D.C. Will Give You $202,000 — If You Can Survive the System That Administers It

You discovered the number. $202,000 in interest-free gap financing through the Home Purchase Assistance Program. No other city in the country offers anything close. You ran the math. You started imagining what homeownership in the District could actually look like.

Then reality set in. In FY2024, the entire $26.2 million HPAP budget was exhausted by January — four months into the fiscal year. Buyers who spent months completing HUD-approved education courses, gathering documentation, and progressing from Notice of Eligibility to Notice to Proceed were told the money was gone. Meanwhile, sellers had already learned to treat HPAP-backed offers as liabilities. A six-week closing timeline. Mandatory government inspections. The ever-present risk that DHCD funding evaporates mid-transaction. Qualified HPAP buyers who offered above asking price lost to conventional bidders offering less.

The programs exist. The money is real. But without a precise understanding of D.C.'s fiscal year timing, the alternative programs that avoid seller stigma, the tax reductions that disappear if a single form is missed at the closing table, and the property-type traps that generic guides never mention — the system works against you.

The D.C. Buyer's Operating System — Every Program, Every Tax Code, Every Competitive Tactic

This is not a national home buying checklist with "check your credit score" and "find an agent." This is a D.C.-specific system that decodes every municipal program, calculates the actual tax math, maps the competitive strategies that win in multiple-offer situations, and warns you about the property-type traps that cost first-time buyers tens of thousands of dollars.

What Makes This Different from Free Guides

The DHCD website lists HPAP eligibility brackets. Real estate blogs mention DC Open Doors. But none of them tell you the truth about how the system actually works in practice.

Free guides will not tell you that HPAP's year-six repayment shock catches moderate-income borrowers off guard — five years of deferred payments followed by a 40-year principal-only amortization that suddenly appears in your monthly budget. They will not explain that renting out your English basement, refinancing to access equity, or simply moving triggers immediate full repayment of the entire HPAP balance, effectively trapping you in the property. They will not warn you that sellers reject HPAP offers even when they are above asking price because a conventional buyer closes in three weeks with zero government friction.

The DCHFA website explains DC Open Doors eligibility. It does not compare it head-to-head with HPAP by income tier and show you which path actually gets you a house. It does not calculate that a dual-income household where one spouse exceeds HPAP limits can have the lower-earning spouse apply as sole borrower to qualify for Open Doors. It does not explain that D.C. government employees can stack DC4ME reduced-rate mortgages with EAHP grants and first responder or teacher enhancements for over $25,000 in combined assistance — without any of the seller stigma.

National guides have no idea that Form ROD 11 must be filed at the exact moment the deed is offered for recordation or the first-time buyer recordation tax reduction is permanently forfeited. They do not know that D.C. condominiums have no statutory reserve study mandate, that co-op boards can reject your purchase application without giving any reason, or that renovating a rowhouse in a historic district requires Historic Preservation Office approval with materials mandates that triple your costs. The free content covers D.C. in a paragraph. This guide covers D.C. in fifteen chapters with program comparison tables, cost calculations, neighborhood intelligence, and decision frameworks by income tier.

