The Listing Says 8% Yield. Your Year-Two Tax Bill, Insurance Stack, and Condo Safety Mandate Say Otherwise.

You found a vacation rental in Kissimmee throwing off $65,000 gross annual revenue. Or a condo in Fort Lauderdale where the HOA is $380/month and the beach is two blocks away. Or a duplex in Jacksonville where the rent-to-price ratio screams cash flow. The numbers work. The cap rate is solid. You're ready to wire earnest money.

Then you run the real numbers. The Kissimmee rental sits in a municipality where operating without a county STR license, $1,000,000 commercial liability policy, and monthly tourist tax remittance gets your license revoked and triggers a tax audit. The Fort Lauderdale condo is in a building where the association hasn't completed its Structural Integrity Reserve Study, the reserve waiver ban means monthly fees are about to spike by hundreds of dollars, and Fannie Mae's Lender Letter LL-2026-03 has just classified the building as non-warrantable -- meaning you can't get conventional financing and neither can the next buyer when you sell. The Jacksonville duplex was last reassessed when the prior owner bought it 12 years ago for $165,000. You're paying $340,000. On January 1 of next year, the county property appraiser resets the assessed value from the capped $210,000 to the full $340,000 -- and your property taxes nearly double.

Here's what no single resource explains: Florida layers a property tax reassessment trap that resets the 10% non-homestead cap on every change of ownership, an LLC transfer penalty under Florida Statute Section 193.1556 that triggers the same reset plus documentary stamp tax, post-Surfside condo safety mandates requiring milestone inspections and fully funded structural reserves with no opt-out, the nation's highest insurance premiums with mandatory flood coverage stacking on top of windstorm regardless of your flood zone, and city-by-city short-term rental enforcement where a single Miami Beach violation costs $20,000 -- into a regulatory environment that punishes investors who apply national assumptions to Florida-specific problems. Every one of these has cost real investors five to six figures because the information existed -- scattered across 14 county property appraiser websites, municipal zoning portals, Citizens Property Insurance bulletins, and BiggerPockets threads from 2023 -- but nobody had assembled it into a single underwriting system.

The Florida Investment Property Guide is a Florida Investor Compliance Navigator -- not a motivational overview of Sun Belt real estate investing, but a structured due diligence framework that maps every Florida-specific financial trap, regulatory restriction, and insurance risk into a process you work through before you wire earnest money. It replaces months of cross-referencing county property appraiser tax estimators, condo association SIRS reports, Citizens insurance phase-in schedules, and municipal STR zoning maps with a single reference that tells you exactly what to verify, exactly what the numbers should look like, and exactly where deals go wrong.

What's Inside the Florida Investor Compliance Navigator

A 13-chapter guide, a standalone due diligence checklist, and 8 printable worksheets and reference cards -- covering every stage from market selection through post-purchase operations, built specifically for the financial traps and regulatory complexity that make Florida different from every other state:

Non-Homestead Property Tax Trap and LLC Reassessment Penalty

The single most common underwriting error among Florida investors. The prior owner's 10% annual assessment cap under Florida Statute Section 193.1554 is completely removed when ownership changes. You model your cash flow using the seller's current tax bill, but on January 1 of the year following your purchase, the county property appraiser resets the assessed value to full market value. On a property where the previous owner held for 10-15 years, your year-two taxes can double or triple. The guide walks through the reset mechanics with dollar-for-dollar examples, shows you how to use county property appraiser tax estimators to model the year-two bill before making an offer, and covers the LLC transfer trap -- where following common BiggerPockets advice to move a rental into an LLC triggers the same full reassessment under Section 193.1556, plus documentary stamp tax on any outstanding mortgage balance at $0.70 per $100, plus a mandatory Form DR-430 filing within 30 days where failure to file exposes you to retroactive back taxes, a 50% penalty, and 15% annual interest. This chapter turns the most expensive blind spot in Florida investing into a calculation you can run in 10 minutes.

