The Yield Looks Great on Paper. Kansas's Localized Traps Will Eat It Before You Cash Your First Rent Check.

You found a duplex in Wichita listed at $165,000 that projects a 7% gross yield. Or a three-bedroom near Fort Riley where BAH covers the entire monthly payment. Or a workforce housing unit in Kansas City, KS priced at half of what you'd pay across the state line in Missouri. Kansas ranks third nationally in investor acquisition share at 18.4%. No state transfer tax. No rent control. A 3-day eviction notice for nonpayment. The fundamentals look bulletproof.

Then the localized reality arrives. Your Kansas City, KS property sits in Wyandotte County, where mill levies push the effective property tax rate above 1.72% — on a $250,000 property, that's $4,300 to $4,500 in annual taxes, compressing your NOI far below what the 11.5% assessment rate implied. Your Fort Riley tenant receives PCS orders and terminates the lease with zero financial penalty under the SCRA — and if you're on a month-to-month arrangement, K.S.A. 58-2570(b) gives them just 15 days' notice. Your Wichita cash-flow property goes to eviction court, and you lose — experienced property managers report losing approximately half of contested cases that should have been straightforward. You skip the radon test on a basement rental, and one in four Kansas homes exceeds the EPA action level of 4.0 pCi/L, exposing you to habitability liability under K.S.A. 58-3078a. A single hail storm triggers your wind/hail deductible — not a flat $1,000, but 1% to 5% of your dwelling's replacement cost — and a $6,000 out-of-pocket expense wipes out your entire year of cash flow.

Here's what no single resource explains: Kansas layers a zero-transfer-tax advantage against county-by-county mill levy traps (Wyandotte's Downtown SSMID adds 8.954 additional mills on top of already-high rates), percentage-based insurance deductibles that replace flat-dollar amounts in Tornado Alley, federal military housing protections that override your lease terms, environmental hazards requiring certified testing in one of every four homes, a short-term rental regulatory patchwork where a strategy that's legal in Wichita requires months of Special Use Permit processing in Kansas City, KS, and an LLC closing mechanic that rejects standard Powers of Attorney. Each of these has cost real investors thousands because the information existed — scattered across county appraiser portals, DoD BAH tables, KDHE radon maps, KSA statutes, and BiggerPockets threads — but nobody had assembled it into a single underwriting system calibrated to Kansas.

The Kansas Investment Property Guide is a Kansas Investor Compliance System — not a motivational overview of Midwest real estate, but a structured due diligence framework that maps every Kansas-specific financial trap, regulatory restriction, and tax mechanic into a process you work through before you commit capital. It replaces months of cross-referencing county tax portals, military housing offices, state statutes, and insurance agents with a single reference that tells you exactly what to verify, exactly what the numbers should look like, and exactly where deals go wrong in this state.

