You Found the House. But the IHFA Down Payment Assistance Isn't a Grant, Water Rights Don't Transfer With the Deed, Nobody Sits at Your Closing Table to Catch the Builder's Arbitration Clause, and Your Year 2 Mortgage Payment Is About to Jump by $400.

You found a four-bedroom in Meridian with a West Ada school assignment and a base price of $411,000. Or a starter in Nampa where the monthly payment projects lower than your current rent on Overland Road. Or a half-acre in Star where the listing says "USDA eligible" and you're running numbers on a zero-down loan. You got pre-approved. You completed "Finally Home!" You're ready to make an offer.

Then Idaho happens. Your lender calls the IHFA down payment assistance "basically free money" -- but it's actually a 15-year second mortgage at 2% above your primary rate, with monthly payments that reduce how much house you qualify for. You tour a new build in a master-planned community and the sales rep walks you through the model home's upgraded finishes -- but the base price excludes landscaping, fencing, blinds, and appliances, and you'll owe $30,000 to $40,000 the month after you close. You find a beautiful rural property near Emmett with a well and a creek running through it -- but owning the creek frontage doesn't give you the legal right to pump a single gallon, because water rights are a separate form of property in Idaho that must be specifically conveyed in the deed. You close on a new build in a Treasure Valley subdivision and your first property tax bill looks manageable -- then six months later the county assessor sends a supplemental bill based on the completed home, your escrow account is short by thousands, and your monthly mortgage payment jumps by $300 to $400.

Here's what no single free resource explains: Idaho layers a state-funded down payment assistance program that is widely marketed as a grant but is actually a repayable 15-year second mortgage, against a water rights system where land ownership and water ownership are legally separate and governed by the doctrine of prior appropriation, against a title company closing system where no attorney reviews your contract unless you hire one yourself, against a new construction market where volume builders routinely generate $30,000 to $40,000 in post-closing costs that were never part of your loan, against Community Infrastructure Districts that embed hidden tax assessments of $500 to $1,500 per year into newer subdivisions and were just validated by the Idaho Supreme Court, against a supplemental property tax system that creates massive escrow shortages and payment shock in Year 2 of new construction ownership, against a wildfire insurance crisis where premiums in some areas have spiked 335% and the state has no FAIR Plan safety net, against pressurized irrigation systems that run on a completely separate water supply from your indoor plumbing and operate on a seasonal schedule with mandatory rationing rules. Each of these has cost real first-time buyers thousands of dollars because the information existed -- scattered across IHFA program PDFs, IDWR water rights databases, county assessor records, Idaho Supreme Court CID rulings, and Reddit threads from buyers who learned after closing -- but nobody had assembled it into a single decision system calibrated to how Idaho actually works.

The Idaho First-Time Home Buyer Guide is an Idaho Home Buyer Navigation System -- not a motivational overview of Treasure Valley lifestyle, but a structured reference that maps every Idaho-specific program, tax structure, water rights requirement, insurance crisis, new construction trap, and regional market dynamic into a process you work through before your earnest money is at risk. It replaces months of cross-referencing IHFA program matrices, IDWR databases, county assessor websites, CID legal rulings, and forum posts with a single guide that tells you exactly what to verify, exactly what the numbers should look like, and exactly where deals go wrong in this state.

The complete guide, a quick-start checklist, and 8 standalone printable tools -- covering IHFA down payment assistance and stacking strategies, water rights due diligence, the RE-21/RE-10 contract mechanics, new construction traps, property tax defense, the wildfire insurance crisis, Mortgage Credit Certificates, and regional market analysis across the Treasure Valley, Coeur d'Alene, and Eastern Idaho. Ten printable files:

- guide.pdf -- The full guide covering every chapter

- checklist.pdf -- Quick-start home buying checklist

- dpa-worksheet.pdf -- IHFA Second Mortgage, Idaho Heroes, Boise HOP, and MCC programs with a fillable stacking calculator

- water-rights-reference.pdf -- Prior appropriation explained, IDWR database search process, well testing requirements, and the 2025 Domestic Well Exemption

- new-construction-worksheet.pdf -- After-keys cost budget ($30,000+), builder contract red flags, CID assessment check, and Year 2 tax shock warning

- homeowner-exemption-reference.pdf -- Homeowner's Exemption filing, CID detection, supplemental tax defense, and the competing July/April/September deadlines