Post-Surfside Condo Due Diligence Framework

The 2021 Champlain Towers South collapse triggered a complete overhaul of Florida condo investing. Senate Bill 4-D and Senate Bill 154 now require milestone structural inspections for every building three stories or higher when it reaches 30 years of age, with Phase 2 destructive testing if Phase 1 reveals substantial structural deterioration. The Structural Integrity Reserve Study mandate requires fully funded reserves across eight mandatory structural components -- roof, primary structure, fire protection, plumbing, electrical, waterproofing, windows, and any other item exceeding $25,000. The reserve waiver ban that took effect January 1, 2025 means condo owners can no longer vote to skip these contributions, and associations that deferred maintenance for decades are now hitting unit owners with massive special assessments. Fannie Mae's Lender Letter LL-2026-03 eliminates the streamlined Limited Review process for buildings with more than 10 units effective August 3, 2026, and raises the minimum reserve funding floor to 15% effective January 4, 2027. The guide gives you a step-by-step condo warrantability assessment framework -- how to request and evaluate the SIRS, milestone inspection report, reserve funding statement, delinquency rates, insurance deductibles, and pending litigation before you commit to a purchase. Buying a condo that Fannie Mae classifies as non-warrantable means you can't sell it to any buyer using conventional financing -- and that's how investors discover their exit strategy has evaporated.

Insurance Stacking Analysis

Florida has the highest average home insurance premiums in the nation -- $4,000+ annually before flood coverage. Citizens Property Insurance, the state-backed insurer of last resort, is actively shrinking its book through the depopulation takeout rule: if a private carrier offers a premium within 20% of Citizens' renewal rate, you're legally required to accept the private policy. Private carriers can then aggressively adjust rates on subsequent renewals. On top of windstorm coverage, Citizens has phased in mandatory flood insurance for all residential policyholders regardless of FEMA flood zone designation -- the final phase covering all remaining property values takes effect January 1, 2027. Average flood insurance premiums were $865 in 2025. The guide models the full insurance stack -- windstorm, mandatory flood, sinkhole loss coverage in Hillsborough/Pasco/Hernando counties, wind mitigation inspection discounts of up to 88% on the windstorm portion, and the 4-Point inspection red flags (Federal Pacific electrical panels, polybutylene piping) that lead to coverage denial. Without this analysis, your NOI projections understate insurance costs by thousands of dollars per year.

City-by-City Short-Term Rental Compliance Map

Florida's vacation rental regulations vary wildly by municipality, and getting them wrong is extraordinarily expensive. Miami Beach bans STRs in all single-family residential zones and low-density multifamily (SF, SD-B, RM-1), restricting legal rentals to RM-2, RM-3, and CMU zones. First violation: $20,000. Second: $40,000. Third: $60,000. Habitual offenders face $100,000 fines plus property liens. Orlando bans entire-home STRs in residential R-1 zones -- the "Home Sharing" program requires the owner to live on-site at least 51% of the year and remain physically present during all guest stays. Osceola County allows entire-home rentals but only in designated STR Overlay Districts, requiring a county license, $1,000,000 commercial liability insurance, a professional floor plan, and monthly remittance of a 13.5% combined state and local tourist tax. The guide maps every major jurisdiction's zoning rules, licensing requirements, tax obligations, and penalty structures so you know exactly what's legal before you list a single night on Airbnb.

Market-by-Market Investment Analysis

Seven metro markets dissected with median listing prices, median rents, gross yields, inventory levels, and economic drivers: Jacksonville ($289,900 median, 8.6% gross yield, the strongest cash-flow market in the state), Tampa ($450,000, 8.7% yield, sinkhole risk in Hillsborough and Pasco counties), Orlando ($379,900, 7.9% yield, STR income concentrated in unincorporated Osceola County), Miami and Fort Lauderdale ($625,000+, 5.5% yield, capital appreciation play with extreme insurance costs), Southwest Florida -- Cape Coral, Naples, and Sarasota (ranging from 6.2% to 10.1% gross yield with elevated condo inventory creating buyer negotiation leverage), and the Panhandle -- Destin and Panama City Beach (seasonal drive-to tourism with permissive STR regulations). Know which risk-reward profile matches your capital and strategy before you deploy.

Landlord-Tenant Law and the State Preemption Advantage

Florida's eviction process is built for speed -- a 3-Day Notice calculated in business days (excluding weekends and holidays), followed by an eviction filing where the tenant must deposit full rent into the court registry within 5 days or receive an immediate default judgment. House Bill 1417 completely preempts all local municipal rent control, tenant screening regulations, and tenant "bills of rights." The guide covers security deposit administration under Section 83.49 (the 30-day itemized claim window you cannot miss without forfeiting all claims), month-to-month termination notice requirements, habitability standards, and the uniform statewide rules that mean no Florida municipality can impose local tenant protections beyond what state law requires.

