You Found the House. But the Tax on Zillow Is the Previous Owner's Capped Rate, and After Transfer, Proposal A Uncaps It to Market Value --- Adding $200 to $400 Per Month to Your Escrow.

You found a three-bedroom in Royal Oak listed at $285,000. Or a starter home in Grand Rapids where the listing says "taxes: $2,400/year" and the payment calculator shows $1,800/month all-in. Or a MSHDA-eligible property in a Targeted zip code where you qualify for $10,000 at zero percent interest. You got pre-approved. You ran the numbers. You're ready to make an offer.

Then Michigan happens. The $2,400 annual tax bill on the listing is the seller's rate --- capped under Proposal A for 15 years while their taxable value stayed frozen. After transfer, the assessor uncaps the property to its current State Equalized Value, and your first full-year tax bill lands at $5,100. Your lender set up escrow based on the seller's capped rate, so six months in, you receive an escrow shortage notice demanding $2,700 immediately or a $225/month payment spike for the next 12 months. In Detroit, a young couple posted about receiving a $20,000 property tax bill after their first transfer. In Grand Rapids, a buyer of a $220,000 home reported a sudden $400/month mortgage increase solely from the uncapping. You applied for MSHDA's $10,000 DPA, but your property is 200 feet outside a Targeted zip code boundary --- Non-Targeted income limits apply, you're $3,000 over, and you lose the entire assistance package two weeks before closing. You didn't file Form 2368 before June 1, so you missed the Principal Residence Exemption and paid 18 extra mills on your summer tax levy --- roughly $2,500 on a $280,000 home that you'll never recover. The well water on the rural property you're considering has never been tested for PFAS, Michigan's statewide "forever chemicals" crisis, and the state has no mandatory testing requirement for private wells. And the land contract the seller offered in the UP carries a monthly payment that annualizes to 78% effective interest, exploiting buyers who don't know about Michigan's 11% usury cap.

Here's what no single free resource explains: Michigan layers a constitutional property tax uncapping mechanism (Proposal A) that routinely generates $2,000 to $5,000 in unexpected annual tax increases on every single property transfer --- against a MSHDA down payment assistance program where eligibility hinges on Targeted vs. Non-Targeted zip code boundaries, county-specific income limits, household size calculations, and dual-layered underwriting with FHA or conventional loans --- against a Principal Residence Exemption that saves 18 mills annually but only if Form 2368 is filed before June 1 --- against a statewide PFAS groundwater contamination crisis where private well owners bear the full $290 testing cost with zero regulatory protection --- against predatory land contract practices in rural areas where a single missed payment triggers total equity forfeiture within 90 days --- against a title-company-only closing system where EMD disputes can freeze your funds for months without attorney intervention --- against post-closing occupancy demands in competitive markets that force you to let sellers remain in your home for 60 days or lose the bid --- against Michigan's heavy clay soil and freeze-thaw cycles that produce foundation failures costing $10,000 to $50,000 to remediate. Each of these has cost real Michigan first-time buyers five figures because the information existed --- scattered across MSHDA program matrices, county assessor databases, EGLE contamination maps, MCL statutes, and Reddit threads --- but nobody had assembled it into a single decision system calibrated to how Michigan actually works.

The Michigan First-Time Home Buyer Guide is a Michigan Tax & Title Protection System --- not a motivational overview of Great Lakes homeownership, but a structured reference that maps every Michigan-specific tax trap, assistance program, environmental hazard, and transaction risk into a process you work through before your earnest money is at risk and your escrow account is underfunded. It replaces months of cross-referencing county assessor uncapping calculations, MSHDA zip code maps, EGLE PFAS databases, MCL land contract statutes, and forum posts with a single guide that tells you exactly what to verify, exactly what the numbers should look like, and exactly where deals go wrong in this state.

