You Got Pre-Approved. But Nobody Told You That Prince George's County Taxes Your Mortgage on Top of Your Purchase Price, Montgomery County's Recordation Tax Jumps from 0.89% to 2.27% at $500,000, and Your Settlement Attorney Can't Fix the First-Time Buyer Exemption If Your Agent Forgot to Check the Box on the Contract.

You found a three-bedroom in Silver Spring with a Metro-accessible commute. Or a renovated rowhouse in Canton with harbor views. Or a colonial in Bowie where the schools are excellent and your drive to Andrews is 18 minutes. You ran the numbers through Zillow's mortgage calculator, your lender pre-approved you for $425,000, and you're ready to write your first offer.

Then Maryland happens. Your mortgage calculator estimated your monthly payment based on principal, interest, property taxes, and insurance. It didn't account for the 0.50% state transfer tax, the 1.40% county transfer tax Prince George's levies on both the deed and the mortgage, the tiered recordation tax Montgomery County charges at five different rates depending on the bracket, or the fact that Maryland law gives first-time buyers a statutory exemption that cuts the state transfer tax in half and shifts it to the seller — but only if your agent checks the right box on the purchase contract before it's ratified. Your lender, a national call center based in Texas, never mentioned that Maryland is an attorney-settlement state. Your employer's HR portal said nothing about the ground rent on your Baltimore property. And your parents' advice from buying in Ohio in 2004 doesn't account for a state where the closing cost difference between two houses separated by a county line can exceed $10,000.

Here's what no single free resource explains: Maryland layers a state transfer tax system — where first-time buyers get a statutory 50% exemption that shifts the remaining 0.25% entirely to the seller, but only if the exemption is invoked in the purchase contract — against county transfer taxes that range from 0% in Calvert to 1.5% in Baltimore City, against recordation taxes that are flat in some counties and tiered progressively in Montgomery (0.89% to 2.27%), against Prince George's County's unique mortgage tax where the 1.4% local transfer tax applies to the security instrument so low-down-payment buyers are double-taxed, against a colonial-era ground rent system in Baltimore where the house is yours but the land is leased and out-of-state lenders kill the deal when they can't underwrite the leasehold, against the Maryland Mortgage Program with county-specific income limits ranging from $131,700 to $196,680, against a SmartBuy 3.0 program that pays off up to $25,000 in student loans at closing but requires a 720 credit score and full loan balance elimination, against a military stacking strategy where VA + MMP + seller concessions drives cash-to-close to near zero but national lenders refuse to process the paperwork, against the Chesapeake Bay Critical Area Act that caps waterfront lot coverage at 15% and blocks the pool, garage, and deck expansion you were planning. Each of these has cost real Maryland first-time buyers thousands of dollars because the information existed — scattered across DHCD program matrices, SDAT property databases, county recordation tax schedules, Reddit threads from buyers who discovered the Prince George's mortgage tax at settlement, and archived Baltimore Sun articles about ground rent — but nobody assembled it into a single decision system calibrated to how Maryland actually works.

The Maryland First-Time Home Buyer Guide is a Maryland Closing Cost Navigation System — not a motivational overview of the DMV housing market, but a structured reference that maps every Maryland-specific transfer tax, recordation rate, ground rent obligation, state assistance program, military stacking strategy, and environmental restriction into a process you work through before your earnest money is at risk. It replaces months of cross-referencing DHCD income limit tables, SDAT ground rent registries, county recordation tax schedules, and forum threads from buyers who learned the hard way with a single guide that tells you exactly what to verify, exactly what the numbers should look like, and exactly where deals go wrong in this state.

