You Found the House. But It's an Estate Property with No Succession Filed, You're About to Waive Your Right to Sue for Hidden Defects, and the $55,000 in Forgivable Assistance Disappears If the Home Sits in a Flood Zone.

You found a renovated shotgun house in Mid-City New Orleans listed at $280,000. Or a three-bedroom in Livingston Parish where the seller inherited it from a parent. Or a starter home in Baton Rouge where the listing says "$1,600/month PITI" and the neighborhood sits two miles from the bayou. You ran the numbers. You got pre-approved. You're ready to make an offer.

Then Louisiana happens. The title search reveals the parent's succession was never opened, two of the seller's siblings are forced heirs under the age of 24, and a Judgment of Possession must be obtained before anyone can legally sell the property. Your agent hands you the standard purchase agreement with a Waiver of Redhibition --- and you sign it without knowing you just surrendered your right to sue the seller for the cracked foundation piers hidden beneath the raised house. Your spouse isn't on the mortgage note, but under community property law the notary won't execute the Act of Sale unless your spouse signs the mortgage instrument too. The termite bond lapsed three years ago, and a new initial treatment costs $2,400. The LHC Resilience Soft Second program would have provided $55,000 in forgivable assistance, but the property sits in Zone AE, so it's categorically ineligible.

Here's what no single free resource explains: Louisiana is the only state in the nation that operates under civil law derived from the Napoleonic Code, meaning the legal terminology is wrong, the closing process is wrong, and the property inheritance rules are wrong in every national home buying guide you've read. The closing is an Authentic Act of Sale executed before a Notary Public and two witnesses --- not a warranty deed through escrow. Children under 24 cannot be disinherited regardless of what any will says, which means estate properties require forced heirship verification before the title is merchantable. The Waiver of Redhibition you'll be asked to sign strips you of a powerful legal protection that doesn't exist in any other state --- and courts enforce it aggressively even when the seller's disclosure was incomplete. Meanwhile, the LHC Resilience Soft Second offers up to $55,000 in forgivable down payment assistance plus $5,000 for closing costs, but only for Zone X properties in designated disaster parishes, while the New Orleans Direct Homebuyer program offers similar amounts but permits flood zone purchases at the cost of mandatory flood insurance running $3,000 to $8,000 annually under FEMA Risk Rating 2.0. Formosan termite bonds are non-negotiable in this climate, and the structural subsidence beneath New Orleans means every pier-and-beam home needs a foundation evaluation, not just an inspection. Each of these has cost real first-time buyers five figures because the information existed --- scattered across LHC eligibility matrices, the Louisiana Civil Code, parish assessor databases, FEMA flood maps, and Reddit threads --- but nobody had assembled it into a single system calibrated to how Louisiana's civil law actually works.

The Louisiana First-Time Home Buyer Guide is a Civil Law Transaction System --- not a motivational overview of bayou living, but a structured reference that maps every Louisiana-specific legal mechanic, subsidy program, insurance requirement, and inspection priority into a process you work through before you sign a waiver you don't understand and lose protections that don't exist in any other state. It replaces months of cross-referencing the Louisiana Civil Code, LHC program matrices, FEMA flood zone maps, parish assessor records, and forum posts with a single guide that tells you exactly what to verify, exactly what the numbers should look like, and exactly where deals go wrong in this state.

What's Inside the Civil Law Transaction System

A comprehensive guide, a quick-start checklist, and 8 standalone printable tools (10 PDFs) --- covering every stage from pre-approval through post-closing filing, built specifically for the civil law framework, subsidy programs, and environmental risks that make Louisiana different from every other state:

The Civil Law Framework: Community Property, Forced Heirship, and Successions

Louisiana is the only state whose legal system derives from the Napoleonic Code, not English common law. Every piece of national home buying advice you've read assumes common law. In Louisiana, the defaults are different. Married buyers operate under community property (Civil Code Article 2338), meaning any property acquired during the marriage is owned jointly regardless of whose name is on the note --- and the non-borrowing spouse must sign the mortgage instrument or your lender cannot close. The guide explains the community property regime, how it affects DTI calculations when the non-borrowing spouse carries debt, and the formal process for establishing a separate property regime via matrimonial agreement. It covers forced heirship (Article 1493) --- Louisiana's unique law that prevents parents from disinheriting children under 24 --- and why this means estate properties require verification that no forced heirs were deprived of their legitime before the title is insurable. It walks through the succession process (Louisiana's version of probate), the Judgment of Possession requirement, the Small Succession Affidavit for estates under $125,000, and usufruct versus naked ownership --- the split that occurs when a surviving spouse has the right to use the property but the children hold the underlying title.