What's Inside the Michigan Tax & Title Protection System

A 63-page guide, a quick-start checklist, and 8 standalone printable worksheets --- covering every stage from pre-approval through post-closing tax management, built specifically for the financial structures, environmental hazards, and assistance programs that make Michigan different from every other state:

Proposal A Tax Uncapping Calculator

Michigan's 1994 constitutional amendment caps annual taxable value increases at the lesser of inflation or 5% for existing owners. But upon transfer, the cap is permanently removed and taxable value resets to State Equalized Value (50% of true cash value). The guide provides the exact formula to calculate your post-purchase tax liability using the county assessor's current SEV --- not the seller's artificially suppressed capped value displayed on Zillow. You'll learn how to pull the three critical numbers (True Cash Value, SEV, and current Taxable Value) from your county's BS&A database, calculate the gap between capped and uncapped values, determine whether your lender is escrowing based on the seller's rate or your actual post-transfer obligation, and model the escrow adjustment you'll face 6-12 months after closing. If you're buying in Oakland, Wayne, Kent, or Washtenaw County, this chapter prevents the single most common financial shock Michigan buyers experience.

MSHDA Down Payment Assistance Decision Framework

MSHDA's MI Home Loan provides up to $10,000 at 0% interest with no monthly payments --- due only upon sale, refinance, or payoff. But qualifying requires navigating a matrix of Targeted vs. Non-Targeted zip codes (which determine whether you need to be a first-time buyer and which income limits apply), county-specific income caps ranging from $91,200 to $174,720 depending on household size and area designation, a 640 minimum credit score, mandatory homebuyer education, and dual-layered underwriting where your application must satisfy both MSHDA requirements and FHA or conventional loan standards simultaneously. The guide maps every eligibility variable, explains the Targeted Area waiver that lets repeat buyers qualify, identifies which participating lenders actually process MSHDA loans efficiently, and walks you through the timing sequence so your education certificate, income documentation, and property location all align before you're under contract.

Principal Residence Exemption Timeline

Filing Form 2368 with your local assessor exempts your primary residence from up to 18 mills of school operating taxes. On a $280,000 home with a $140,000 SEV, that's approximately $2,520 per year. But the filing deadline is strictly enforced: file before June 1 and you receive the exemption on both summer and winter levies. File after June 1 but before November 1, and you only get the winter levy exemption. Miss both deadlines and you pay the full non-homestead rate for an entire year. The guide provides the exact filing timeline, the form itself explained line by line, and the calculation showing exactly how many dollars you lose by filing late --- so this never becomes a forgotten administrative task that costs you thousands.

PFAS Contamination Testing Protocol

Michigan has more identified PFAS contamination sites than any other state. Municipal water systems are tested and regulated. Private wells are not. If you're buying a property on well water --- common in rural Michigan, the UP, and exurban areas around metro Detroit --- the state provides zero mandatory disclosure or testing requirements. The EGLE PFAS Action Response Team maintains contamination maps, but most residential wells have never been sampled. The guide covers how to check MPART's interactive map for known Areas of Interest near your target property, how to order the EPA Method 537.1 test kit ($290 through EGLE's laboratory), what results require immediate action vs. monitoring, how to negotiate seller-funded testing during the inspection contingency, and what remediation systems cost ($1,500-$4,000 for point-of-entry treatment) if results exceed Michigan's 8 ppt advisory level for PFOS/PFOA.

Foundation and Waterproofing Inspection Guide

Michigan's combination of heavy clay soil, a high water table in many metro areas, and severe freeze-thaw cycles creates foundation conditions unlike coastal or southern states. Horizontal cracks in poured concrete or block walls signal lateral soil pressure failure --- not cosmetic settling --- and repairs run $10,000 to $50,000 depending on severity. Basement waterproofing (interior drain tile, sump pump, exterior membrane) is a $5,000-$15,000 cost that most buyers don't budget. The guide identifies the specific warning signs unique to Michigan soil conditions, explains when vertical cracks are cosmetic vs. when horizontal cracks indicate structural failure requiring an engineer, what interior vs. exterior waterproofing systems cost, and how to use foundation findings to negotiate repair credits or walk away during your inspection contingency.

Land Contract Risk Assessment

Michigan's land contract market is concentrated in rural areas, the Upper Peninsula, and economically distressed neighborhoods where traditional financing is difficult. Sellers retain the deed until full payoff, and buyers face devastating forfeiture rules: if you've paid less than 50% of the purchase price, the seller can reclaim the property and all your prior payments within 90 days of a single missed payment. The guide covers Michigan's 11% usury cap under MCL 438.31c, how to calculate whether a seller's quoted payment exceeds the legal limit, the critical difference between forfeiture (total loss of equity) and foreclosure (judicial process preserving some rights), the "disguised interest" doctrine that voids contracts with hidden fees, and the specific scenarios where a land contract might make sense vs. when it's a predatory trap. If you're considering any property advertised as "land contract available," this chapter could save your entire investment.