Everything Inside

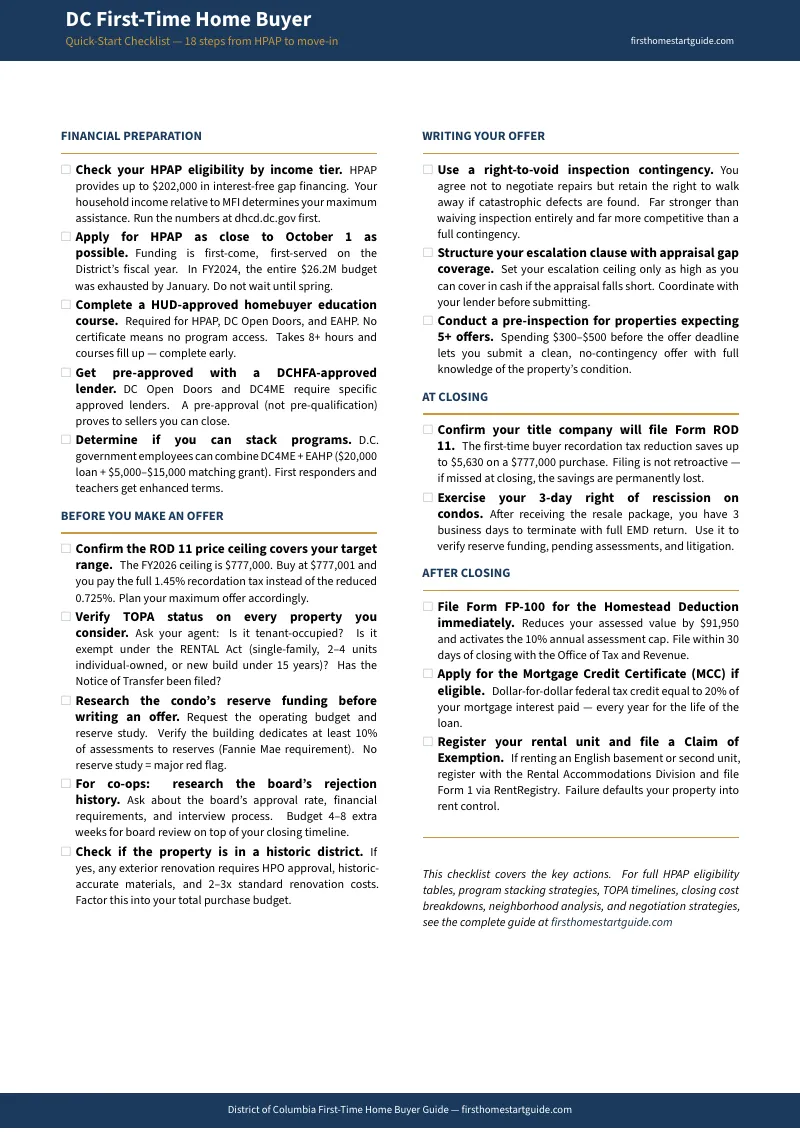

HPAP Decoded — The full program mechanics: income tiers by household size (up to 50% MFI for maximum $202,000 assistance, 51-80% MFI for scaled amounts, 81-110% MFI for reduced assistance), the $4,000 closing cost supplement, minimum buyer contribution formula, and the NOE-to-NTC-to-NTP pipeline with its 90-day property search deadline. The year-six repayment shock modeled in dollars. Repayment triggers that trap you in the property. The fiscal year funding strategy — apply as close to October 1 as possible. How the 2023 retroactive 30% cap caused chaos and what emergency legislation followed.

DC Open Doors vs. HPAP — Side-by-side comparison: $202,000 maximum from HPAP versus 3% deferred down payment from Open Doors. Why Open Doors' smaller dollar amount frequently wins you the house that HPAP cannot. Income limits ($275,400 for Open Doors vs. 110% MFI for HPAP), purchase price caps (none vs. market-constrained), closing timelines (30 days vs. 6+ weeks), and seller acceptance rates. The decision framework by income bracket.

EAHP, DC4ME, and NACA for Government Employees — The Employer-Assisted Housing Program ($20,000 deferred loan + up to $5,000 matching grant, no income cap, enhanced grants for first responders and teachers). DC4ME reduced-rate mortgages with 3% DPA. How to stack EAHP + DC4ME for maximum benefit. NACA's no-down-payment, no-closing-cost, no-PMI option.

The ROD 11 Recordation Tax Reduction — How to cut your recordation tax from 1.45% to 0.725% and save up to $5,630 on a $777,000 purchase. The FY2026 price ceiling mechanics — buy at $777,001 and you pay the full rate. Why Form ROD 11 must be filed simultaneously with the deed. The ROD 9 exemption for lower-income buyers. Worked calculations at $500K, $650K, and $777K.

Transfer and Recordation Tax Structure — The full 2.2% rate on sales under $400,000 (1.1% transfer + 1.1% recordation) escalating to 2.9% at $400,000+ (1.45% each). On a $700,000 home, your baseline responsibility exceeds $10,000 before any other closing costs.

TOPA and the RENTAL Act of 2025 — What happens when a tenant has the statutory right to buy before you do. The RENTAL Act reforms: 15-year exemption for new-build multifamily, streamlined procedures for 2-4 unit buildings, 45-day Notice of Transfer window, 5-day cooling-off period. How to verify TOPA status before writing an offer.

Condo Due Diligence — D.C. has no statutory mandate requiring reserve studies. How boards suppress HOA dues and defer maintenance until a catastrophic special assessment lands on owners. The Fannie Mae 10% funding test. What to demand from the resale package. Red flags that should kill the deal before you commit.