The Act of Sale and the Louisiana Closing Process

National guides tell you to expect a warranty deed through escrow. In Louisiana, property is transferred via an Act of Sale executed as an Authentic Act --- signed simultaneously by buyer, seller, Notary Public, and two competent witnesses. The guide covers the LREC Residential Agreement to Buy or Sell (Louisiana's standardized purchase contract), the 10-15 day due diligence and inspection period, the 30-year title abstract requirement, the title opinion rendered by a Louisiana-licensed attorney, the curative period for clearing title defects (15-45 days, seller pays), and why it is standard practice to close through a title company operated by a real estate attorney even though non-attorney notaries in Louisiana hold vastly broader powers than notaries in any other state.

Redhibition and the As-Is Waiver

Louisiana has a unique buyer protection called redhibition that lets you sue the seller for hidden defects discovered after closing. And Louisiana sellers universally demand you waive it. The Waiver of Redhibition is the single most consequential document you'll sign, and most first-time buyers treat it as a formality. The guide explains the legal doctrine, the Spradley v. Perez precedent (where the court enforced the waiver against a buyer who discovered total foundation failure years later), and why this makes your due diligence period the most important phase of the entire transaction. It specifies the minimum inspection scope for a Louisiana purchase: general inspection, WDIR, foundation evaluation for raised structures, mold assessment, HVAC dehumidification check, sewer scope, and lead paint inspection for pre-1978 historic stock.

Government Programs and the $60,000 Assistance Playbook

Louisiana offers some of the most aggressive homebuyer subsidy programs in the country. The guide breaks down every program with exact dollar amounts, eligibility thresholds, and the restrictions that disqualify buyers who don't verify them before going under contract. LHC Resilience Soft Second: up to $55,000 + $5,000 closing costs, 0% deferred, forgiven after 10 years, but Zone X only in 51 designated disaster parishes. New Orleans Direct Homebuyer: $55,000 + $5,000, permits flood zones, caps sales price at $324,000. Lagniappe Advantage Program (LAP): 0-4% grant in Jefferson and surrounding parishes, stackable with MCCs, plus the Heroes to Homeowners $2,500 bonus. Capital Area Finance Authority: non-repayable 5% grant in East Baton Rouge. Keys for Service: $10,000 for teachers, police, fire, EMS. Delta 100: 100% financing in Delta parishes. MRB programs: 4-9% DPA grants. The stacking strategy section shows how to match your income, location, and flood zone status to the optimal program combination.

Flood Insurance, Risk Rating 2.0, and the Insurance Cliff

Approximately 80% of NFIP policyholders in Louisiana saw immediate premium increases when FEMA rolled out Risk Rating 2.0. New buyers without an assumable existing policy can face the full actuarial rate immediately --- $3,000 to $8,000+ annually. The guide covers the new property-specific pricing methodology (distance to water, elevation, flood type, replacement cost), the 18% annual glide path cap on grandfathered policies, the trajectory from a $1,200 baseline to $3,800+ over eight years, why Zone X doesn't guarantee safety (the 2016 Baton Rouge floods devastated Zone X neighborhoods), when private flood insurance alternatives offer 20-40% savings, and the critical due diligence steps: FEMA flood zone lookup, Elevation Certificate, prior claims history, and pre-closing insurance quotes from both NFIP and private markets.

Formosan Termites, Subsidence, and Environmental Due Diligence

Louisiana has the worst Formosan subterranean termite infestations in the United States. The WDIR (Wood Destroying Insect Report) is mandatory for VA loans and standard for all transactions. But the real cost is the termite bond: $1,000-$2,500+ for initial treatment if no active bond exists, plus $150-$300 annually for maintenance. If drywood termites are found, full tenting runs $3,000-$10,000. The guide covers the statutory transferability of termite contracts (LA RS 3:3370), how to negotiate the bond transfer, and what happens when the bond has lapsed. It also covers subsidence --- the gradual sinking of ground in New Orleans and coastal parishes that cracks foundations and damages plumbing --- humidity-driven mold risks, HVAC oversizing problems, and lead paint in pre-1978 historic stock.

