You Heard Mississippi Has the Cheapest Homes in America and Assumed the Hard Part Was Over

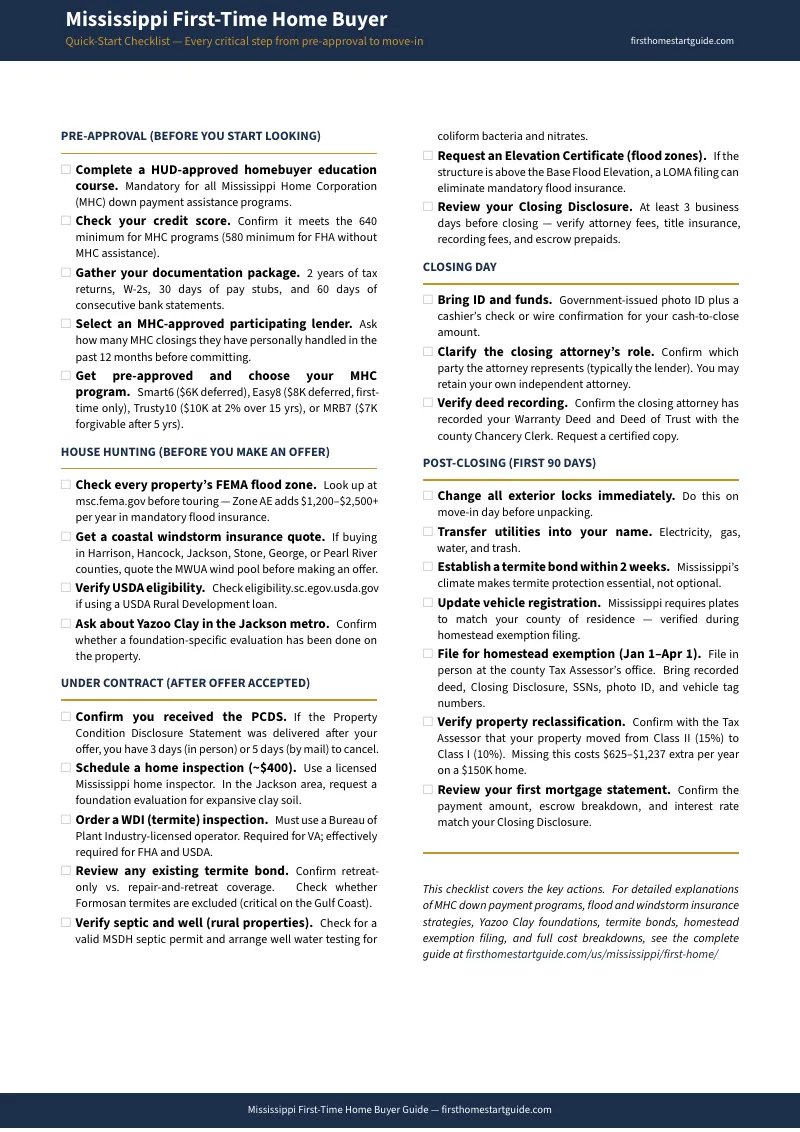

You found a three-bedroom brick ranch in Rankin County for $165,000. Your lender quoted a 6.5% rate on an FHA loan with 3.5% down. The monthly payment looked manageable. Then you called the Mississippi Home Corporation about down payment assistance and discovered six different programs with different repayment rules --- Smart6 gives you $6,000 as a silent second mortgage, Easy8 gives you $8,000 but triggers a federal tax recapture penalty if you sell within 10 years, Trusty10 gives you $10,000 but adds $64 per month to your payment, and MRB7 gives you $7,000 that is forgiven after 10 years but only through specific lenders. You asked your loan officer which one was best for your situation. They said "we usually do Smart6" and moved on.

Then your lender's closing estimate showed a $950 line item for a "closing attorney." You called your realtor. They suggested skipping the attorney and using a title company instead. What they did not tell you is that Mississippi law defines real estate closings as the practice of law --- an attorney must draft your Warranty Deed, your Deed of Trust, and certify a 50-year title search. There is no legal way to close without one.

