You Lost the Bidding War. Then You Lost Your Deposit. Then You Found Out the Septic Would Have Cost You $38,000 Anyway.

You got pre-approved and found a single-family home in a town west of Boston. Your agent told you to "go in strong" — waive the home inspection, escalate $50K over asking, and put up a $30,000 deposit with no contingencies. You did it because the last three offers you submitted lost to cash buyers who offered faster closes. This time, you won.

Then your attorney reviewed the Purchase and Sale agreement and flagged the Title V septic inspection. The seller had an older system. The inspection came back failed. Suddenly you were looking at a $38,000 engineered septic replacement — and you had already released your contingencies during the Offer to Purchase phase because your agent said "that's how you win in Massachusetts." The seller refused to credit you. Your lender would not fund without a passing Title V or escrow holdback. You were trapped between losing your $30,000 deposit or absorbing a five-figure liability nobody mentioned before you signed.

Or maybe you did everything right. Got a home inspection. Passed Title V. Closed on a beautiful 1920s Colonial in Somerville. Six months later, your child turned six, and you received a letter from the city: under Massachusetts Lead Paint Law, you had strict liability for any lead hazard in a home occupied by a child under six. The deleading estimate came in at $22,000. The law does not care that you bought the home in good faith. The law does not care that your inspector mentioned "lead paint likely present" without explaining the legal consequence. Ninety days to comply — or face fines up to $10,000 per violation and personal injury liability with no cap.

The problem is not that Massachusetts is expensive. The problem is that Massachusetts runs a two-step contract system where you can lose your deposit between the OTP and the P&S, requires an attorney at closing, layers Title V septic liability that ranges from $15,000 to $45,000, imposes strict liability lead paint obligations on any home with a child under six, adds a 2% Land Bank surcharge in Barnstable County that buyers pay on top of the purchase price, and offers down payment assistance up to $50,000 in Gateway Cities through MassHousing — and no single resource maps all of these into a decision framework you can work through before you sign.

The Massachusetts First-Time Home Buyer Guide is an Attorney State Closing Playbook — a structured walkthrough of every Massachusetts-specific contract trap, liability exposure, tax benefit, and assistance program that determines whether your purchase protects you or bankrupts you. It replaces months of cross-referencing DHCD program portals, MassHousing eligibility calculators, town assessor websites, Title V regulations, and r/bostonhousing threads with a single reference that tells you exactly what to verify, exactly when your deposit is at risk, and exactly where Massachusetts transactions destroy first-time buyers who assumed their agent and lender would catch everything.

What's Inside the Attorney State Closing Playbook

A comprehensive guide, a quick-start checklist, and 8 standalone worksheets and reference cards — 10 printable PDFs covering every stage from pre-approval through post-purchase setup, built specifically for the legal structures, liability exposures, and assistance programs that make Massachusetts unlike any other state:

The Two-Step Contract System Decoded

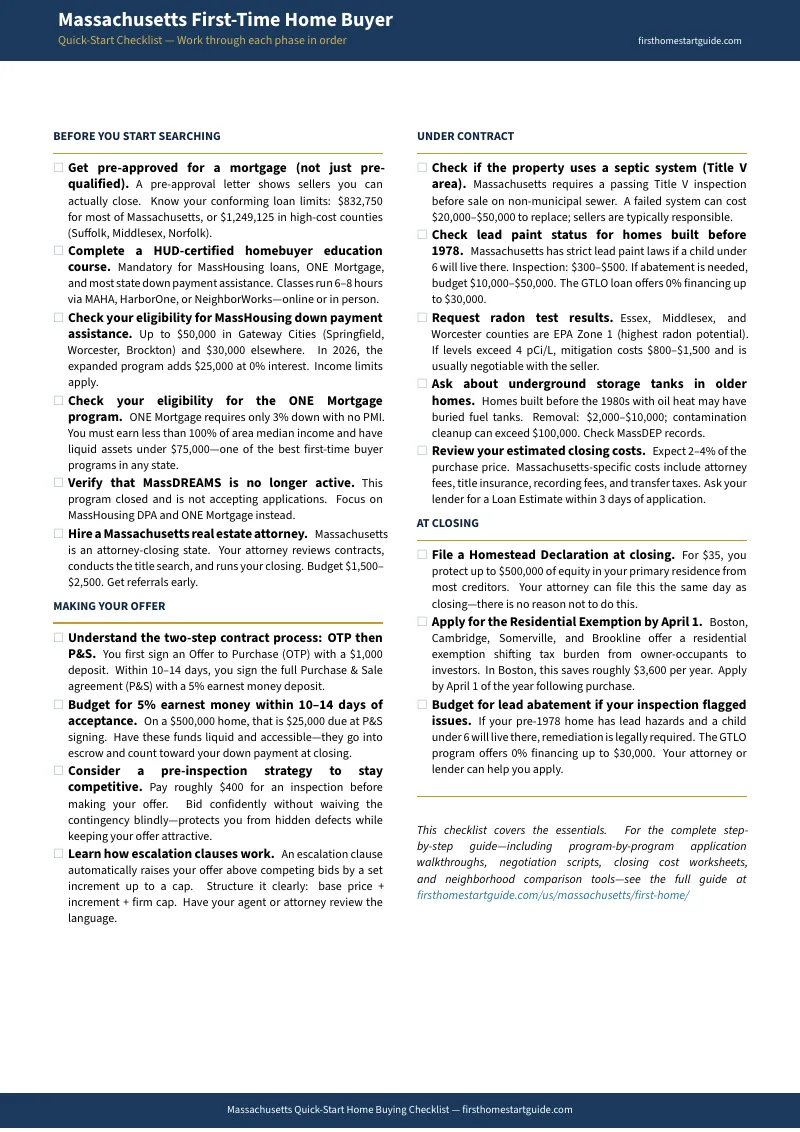

Massachusetts is one of the few states where you sign two separate contracts: the Offer to Purchase (OTP) and the Purchase and Sale Agreement (P&S). The OTP is a binding contract with a deposit — typically $1,000 to $5,000 — that becomes at risk the moment the seller countersigns. The P&S follows 7 to 14 days later with a much larger deposit, typically 5% of the purchase price. The guide walks you through exactly what protections to include in the OTP, how the Buyer's Rider works and which contingencies you should never waive even in a competitive market, the deposit risk window between OTP and P&S signing, what happens to your money if you walk during each phase, how escalation clauses work and when they help versus when they expose you, and pre-inspection strategies that let you compete without waiving your right to know what you are buying. If you have never navigated an attorney-closing state, this section alone prevents the most common five-figure mistake Massachusetts buyers make.

Title V Septic: The $15K-$45K Liability Nobody Mentions During Showings

Massachusetts requires a passing Title V septic inspection for any property transfer where the home is not connected to municipal sewer. A failed Title V means the system must be upgraded or replaced before transfer — or the buyer must accept the liability with an escrow holdback. Replacement costs range from $15,000 for a straightforward gravity system to $45,000 or more for an engineered system on a tight lot with ledge or high groundwater. The guide covers how to identify Title V properties before you fall in love with them (town sewer maps), what a conditional pass versus a full pass means for your liability, how to negotiate Title V cost allocation with the seller, the escrow holdback option and when it protects you versus when it traps you, and how to evaluate the remaining useful life of a system that passed today but may fail in five years. In towns west and south of Boston, on the Cape, and in the Pioneer Valley, this is not an edge case — it is the majority of listings.

Lead Paint Strict Liability: The 90-Day Clock

Massachusetts Chapter 111, Section 197 imposes strict liability on property owners for lead paint hazards in homes occupied by children under six. This means you are liable regardless of whether you knew about the lead, regardless of whether the previous owner disclosed it, and regardless of whether the child has actually been harmed. The deleading compliance window is 90 days from the date a child under six occupies the property. Deleading costs range from $10,000 to $50,000 depending on the scope. The guide explains which homes are at highest risk (pre-1978 construction), what interim controls versus full abatement means, how to get a lead inspection before you make an offer, the $3,000 tax credit for deleading expenses and how to claim it, and how to evaluate whether a home's lead status is a manageable cost or a deal-breaker — before you are 90 days into a liability you cannot negotiate away.