Property Taxes, the Homestead Exemption, and Closing Costs

Louisiana assesses residential property at exactly 10% of fair market value, then applies local millage rates that vary dramatically by parish and taxing district. The guide includes a worked example showing the full calculation from assessor's determination through final tax obligation, the Homestead Exemption (first $75,000 of fair market value exempt from most property taxes, saving $750-$1,200+ per year depending on millage rates), the filing deadline (December 31 of the year of acquisition --- miss it and you pay full unexempted taxes), the 100% VA disability complete exemption, and a closing cost breakdown for a $225,000 purchase showing every line item from origination fee through initial escrow.

Financing: FHA, VA, USDA, and the Community Property DTI Trap

The guide covers conforming loan limits ($832,750 uniformly across all 64 parishes), FHA ($524,225 with 3.5% down), VA (zero down, concentrated around Fort Johnson and Barksdale AFB with BAH-driven purchase power), and USDA (100% financing in Louisiana's extensive rural footprint). A complete financing worked example shows how an FHA + LHC Resilience Soft Second combination eliminates cash-at-closing for a buyer earning 75% AMI: the $45,000 soft second covers the down payment, the $5,000 grant covers closing costs, and the monthly PITI runs $1,814-$1,964 on a $225,000 home. The community property section explains why some lenders evaluate both spouses' debts for DTI even when only one spouse's income qualifies, and when a matrimonial agreement changes the picture.

Regional Market Profiles: New Orleans, Baton Rouge, Lafayette, Shreveport

Every Louisiana metro has different pain points. New Orleans: insurance costs of $8,000-$12,000 annually dominate affordability, subsidence is a certainty not a risk, and historic stock requires specialized inspectors. Baton Rouge: the 2016 Great Flood permanently altered the market --- verify post-flood remediation and elevation certificates. Lafayette: the best purchasing power in the state ($160,000-$250,000) with lower insurance and moderate flood risk, but tied to oil and gas cycles. Shreveport/Bossier City: the most stable insurance market in Louisiana, dominated by VA loans tied to Barksdale AFB. A regional comparison table maps median entry price, insurance burden, flood risk, and key subsidy for each metro.