Financing Strategies, Tax Optimization, and Entity Structuring

Conventional investment loans, DSCR financing for portfolio scaling, FHA house-hacking for Tampa duplexes, hard money for fix-and-flip, and non-warrantable condo financing through portfolio lenders and non-QM products. Florida's zero state income tax means all rental income and capital gains flow through to your federal return only -- no state-level drag. 1031 exchange mechanics under full federal IRC Section 1031 conformity. Cost segregation and 27.5-year depreciation strategies. LLC asset protection without triggering the tax reset -- including the option to buy directly in the LLC name, the unencumbered property transfer exception under the Crescent Miami Center precedent, and the land trust with LLC beneficiary structure under Florida Statute Section 689.071. FIRPTA withholding for foreign investors using disregarded-entity LLCs.

Who This Guide Is For

This guide is for real estate investors targeting Florida markets who:

- Are analyzing a Florida rental property and need to model the year-two property tax bill after the non-homestead assessment cap resets -- not the seller's current tax bill that reflects a decade of capped increases

- Are evaluating a Florida condo and need to determine whether the building will pass Fannie Mae warrantability standards after August 2026, whether the association is on track for the 15% reserve funding floor, and whether a pending special assessment is going to wipe out your projected returns

- Are planning to operate a vacation rental and need the exact zoning designation, licensing requirements, tax remittance obligations, and penalty structure for your specific municipality -- not a generic "check local laws" disclaimer

- Are an out-of-state investor from New York, New Jersey, California, or Illinois attracted by Florida's zero state income tax and want every Florida-specific regulatory trap, insurance requirement, and closing cost calculation in one reference before you deploy capital 1,000 miles from home

- Are a Canadian or international buyer executing an all-cash transaction and need to understand FIRPTA withholding, non-resident insurance requirements, and the entity structuring options that provide asset protection without triggering tax resets

- Are a local Florida homeowner leveraging equity to buy your first rental property and need to understand how the 10% assessment cap, LLC transfer rules, and insurance stacking affect your actual cash-on-cash return -- not the return your real estate agent projects using the current owner's numbers

Why Not Free Tools and Forums?

Free information on Florida real estate investing exists across dozens of sources. Here's what it actually delivers:

- BiggerPockets forums are where someone in a 2023 thread recommends transferring your rental into an LLC for asset protection, and nobody mentions that this triggers a full property tax reassessment under Section 193.1556 plus documentary stamp tax on the mortgage balance. You'll find genuinely useful experience reports mixed with advice that predates the reserve waiver ban, the Fannie Mae warrantability changes, and the latest Citizens mandatory flood insurance phase-in. Sorting current from outdated takes longer than reading a guide that has already done it.

- County property appraiser websites show you the current assessed value and last sale price. They don't model the post-sale reassessment reset, don't calculate the year-two tax bill at your projected purchase price, don't explain the LLC transfer trap, and don't connect the tax reset to your cash flow projections. You get the data without the investment analysis.

- Municipal planning portals publish zoning maps and STR ordinance text in legal language. They don't tell you which zones allow short-term rentals versus long-term only, don't compare the rules and fines across Miami Beach, Orlando, Osceola County, and Fort Lauderdale in one place, and don't flag the private CC&R restrictions that can override municipal zoning allowances. You get compliance documents without the investor-specific interpretation.

- Florida Realtors and national investing courses teach cap rate analysis, DSCR mechanics, and 1031 exchanges that apply everywhere. They don't mention the non-homestead tax reset, the post-Surfside condo warrantability crisis, the Citizens depopulation takeout rule, the mandatory flood phase-in schedule, or the $20,000 Miami Beach STR fine. Applying national frameworks to Florida-specific problems is how investors lose five figures on their first deal.

This guide fills the Florida-specific gap -- the space between knowing how to analyze a rental property in general and knowing how to underwrite one in a state where the non-homestead tax reset, post-Surfside condo safety mandates, $4,000+ stacked insurance premiums, and city-by-city STR enforcement can each independently turn a profitable deal into a losing one. It's the analysis that would take a Florida real estate attorney, a condo association specialist, an insurance broker, and a property tax consultant to assemble -- structured as a reference you own permanently.

