You Ran the Numbers on a Capitol Hill Rowhouse. But You Didn't Know the Tenants Can Block Your Sale for a Year Under TOPA, That Your LLC Disqualifies You from the Rent Control Exemption, or That Your Franchise Tax Bill Arrives Even When the Property Loses Money.

You found a two-unit rowhouse on Capitol Hill projecting 5.2% gross yield against government-employee tenant demand that never dries up. Or a four-unit walkup in Petworth where the rent roll shows market-rate rents on every unit. Or a distressed property in Ward 7 where the acquisition price is 40% below the citywide median and the value-add math pencils out beautifully. You ran the deal analyzer. You lined up financing. You're ready to wire earnest money.

Then Washington DC happens. You make an offer on the Petworth four-unit and the tenants file a formal Statement of Interest under TOPA -- triggering a 90-day mandatory negotiation period, followed by a 15-day right of first refusal, followed by a 45-day settlement window that can extend to 75 days. Your capital is frozen in a contingent contract for six months while a tenant association you never anticipated decides whether to match your offer or demand a cash buyout. You close on the Capitol Hill rowhouse and hold it through an LLC for liability protection -- then discover that the small landlord rent control exemption requires ownership by a "natural person" with five or fewer units, and your LLC doesn't qualify. Your building, constructed in 1962, defaults to rent-controlled status. The Rental Housing Commission has capped your annual increase at 4.8% for general tenants and 2.5% for elderly tenants -- and you cannot raise rents to market without filing a Hardship Petition proving the property yields less than a 12% return on equity. Meanwhile, the Office of Tax and Revenue sends you a D-30 Unincorporated Business Franchise Tax notice: because your gross rental income exceeds $12,000, you owe 8.25% on your taxable District income -- with a $250 minimum even in years the property operates at a net loss. And when you try to renovate the exterior of the rowhouse to increase its ARV, the Historic Preservation Review Board rejects your vinyl window replacement, mandates expensive wood-clad alternatives, and adds four months of holding costs to your project timeline.

Here's what no single free resource explains: DC layers a Tenant Opportunity to Purchase Act that can freeze your acquisition for 6 to 12 months against a rent stabilization program where every pre-1975 building defaults to controlled status unless the landlord holds a filed RAD exemption against a franchise tax that treats all rental income above $12,000 as business income taxable at 8.25% even when the property loses money against a Basic Business License chain where operating without a BBL voids your lease and blocks your evictions against a Historic Preservation Review Board that controls exterior renovations across Capitol Hill, Georgetown, Dupont Circle, and Anacostia against a "just cause" eviction regime where tenants hold perpetual tenure and a 30-day notice period is required before you can even file a nonpayment complaint against Class 2 property tax rates of $1.65 per $100 of assessed value -- nearly double the owner-occupied rate -- with no homestead deduction. Each of these has cost real DC investors tens of thousands because the information existed -- scattered across OTR filing requirements, RAD registration databases, DHCD tenant rights publications, DOB Scout records, HPRB meeting minutes, and Reddit threads from landlords who learned the hard way -- but nobody had assembled it into a single investment framework calibrated to how Washington DC actually works in 2026.

The District of Columbia Investment Property Guide is a DC Regulatory Compliance Engine -- not a motivational overview of capital-region real estate, but a structured reference that maps every DC-specific regulation, tax mechanism, exemption strategy, and ward-by-ward market dynamic into a process you work through before your earnest money is at risk. It replaces months of cross-referencing OTR filings, RAD registration forms, TOPA waiver templates, DOB Scout searches, HPRB guidelines, and BiggerPockets threads with a single guide that tells you exactly what to verify, exactly what the numbers should look like, and exactly where deals go wrong in this jurisdiction.