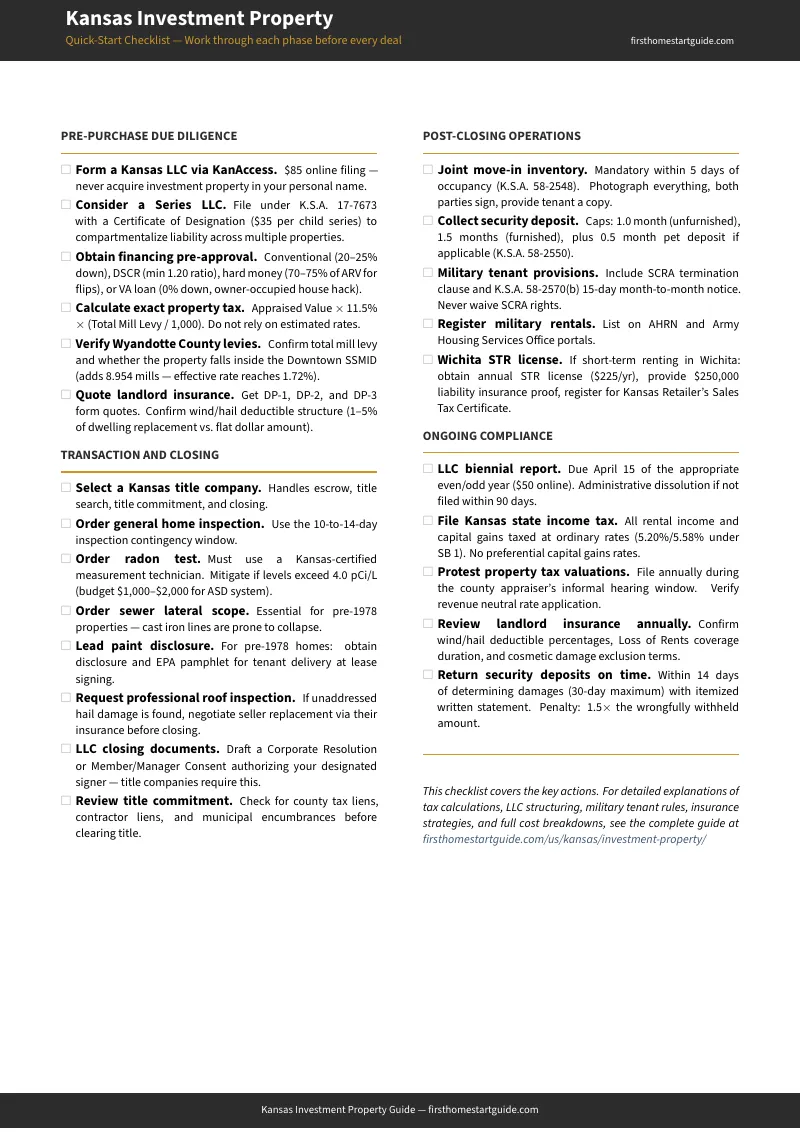

What's Inside the Kansas Investor Compliance System

A comprehensive guide plus 9 standalone worksheets, reference cards, and checklists — covering every stage from market selection through post-purchase operations, built specifically for the regulatory mechanics and tax structures that make Kansas different from every other state:

Submarket Deep Dives Across Four Investment Corridors

Kansas contains four distinct investment ecosystems, each with different entry points, yield profiles, and risk exposures. Wichita (Sedgwick County) offers $120,000–$180,000 entry with 5.02% gross yields, anchored by Spirit AeroSystems, Textron Aviation, and McConnell AFB — but municipal judges have shifted tenant-friendly in contested evictions, and you need to price that risk into your underwriting. The Kansas City Metro splits across a state line that creates fundamentally different tax, regulatory, and yield structures on each side — Johnson County's affluent $589,350 median with 4.88% yields versus Wyandotte County's $245,000 workforce play with 5.88% yields and the mill levy trap that erases the advantage. Fort Riley and Fort Leavenworth offer recession-proof rental income backed by federal BAH stipends — but SCRA termination rights, seasonal PCS vacancy cycles, and on-post housing competition from privatized providers create operational patterns you must model before you buy. Rural and university towns — Lawrence (3.09% yield, University of Kansas demand), Topeka (4.90% yield, state government employment), Emporia (6.16% yield, highest in the state) — deliver long-term tenancy and minimal regulatory friction at the cost of micro-market economic concentration risk.

The Wyandotte County Mill Levy Trap

Kansas assesses residential property at 11.5% of fair market value — lower than Missouri's 19%. Investors see that number and assume Kansas-side properties carry lighter tax burdens. In Wyandotte County, they're wrong. The county's total mill levy has remained above 72 mills, driving effective property tax rates to approximately 1.72%. The Downtown Kansas City, KS Self-Supported Municipal Improvement District (SSMID) adds another 8.954 mills on top. On a $250,000 property, that's $4,300 to $4,500 in annual property taxes — an NOI compression that changes the entire investment thesis. The guide includes the exact tax formula (Appraised Value × 11.5% × Mill Levy ÷ 1,000), historical mill rate data from 2022 to 2025, and a comparison against Johnson County, Jackson County (MO), and rural Kansas counties so you model the actual liability before you make an offer.

Military Rental Investment Mechanics

Investing near Fort Riley or Fort Leavenworth means pricing your rental to capture the Basic Allowance for Housing (BAH) paid directly to service members by the federal government. The guide includes complete 2026 BAH rate tables for both installations — E-5 through O-4 pay grades, with and without dependents — so you can set rent at the exact level that aligns with your target tenant's stipend cap. Fort Leavenworth commands higher rates ($2,133 for an E-6 with dependents versus $1,782 at Fort Riley) because it houses mid-career officers attending the Command and General Staff College. But the operational mechanics are strict: under the SCRA, tenants can terminate leases with zero financial penalty upon receiving PCS or deployment orders. The lease ends 30 days after the next periodic rent date. For month-to-month tenancies, Kansas law (K.S.A. 58-2570(b)) gives military tenants only 15 days' notice — bypassing the standard 30-day requirement. PCS cycles peak in summer, and a winter termination can leave you with a multi-month vacancy. The guide covers BAH-aligned pricing strategies, SCRA-compliant lease structures, AHRN registration with the base housing office, and vacancy reserve modelling for military turnover cycles.