-- Less Than One Tax Reset Surprise

A single property tax reassessment you didn't model adds thousands to your annual carrying costs -- every year you own the property. An LLC transfer that triggers a full reassessment under Section 193.1556 plus documentary stamp tax on a $300,000 mortgage costs you $2,100 in stamp tax alone, before the tax reset hits your bottom line. A condo special assessment for unfunded structural reserves can run tens of thousands per unit. A wind and flood insurance stack you didn't budget for erodes $3,000 to $5,000 from your NOI annually. A Miami Beach STR violation costs $20,000 on the first offense. A security deposit claim you file one day past the 30-day window forfeits your entire claim.

This guide doesn't replace your real estate attorney or your CPA. But it gives you the property tax reset analysis, condo warrantability framework, insurance stacking model, and STR compliance map that ensure you identify every Florida-specific risk before you're contractually committed -- instead of discovering them on your year-two TRIM notice, your first Citizens takeout letter, or your first code enforcement citation.

If it catches a single tax reset you didn't model, prevents a single non-warrantable condo purchase, or saves you from a single STR zoning violation, it pays for itself before you've finished reading it.

30-day money-back guarantee. If the guide doesn't sharpen your underwriting and protect your capital in Florida's regulatory environment, you pay nothing.

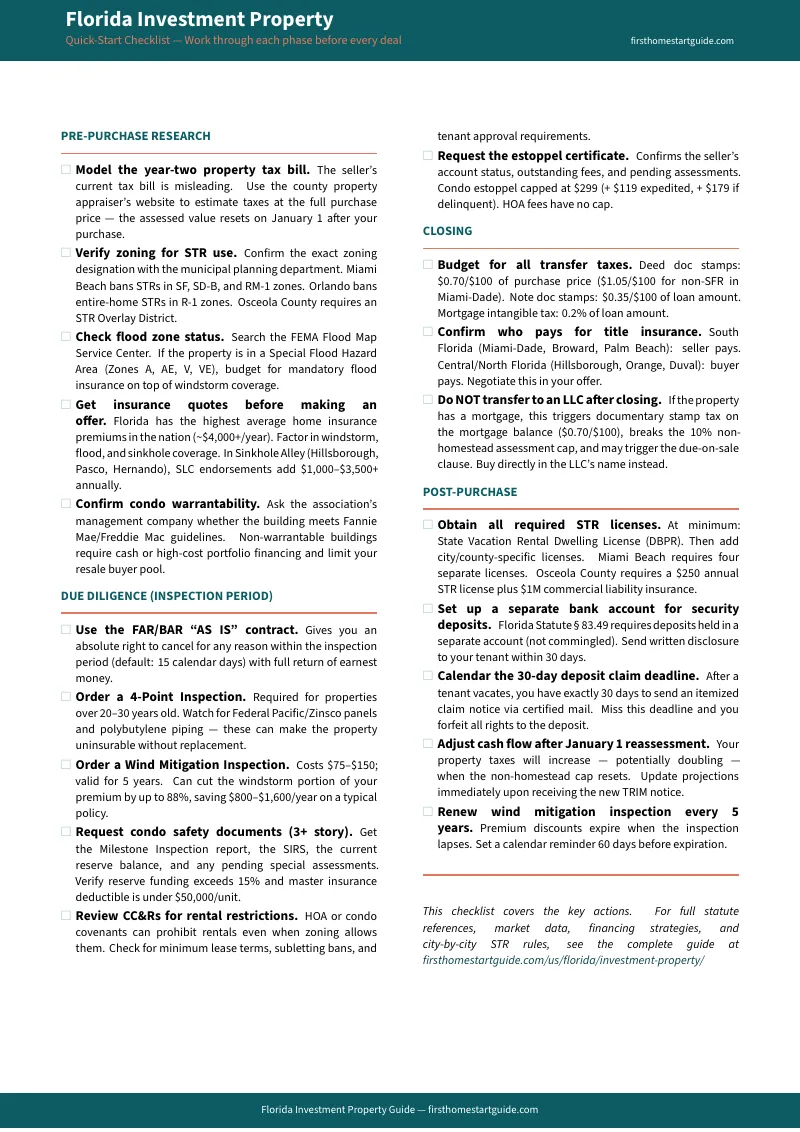

Download the free Florida Quick-Start Checklist to see the due diligence framework covering pre-purchase research, financial analysis, under-contract inspections, closing, and post-purchase setup. When you're ready for the full property tax reset analysis, condo warrantability framework, insurance stacking model, and 13-chapter investment system, the complete guide is here.

The deal looks good on the spreadsheet. This guide tells you whether Florida agrees.