What's Inside the DC Regulatory Compliance Engine

A comprehensive guide, a quick-start checklist, and 6 standalone worksheets and reference cards -- 8 printable PDFs covering every stage from pre-purchase due diligence through post-closing operations, built specifically for the regulations, taxes, exemptions, and market dynamics that make Washington DC unlike any other jurisdiction:

TOPA Timeline Navigator

The Tenant Opportunity to Purchase Act is the single most disruptive force in DC investment acquisitions. It gives existing tenants a statutory right of first refusal that can freeze your deal for months. The guide maps the complete timeline for every property type: the single-family exemption (post-2018, with the critical grandfather clause for elderly and disabled tenants who signed leases before March 31, 2018), the 2-to-4 unit process (22-day cooling period, 90-day negotiation, 15-day right of first refusal, 45-to-75-day settlement window), and the 5+ unit process (45-day tenant organization period, 120-day negotiation that extends day-for-day when you delay providing property information, 120-to-240-day settlement window, and the 360-day lapse provision that forces you to restart the entire process). It covers the 2025 RENTAL Act exemptions for new construction (buildings constructed 2010-2025 retroactively exempt, post-2025 builds exempt for 15 years), tenant buyout negotiation strategies, TOPA waiver acquisition, and how to underwrite the holding costs of a frozen contract before you submit your offer.

D-30 Franchise Tax Modeling

In DC, rental income is not passive Schedule E income -- it is statutorily classified as business income. If your gross rents exceed $12,000 in a calendar year, you are operating an "unincorporated business" and must file Form D-30 regardless of whether you live in DC or out of state. The guide walks through the complete calculation: gross rent minus operating expenses, multiplied by 0.70 (after the 30% salary allowance), minus the $5,000 statutory exemption, taxed at 8.25%. It covers the $250 minimum tax that applies even when the property operates at a net loss after depreciation and mortgage interest, the cross-agency enforcement mechanism where failure to file triggers a Clean Hands violation that blocks your BBL renewal and halts pending evictions, and the entity-level structuring decisions that determine whether your D-30 liability compounds across properties or stays isolated.

The LLC Rent Control Trap

DC's rent stabilization program automatically covers every building constructed before 1975 unless the landlord holds a filed exemption. The small landlord exemption requires ownership by "natural persons" with five or fewer rental units citywide. Here is the trap: if you hold the property through an LLC -- which every asset protection attorney recommends -- you do not qualify as a "natural person," and your pre-1975 building defaults to rent-controlled status. The guide covers the complete exemption analysis: new construction (post-1975), small landlord (natural person, five or fewer units), separately deeded condominiums, and the operational consequences of each. It explains the 2025-2026 rent increase caps (4.8% for general tenants, 2.5% for elderly and disabled tenants), the Hardship Petition process for requesting increases above the cap (proving the property yields less than 12% return on equity), the RAD registration requirement that must be completed before your BBL is issued for apartment buildings, and why a single administrative oversight -- failing to file your exemption form -- can retroactively subject your property to rent rollbacks and overcharge liability.

BBL Licensing Chain

Every DC landlord needs a Basic Business License with the correct housing endorsement before collecting a single dollar of rent. Operating without one voids your lease, blocks your evictions in Landlord-Tenant Court, and exposes you to municipal fines. The guide maps the complete licensing chain: tax registration with OTR, Clean Hands certification (no more than $1,000 in outstanding debt to DC government), Certificate of Occupancy for two-family and apartment buildings, DOB physical inspection (free initial, $90 re-inspection fee per failure), and RAD registration. It covers the three endorsement categories (One-Family Rental, Two-Family Rental, Apartment), the sequencing trap where apartment buildings must register with RAD before the BBL is issued while one-family and two-family rentals register after, and the $300 biennial report filing that keeps your LLC in good standing -- because an administratively dissolved LLC cannot file evictions in DC courts.

Historic Preservation Holding Cost Modeling

Capitol Hill, Georgetown, Dupont Circle, and parts of Anacostia are designated Historic Districts under the jurisdiction of the Historic Preservation Review Board. Any exterior renovation -- window replacement, masonry repointing, roof work, structural additions -- requires HPRB review that can add three to six months to your project timeline. The guide covers the review tiers: minor in-kind repairs (administrative HPO approval), larger alterations (formal HPRB presentation with 21-day advance submission), and the material restrictions that routinely inflate construction budgets (wood-clad windows instead of vinyl, specific mortar mixes, historically accurate roofing). It includes a holding cost model for HPRB delays -- mortgage payments, insurance, property taxes, and opportunity cost -- so you can underwrite the true cost of a flip or value-add project in a historic district before you commit capital.