MassHousing DPA and ONE Mortgage: Up to $50K in Gateway Cities

MassHousing offers down payment assistance of up to $50,000 in designated Gateway Cities — places like Springfield, Worcester, Lawrence, New Bedford, and Brockton where the state is actively incentivising homeownership. Even outside Gateway Cities, MassHousing DPA provides $30,000 to $50,000 depending on location and income. The ONE Mortgage program offers 3% down with no PMI and a fixed rate — a structure that saves most buyers $150 to $250 per month compared to a conventional loan with PMI. The guide covers MassHousing DPA eligibility by income and geography, the full ONE Mortgage qualification criteria, how to compare MassHousing versus ONE Mortgage versus FHA versus conventional for your specific income and purchase price, the MassDREAMS program (currently depleted — the guide tells you this so you stop wasting time), and worked dollar comparisons showing which combination gives you the lowest total cost of ownership over 5 and 10 years.

The Residential Exemption: $3,600-$4,578 Per Year Most Buyers Never Claim

Thirty-one Massachusetts municipalities offer a Residential Exemption that shifts a portion of the property tax burden from owner-occupied homes to commercial properties and non-owner-occupied units. In Boston, the 2025 residential exemption saves qualifying homeowners approximately $4,578 per year. In Somerville, Cambridge, Brookline, and other cities, the savings range from $1,800 to $3,600 annually. But you must apply by April 1 of the fiscal year — and the exemption is not automatic. The guide identifies every municipality that offers the residential exemption, the application deadlines and documentation requirements, how to calculate your actual tax savings before you compare towns, and how the exemption interacts with the statewide Clause 41A/41C senior and veteran exemptions. This is free money that requires a single filing — and most first-time buyers either do not know it exists or miss the deadline.

Cape Cod and Islands: The 2% Land Bank Surcharge

If you are buying in Barnstable County (Cape Cod), Nantucket, or Martha's Vineyard, the buyer pays a 2% Community Preservation Act / Land Bank surcharge on top of the purchase price at closing. On a $600,000 home, that is $12,000 in additional closing costs that does not appear on any standard closing cost calculator and is not included in your lender's initial estimates. The guide breaks down exactly where the surcharge applies, how it interacts with the CPA surcharge on your annual property tax, and how to budget for it so it does not blindside you at the closing table.

Attorney-Closing Transaction Timeline

Massachusetts is an attorney-closing state. You will hire a real estate attorney — typically at $1,500 to $2,500 — who reviews and negotiates the P&S, conducts the title search, handles the closing, and records the deed. There is no title company running the transaction as in escrow states. The guide walks through the complete timeline: pre-approval, OTP negotiation and signing, the 7-to-14-day gap before P&S, attorney review and Buyer's Rider negotiation, home inspection (and pre-inspection strategy), Title V and lead inspection, mortgage commitment deadline, final walkthrough, and closing at your attorney's office. It includes Massachusetts-specific inspections: radon testing (required disclosure in some towns), pest/termite inspection, chimney inspection for wood-burning homes, and underground oil tank searches for homes built before 1970.

Regional Market Context

Five distinct Massachusetts markets with current pricing, competition dynamics, and financing strategies: Greater Boston (extreme competition, escalation clauses standard, pre-inspection culture, highest residential exemption savings), MetroWest suburbs (commuter rail access premium, Title V prevalence, school district pricing), South Shore to Cape Cod (seasonal market timing, Land Bank surcharge, vacation property vs primary residence financing), Worcester and Central Mass (Gateway City DPA access, emerging market with less competition), and Western Mass/Pioneer Valley (most affordable in-state option, USDA eligibility in many towns, Title V prevalence in rural areas).

Who This Guide Is For

- Renters in Greater Boston losing bidding wars who need a competitive offer strategy — escalation clauses, pre-inspections, and Buyer's Rider protections — that lets them compete without waiving the contingencies that protect their deposit and their financial future

- Out-of-state buyers relocating for biotech, healthcare, or higher education jobs who have never navigated an attorney-closing state, do not understand the two-step OTP/P&S contract, and assume their experience buying in a title company state (California, Texas, Florida) translates to Massachusetts — it does not

- Young families buying pre-1978 homes who do not realise that strict liability lead paint law activates the moment a child under six occupies the property, and who need to understand deleading costs, compliance timelines, and tax credits before they close — not after

- Gateway City buyers in Springfield, Worcester, Lawrence, or New Bedford who qualify for up to $50,000 in MassHousing DPA and ONE Mortgage's 3% down with no PMI but do not know how to compare these against FHA or conventional options for their specific income

- Cape Cod and Islands buyers who need to budget for the 2% Land Bank surcharge, seasonal market timing, Title V prevalence in waterfront towns, and the difference between primary residence and vacation property financing

- First-time condo buyers in Boston, Cambridge, or Somerville who want to understand the residential exemption (up to $4,578/year in Boston), condominium document review, special assessment risk, and how Massachusetts condo transactions differ from single-family purchases

Why Not Free Tools and Forums?