30-45 Day Closing Timeline

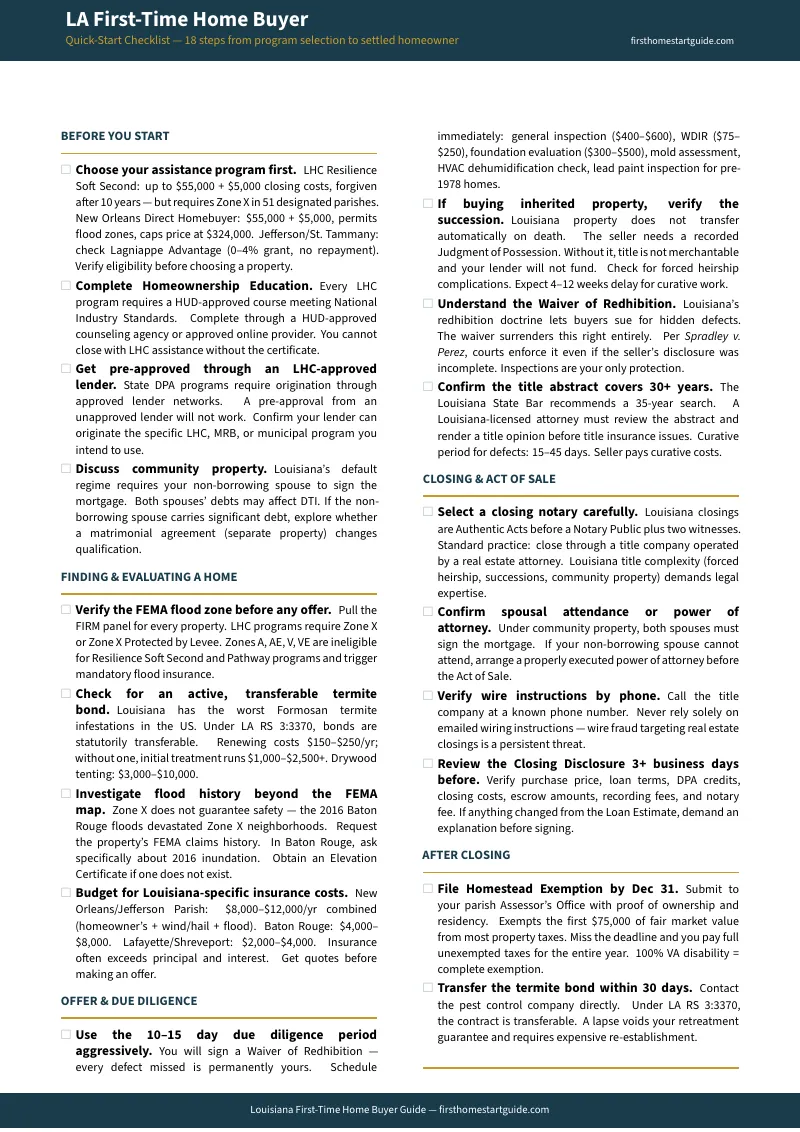

A week-by-week timeline from contract execution through post-closing, with specific Louisiana deadlines mapped: earnest money delivery, the 10-15 day due diligence window, the 30-year title abstract commissioning, the curative period for succession and forced heirship issues, the Closing Disclosure review, spousal attendance confirmation, the Authentic Act of Sale execution, and post-closing deadlines for homestead exemption filing, termite bond transfer, and flood insurance setup.

8 Standalone Printable Tools

Every tool is a separate PDF you can print and use independently --- at your lender's office, during due diligence, or pinned to your wall during closing:

- Carrying Cost Worksheet --- fill in the numbers for any property: PITI, flood insurance, wind/hail, homeowner's, termite bond, property tax after homestead exemption. Includes a worked example for a $225,000 home with LHC assistance plus closing cost estimates.

- DPA Decision Framework --- side-by-side comparison of LHC Resilience Soft Second, New Orleans Direct Homebuyer, LAP, CAFA, Keys for Service, Delta 100, and MRB programs. Eligibility thresholds, flood zone restrictions, forgiveness terms, and stacking compatibility.

- Closing Timeline --- 30-to-45-day reference card with every phase from contract execution through post-closing deadlines, with fillable fields for your dates and contacts.

- Inspection and Termite Checklist --- due diligence scope covering general inspection, WDIR, foundation evaluation, mold assessment, HVAC dehumidification check, sewer scope, and lead paint. Cost ranges, termite bond negotiation steps, and escalation triggers.

- Homestead Exemption Filing Guide --- step-by-step filing process for the $75,000 exemption, the December 31 deadline, required documentation, the 100% VA disability complete exemption, and parish assessor contact information.

- Civil Law Quick Reference --- one-page reference for community property, forced heirship, successions, usufruct, the Authentic Act of Sale, and the Waiver of Redhibition. The terms and rules that make Louisiana different from every common law state.

- Regional Market Quick Reference --- one-page comparison of New Orleans, Baton Rouge, Lafayette, and Shreveport/Bossier City with entry prices, insurance ranges, flood risk levels, and primary subsidy programs.

- Key Contacts and Resources --- every agency, assessor's office, and government website you need during the Louisiana home buying process, plus fillable fields for your own team contacts.

Who This Guide Is For

This guide is for first-time home buyers in Louisiana who:

- Are buying their first home anywhere in Louisiana and need to understand how the civil law system changes the entire transaction --- the Act of Sale, the Notary Public's role, the Waiver of Redhibition, community property requirements, and the succession process for estate properties --- before they sign documents that work differently than in every other state

- Are relocating from another state and need a clear explanation of why national home buying advice is wrong for Louisiana --- why there's no warranty deed, why a notary closes instead of an escrow company, why children under 24 have inheritance rights that can cloud the title on any estate property, and why the "as-is" clause carries far more legal weight here than anywhere else

- Want to claim every dollar of down payment assistance available and need to understand which program fits their income, location, and flood zone status --- LHC Resilience Soft Second ($60,000, Zone X only), New Orleans Direct Homebuyer ($60,000, flood zones permitted), LAP (no-repayment grant), CAFA (East Baton Rouge grant), or MRB programs --- and which combinations stack

- Need to calculate the true cost of owning in Louisiana --- not just PITI, but flood insurance ($3,000-$8,000+ under Risk Rating 2.0), wind and hail coverage, termite bond maintenance ($150-$300/year), and property tax after the Homestead Exemption --- so their monthly budget reflects what they'll actually pay

- Are active-duty military or veterans buying near Fort Johnson or Barksdale AFB and want to understand VA loan requirements in Louisiana, BAH-driven purchase power, and the VLB programs available to them

- Want every Louisiana-specific legal mechanic, subsidy program, insurance requirement, and inspection priority in one reference --- instead of assembling it from the Louisiana Civil Code, LHC eligibility matrices, FEMA flood maps, parish assessor databases, and Reddit threads that may predate Risk Rating 2.0 or the latest program changes

Why Not Free Tools and Forums?