What's Inside the Maryland Closing Cost Navigation System

A comprehensive guide, a quick-start checklist, and 8 standalone printable tools (10 PDFs) — covering every stage from pre-approval through post-closing, built specifically for the tax structures, assistance programs, ground rent laws, and environmental regulations that make Maryland different from every other state:

County-by-County Transfer and Recordation Tax Navigator

Maryland's closing cost structure is nationally unique and financially devastating when misunderstood. The state charges a 0.50% transfer tax, each county adds its own transfer tax (0% to 1.50%), and recordation taxes vary from flat rates to Montgomery County's five-tier progressive system. The guide breaks down every jurisdiction's exact rates — including the first-time buyer exemption that halves the state transfer tax to 0.25% and legally shifts it onto the seller — with worked examples showing exactly what a $400,000 home costs to close in each major county. It covers the Prince George's County mortgage tax trap where the 1.4% local transfer tax applies to both the deed and the security instrument, meaning an FHA buyer with 3.5% down is taxed on the purchase price and then taxed again on the 96.5% mortgage — creating thousands in unexpected dual taxation that Zillow's calculator never shows. It includes the Montgomery County tiered recordation system (0.89% on the first $500,000, jumping to 1.35%, then 2.04%, then higher), the Baltimore City $22,000 exemption for owner-occupied properties, the Frederick County zero-county-transfer-tax advantage, and the exact math for every bracket so your closing cost estimate reflects reality, not a national calculator's state-average approximation.

SmartBuy 3.0 Eligibility and Decision Framework

Maryland's SmartBuy program pays off up to $25,000 of your student loans at closing — arguably the most aggressive first-time buyer program in the country. The guide covers the mechanical reality that loan officers gloss over: the $25,000 is structured as a 0% interest unsecured promissory note forgiven at 20% per year over five years, but your entire student loan balance must be eliminated at closing. If you owe $35,000, SmartBuy covers $25,000 and you bring the remaining $10,000 in cash to the settlement table. It covers the 720 credit score minimum (remarkably high for state assistance), the primary residence requirement, the prohibition on owning other real estate worldwide, the mandatory HUD-approved homebuyer education, and the fixed interest rate trade-off — where you accept a state-set rate instead of shopping the open market, a trade-off that's mathematically favorable for cash-poor buyers but costly for those who plan to refinance within five years and trigger recapture.

Baltimore Ground Rent Identification and Buyout Guide

For buyers exploring Baltimore City and parts of Baltimore County, ground rent is the issue that kills deals and terrifies newcomers. The guide translates the SDAT statutory language into a plain-English flowchart: how to search the SDAT Real Property database for ground rent status, how to check the Ground Rent Registry for the current owner, and how to calculate the redemption price using the statutory capitalization rates (12% for leases created after 1982, 6% for 1888-1982, 4% for 1884-1888, negotiable for older). It covers the out-of-state lender problem — where national underwriters refuse to fund the loan because the leasehold threatens their first-lien position — the VA loan prohibition on ground lease properties that forces military buyers to redeem before closing, the holding company extortion tactic where uninformed buyers pay $6,000 for a $1,000 buyout because they don't know the statutory math, and the "unregistered purgatory" scenario where the ground rent holder is unknown and you must file an affidavit and escrow the redemption amount with SDAT directly.

Military Stacking Strategy (VA + MMP + Seller Concessions)

Active-duty personnel and veterans at Fort Meade, Joint Base Andrews, and Aberdeen Proving Ground have access to a capital stacking strategy that national lenders never mention because it requires too much paperwork. The guide details the exact combination: a zero-down VA loan covers 100% of the purchase price and eliminates PMI, an MMP closing cost grant covers $6,000-$17,500 of Maryland's layered transfer and recordation taxes, and VA-permitted seller concessions of up to 4% of the purchase price cover the remaining settlement friction. The result: the military family's savings remain completely untouched. It covers why national call-center lenders hide this strategy (processing state-level DPA requires manual underwriting and DHCD compliance), which local MMP-approved lenders have closed stacked transactions in the last six months, and the commute-reality check showing that Severn offers a 10-minute drive to Fort Meade's Reece Road gate while a slightly cheaper home across a county line can mean an hour on the Capital Beltway.