Ward-by-Ward Yield Analysis

Washington DC is six fundamentally different investment environments sharing one set of tax codes. The guide provides data-driven profiles for each major submarket: Ward 8/Anacostia (highest gross yields, lowest entry prices, value-add territory with the 11th Street Bridge Park catalyst), Petworth (emerging middle-market, rowhouse conversion opportunities), Columbia Heights (established demand, heavy pre-1975 stock requiring rent control navigation), Capitol Hill (compressed cap rates below 5%, capital preservation, severe historic district constraints), NoMa (institutional density, Class A competition, concession-heavy leasing), and Navy Yard/Capitol Riverfront (premium rents, supply-wave vacancy risk). Each profile includes median rents by unit type, acquisition cost ranges, cap rate benchmarks, the dominant strategy, and the specific regulatory risks that apply in that ward.

Acquisition Cost Modeling

DC's dual-tax mechanism at closing -- recordation tax plus transfer tax -- creates acquisition friction that other jurisdictions don't impose. For properties under $400,000: 1.1% recordation plus 1.1% transfer (2.2% combined). For properties at $400,000 and above: 1.45% plus 1.45% (2.9% combined), applied to the entire purchase price, not just the amount above the threshold. The guide covers how to model total closing costs at 3.0% to 4.5% of purchase price, the first-time homebuyer exemption that investors are categorically excluded from, and the interaction between transfer taxes and your cash-on-cash return calculation. On a $600,000 Capitol Hill rowhouse, the combined recordation and transfer taxes alone exceed $17,400 before you add title insurance, settlement fees, and attorney costs.

Eviction Underwriting and Just Cause Framework

DC tenants hold perpetual tenure. A landlord cannot decline to renew a lease when the term expires -- this is completely illegal in Washington DC. You must have a statutorily defined "just cause" for every termination: nonpayment, material lease breach, illegal activity, owner-occupancy intent, or intent to sell (which triggers TOPA). For nonpayment, you must serve a 30-day notice to cure before filing in Landlord-Tenant Court, and tenants can halt the eviction at virtually any point by paying the arrears. The guide covers the complete eviction timeline, the right to redeem that tenants retain until the US Marshals arrive for physical set-out, the security deposit cap at exactly one month's rent with interest-bearing escrow requirements, and why tenant screening has become the single most important operational skill for DC landlords -- because once you hand over the keys, removing a nonpaying tenant is a months-long process with guaranteed carrying costs.

Capital Gains and 1031 Exchange Framework

The District taxes capital gains as ordinary income with no preferential rate -- subjecting profits to the top marginal rate of 10.75%, one of the highest in the nation. The guide covers 1031 exchange execution: engaging a Qualified Intermediary before closing, the 45-day identification window and 180-day closing deadline, the three-property rule, boot avoidance, and why building your replacement property shortlist before the relinquished sale closes is non-negotiable in DC's low-inventory market. It also covers cost segregation studies for accelerated depreciation and the interaction between federal depreciation recapture and DC's capital gains treatment.

Who This Guide Is For

This guide is for real estate investors targeting District of Columbia rental or flip properties who:

- House hackers buying a two-unit rowhouse to live in one unit and rent the other -- and who need to understand the Two-Family BBL endorsement requirements, whether their owner-occupied status qualifies for the rent control exemption, how TOPA applies when they eventually move out and sell, and how the D-30 franchise tax obligation kicks in the moment gross rental income from the second unit exceeds $12,000

- Out-of-state yield seekers deploying capital into DC from Virginia, Maryland, Texas, or California -- attracted by government-backed tenant demand and recession-resistant rents but who have never navigated TOPA timelines, D-30 filing requirements, BBL licensing chains, or a "just cause" eviction regime where tenants hold perpetual tenure and can halt eviction proceedings by paying arrears at any point before the Marshals arrive

- Capitol Hill and Georgetown flippers targeting rowhouse renovations in the highest-demand neighborhoods -- who need to model HPRB review timelines (3-6 months for exterior work), mandatory material upgrades (wood-clad windows, historically accurate masonry), and the holding cost impact on IRR before submitting an offer, plus the Mansion Tax-equivalent pricing dynamics where the $400,000 transfer tax threshold creates a bracket cliff that affects buyer demand

- Ward 7 and Ward 8 value investors pursuing the highest cap rates in the District at the lowest entry prices -- who need realistic underwriting that accounts for the 11th Street Bridge Park appreciation catalyst, the concentration of pre-1975 rent-controlled stock, the operational realities of the District's most tenant-protective enforcement environment, and the specific TOPA dynamics in buildings where tenant associations routinely organize and exercise their statutory rights

Why Not Free Tools and Forums?