And nobody mentioned what happens after closing. If you fail to file your homestead exemption by April 1 at the county Tax Assessor's office --- with your recorded deed, your Social Security number, your photo ID, and the tag numbers for every vehicle in your household --- your property stays classified as a rental at a 15% assessment ratio instead of the 10% owner-occupied rate. On a $150,000 home, that mistake costs you $625 to $925 every single year. And the filing window does not reopen until the following January.

The problem is not that Mississippi is expensive. The problem is that Mississippi layers mandatory attorney closings, a uniquely complex property tax reclassification system, six overlapping down payment assistance programs with hidden repayment triggers, statewide termite inspection mandates, coastal windstorm insurance exclusions, and FEMA flood zones covering vast stretches of the state --- and no single resource explains how these interact or what each one costs you when you get it wrong.

The Mississippi First-Time Home Buyer Guide is a Mississippi Buyer Protection System --- a structured walkthrough of every Mississippi-specific financial trap, environmental hazard, legal requirement, and assistance program that determines whether your purchase protects your money or silently drains it. It replaces months of cross-referencing the MHC website, the Department of Revenue's homestead FAQ, FEMA flood maps, the Mississippi Bureau of Plant Industry's termite rules, and Reddit threads about Smart6 versus Easy8 with a single reference that tells you exactly what to verify, exactly what the numbers should look like, and exactly where Mississippi transactions go wrong.

What's Inside the Mississippi Buyer Protection System

A comprehensive 17-chapter guide, a quick-start checklist, and 6 standalone worksheets --- 8 printable PDFs covering every stage from financial preparation through post-closing compliance, built specifically for the regulatory structures and environmental risks that make Mississippi different from every other state:

MHC Down Payment Assistance Decision Framework

Mississippi Home Corporation offers six programs with wildly different terms, and choosing the wrong one can cost you thousands. The guide breaks down Smart6 ($6,000 silent second at 0%, repaid on sale or refi), Easy8 ($8,000 but restricted to first-time buyers with a federal tax recapture penalty under 10 years), Trusty10 ($10,000 at 2% interest adding $64/month to your debt ratio), MRB7 ($7,000 forgivable after 10 years through approved lenders only), HAT (up to $6,000 fully forgiven for teachers in critical-shortage districts), and the DPA14 regional grant for Tunica and Washington counties. You get the eligibility thresholds, the repayment triggers, and the total cost comparison so you can see which program yields the best financial outcome for your income level and timeline --- not just which one your loan officer happens to be familiar with.

Attorney-Led Closing Process Decoded

Mississippi is one of the few states where closings are legally defined as the practice of law. The guide explains the mandatory role of the closing attorney (deed drafting, 50-year title certification, Deed of Trust preparation), typical flat-fee ranges ($750 to $1,250), what the attorney legally owes you versus the lender, and how to evaluate attorney fees on your Loan Estimate so you are not paying $343 per hour for work that should be a flat fee. You will know exactly what your closing attorney is supposed to do --- and what to push back on if they are not doing it.

Flood Zone and Insurance Cost Analysis

Standard homeowners insurance in Mississippi excludes flood damage entirely. Under FEMA's Risk Rating 2.0 methodology, average Mississippi flood premiums have risen 149% to a risk-based average of $2,137 per year. The guide covers how to check any property's flood zone before making an offer, what Zone X ($400 to $800/year, optional but recommended), Zone AE ($1,200 to $2,500+/year, mandatory with a federal mortgage), and Zone VE ($2,000 to $5,000+/year, coastal storm surge) actually cost in monthly carrying charges, how a late-discovered flood zone can blow up your DTI ratio and kill your loan days before closing, and the Elevation Certificate and LOMA process that can legally remove mandatory insurance requirements. You will know your real insurance costs before you write an offer, not after underwriting rejects you.

Termite Protection Strategy

Mississippi carries a "very heavy" termite risk rating. WDI inspections are mandatory for VA loans statewide and effectively required for FHA and USDA. But the inspection is only half the story. The guide covers the critical difference between a "retreat-only" bond (the company sprays again but you pay for all structural repairs) and a "repair-and-retreat" bond (the company covers both treatment and damage), the Formosan termite exclusion loophole that national pest companies build into Gulf Coast contracts, how Formosan colonies build moisture-retaining nests inside wall cavities that standard soil-line inspections miss, and what to verify in any existing termite bond before accepting a transfer at closing.