Free information on buying a home in Massachusetts exists. Here is what it actually delivers:

- MassHousing.com and DHCD portals give you income limit tables, program descriptions, and approved lender lists. They do not tell you whether ONE Mortgage or MassHousing DPA gives you the better 10-year outcome at your income level, whether you can combine programs, or that MassDREAMS is depleted and you should stop looking for it. You get eligibility inputs scattered across four state agency websites without a decision framework.

- Reddit threads (r/bostonhousing, r/FirstTimeHomeBuyer, r/RealEstate) contain genuine warnings about escalation clauses gone wrong and Title V horror stories, but mixed with advice from buyers who confuse the OTP with the P&S, do not understand when their deposit is actually at risk, and recommend waiving inspections without explaining the legal consequence in an attorney-closing state. Sorting current strategy from outdated anecdote takes longer than reading a guide that already did it.

- National home buying guides (NerdWallet, Bankrate, Rocket Mortgage) assume you are buying in an escrow state with a title company running the transaction. They do not cover the two-step contract, attorney-closing mechanics, Title V septic liability, lead paint strict liability, the residential exemption, or the Land Bank surcharge. You get generic advice that misses every Massachusetts-specific trap and opportunity.

- Real estate agent blogs and buyer seminar PDFs focus on "6 steps to buying your first home in Massachusetts" content designed to capture leads and book consultations. They do not explain how to structure a Buyer's Rider, calculate your Title V exposure before making an offer, evaluate lead paint liability against your family plans, or model the residential exemption savings into your town-comparison spreadsheet. You get marketing content, not analytical tools.

This guide fills the Massachusetts-specific gap — the space between knowing how to buy a home in general and knowing how to buy one in an attorney-closing state where a two-step contract puts your deposit at risk before the P&S even exists, Title V can add $45,000 to your purchase cost, lead paint law creates strict liability for families with young children, and assistance programs worth up to $50,000 are scattered across agencies that do not cross-reference each other. It is the analysis that would take a Massachusetts real estate attorney, a MassHousing-approved lender, a Title V inspector, and a lead paint consultant to assemble — structured as a reference you own permanently.

— Less Than One Hour of Attorney Time

A real estate attorney in Massachusetts charges $1,500 to $2,500 for a standard residential closing. A Title V septic failure you did not budget for costs $15,000 to $45,000. Lead paint deleading you did not know was your legal obligation costs $10,000 to $50,000. Missing the residential exemption deadline costs you $3,600 to $4,578 every single year. Not knowing about MassHousing DPA in your Gateway City means leaving up to $50,000 in assistance on the table. Waiving your inspection contingency in the OTP without understanding when your deposit becomes non-refundable can cost you $30,000 or more in a single afternoon.

This guide does not replace your real estate attorney, your lender, or your home inspector. But it gives you the contract analysis, liability assessment, tax benefit identification, and transaction walkthrough that ensure you identify every Massachusetts-specific risk and opportunity before your deposit is at stake — instead of discovering them at the P&S signing, the Title V inspection, or your first property tax bill in a town that offers an exemption you never applied for.

If it catches a single Title V liability before you waive your contingency, prevents a single lead paint compliance surprise, connects you with a single DPA program worth $30,000-$50,000, or reminds you to file the residential exemption before April 1, it pays for itself before you have finished reading it.

30-day money-back guarantee. If the guide does not sharpen your Massachusetts home buying analysis and protect your deposit, you pay nothing.

Download the free Massachusetts Quick-Start Home Buying Checklist to see the step-by-step framework covering financial preparation, contract navigation, program eligibility, property due diligence, offer and close, and post-purchase essentials. When you are ready for the full Title V evaluation worksheet, lead paint liability checklist, DPA comparison card, residential exemption guide, closing cost worksheet, and the complete guide with market-by-market analysis, the full 10-PDF toolkit is here.

Massachusetts rewards buyers who understand the attorney-closing system. This guide makes sure you do.