Co-op Realities — Why monthly fees exceed $1,200-$1,400 for a one-bedroom and what is actually bundled inside them (underlying commercial mortgage, utilities, aggregate property tax). The board application process and subjective rejection authority. Subletting and rental restrictions that trap you if your plans change.

Historic District Renovation Rules — Which neighborhoods fall under HPO jurisdiction (Capitol Hill, Shaw, Mount Pleasant, Adams Morgan, Georgetown). What requires approval, what does not, and why renovation budgets for historic rowhouses should assume 2-3x standard costs.

Bidding War Strategies — The right-to-void inspection contingency: how to stay competitive without waiving your safety net. Escalation clauses with appraisal gap coverage. Pre-inspections for properties expecting five or more offers. When to waive contingencies and when that decision becomes reckless.

D.C. vs. Maryland vs. Northern Virginia — Side-by-side comparison of income taxes, transfer taxes, and property tax rates across all three jurisdictions. The counterintuitive math: D.C.'s punishing income tax is offset by the lowest property tax in the region, meaning monthly carrying costs can be lower than Virginia over a 30-year horizon.

Neighborhood Analysis — Best-value neighborhoods for first-time buyers with median prices, appreciation trajectories, and lifestyle profiles. Brookland, Petworth, Brightwood, Capitol Hill East, Congress Heights, and Wards 7-8 with targeted HPAP-E enhancement funds.

Decision Frameworks by Income Tier — Under $80K: HPAP despite the friction. $80K-$150K: DC Open Doors for speed and seller acceptance. $150K+: conventional financing with ROD 11. D.C. government employees: stack DC4ME + EAHP regardless of income.

6 Standalone Printable PDFs — HPAP eligibility calculator with MFI tiers and repayment modeling. Closing cost estimator with recordation and transfer tax calculations by price point. Condo due diligence checklist. Bidding strategy worksheet. D.C. vs. Maryland vs. Virginia cost comparison. Monthly budget projection with homestead deduction and program stacking scenarios.

Who This Is For

- First-time home buyers anywhere in Washington, D.C. — Capitol Hill, Brookland, Petworth, Adams Morgan, Columbia Heights, Shaw, Georgetown, Congress Heights, or Wards 7 and 8

- Federal employees, congressional staffers, NGO workers, and government contractors navigating HPAP income limits while competing against all-cash investors

- D.C. government employees who want to stack DC4ME reduced-rate mortgages with EAHP grants and first responder or teacher enhancements

- Renters who discovered HPAP's $202,000 headline and need to understand the real timeline, funding risks, and seller stigma before committing months of effort

- Buyers choosing between a condo, co-op, or rowhouse who need the full breakdown of each property type's hidden financial and legal liabilities

- Anyone weighing D.C. against Montgomery County, Prince George's County, Arlington, Alexandria, or Fairfax who needs the actual long-term cost comparison across state lines

Why Not Just Use the DHCD and DCHFA Websites?

The DHCD website lists HPAP eligibility brackets. The DCHFA website explains DC Open Doors requirements. Neither will tell you that HPAP's entire annual budget was exhausted in four months, that sellers systematically reject HPAP offers even above asking price, that the year-six repayment shock will add hundreds per month to your housing costs, or that filing Form ROD 11 one minute late means permanently forfeiting thousands of dollars in recordation tax savings.

Government websites give you the rules. This guide gives you the strategy — which programs to use, which to avoid, how to time your application, how to structure your offer so sellers accept it, and how to avoid the property-type traps that cost uninformed D.C. buyers tens of thousands of dollars.

100% Satisfaction Guarantee

If the guide does not save you more than you paid for it — in program assistance you would have missed, tax reductions you did not know to claim, or closing cost traps you avoided — email us and we will refund every cent. The HPAP timing strategy in Chapter 2 alone is worth the entire cost of the guide.

Start With the Free Checklist or Get the Full Guide

Download the District of Columbia Quick-Start Home Buying Checklist free — a printable 18-step action plan covering HPAP application timing, program stacking, ROD 11 compliance, TOPA verification, condo reserve analysis, and post-purchase homestead filing. It covers what to do. The full District of Columbia First-Time Home Buyer Guide covers how — with the program comparison tables, the tax calculations, the bidding strategies, the neighborhood intelligence, the decision frameworks by income tier, and the six standalone PDFs that turn fifteen chapters of D.C.-specific intelligence into tools you can use at your closing table.

For less than the cost of one hour with a D.C. real estate attorney, you get the complete D.C. home buying operating system — .