Property Tax Reclassification and Homestead Exemption

Mississippi taxes owner-occupied homes at 10% of true market value (Class I) and everything else at 15% (Class II). When you buy a home, it is almost certainly classified as Class II on the tax rolls. If you do not actively reclassify it and file for the homestead exemption by April 1, you pay 50% more in assessed value for the entire year --- and the filing window does not reopen until January. The guide walks you through the exact documentation you need (including the vehicle tag number requirement that catches nearly everyone off guard), the regular homestead credit ($300 for standard filers), the special exemption for homeowners 65+ or disabled, the complete veteran exemption, and the mathematical proof of what each classification costs on your specific home value.

Coastal Wind Insurance and the MWUA

In six Gulf Coast counties, private insurers exclude windstorm and hail coverage from standard policies or impose 2% to 5% deductibles. A 5% deductible on a $250,000 home means $12,500 out of pocket before a single claim dollar. Coastal buyers must purchase a separate windstorm policy through the Mississippi Windstorm Underwriting Association (MWUA), creating a "triple-premium" carrying cost (standard hazard + MWUA wind + NFIP flood) that can add $400 to $600 per month to your housing costs. The guide shows you exactly how to budget for these premiums before making a coastal offer.

Regional Market Comparison

What $150,000 buys varies dramatically across Mississippi. The guide covers the Jackson metro (older brick ranches, clay soil foundation risks, high ad valorem millage), the Gulf Coast (extreme insurance costs, military buyer concentration near Keesler AFB, Formosan termite pressure), and Tupelo/North Mississippi (stable manufacturing economy, tornado alley exposure, river basin flooding). You get the risk factors, the economic drivers, and the financing strategies that work in each region.

Complete Transaction Timeline

The full 30-to-45-day closing process mapped from pre-approval through post-closing compliance: MHC lender selection, property disclosure requirements (including Mississippi's 3-day and 5-day cancellation windows), inspection contingencies, the attorney-led closing procedure, deed recording at the Chancery Clerk's office, and the rigid post-closing homestead filing calendar. Every deadline is specific to Mississippi law.

Standalone Printable Worksheets

Six standalone worksheets you can print and bring to meetings, fill in at your desk, or post on the fridge:

- Closing Cost Worksheet --- calculate your total cash needed at closing and monthly carrying cost, line by line, with MHC DPA and seller concession offsets

- MHC Program Comparison --- all 6 Mississippi Home Corporation programs side-by-side (Smart6, Easy8, Trusty10, MRB7, HAT, DPA14) with pre-filled eligibility, repayment triggers, and a fillable section for comparing your top two options

- Flood and Insurance Risk Worksheet --- evaluate any property's flood zone, MWUA windstorm exposure, and combined insurance budget before you make an offer

- Termite Bond Checklist --- step-by-step due diligence from pre-offer through post-closing transfer, including the Formosan termite exclusion trap on the Gulf Coast

- Homestead Exemption Filing Checklist --- exact documents, qualification criteria, tax impact math, the April 1 deadline, and the vehicle registration requirement that catches everyone

- Post-Closing Checklist --- time-phased action items for the first 90 days after closing, from changing locks through your first tax bill

Who This Guide Is For

- First-time buyers earning $50,000 to $95,000 who qualify for multiple MHC programs but cannot determine whether Smart6, Easy8, Trusty10, or MRB7 gives them the best financial outcome --- and want a side-by-side comparison of total cost, repayment triggers, and tax implications before committing to a program

- USDA or VA buyers in rural Mississippi who are planning to use zero-down financing but need to understand how flood zones, termite inspections, and property tax reclassification affect their real monthly costs beyond the mortgage payment

- Gulf Coast buyers near Biloxi, Gulfport, or Pascagoula facing triple-premium insurance costs (standard + MWUA windstorm + NFIP flood) who need to budget the true carrying cost of coastal homeownership before making an offer they cannot afford