- inspection-checklist.pdf -- General inspection, radon testing, well and septic items, WUI zone assessment, and every due diligence item to bring to your inspection

- closing-cost-worksheet.pdf -- Line-by-line buyer and seller closing costs with Idaho's $0 transfer tax advantage

- regional-market-reference.pdf -- Treasure Valley, Coeur d'Alene, and Eastern Idaho markets at a glance with pricing, competition, and USDA eligibility

- closing-timeline.pdf -- Your 30-to-45-day roadmap from offer to keys with RE-21/RE-10 deadlines

What's Inside the Idaho Home Buyer Navigation System

A comprehensive guide with a quick-start checklist -- covering every stage from pre-approval through post-closing, built specifically for the programs, tax structures, water rights, insurance dynamics, and new construction traps that make Idaho different from every other state:

IHFA Down Payment Assistance Decision Framework

Idaho's primary assistance program -- the IHFA Second Mortgage -- is genuinely powerful but widely misunderstood. The guide breaks down the program mechanics in detail: up to 8% of the purchase price as a 15-year fixed-rate second mortgage, at exactly 2% above your primary mortgage rate, with a minimum personal contribution of just $500. It covers the income limit ($170,000 household -- high enough to include most working professionals), the credit score floors (620 conventional, 580 FHA), and the mandatory "Finally Home!" education course ($50 online). Then it shows you how to stack IHFA with every federal loan type: IHFA + FHA (the most common combination, where 8% assistance covers the 3.5% down payment and absorbs closing costs), IHFA + VA (for Mountain Home AFB personnel, directing all assistance toward closing costs on a zero-down loan), IHFA + USDA (zero down in eligible exurban communities like Star, Kuna, and Middleton), and IHFA + Conventional. It covers the Idaho Heroes program for teachers, nurses, firefighters, law enforcement, and military -- which waives the $500 minimum contribution entirely and offers below-market rates with zero origination fees. And it details the Boise HOP program -- up to $65,000 as a silent second mortgage with zero monthly payments, repaid only upon sale, explicitly stackable with IHFA.

Water Rights Due Diligence -- Prior Appropriation and the IDWR Database

The single most dangerous knowledge gap for anyone buying rural or semi-rural property in Idaho. Water rights are a separate form of legal property governed by "first in time, first in right." A property may have a physical well drilled on it, but the well is meaningless without the legal authority to divert water. Owning riverfront property does not give you the right to pump from the river. Water rights can be appurtenant (intended to transfer with the land but requiring proper legal conveyance) or separate (owned independently and transferable only via specific assignment). The guide walks you through the IDWR public database search process, explains the 2025 Domestic Well Exemption (SB 1083a) that caps outdoor irrigation to half an acre from a domestic well, and covers the well water testing requirements that FHA, VA, and USDA lenders mandate before closing -- including the specific contaminants to test for (coliform, nitrates, arsenic, uranium) and the action levels that trigger loan denial.

New Construction Traps -- The $30,000 After-Keys Bill and Builder Contracts

Volume builders in Meridian, Star, Nampa, and Kuna market base prices that systematically exclude functional necessities. The guide itemizes the typical post-closing costs: landscaping ($8,000 to $15,000), fencing ($5,000 to $12,000), window blinds ($2,000 to $5,000), appliances ($3,000 to $8,000), and sod and sprinkler adjustments ($2,000 to $6,000). It explains why builders classify landscaping, soil compaction, and drainage as non-warrantable. It covers builder contract pitfalls -- mandatory arbitration clauses, price escalation provisions, limited warranty exclusions, and restricted agent access -- and tells you why having an independent attorney review a builder contract ($500 to $1,500) is the single most important place to spend money on legal representation in Idaho. It includes the verification protocol: visit completed homes at least two years old, check the Better Business Bureau, search r/Boise and r/Idaho for buyer experiences, and always register your buyer's agent at the first model home visit.

Property Tax Defense -- Homeowner's Exemption, CIDs, and the Year 2 Shock

Idaho's property tax system contains a powerful protection and a dangerous trap, both of which most first-time buyers miss. The Homeowner's Exemption reduces your taxable value by 50% (capped at $125,000) -- but it is not automatic. You must affirmatively file at your county assessor's office, and the competing deadlines between the Exemption (second Monday in July), the Circuit Breaker (April 15), and the Property Tax Deferral (September 8) cause widespread confusion among county assessors themselves. The guide tells you to file the week you close and never wait for a deadline. It covers Community Infrastructure Districts -- the Harris Ranch CID precedent, the Idaho Supreme Court's February 2026 ruling validating developer-imposed tax assessments, and the question you must ask before buying in any newer subdivision. And it explains the new construction supplemental tax bill that creates escrow shortages and payment shock in Year 2, with the specific request to make to your lender to avoid the surprise.

