastern Connecticut for pyrrhotite-aware buyers. Litchfield County for rural purchasers navigating private wells, septic systems, and radon.

The 45-to-60-Day Timeline — the full sequence from binder (Northern CT) or direct contract (Lower Fairfield County) through attorney review, inspections, mortgage contingency, clear-to-close, and deed recording. Where CHFA loans add time, where municipal grant coordination adds complexity, and exactly when you need to have completed each step to avoid deadline failures.

The Recapture Tax Myth — why the CHFA federal recapture tax scares thousands of buyers away from the state's best financing programs, even though it requires three conditions to trigger simultaneously (sale within 9 years, net gain, and income exceeding federal limits) and is capped at 6.25% of your highest loan principal. CHFA even reimburses you if it does trigger. This section alone can save you tens of thousands in avoided interest by keeping you on CHFA financing instead of pushing you toward conventional loans out of misplaced fear.

Printable Worksheets Included

- Mill Rate Comparison Worksheet — input any purchase price, apply the 70% assessment formula, calculate annual and monthly tax for any Connecticut town, compare up to five municipalities side by side

- Closing Cost Calculator — every buyer-side cost line item, CHFA DAP or TTO offset modelling, seller concession scenarios, net cash to close

- Environmental Inspection Decision Matrix — which inspections to order by property characteristics, cost, timeline, and walk-away criteria

- CHFA Eligibility Worksheet — income limits by region and household size, sales price limits, Targeted Area lookup, DAP vs TTO comparison

Who This Is For

- First-time buyers anywhere in Connecticut who need to understand mill rates, CHFA programs, and the attorney-closing process before making an offer

- NYC relocators moving to Fairfield County who assume their pre-approval from New York translates directly to Connecticut buying power

- Buyers using CHFA, DAP, TTO, or municipal grants who need to understand the stacking rules and eligibility requirements across planning regions

- Anyone purchasing a pre-1985 home who needs to navigate underground storage tank liability, lead paint, and radon testing

- Buyers in Eastern or Central Connecticut who need the pyrrhotite inspection playbook before making offers in affected towns

- Anyone buying a property with a private well or septic system who does not yet understand what Connecticut's regulatory gaps mean for their liability

Why Generic Guides Fail in Connecticut

National home buying books do not explain the attorney-closing mandate. They do not cover the conveyance tax. They do not know what a mill rate is. They have never heard of pyrrhotite. They do not mention oil tank sweeps because most states do not have widespread underground heating oil infrastructure. They estimate your closing costs using national averages that undercount the attorney fees, the MERS recording surcharge, and the heating oil proration that hits you at the closing table.

Free CHFA resources explain program rules but not strategy. They will not tell you whether DAP or TTO leaves you better off over ten years. They will not model the DTI impact of choosing one town over another. They will not show you how to stack a municipal grant on top of CHFA financing to create effective 100% financing. They answer individual questions — they do not connect the dots into a path from pre-approval to closing.

Zillow and Realtor.com get Connecticut property taxes wrong because they use county-level or state-level estimates. Connecticut does not have county-level taxation. Every calculation they show you is meaningless. SmartMLS is the source of truth for 96% of the state's listings — but national platforms do not tell you that, and they do not pass through the localized tax data correctly.

The Free Checklist Gets You Started

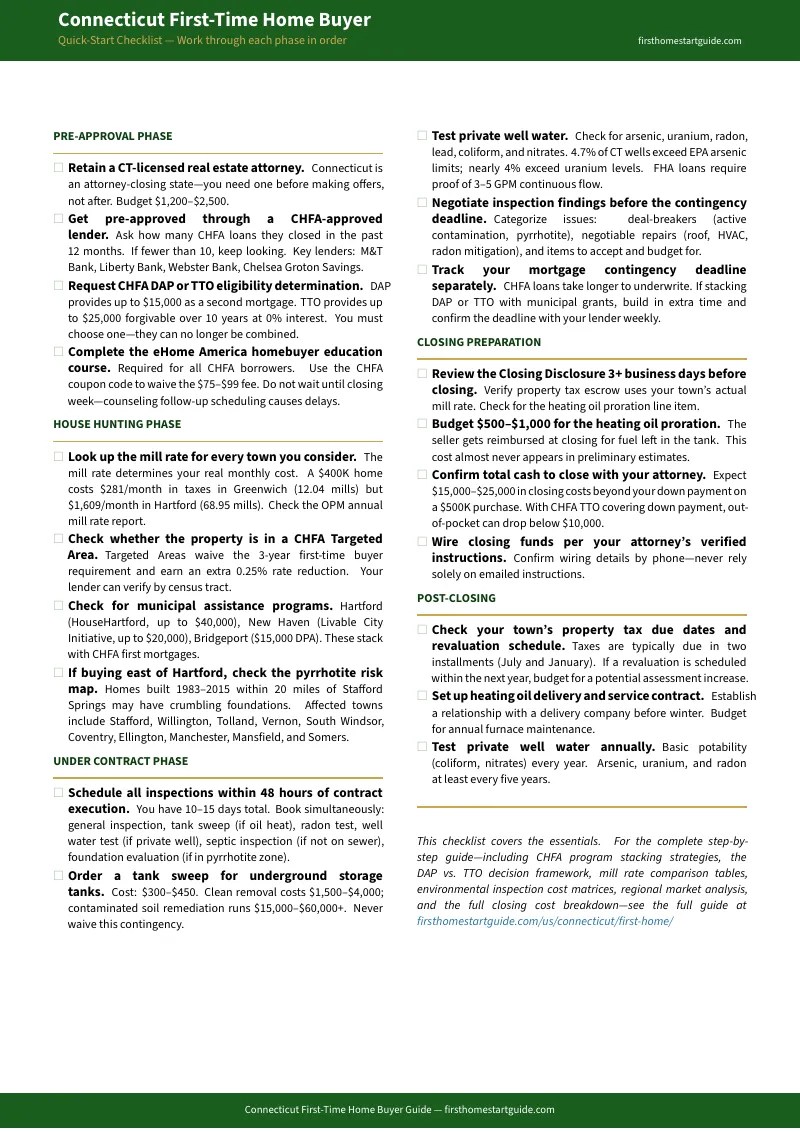

Download the Connecticut Quick-Start Home Buying Checklist — 20 actionable items organised by phase (pre-approval, house hunting, under contract, closing prep, post-closing) with the Connecticut-specific details your realtor may not mention. It covers the CHFA lender selection criteria, the mill rate lookup process, the environmental inspection schedule, and the closing cost line items unique to Connecticut.

The checklist tells you what to do. The full guide tells you how — with the math, the strategy, the worked examples, and the worksheets that turn each step into a decision you can make with confidence.

Get the Connecticut First-Time Home Buyer Guide — , instant download. Start with the Mill Rate Comparison Worksheet to find the towns where your pre-approval actually works, then work through the CHFA eligibility worksheet to lock in the best financing stack available for your income and region.