Post-Closing Occupancy Strategy

In Ann Arbor, the Detroit suburbs, and Grand Rapids, sellers routinely demand 30-60 day rent-backs as a condition of accepting your offer. Buyers who refuse lose bidding wars. But post-closing occupancy carries real risks: the seller occupies your property after you own it, pays you 1/30th of PITI daily, and if they refuse to leave, pending Michigan legislation (HB 5384-5386) determines whether you evict them as a tenant (months-long process) or through summary proceedings (weeks). The guide covers the standard occupancy agreement structure, the security deposit holdback from seller proceeds, your insurance obligations during the rent-back period, the 60-day maximum for primary residence loan compliance, and the exact contract language that protects you if the seller holds over.

Title Company Closing Process and EMD Protection

Michigan is a title company state --- attorneys are rarely present at standard residential closings. The title company verifies ownership, issues insurance, and holds escrow. Your Earnest Money Deposit (typically 1-3% of purchase price) is deposited within two banking days under MCL 339.2512. If the deal falls through and the seller disputes your contingency exit, the title company cannot release your EMD without mutual consent. Without that signature, your money is frozen --- potentially for months --- while you pursue mediation or district court interpleader. The guide explains how Michigan's EMD rules differ from attorney states, what contract language protects your deposit, how to structure contingencies that provide clean exit paths, and what to do if a seller refuses to sign the release.

Transfer Taxes and Closing Cost Breakdown

Michigan's bifurcated transfer tax hits at $3.75 per $500 (state) plus $0.55 per $500 (county), totaling $8.60 per $1,000 of sale price. On a $280,000 home, that's $2,408 paid by the seller --- but buyers need to understand how this affects negotiations, especially when sellers demand net proceeds. The guide provides a complete closing cost model including title insurance, recording fees, prepaid taxes and insurance, and the interaction between MSHDA DPA credits and your cash-to-close calculation.

Carrying Cost Worksheet and Timeline

A day-by-day timeline from accepted offer through county recording, with Michigan-specific deadlines mapped: EMD delivery within 48 hours, inspection contingency window (7-10 days), title commitment review, Form 2368 filing deadline, and closing disclosure review 3 days before settlement. Plus a carrying cost worksheet that models every line item: PITI with post-uncapping tax rate, HOA dues, insurance, PFAS remediation amortization, foundation maintenance reserves, and the true monthly cost --- so your budget reflects what you'll actually pay in Michigan, not what the listing showed.