Free information on DC real estate investing exists. Here's what it actually delivers:

- BiggerPockets forums contain dozens of threads from investors who discovered TOPA after signing a contract -- posting about $15,000 to $20,000 tenant buyouts they didn't budget for, six-month closing delays they didn't underwrite, and tenant associations that matched their offers and forced them to walk away. The information about TOPA's existence is there, but the operational framework for navigating it -- timeline modeling by property type, the 2025 RENTAL Act exemptions, waiver acquisition strategies, and the 360-day lapse provision -- is not. You get the horror stories without the prevention system.

- DC government websites spread critical compliance information across six agencies: OTR for tax registration and D-30 filing, DLCP for BBL licensing and LLC biennial reports, DHCD for RAD registration and rent control, DOB for physical inspections and Scout violation searches, HPO for historic preservation review, and OTA for tenant rights publications. Each agency publishes accurate but fragmented information about its own domain. None of them explain how a Clean Hands violation from an unfiled D-30 return blocks your BBL renewal, which blocks your eviction filing, which leaves you collecting zero rent from a nonpaying tenant while your franchise tax minimum still accrues. The cross-agency chain reaction is where investors lose money, and no single government website maps it.

- Real estate agents in DC will walk you through comparable sales, neighborhood trends, and offer strategy. They rarely model the D-30 franchise tax into your NOI calculation, don't explain why your LLC disqualifies you from the rent control exemption, don't quantify the HPRB holding cost impact on your flip margin, and never mention that operating without a BBL voids your lease and blocks your evictions. The brokerage process is designed to close transactions, not to identify the regulatory landmines that determine whether the deal actually produces the yield your spreadsheet projects.

- Reddit threads (r/dcarea, r/washingtondc, r/realestateinvesting) surface genuine operational experiences -- landlords posting about $250 minimum franchise tax bills on properties that lost money, investors discovering their LLC ownership triggered rent control status, flippers watching their margins evaporate over four months of HPRB review. The experiences are real, but the advice is contradictory, often outdated (pre-RENTAL Act TOPA timelines mixed with current ones), and scattered across hundreds of posts. Assembling current DC investment law from Reddit takes longer than reading a guide that has already done it.

This guide fills the DC-specific gap -- the space between knowing how to analyze a rental property in general and knowing how to invest in a jurisdiction where tenants can block your sale for a year, where your LLC triggers rent control, where the franchise tax applies even on loss-making properties, where operating without a BBL voids your lease, where historic preservation review adds months to your renovation timeline, and where capital gains are taxed at 10.75% with no preferential rate. It's the analysis that would take a DC real estate attorney, a tax advisor familiar with D-30 filing, a TOPA specialist, and a historic preservation consultant to assemble -- structured as a reference you own permanently.

-- Less Than One Hour of a DC Real Estate Attorney

A DC real estate attorney charges $2,000 to $5,000 for a standard closing. A TOPA tenant buyout on a four-unit building runs $15,000 to $20,000 per tenant when you haven't planned for it. Discovering your LLC ownership disqualifies you from the rent control exemption triggers retroactive rent rollbacks and overcharge liability. A $250 minimum franchise tax on a loss-making property is a guaranteed annual cost that most out-of-state investors never model. Operating without a BBL -- because you didn't know you needed one before collecting rent -- voids your lease and blocks your eviction when a tenant stops paying. An HPRB rejection on a Capitol Hill flip adds $15,000 to $30,000 in holding costs while you revise plans and wait for the next board meeting. Listing a property at $410,000 instead of $395,000 pushes both buyer and seller into the 1.45% transfer tax bracket, adding $3,500 in combined tax friction that can stall a deal.