Free information on buying a home in Louisiana exists. Here's what it actually delivers:

- LHC and municipal program websites publish eligibility tables, income limits, and application procedures. They don't explain how to choose between the Resilience Soft Second and the New Orleans Direct Homebuyer program when your income qualifies for both, don't show how flood zone restrictions interact with your property search, and don't cover parish-level programs that stack on top. You get the program specs without the decision framework that tells you which program to apply for.

- National guides (Zillow, Bankrate, NerdWallet) confidently instruct you to "hire a closing attorney" and "expect a warranty deed." In Louisiana, this advice is wrong. Closings are executed by a Notary Public as an Authentic Act. Children under 24 have forced inheritance rights. The "as-is" clause waives a legal protection that doesn't exist in any other state. Every national guide treats Louisiana as if it follows common law. It doesn't.

- Real estate agent blogs and lender content highlight affordable entry prices and "up to $55,000 in assistance." They minimize the flood zone restriction that disqualifies most urban inventory from the best programs, gloss over the Waiver of Redhibition, and never explain that termite bonds are a non-negotiable carrying cost that can add $2,500 upfront before closing. The content is designed to generate leads, not to explain the civil law traps that cost first-time buyers five figures.

- Reddit threads (r/NewOrleans, r/Louisiana, r/FirstTimeHomeBuyer) contain genuinely useful local experience --- people sharing insurance sticker shock, succession delays, and flood zone surprises. But advice from 2023 doesn't reflect the latest Risk Rating 2.0 premium trajectories, current LHC income limits, or updated program terms. Sorting current from outdated takes longer than reading a guide that has already done it.

This guide fills the Louisiana-specific gap --- the space between knowing how to buy a house in general and knowing how to buy one in the only state where the legal system derives from the Napoleonic Code, where children under 24 have forced inheritance rights, where signing the standard "as-is" clause waives a legal protection no other state offers, where $60,000 in forgivable assistance evaporates if you pick a property in the wrong flood zone, and where termite bonds and flood insurance can double your monthly carrying costs beyond what the listing agent quoted. It's the analysis that would take a Louisiana real estate attorney, an LHC-approved lender, and a licensed pest control operator to assemble --- structured as a reference you own permanently.

--- Less Than One Home Inspection

A single general home inspection in Louisiana runs $400 to $600. A WDIR termite inspection adds $75 to $250. A foundation evaluation for a raised or pier-and-beam home adds $300 to $500. Signing the Waiver of Redhibition without understanding it means you permanently forfeit your right to sue the seller for hidden defects. Choosing a property in Zone AE when you could have stayed in Zone X costs you $55,000 in forgivable assistance. Missing the Homestead Exemption filing deadline by January 1 costs you $750 to $1,200 in property tax savings for the entire year.

This guide doesn't replace your real estate attorney or your lender. But it gives you the civil law framework, DPA decision matrix, flood zone verification protocol, inspection checklist, and closing timeline that ensure you identify every Louisiana-specific risk before you sign the Waiver of Redhibition --- instead of discovering them when the title search reveals an unopened succession, your first flood insurance renewal arrives, or your termite bond transfer falls through.

If it catches a single flood zone disqualification, prevents a single uninformed redhibition waiver, or saves you from missing the Homestead Exemption deadline, it pays for itself before you've finished reading it.

30-day money-back guarantee. If the guide doesn't sharpen your decision-making and protect your deposit in Louisiana's civil law system, you pay nothing.

Download the free Louisiana Quick-Start Home Buying Checklist to see the 18-step action plan covering program selection, flood zone verification, due diligence inspections, the Act of Sale closing process, and post-closing deadlines. When you're ready for the full DPA decision framework, carrying cost worksheet, civil law reference, regional market profiles, and closing timeline, the complete guide is here.

The house looks perfect on Zillow. This guide tells you whether Louisiana agrees.