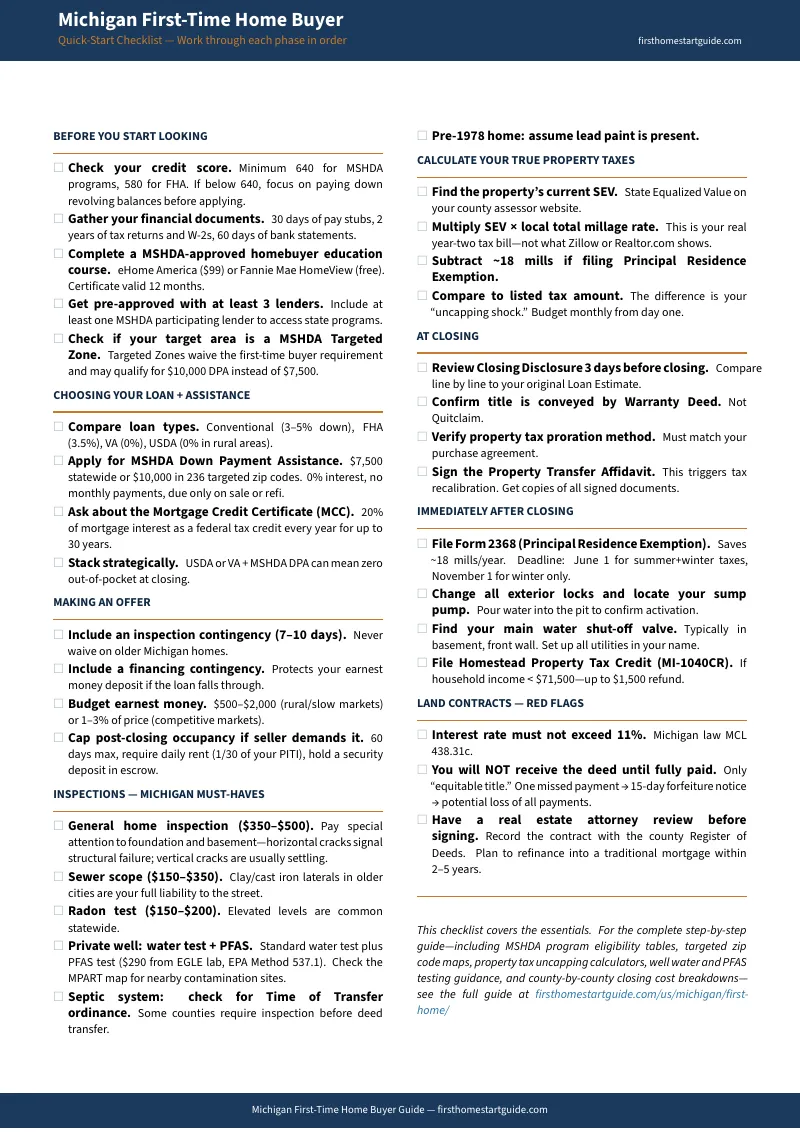

Standalone Printable Worksheets Included

In addition to the full guide, your purchase includes 8 standalone worksheets designed to print and bring to lender meetings, property viewings, inspections, and closing:

- Tax Uncapping Worksheet --- Fillable Proposal A calculator. Look up SEV on BS&A Online, calculate your real post-transfer tax bill and escrow gap for up to three properties.

- MSHDA Eligibility Self-Assessment --- Step-by-step worksheet for MI Home Loan Standard vs. Flex, $7,500 vs. $10,000 DPA, Targeted zone verification, income limits, and MCC eligibility.

- Closing Cost Worksheet --- Every Michigan-specific line item, transfer tax formula, property tax proration (summer vs. winter, advance vs. arrears), and cash reserve planning.

- Carrying Cost Worksheet --- True monthly ownership cost projection using your post-uncapping tax rate, with DTI affordability check and Year 2 budget adjustment.

- PFAS Testing Checklist --- MPART map check, EGLE lab ordering, sampling protocol, results interpretation at Michigan's 8 ppt advisory level, and county Time of Transfer requirements.

- Inspection Reference Card --- Crack severity guide for Michigan clay soil (cosmetic vs. structural), waterproofing system comparison, and negotiation quick reference.

- Land Contract Red Flags --- Interest rate calculator, 11% usury cap verification, forfeiture timeline, and red-flag checklist before signing any seller-financed deal.

- Transaction Timeline --- Day-by-day from accepted offer through closing and your first 30 days, with critical Michigan deadlines and Year 1 financial calendar.

Who This Guide Is For

This guide is for first-time home buyers in Michigan who:

- Are buying their first home in the Detroit metro (Wayne, Oakland, Macomb Counties) and need to understand how Proposal A uncapping will increase their property tax bill after transfer --- not the capped rate shown on the listing, but the actual post-purchase obligation their lender should be escrowing for from day one

- Are house-hunting in Grand Rapids, Kalamazoo, or Lansing and want to claim MSHDA's $10,000 DPA but need to navigate the Targeted vs. Non-Targeted zip code map, county income limits, household size calculations, and the dual-underwriting process with FHA or conventional loans without losing the assistance package to a technicality

- Are considering rural or UP properties where land contracts are offered and need to understand Michigan's 11% usury cap, forfeiture vs. foreclosure consequences, and the equity forfeiture timeline before signing a seller-financed agreement that could cost them everything on a single missed payment

- Are relocating from out of state and expect an attorney at closing --- but Michigan uses title companies, and they need to understand how EMD disputes work, what happens when a seller refuses to sign a release, and how to structure contingencies that provide clean exit protection without legal representation at the table

- Are MSHDA-eligible buyers earning under the income threshold who need the exact sequence: homebuyer education completion, participating lender selection, Targeted Area verification, and FHA/conventional overlay requirements --- timed correctly so nothing disqualifies them mid-transaction

- Are bidding in competitive markets (Ann Arbor, Birmingham, Royal Oak, East Grand Rapids) where sellers demand post-closing occupancy and buyers who refuse lose --- and need to understand the rent-back structure, insurance requirements, 60-day loan compliance limit, and holdover eviction process before they agree to let a seller stay in their new home

Why Not Free Resources?