The Wildfire Insurance Crisis -- WUI Zones and the Missing Safety Net

Between 2021 and 2024, Idaho home insurance premiums surged 17% statewide. In some WUI (Wildland-Urban Interface) areas, premiums have increased 335% -- Huston, near Caldwell, saw annual premiums spike from $1,234 to $5,374. Unlike California or Oregon, Idaho has no state FAIR Plan -- no insurer of last resort. If no private carrier will cover your property, your mortgage cannot be funded. The guide covers the defensible space requirements that insurers evaluate (noncombustible zone within 5 feet, trees limbed up 6 to 10 feet in the 5-to-30-foot zone, Class A fire-rated roofing), the Boise WUI Overlay zones, and the critical step most buyers skip: getting insurance premium quotes for a specific address before making an offer, not after.

Regional Market Analysis -- Treasure Valley, Coeur d'Alene, and Eastern Idaho

Idaho is at least four distinct housing markets. The guide covers each in detail: Boise (the urban core, $450K to $550K medians, $140K+ income needed, limited entry-level inventory), Meridian (hyper-growth suburban, new construction dominant, West Ada schools, severe Eagle Road traffic, high CID risk), Nampa and Caldwell (the affordability release valve, $350K to $420K, punishing commute trade-off), Coeur d'Alene (37% cash buyers, premium lifestyle market, first-timers pushed to Post Falls and Rathdrum), and Eastern Idaho (Idaho Falls, Pocatello, Twin Falls -- significantly more affordable, agricultural economies). It maps the exurban value plays: Star, Kuna, Middleton, and Emmett, where USDA-eligible zones make zero-down financing possible within commuting distance of major employers. And it covers Mountain Home's military micro-market for VA-eligible buyers near the Air Force Base.

Tax Credits and Savings Programs

Beyond down payment assistance, Idaho offers the Mortgage Credit Certificate -- a $2,000/year federal tax credit that lenders factor directly into your DTI, increasing the loan amount you qualify for. The guide covers the MCC's eligibility requirements, the 27 targeted counties where the three-year first-time buyer rule is waived, and the lifetime value that can exceed $50,000. It also covers the Idaho First-Time Home Buyer Savings Account ($15,000/$30,000 annual deductions, $100,000 lifetime cap) and how to open one 12 to 24 months before buying to maximize tax savings.

RE-21 Contract Mechanics and the RE-10 Deadline

The RE-21 is Idaho's standard purchase agreement. The guide walks through the entire timeline from mutual acceptance through recording. It covers earnest money delivery (1% to 3%, within 3 business days), the inspection window (5 business days), the financing contingency (10 business days), and the final walk-through (3 days before closing). Most importantly, it explains the RE-10 Inspection Contingency Notice -- the most critical deadline in your transaction. If you miss the 5:00 PM deadline on the fifth business day, Idaho contract law treats your silence as unconditional acceptance. You waive all inspection objections, assume full liability, and your earnest money becomes non-refundable. The guide covers all three RE-10 options, the appraisal protection built into the RE-21, and why you should set a calendar alarm for 24 hours before.