Chesapeake Bay Critical Area Restriction Guide

Buyers drawn to Maryland's tidal shorelines in Anne Arundel, Queen Anne's, and Talbot counties routinely underestimate the regulatory power of the Critical Area Act. Within 1,000 feet of tidal waters, total lot coverage — including the house, driveway, decking, patios, walkways, and detached structures — is capped at 15% of the parcel. The guide covers the three zone classifications (Intensely Developed, Limited Development, Resource Conservation), the grandfathered exceptions for pre-1985 lots under half an acre (25% plus 500 square feet), the tree-clearing permit requirements, and the practical reality that most older waterfront homes have already maximized their allowance — meaning the pool, garage addition, and expanded deck you were planning are blocked before you even hire an architect. This section saves Eastern Shore lifestyle buyers from post-purchase renovation shock.

County and Municipal Grant Stacking Guide

Beyond the MMP and SmartBuy, Maryland's county governments operate their own assistance programs — and the guide covers how to stack them. Prince George's County's Pathway to Purchase offers $50,000 in down payment and closing cost assistance as a 0% interest deferred loan forgiven after 15 years, but requires a separate county application with parallel underwriting and a Housing Quality Standard inspection. Baltimore City's Buying Into Baltimore provides $5,000 for attending a Live Baltimore Trolley Tour. The FTHIP offers up to 50% of the required down payment for buyers earning below 80% AMI. Baltimore's Fixed Pricing Program sells city-owned vacant buildings for $1 with a $90,000 rehabilitation commitment. The guide covers the eligibility requirements, application sequences, and the specific trap of running parallel underwriting processes that can delay closings beyond rate-lock windows.

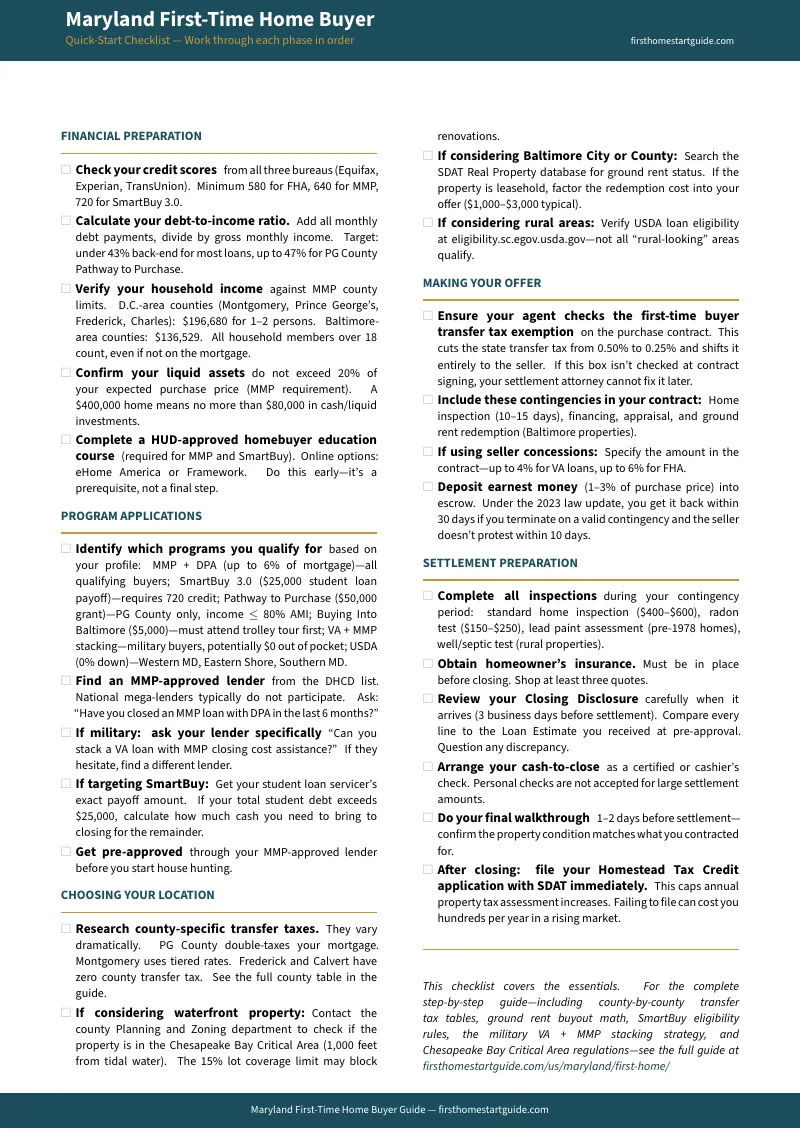

20-Item Quick-Start Checklist

A structured checklist covering five phases — financial preparation, program applications, choosing your location, making your offer, and settlement preparation — with Maryland-specific deadlines, first-time buyer exemption verification, MMP/SmartBuy requirements, ground rent checks, and county-level closing cost calculations at each stage. Print it and check items off as you go.