Eviction Process Compliance Flowchart

Kansas offers one of the fastest eviction notice periods in the country — 3 days for nonpayment of rent. But a single procedural error can get your case dismissed. If you serve the 3-Day Notice via mail instead of hand delivery, Kansas law automatically adds two additional days, turning it into a 5-day notice — and filing before the extended period expires voids the case. For lease violations, you must issue a 14/30-Day Notice: the tenant gets 14 days to cure, and if they fail, the lease terminates on day 30. Repeat violations within the same lease term allow a non-curable 30-day notice with no opportunity to cure. Forcible detainer filing fees are tiered: $35 for claims under $500, $55 for $500–$5,000, $101 for claims over $5,000. After a judgment, the sheriff must execute the Writ of Restitution within 14 days. Self-help evictions — changing locks, shutting off utilities — carry a statutory penalty of 1.5 months' rent. And if the tenant leaves belongings behind, you must store them for 30 days, publish a newspaper notice 15 days before disposal, and mail a copy to the tenant within 7 days of publication.

Insurance and Environmental Hazard Framework

Kansas sits in the heart of Tornado Alley, and insurance carriers have responded by replacing flat-dollar deductibles with percentage-based wind/hail deductibles. A 2% deductible on a $300,000 replacement cost means $6,000 out-of-pocket before insurance pays a dime — a single roof replacement after a hail storm can wipe out your entire year of cash-on-cash return. Many carriers now include cosmetic damage exclusions: metal roofs or siding damaged by hail that remain structurally functional will not be repaired or replaced. The guide covers DP-1, DP-2, and DP-3 policy form differences, wind/hail percentage buy-down riders, Loss of Rents coverage for tornado-damaged properties (repairs can take 6 to 12 months in post-disaster zones), and how to build a dedicated reserve account based on your actual percentage deductible. On the environmental side: 25% of Kansas homes contain radon levels at or above 4.0 pCi/L. Under K.S.A. 58-3078a, all residential sales contracts must include state-approved radon warning language. Renting a basement apartment with untested or elevated radon levels exposes you to habitability liability under the KRLTA. Active soil depressurization systems cost $1,000 to $2,000 — far less than the legal exposure from not testing.

Tax Strategy and Entity Structure

Kansas consolidated its income tax brackets under 2024 Senate Bill 1 into a two-bracket system: 5.20% on income up to $23,000 ($46,000 married) and 5.58% above that. Capital gains are taxed at ordinary rates — no preferential treatment at the state level for long-term holds. The guide covers 1031 exchange full conformity, cost segregation studies for accelerated depreciation on rental properties, the $75,000 school finance levy exemption under K.S.A. 79-201x, and the revenue neutral rate framework that requires public hearings when counties exceed the prior year's tax revenue. For entity structure: form a Kansas LLC online via KanAccess for $85 (reduced from $160 in February 2026), file a biennial (not annual) report for $50, and consider a Series LLC under K.S.A. 17-7673 ($35 per child series) if you're building a multi-property portfolio. The guide explains why a personal Power of Attorney won't work for LLC closings, why you need a Corporate Resolution or Member/Manager Consent, and the 90-day administrative dissolution timeline if you miss a biennial report.

Short-Term Rental Regulatory Matrix

Kansas regulates STRs at the municipal level, creating a patchwork that varies dramatically by city. In Wichita, owner-occupied STRs are permitted by right in residential zones. Non-owner-occupied units require an Administrative or Special Use Permit — and if 50% or more of notified neighbors object, it goes to a public hearing. The annual license fee is $225, you need $250,000 in general liability insurance, and you must designate a local contact if you live more than 30 miles from the property. In Kansas City, KS, the process is far more restrictive: a mandatory pre-application meeting with the Planning Department, a neighborhood meeting at least 14 days before the Planning Commission hearing, mailed notices to all property owners within 200 feet, a physical zoning sign posted 20 days before the hearing, and a home inspection. Budget months, not weeks. Both cities require Kansas Retailer's Sales Tax registration.