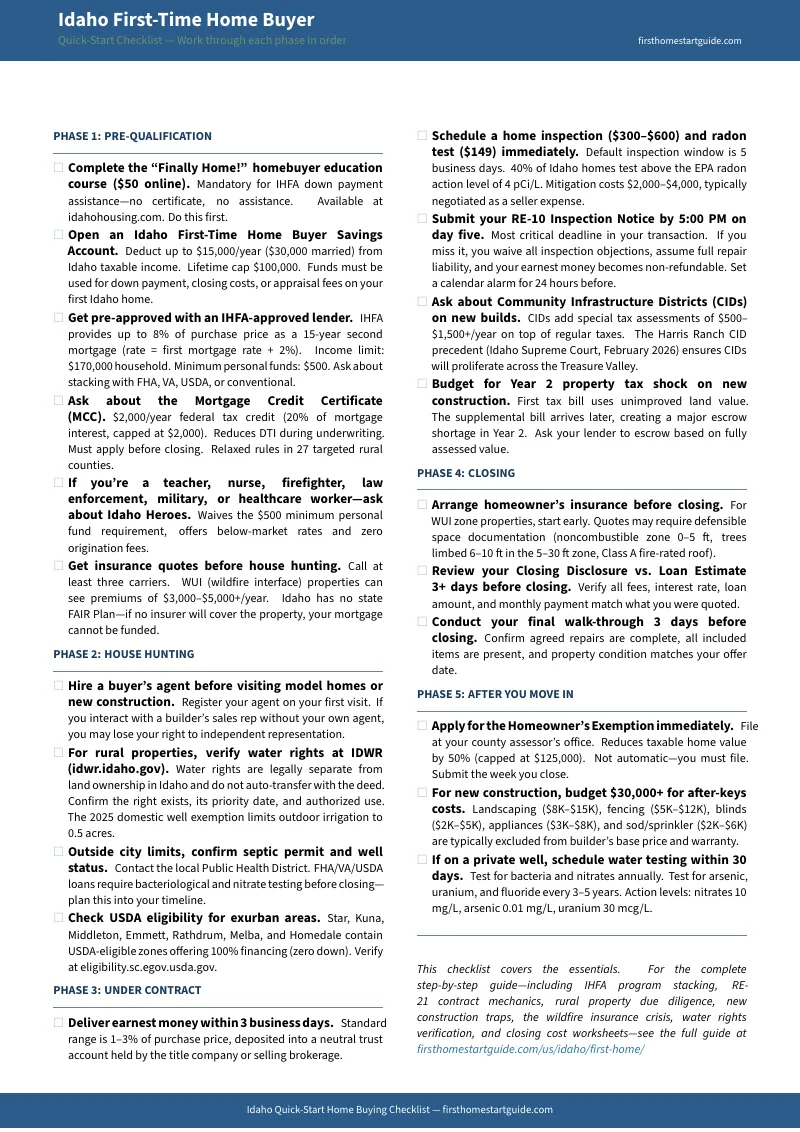

Quick-Start Checklist

A structured checklist covering five phases -- pre-qualification, house hunting, under contract, closing, and after you move in -- with the specific Idaho deadlines, program requirements, and verification steps you need at each stage. Print it and check items off as you go.

Standalone Printable Tools

Every paid download includes 8 standalone tools you can print and bring to your lender meeting, home inspection, or closing appointment:

- Down Payment Assistance Worksheet -- IHFA Second Mortgage, Idaho Heroes, Boise HOP, and MCC programs with a fillable stacking calculator

- Water Rights Reference -- prior appropriation explained, IDWR database search process, well testing requirements, and the 2025 Domestic Well Exemption

- New Construction Worksheet -- the $30,000+ after-keys cost budget itemized, builder contract red flags, CID assessment check, and Year 2 tax shock warning

- Homeowner's Exemption Reference -- filing instructions, CID detection, supplemental tax defense, and the competing July/April/September deadlines

- Inspection Checklist -- general inspection, radon testing, well and septic items, WUI zone assessment, and every due diligence item

- Closing Cost Worksheet -- line-by-line buyer and seller closing costs with Idaho's $0 transfer tax advantage

- Regional Market Reference -- Treasure Valley, Coeur d'Alene, and Eastern Idaho at a glance with pricing, competition, and USDA eligibility

- Closing Timeline -- your 30-to-45-day roadmap from offer to keys with RE-21/RE-10 deadlines

Who This Guide Is For

This guide is for first-time home buyers in Idaho who:

- Are relocating to the Treasure Valley from California, Washington, or Oregon -- and need to understand why "affordable Idaho" now means $450,000+ medians in Boise, which exurban communities still qualify for USDA zero-down loans, how water rights work differently from anything you've experienced, and why the closing process has no attorney unless you hire one

- Are renting in Boise or Meridian and watching rent climb toward mortgage-payment territory -- and need to know whether buying makes financial sense right now, how to stack IHFA assistance with FHA or conventional financing to get in with as little as $500 out of pocket, and which nearby markets (Nampa, Caldwell, Star, Kuna) offer more house for the money

- Are a teacher, nurse, firefighter, law enforcement officer, or military family at Mountain Home AFB -- and want the Idaho Heroes program details, VA loan stacking strategy, and the specific programs that can eliminate your out-of-pocket costs entirely

- Are considering new construction in the Treasure Valley -- and need the builder contract review protocol, the $30,000 after-keys cost budget, the CID assessment question to ask before signing, and the Year 2 property tax shock that most lenders won't warn you about

- Are buying rural or semi-rural property with a well and septic -- and need to understand water rights verification, the 2025 Domestic Well Exemption limits, well water testing requirements for government-backed loans, and septic inspection procedures

- Want every Idaho-specific program, tax structure, insurance crisis, water rights requirement, and closing cost in one reference -- instead of assembling it from IHFA program sheets, IDWR databases, county assessor websites, Idaho Supreme Court rulings, and Reddit threads designed to vent frustration, not structure a transaction

Why Not Free Tools and Forums?