This guide doesn't replace your DC real estate attorney or your tax advisor. But it gives you the TOPA timeline navigator, D-30 franchise tax model, rent control exemption analysis, BBL licensing sequence, historic preservation holding cost framework, ward-by-ward yield data, and just cause eviction protocol that ensure you identify every DC-specific risk before your earnest money is committed -- instead of discovering them on your closing timeline, your first D-30 filing, your first HPRB hearing, or your first Landlord-Tenant Court appearance.

If it catches a single TOPA timeline you didn't underwrite, prevents a single rent control classification you didn't anticipate, or keeps you from operating without the BBL that your eviction filing requires, it pays for itself before you've finished reading it.

30-day money-back guarantee. If the guide doesn't sharpen your underwriting and protect your investment in DC's regulatory environment, you pay nothing.

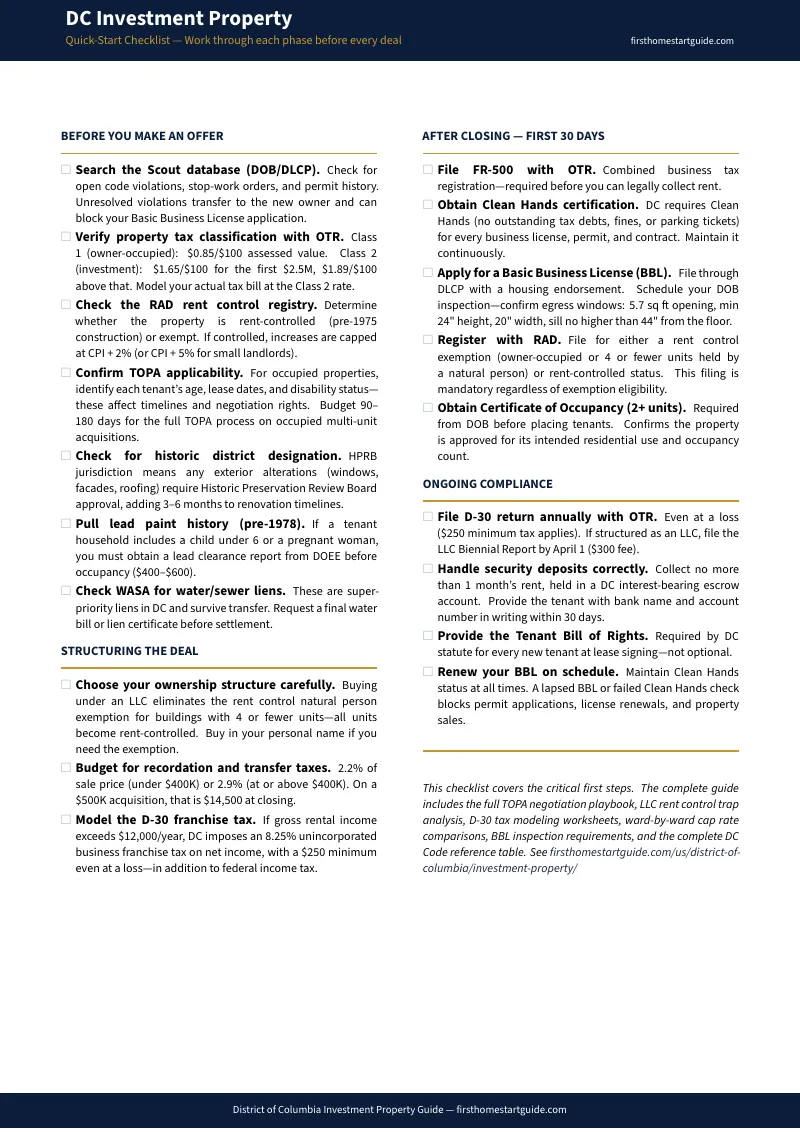

Download the free District of Columbia Quick-Start Home Buying Checklist to see the action plan covering pre-purchase research, TOPA verification, due diligence, and post-purchase compliance. When you're ready for the full TOPA navigator, D-30 tax modeling, rent control exemption framework, BBL licensing chain, and ward-by-ward yield analysis, the complete guide is here.

The deal pencils out on the spreadsheet. This guide tells you whether Washington DC agrees.