Free information on buying a home in Michigan exists. Here's what it actually delivers:

- MSHDA's website publishes income limit tables, purchase price caps, and participating lender lists. It doesn't explain how to determine whether a specific property falls in a Targeted or Non-Targeted zone without cross-referencing census tract data, doesn't show how household size interacts with county-specific income limits to create scenarios where a married couple qualifies but the same couple with one child doesn't, and doesn't walk you through the dual-underwriting timeline where MSHDA approval and FHA approval must converge. You get raw eligibility data without the decision framework that prevents disqualification.

- Zillow and Realtor.com display "tax history" showing the seller's annual bill --- which reflects their capped Proposal A taxable value, not yours. A listing showing $2,400/year in taxes on a home with $140,000 SEV doesn't mean you'll pay $2,400. If the seller's capped taxable value was $85,000, your post-transfer bill will jump to $4,200 or more. No listing platform calculates the uncapping gap or warns you that your escrow will be underfunded.

- NerdWallet and Bankrate Michigan guides list MSHDA as "a program that offers down payment assistance" in a single paragraph, mention that Michigan has "above-average property taxes," and link to generic first-time buyer tips. They don't explain Proposal A mechanics, don't cover the PRE filing deadline, don't mention PFAS, don't address land contract forfeiture law, and provide zero Michigan-specific transaction guidance. The content is written for national SEO, not for someone who needs to calculate their actual post-transfer tax bill in Oakland County.

- Reddit threads (r/Detroit, r/grandrapids, r/RealEstate) contain devastating real-time buyer stories --- the $20,000 tax bill, the $400/month escrow spike, the MSHDA disqualification at closing, the land contract forfeiture. These are genuine data points. But they're scattered across years of posts, reflect outdated MSHDA income limits and rate structures, and offer no systematic framework for preventing the same outcomes. Reading them creates anxiety without providing a solution.

This guide fills the Michigan-specific gap --- the space between knowing how to buy a house in general and knowing how to buy one in a state where every property transfer triggers a constitutional tax uncapping that routinely doubles the displayed tax bill, where $10,000 in free assistance depends on zip code boundaries and household size calculations that change annually, where private well water may contain PFAS at concentrations the state hasn't tested, where land contracts can forfeit your entire investment in 90 days on a single missed payment, where no attorney sits at your closing table to catch title issues in real time, and where competitive markets demand you let the seller live in your home after you own it or lose the bid. It's the analysis that would take a Michigan real estate attorney, a MSHDA-approved lender, an environmental consultant, and a title insurance agent to assemble --- structured as a reference you own permanently.

--- Less Than One Escrow Shortage Payment

A single Proposal A uncapping on a $280,000 Michigan home generates $2,000-$3,000 in unexpected additional annual taxes. The PFAS test kit from EGLE costs $290. Foundation repair on Michigan's clay soil runs $10,000-$50,000. Missing the PRE filing deadline costs $2,500 in the first year alone. Choosing the wrong MSHDA pathway --- or discovering your zip code is Non-Targeted after you've made an offer --- loses you $10,000 in zero-interest assistance.

This guide doesn't replace your real estate agent or your lender. But it gives you the tax uncapping calculator, MSHDA decision framework, PRE filing protocol, PFAS testing checklist, foundation inspection guide, land contract risk assessment, and post-closing occupancy strategy that ensure you identify every Michigan-specific cost before your earnest money is at risk --- instead of discovering them on your first escrow shortage notice, your first contamination test result, or your first post-transfer tax bill.

If it catches a single uncapping gap your lender didn't escrow for, prevents a single MSHDA disqualification, or saves you from signing a land contract with disguised interest above 11%, it pays for itself before you've finished reading it.

30-day money-back guarantee. If the guide doesn't sharpen your decision-making and protect your budget in Michigan's complex, uncapping-driven housing market, you pay nothing.

Download the free Michigan Quick-Start Home Buying Checklist to see the step-by-step action plan covering pre-approval, MSHDA eligibility, house hunting, inspections, and post-closing tax management. When you're ready for the full tax uncapping calculator, MSHDA decision framework, PFAS protocol, land contract risk assessment, and carrying cost worksheet, the complete guide is here.

The listing says $2,400 in taxes. This guide tells you what you'll actually pay after Proposal A uncaps.