8 Standalone Printable Tools

Print-ready reference cards and worksheets you can bring to lender meetings, property showings, inspections, and settlement appointments:

- Closing Cost Calculator Worksheet — Line-by-line fillable worksheet covering state transfer tax (with first-time buyer exemption), county transfer tax, recordation tax, title insurance, settlement attorney fees, prepaid items, MMP DPA credits, and seller concessions

- Home Inspection Checklist — Standard inspection items plus Maryland-specific checks for ground rent status, lead paint (pre-1978 rowhouses), radon, well/septic (rural properties), and Chesapeake Bay Critical Area lot coverage compliance

- MMP/SmartBuy Program Comparison Card — Side-by-side reference for 1st Time Advantage (with DPA tiers), SmartBuy 3.0, HomeStart, Flex products, and qualification requirements including county-specific income limits

- Transfer and Recordation Tax Reference Card — County-by-county rate table for all 24 jurisdictions with the Prince George's mortgage tax flag, Montgomery County tier breakpoints, and Baltimore City exemption thresholds

- Ground Rent Identification Flowchart — Step-by-step SDAT search process, registry check, capitalization rate table (4%/6%/12%), redemption cost calculator, and the unregistered-owner escrow procedure

- Military Stacking Strategy Worksheet — VA + MMP + seller concessions assembly checklist with the specific dollar math for Fort Meade, Andrews, and Aberdeen area purchases

- Chesapeake Bay Critical Area Quick Reference — Zone classifications, lot coverage limits, grandfathered exceptions, tree-clearing permit requirements, and the pre-offer zoning verification checklist

- Settlement Day Preparation Card — Attorney-settlement process overview, cash-to-close verification, Closing Disclosure review checklist, homestead tax credit filing deadline, and the first-time buyer exemption contract-clause verification

Who This Guide Is For

This guide is for first-time home buyers in Maryland who:

- Are buying their first home anywhere in Maryland and need to understand how the state transfer tax, county transfer tax, and recordation tax combine at every county line — before the pre-approval letter becomes a purchase agreement and the closing cost estimate turns out to be $8,000 too low because your lender used a state-average flat rate instead of your county's actual tiered formula

- Carry student loan debt and want to use SmartBuy 3.0's $25,000 student loan payoff — with the full eligibility rules including the 720 credit score minimum, the mandatory full-balance payoff, the 0% interest five-year forgiveness schedule, and the fixed-rate trade-off that matters if you plan to refinance

- Are active duty or veteran at Fort Meade, Joint Base Andrews, or Aberdeen Proving Ground and need the VA + MMP + seller concession stacking strategy — the one national call-center lenders don't offer because the paperwork requires DHCD compliance they're not set up to handle

- Are considering Baltimore City or Baltimore County and need to navigate ground rent — the colonial-era leasehold system where you own the structure but lease the land, out-of-state lenders refuse to underwrite it, VA loans prohibit it, and holding companies demand inflated buyout prices from buyers who don't know the statutory capitalization math

- Are eyeing waterfront property on the Eastern Shore and need to understand the Chesapeake Bay Critical Area Act — specifically the 15% lot coverage limit that blocks the deck expansion, pool, and detached garage you were planning before you committed to the purchase

- Want every Maryland-specific tax, program, ground rent procedure, environmental restriction, and settlement process detail in one reference — instead of piecing it together from DHCD program PDFs, SDAT property searches, county recordation schedules, and Reddit threads from buyers who discovered the Prince George's mortgage tax at the closing table

Why Not Free Tools and Forums?

