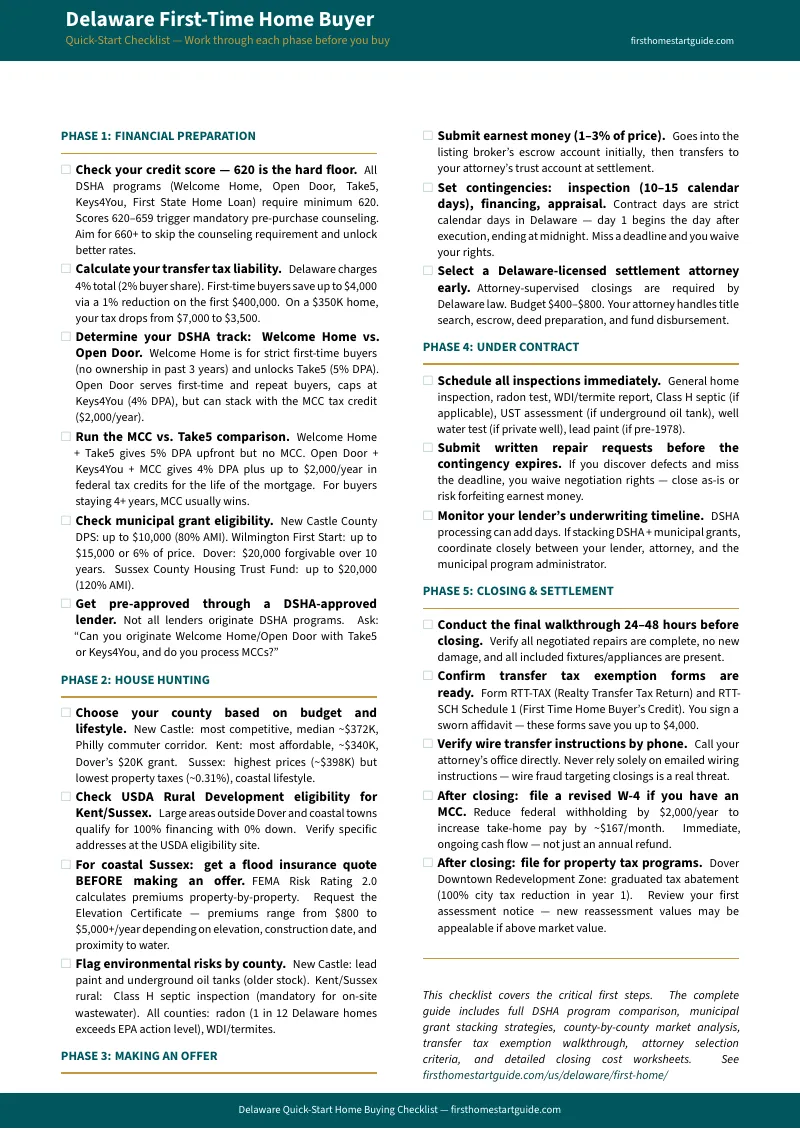

Delaware's Low-Tax Promise Has a $7,000 Catch at the Closing Table

You heard Delaware has no sales tax, no estate tax, and property taxes that barely register. You ran the numbers. You decided to buy here. Then your lender sent the closing cost estimate and the transfer tax line item wiped out your budget.

Delaware charges a 4% real estate transfer tax — your share is 2%. On a $350,000 home, that is $7,000 in transfer taxes alone. Add it to your down payment, attorney fees, title insurance, and recording costs, and first-time buyers routinely face $12,000 to $15,000 in total closing costs. More than double what national calculators predict.

The irony is brutal: Delaware offers some of the most generous down payment assistance and tax credit programs in the country. But the programs are scattered across three state tracks, four municipal grant systems, and a federal tax credit with stacking rules that most loan officers get wrong. Buyers who do not know the system leave thousands of dollars on the table. Buyers who know exactly which forms to file, which programs to stack, and which track to choose can cover nearly all of their closing costs with assistance money.

The Delaware Closing Cost Playbook — Every Program, Every Dollar, Every Form

This is not a generic home buying checklist with "check your credit score" and "find a real estate agent." This is a Delaware-specific system that decodes every state, county, and municipal program, calculates the exact math, and tells you precisely which combination puts the most money in your pocket at closing.

What Makes This Different from Free Guides

The DSHA website lists program names. Real estate blogs mention the transfer tax exemption. But none of them do the math for you, explain the stacking rules, or warn you about the traps.

Free guides will not tell you that the Mortgage Credit Certificate cannot be combined with the Welcome Home program — that it pairs only with Open Door. They will not explain that choosing Open Door + Keys4You + MCC generates more total value than Welcome Home + Take5 for any buyer staying four or more years. They will not calculate that a Kent County buyer purchasing a $280,000 home in Dover can stack over $45,000 in combined assistance by layering DSHA, Home Sweet Home, and the Dover municipal grant.

National guides have no idea that Delaware requires a licensed attorney at every closing, that Sussex County charges different transfer tax rates than New Castle County municipalities, or that FEMA Risk Rating 2.0 makes flood insurance a property-by-property gamble along the coast. The free content covers Delaware in a paragraph. This guide covers Delaware in twelve chapters with embedded calculators, program comparison tables, and county-by-county market intelligence.

Everything Inside

The Transfer Tax Decoded — The full 4% structure broken down: 2.5% state plus 1.5% county, split evenly between buyer and seller. The first-time buyer exemption mechanics: 0.5% state reduction plus 0.5% county reduction on the first $400,000, capped at exactly $4,000. The joint-purchase disqualification rule. Municipal variations for Wilmington, Dover, and Sussex County towns. Anti-circumvention ordinances. Worked calculations at four price points. Form RTT-TAX and RTT-SCH Schedule 1 filing instructions.