- Military families at Keesler AFB, Columbus AFB, or Camp Shelby using VA loans who need to understand the statewide WDI inspection mandate, the Easy8 tax recapture risk for families who may relocate within 10 years, and how PCS orders interact with MHC repayment triggers

- Jackson metro buyers navigating higher millage rates, Yazoo Clay foundation risks, and a competitive market where MHC lender competence varies widely --- and who cannot afford a delayed closing from an incomplete DPA file

- Post-closing homeowners who have already purchased but have not yet filed their homestead exemption and need a step-by-step walkthrough of the documentation, the vehicle registration requirement, and the April 1 deadline before they lose hundreds of dollars in unnecessary taxes

Why Not Free Tools and Forums?

Free information on buying a home in Mississippi exists. Here is what it actually delivers:

- The MHC website gives you program descriptions, income limits, and a list of participating lenders. It does not tell you which program yields the best total financial outcome for your income level, how the Easy8 tax recapture penalty actually works, whether you can stack programs, or how to vet a participating lender's MHC experience before trusting them with your closing timeline. You get the eligibility inputs without the decision framework.

- Reddit threads (r/mississippi, r/FirstTimeHomeBuyer) contain genuine warnings about MHC programs and flood zones, but mixed with advice from people who confuse silent second mortgages with grants, who do not mention the vehicle tag requirement for homestead filing, and who posted income limits that have since been updated. Sorting current from outdated takes longer than reading a guide that already did it.

- Zillow and Rocket Mortgage estimate your monthly payment using national formulas. They do not account for Mississippi's attorney-close requirement adding $750 to $1,250 to closing costs, the flood insurance premium that can add $100 to $375 per month to your payment overnight, or the MHC programs that could eliminate your entire down payment. You get a national estimate, not a Mississippi-specific one.

- Real estate agent blogs post "5 tips for buying a home in Mississippi" articles designed to capture search traffic and generate leads. They do not explain the difference between retreat-only and repair-and-retreat termite bonds, the Class I versus Class II tax assessment that doubles your property tax if you miss a filing deadline, or the triple-premium insurance reality on the Gulf Coast. You get marketing content, not the analysis that protects your money.

This guide fills the Mississippi-specific gap --- the space between knowing how to buy a home in general and knowing how to buy one in a state where mandatory attorney closings, a rigid property tax reclassification system, six overlapping DPA programs with hidden repayment triggers, statewide termite mandates, and extreme flood and wind exposure each independently determine whether your purchase is financially sound. It is the analysis that would take a Mississippi real estate attorney, a property tax consultant, a pest control specialist, and an insurance broker to assemble --- structured as a reference you own permanently.

--- Less Than One Termite Inspection

A single WDI termite inspection in Mississippi runs $100 to $200. Missing the homestead exemption deadline costs $625 to $925 per year. Choosing the wrong MHC program --- or not knowing you qualified for one at all --- can mean leaving $6,000 to $14,000 in assistance on the table. A late-discovered flood zone adds $1,200 to $5,000 per year in mandatory insurance. Accepting a retreat-only termite bond on a home with hidden Formosan damage can leave you with repair bills in the tens of thousands.

This guide does not replace your real estate agent, your closing attorney, or your home inspector. But it gives you the MHC program comparison, the flood zone analysis framework, the termite bond evaluation criteria, the property tax reclassification walkthrough, and the transaction timeline that ensure you identify every Mississippi-specific risk and opportunity before you are contractually committed --- instead of discovering them on your first tax bill, your first insurance renewal, or your first call from a pest control company telling you the bond does not cover the damage.

If it catches a single property tax miscalculation, prevents a single unbudgeted insurance cost, or connects you with the right MHC program, it pays for itself before you have finished reading it.

30-day money-back guarantee. If the guide does not sharpen your Mississippi home buying analysis and protect your down payment, you pay nothing.

Download the free Mississippi Quick-Start Home Buying Checklist to see the step-by-step framework covering pre-approval, house hunting, closing, and post-purchase compliance. When you are ready for the full MHC program comparison, flood zone analysis, termite bond evaluation, property tax worksheets, and the complete 17-chapter guide, the full toolkit is here.

Mississippi's affordability only works if you know how to protect it. This guide makes sure you do.