Free information on buying a home in Maryland exists. Here's what it actually delivers:

- DHCD's website publishes MMP program guidelines, income limits, and lender directories. It doesn't compare the DPA tiers with the refinancing trap (the entire DPA comes due immediately when you refinance), doesn't explain the SmartBuy 720 credit score hurdle or the mandatory full-balance payoff, and doesn't walk through how to stack MMP with county grants without tripping parallel underwriting delays. You get the program specs without the decision framework.

- Zillow and Realtor.com show estimated monthly payments and "closing costs" based on state-average percentages. They don't calculate Montgomery County's tiered recordation tax (which means a $550,000 home pays a blended rate far higher than the 0.89% base tier), don't flag Prince George's mortgage tax on the security instrument, and don't know that the first-time buyer state transfer tax exemption shifts 0.25% from you to the seller. Your estimated closing costs can be off by $5,000 to $12,000.

- Real estate agent blogs mention MMP assistance and SmartBuy. They don't explain the ground rent buyout math, don't disclose the Chesapeake Bay lot coverage limit that kills renovation plans, and don't cover the military stacking strategy because the referral commission is the same whether the buyer uses it or not. The content is designed to generate leads, not to prevent closing-table surprises.

- Reddit threads (r/maryland, r/baltimore) contain genuine buyer experiences — people sharing ground rent confusion, SmartBuy success stories, and transfer tax shock. But advice from 2023 doesn't reflect current MMP income limits, updated county recordation rates, or the latest SmartBuy eligibility rules. And the guidance from a lifelong Baltimore local who calls ground rent "just a $14 bill" doesn't help the out-of-state buyer whose VA lender is threatening to kill the deal over it.

This guide fills the Maryland-specific gap — the space between knowing how to buy a house in general and knowing how to buy one in a state where closing costs change at every county line, where a colonial-era land lease can derail your financing, where a student loan payoff program requires a 720 credit score and full balance elimination, where your agent's failure to check one box on the contract costs you thousands in transfer taxes, and where an environmental regulation written in 1984 determines whether you can build a deck on your waterfront property. It's the analysis that would take a Maryland settlement attorney, a DHCD-approved loan officer, and a Baltimore title specialist to assemble — structured as a reference you own permanently.

— Less Than One Transfer Tax Surprise

A single miscalculated county transfer tax on a $400,000 home in Prince George's County — where the 1.4% tax hits both the deed and the mortgage — runs over $11,000. Choosing the wrong DPA tier costs thousands in deferred-loan liability you didn't plan for. A ground rent holding company that demands $6,000 when the statutory buyout is $1,000 pockets $5,000 from a buyer who doesn't know the math. Missing the first-time buyer transfer tax exemption checkbox on the purchase contract shifts 0.25% of the sale price — $1,000 on a $400,000 home — from the seller back to you, with no recourse after ratification.

This guide doesn't replace your settlement attorney or your lender. But it gives you the county-by-county transfer and recordation tax tables, the SmartBuy eligibility flowchart, the ground rent identification and buyout procedure, the military stacking strategy worksheet, the Chesapeake Bay lot coverage verification checklist, and the first-time buyer exemption contract-clause check that ensure you identify every Maryland-specific financial risk before your earnest money is committed — instead of discovering them on the Closing Disclosure, at the settlement table, or in your first ground rent demand letter.

If it catches a single transfer tax miscalculation, prevents a single ground rent extortion, or saves you from missing the first-time buyer exemption on your contract, it pays for itself before you've finished reading it.

30-day money-back guarantee. If the guide doesn't sharpen your decision-making and protect your investment in Maryland's unique closing cost and regulatory landscape, you pay nothing.

Download the free Maryland Quick-Start Home Buying Checklist to see the 20-item action plan covering financial preparation, program applications, location selection, offer strategy, and settlement preparation. When you're ready for the full county-by-county tax navigator, SmartBuy decision framework, ground rent buyout guide, and military stacking strategy, the complete guide is here.

The house looks perfect on Zillow. This guide tells you whether Maryland's tax code agrees.