Free information on buying a home in Idaho exists. Here's what it actually delivers:

- IHFA's website publishes program guidelines, interest rates, and income limits. It doesn't show you how the second mortgage payment reduces your purchasing power, doesn't compare stacking strategies across FHA, VA, USDA, and conventional loans, and doesn't explain how the Boise HOP program layers on top for qualifying buyers. You get the program specs without the decision framework.

- Zillow and Realtor.com show estimated monthly payments using generic tax rates. Idaho's Homeowner's Exemption, CID assessments, pressurized irrigation fees, and Year 2 supplemental tax bills make those estimates unreliable -- often by hundreds of dollars per month. No listing platform flags whether a property is in a CID, whether water rights transfer with the deed, or whether the WUI zone makes it effectively uninsurable. You get a number that looks affordable and may not be.

- Real estate agent blogs promote the Boise lifestyle, highlight mountain views, and mention IHFA assistance in passing. They don't explain builder contract arbitration clauses, don't quantify the after-keys bill, and never mention the CID assessments that their developer partners would prefer buyers not calculate until after closing. The content generates leads. It doesn't identify reasons to slow down.

- Reddit threads (r/Boise, r/Idaho) contain genuine buyer experiences -- builder complaints, sticker shock from transplants, frustration from locals earning $140,000 who still can't comfortably afford Boise. But advice from 2023 doesn't reflect the 2025 Domestic Well Exemption, the February 2026 CID Supreme Court ruling, or current IHFA rates. Sorting current from outdated takes longer than reading a guide that has already done it.

This guide fills the Idaho-specific gap -- the space between knowing how to buy a house in general and knowing how to buy one in a state where down payment assistance is a repayable second mortgage (not a grant), where water rights are legally separate from land ownership, where no attorney sits at closing unless you hire one, where new construction generates $30,000+ in undisclosed post-closing costs, where CID assessments create invisible tax burdens validated by the state Supreme Court, and where wildfire risk can make a property uninsurable with no state fallback. It's the analysis that would take an IHFA-approved lender, an Idaho water rights attorney, and a regional market analyst to assemble -- structured as a reference you own permanently.

-- Less Than One Hour With a Real Estate Attorney

An Idaho real estate attorney charges $500 to $1,500 to review a builder contract. A new construction after-keys bill runs $30,000 to $40,000. Choosing the wrong IHFA stacking strategy can mean paying thousands more out of pocket than necessary. Missing the Homeowner's Exemption filing means losing the 50% taxable value reduction on your home. Skipping a water rights verification on rural property can mean owning land you can't legally irrigate. And making an offer on a WUI property without checking insurance first can mean discovering your mortgage is unfundable after your earnest money is committed.

This guide doesn't replace your real estate agent or your lender. But it gives you the IHFA program analysis, water rights verification process, new construction cost framework, property tax defense strategy, insurance crisis assessment, and RE-21 contract mechanics that ensure you identify every Idaho-specific risk before your earnest money is at stake -- instead of discovering them on your supplemental tax bill, your first CID assessment, or the day your title agent tells you they can't answer your legal question.

If it catches a single CID assessment you didn't know about, prevents a single water rights oversight, or saves you from a $30,000 after-keys surprise you hadn't budgeted for, it pays for itself before you've finished reading it.

30-day money-back guarantee. If the guide doesn't sharpen your decision-making and protect your investment in Idaho's unique real estate landscape, you pay nothing.

Download the free Idaho Quick-Start Home Buying Checklist to see the action plan covering pre-qualification, house hunting, offer strategy, closing preparation, and post-closing protection. When you're ready for the full IHFA decision framework, water rights due diligence protocol, new construction cost breakdown, property tax defense strategy, and regional market analysis, the complete guide is here.

The house looks perfect on Zillow. This guide tells you whether Idaho agrees.