Who This Guide Is For

- Out-of-state investors moving capital from coastal markets into Kansas's affordable entry points — who need to understand mill levy calculations, percentage-based insurance deductibles, and closing mechanics they won't encounter in their home states

- Military investors and service members using VA loans for house-hacking near Fort Riley or Fort Leavenworth — who need BAH-aligned pricing strategies and SCRA-compliant lease structures

- Kansas City metro cross-state investors evaluating whether to buy on the Kansas or Missouri side — who need to model the true tax burden in Wyandotte County versus Jackson County's 1% earnings tax

- Wichita-focused cash-flow investors targeting workforce housing in Delano, Fairmount, or West Wichita — who need realistic expectations about the municipal court eviction environment

- Rural and university town buyers targeting long-term holds in Lawrence, Topeka, or Emporia — who need to navigate septic regulations, radon testing, and micro-market economic concentration risk

- First-time landlords in Kansas who need the KRLTA compliance roadmap — joint move-in inventory within 5 days, security deposit caps, eviction notice sequences, and abandoned property procedures — to avoid the 1.5x statutory penalty for wrongful deposit withholding

Why Not Free Tools and Forums?

Free information on Kansas real estate investing exists. Here's what it actually delivers:

- BiggerPockets forums are where someone in a 2023 thread recommends Kansas City, KS for its low entry prices, someone else in 2024 warns about Wyandotte County's mill levies, and a third poster debates whether the insurance premium increases justify a higher deductible. You'll find genuinely useful experience reports mixed with advice that predates the February 2026 LLC fee reduction, this year's mill rate adjustments, and the current BAH tables. Sorting current from outdated takes longer than reading a guide that has already done it.

- County appraiser websites give you mill levy tables and assessment ratios. They don't explain how the revenue neutral rate framework affects future tax bills, don't compare Wyandotte County's effective rate against Johnson County or rural counties, and don't show you how the SSMID surcharge compounds on downtown KCK properties. You get the raw numbers without the underwriting context that determines whether the deal works.

- Military housing websites publish BAH rate tables and installation guides. They don't explain how to align rental pricing to specific rank brackets, how SCRA termination timelines interact with Kansas's month-to-month notice exception, or how PCS cycle seasonality creates predictable vacancy windows that must be modelled in your cash flow. You get the stipend amounts without the investment strategy that captures them.

- National investing courses and books teach cap rate, DSCR, and 1031 exchange mechanics that apply everywhere. They don't cover Kansas's percentage-based wind/hail deductibles, the Wyandotte County mill levy trap, K.S.A. 58-3078a radon disclosure requirements, the KRLTA's 5-day joint inventory mandate, or the difference between Wichita's STR licensing and KCK's multi-month Special Use Permit process. Applying national frameworks to Kansas-specific structures is how investors model the wrong insurance cost, the wrong tax rate, or the wrong eviction timeline.

This guide fills the Kansas-specific gap — the space between knowing how to analyze a rental property in general and knowing how to underwrite one in a state where county-level mill levies, federal military housing protections, percentage-based insurance mechanics, radon habitability liability, and municipality-specific STR regulations can each independently turn a profitable deal into a losing one. It's the analysis that would take a Kansas real estate attorney, a local insurance agent, a military housing specialist, and a county property tax consultant to assemble — structured as a reference you own permanently.

— Less Than One Property Inspection

A single home inspection in Kansas runs $400 to $530. A radon mitigation system you didn't budget for costs $1,000 to $2,000. Modeling the wrong mill levy rate on a Wyandotte County property means overestimating your NOI by $2,000+ per year for the life of the investment. A self-help eviction — changing the locks on a tenant instead of following the KRLTA's 3-day notice process — carries a statutory penalty of 1.5 months' rent. A wind/hail deductible you didn't understand can cost $6,000 on a single claim.

This guide doesn't replace your real estate attorney or your insurance agent. But it gives you the mill levy calculator, BAH pricing framework, eviction compliance flowchart, insurance deductible analysis, and entity structure roadmap that ensure you identify every Kansas-specific risk before you're contractually committed — instead of discovering them on your first tax bill, your first SCRA termination, or your first insurance claim.

If it catches a single mill levy miscalculation, prevents a single eviction procedural error, or saves you from the wrong insurance deductible structure on a six-figure acquisition, it pays for itself before you've finished reading it.

30-day money-back guarantee. If the guide doesn't sharpen your underwriting and protect your capital in Kansas's investment landscape, you pay nothing.

Download the free Kansas Quick-Start Home Buying Checklist to see the due diligence framework covering pre-purchase research, LLC formation, property inspections, closing mechanics, and post-purchase compliance. When you're ready for the full mill levy analysis, BAH pricing system, eviction compliance flowchart, and submarket-by-submarket investment breakdown, the complete guide is here.