Every DSHA Program Compared Side by Side — Welcome Home vs. Open Door eligibility. Smart Start, First State Home Loan (3% DPA), Keys4You (4% DPA), Take5 (5% DPA — Welcome Home only), and Diamond in the Rough (5% DPA for renovation loans). Home Sweet Home ($12,000 forgivable over 10 years for homes under $285,000). Delaware Diamonds ($10,000 forgivable for essential workers). Full comparison table with eligibility criteria, DPA amounts, forgiveness timelines, and stacking compatibility.

The Mortgage Credit Certificate Strategy — The 35% federal tax credit on mortgage interest, capped at $2,000 per year for the life of the loan. How to adjust your W-4 for an extra $167/month in take-home pay. The three-year carryforward for unused credits. The critical stacking limitation with Welcome Home. The Welcome Home + Take5 vs. Open Door + Keys4You + MCC decision framework with breakeven analysis.

Municipal and County Grants — New Castle County DPS ($10,000, 0% interest, payments deferred two years). Wilmington First Start (up to $15,000 or 6% of purchase price, dual income pools). Dover Homeownership Assistance ($20,000 forgivable after 10 years, plus graduated downtown tax abatement). Sussex County Housing Trust Fund ($20,000, available to repeat buyers, 120% AMI eligibility). Income limits, personal contribution requirements, and stacking rules for each.

Attorney-State Closing Process — Why Delaware requires a licensed attorney at every closing, what they do, what they charge, and how the escrow and title process works. Deed types explained. Title insurance strategy. The 30-to-45-day settlement timeline mapped step by step.

Environmental Due Diligence Checklist — Class H septic inspections for Kent and Sussex counties. Underground oil tank liability in older Wilmington-area homes and DNREC's tank closure assistance program. Radon testing (1 in 12 Delaware homes exceeds the EPA action level). WDI reports. Lead paint inspections. Well water testing. FEMA Risk Rating 2.0 for coastal Sussex County — why you need an Elevation Certificate and an actual flood insurance quote before making a binding offer.

County-by-County Market Guide — New Castle County (Philly commuter corridor, median ~$372K, intense competition, financial services and healthcare employment). Kent County (most affordable at ~$340K, Dover AFB anchor, VA loan utilization, massive USDA-eligible rural zones, the $20K Dover grant). Sussex County (highest prices at ~$398K but lowest property taxes at 0.31%, seasonal pricing dynamics, HOA and flood insurance cost layering).

Property Tax Reassessment — Delaware's historic reassessment from 1974, 1983, and 1987 base-year valuations to current market values. Revenue neutrality explained. What the reassessment means for your tax bill and future assessments. Appeal rights.

Financing Strategy Framework — FHA, VA, USDA Rural Development, and conventional loans compared for each Delaware county. Which financing type pairs best with which DSHA track. The maximum stacking scenario calculated.

Bidding Strategy for Competitive Markets — Inspection gap waivers, escalation clauses, and appraisal gap coverage specifically for New Castle County's $300K–$400K battleground. Risk-mitigation tactics so you stay competitive without taking on dangerous exposure.

6 Standalone Printable PDFs — Transfer tax calculator. DSHA program eligibility self-assessment. Closing cost estimator. Delaware inspection checklist. Municipal grant comparison worksheet. Monthly cost projection with DTI and insurance variables.

Who This Is For

- First-time buyers anywhere in Delaware — Wilmington, Newark, Middletown, Dover, Lewes, Rehoboth Beach, or rural areas

- Philly commuters crossing into New Castle County for lower property taxes who need the full trade-off analysis including the transfer tax

- Military families at Dover Air Force Base navigating VA loans alongside DSHA assistance and the Dover $20K grant

- Remote workers relocating to Sussex County's coast who have never dealt with flood insurance, seasonal pricing, or HOA-heavy markets

- Anyone earning under DSHA income limits who wants to know exactly which programs stack and how to maximize their combined assistance

Why Not Just Use the DSHA Website?

The DSHA website lists program names, eligibility requirements, and income limits. It does not tell you which combination of programs generates the most total value for your specific situation. It does not compare Welcome Home + Take5 against Open Door + Keys4You + MCC and show you the breakeven point. It does not calculate your transfer tax with the first-time buyer exemption applied and the municipal variation for your specific town. It does not explain that the 1% MCC issuance fee is waived when you pair it with a DSHA mortgage, or that skilled lenders can factor the MCC credit into your DTI ratio to qualify you for a home priced $20,000 to $30,000 higher.

State websites give you the rules. This guide gives you the strategy.

100% Satisfaction Guarantee

If the guide does not save you more than you paid for it — in transfer tax savings, DPA you would have missed, or tax credits you did not know existed — email us and we will refund every cent. The strategies in Chapter 3 alone are worth the entire cost of the guide.

Start With the Free Checklist or Get the Full Guide

Download the Delaware Quick-Start Home Buying Checklist free — a printable 20-item action plan covering financial preparation, DSHA pre-approval, county selection, offer strategy, and closing. It covers what to do. The full Delaware First-Time Home Buyer Guide covers how — with the math, the stacking strategies, the program comparison tables, the inspection checklists, and the six standalone PDFs that turn twelve chapters of intelligence into tools you can use at your closing table.

For less than the cost of one hour with a real estate attorney, you get the complete Delaware closing cost playbook.